Owner income$180k

Owner income$180kHow Much Financial Advisory Firm Owners Make: $180K Base Case

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180k  Net margin3.6%

Net margin3.6% Revenue for target pay$498k

Revenue for target pay$498k Business difficultyHard

Business difficultyHard

You’re planning owner pay before the firm has steady scale, so treat this as a US registered investment adviser, or RIA, planning case, not promised income The model uses a $180,000 lead advisor pay assumption, $18,000 Year 1 EBITDA, Month 7 breakeven, 17-month payback, and a five-year operating view It excludes tax advice, employee advisor benchmarks, and guaranteed distributions

Owner income$180kNet margin3.6%Revenue for target pay$498kBusiness difficultyHardWant to test your owner income number?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

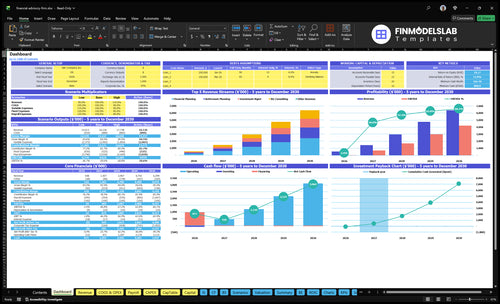

How do you check owner income in the Financial Advisory Firm financial model?

This dashboard shows revenue, margin, costs, reserves, and owner take-home assumptions; open the Financial Advisory Firm Financial Model Template.

Owner-income model highlights

- Month 7 breakeven

- 17-month payback

- $801k minimum cash

- $18k Year 1 EBITDA

- $100k launch capex

- Tests AUM and fees

- Checks hiring and CAC

- Low/base/high scenario charts

What profit margin and RIA operating costs drive owner take-home?

Owner take-home in a Financial Advisory Firm is driven more by payroll timing than by fee margin, because fixed overhead is only $8,750/month while payroll starts at $255,000 in Year 1 and rises to $775,000 by Year 5. If you’re sizing the cash need, How Much Does It Cost To Open, Start, Launch Your Financial Advisory Firm? helps frame the upfront spend, and the main swing points are client acquisition cost, service cost, and reserve policy. Service-related costs fall from 21% of revenue to 15%, but marketing climbs from $15,000 to $100,000, so cash can stay tight even as margin improves.

Main cost drivers

- $8,750 fixed overhead each month

- Rent, internet, CRM, insurance

- Legal, accounting, compliance, website upkeep

- Year 1 payroll: $255,000

Take-home margin levers

- Service costs drop from 21% to 15%

- Marketing grows from $15,000 to $100,000

- Year 5 payroll hits $775,000

- Reserve policy changes owner cash

How much can an independent financial advisory firm owner make?

An independent Financial Advisory Firm owner can model $180,000 in owner role pay, plus $18,000 of Year 1 EBITDA before reserves, taxes, debt service, and distributions; this is owner economics, not an employee wage, and it ties directly to What Is The Primary Goal Of Your Financial Advisory Firm?. Take-home rises only if recurring revenue, client retention, fee realization, and staffing leverage grow faster than overhead.

Owner Pay

- Model role pay at $180,000

- Add Year 1 EBITDA: $18,000

- Exclude taxes, debt, and reserves

- Measure distributions after cash needs

Profit Levers

- Cut direct costs from 21% to 15%

- Protect recurring client revenue

- Track client retention closely

- Set AUM scale as user input

How much revenue does a financial advisory firm need to pay the owner?

A Financial Advisory Firm needs about $498,000 of revenue in Year 1 to pay the owner $180,000, fund $75,000 of analyst payroll, cover $105,000 of fixed overhead, and spend $15,000 on marketing while still generating $18,000 EBITDA. Here’s the quick math: $393,000 of contribution needed divided by a 79% contribution margin = about $497,468.

Revenue math

- $180,000 owner pay

- $75,000 analyst payroll

- $105,000 fixed overhead

- $15,000 marketing spend

AUM rule

- Divide revenue by fee rate

- No single AUM threshold

- Fee mix changes the answer

- Use client fee rate only

If you want the AUM number, compute it from the required advisory revenue and the firm’s fee rate; there is no universal AUM threshold. One line does the job: AUM needed = required advisory revenue ÷ advisory fee rate.

Want the six financial advisory firm income drivers?

1

$225-$340Fee Capture

The hourly rate ladder from $225 to $340 sets the ceiling on revenue per engagement before overhead and reserves bite.

2

$825-$3.6KHousehold Mix

A higher-value household mix lifts revenue per client, since consulting work earns far more than planning or investment-only work.

3

M7Recurring Base

Retained clients keep revenue flowing past Month 7 breakeven, which protects owner pay when new sales slow.

4

$255K-$775KAdvisor Output

Payroll climbs from $255K to $775K, so billable output per advisor has to stay ahead of wage growth.

5

21%-15%Cost Discipline

Moving direct costs from 21% to 15% and keeping fixed overhead at $105K a year leaves more cash for the owner.

6

$15K-$100KGrowth Reserves

Marketing scales from $15K to $100K and CAC falls from $500 to $350, but distributions only happen after the $801K cash floor is covered.

Financial Advisory Firm Core Six Income Drivers

AUM, Fee Rate, and Revenue Realization

AUM, Fee Rate, and Realization

This driver sets the revenue base before expenses. For AUM pricing, use AUM × blended advisory fee rate × billing realization, where billing realization means the share of billed work you actually collect. If hourly pricing is used, Year 1 rates are $225 to $300, and Year 5 rates rise to $245 to $340.

One clean line: price only matters if it gets billed and collected. Fee compression, weak billing discipline, and low conversion all cut realized revenue, and that hits owner pay only after payroll, compliance, software, and cash reserves are covered.

Track Realized Revenue

Measure this driver by service line, client, and advisor. Track AUM, blended fee rate, billable hours, billed amount, collected cash, and the gap between booked work and cash received. If conversion slips, the firm may look busy but still miss take-home income.

- Track billed versus collected monthly

- Separate AUM and hourly revenue

- Watch fee cuts by client segment

- Bill fast, then collect fast

- Review low-conversion proposals weekly

1

Client Household Economics

Client Household Revenue Density

Client household economics is about how much revenue each household brings in and how many advisor hours it consumes. In Year 1, the mix is 70% financial planning, 60% investment management, 30% retirement planning, and 15% business consulting, with service time ranging from 3 hours for investment management to 12 hours for business consulting. More revenue per household can lift owner take-home without adding as many clients.

The catch is capacity. A high-revenue household can also require more advisor time, so revenue growth without scope control can squeeze margin and cash flow. The key inputs are household count, service mix, billable hours, minimum fees, retainers, and how tightly the firm limits scope. One clean rule: if the fee does not rise with the time load, the owner pays for it later in payroll and lost draw.

Protect Margin Per Household

Track revenue per household beside hours per household, not just total client count. Split offers into clear tiers, use minimums, and price the 12-hour consulting work above the 3-hour investment management work. That helps the firm keep high-value accounts from becoming low-margin time drains.

Build forecasts from actual service load: households served, service mix by line, billable hours, and retainer level. Then test whether each tier still supports owner pay after advisor time is covered. If the mix shifts toward more planning or consulting, tighten scope in writing so revenue grows faster than labor.

- Measure revenue per household monthly.

- Cap hours by service tier.

- Use retainers for complex work.

- Review scope before discounts.

2

Retention and Recurring Revenue Stability

Recurring Revenue Stability

When more of the book renews on its own, the owner needs fewer new clients just to hold revenue flat. Here, investment management allocation rises from 60% to 85% over five years, so recurring fees can support steadier owner distributions if clients stay and balances hold.

Market movement can change AUM-based billings, so this is not fully controllable revenue. Still, stable relationships help fund payroll, compliance, and reserve targets, while referrals reduce pressure on paid acquisition and protect cash flow.

Track Retention, Not Just New Wins

Measure client retention, recurring revenue mix, and referral share each month. Here’s the quick math: if recurring revenue holds while new-client demand eases, the owner can pay fixed costs with less sales churn and keep distributions more predictable.

Watch the inputs that drive stability: active households, AUM that stays on the book, billing realization, and the share of revenue tied to ongoing service. If retention slips, replacement-client pressure rises fast, and owner pay gets less reliable even when top-line revenue looks fine.

3

Advisor Capacity and Staffing Leverage

Advisor Capacity Leverage

Staffing is a cost first, then a growth lever. Payroll starts at $255,000 in Year 1 and rises to $775,000 by Year 5, a jump of $520,000. That means the firm needs enough new client revenue, or higher billable hours, to cover each added hire before owner distributions stay healthy.

Here’s the quick math: lead advisor and analyst pay comes first, then senior advisors, client service, marketing, and operations. If support staff frees advisor time but billed revenue does not rise fast enough, cash flow tightens and the owner’s take-home drops. One clean rule: hire when added capacity clearly pays for itself.

Track Revenue per FTE

FTE means full-time equivalent, or the payroll load per worker. Track revenue per advisor FTE, payroll as a share of revenue, and billable hours per advisor each month. Those three numbers show whether staffing is lifting margin or just adding fixed cost.

Test each hire against new revenue, not hope. If a senior advisor or service hire does not lift client capacity, close rates, or retention enough to cover the salary, delay the role. Support staff should free time for higher-value work; it only helps owner income when the new client revenue is bigger than the added payroll burden.

4

Operating Cost Discipline and Overhead

Operating Cost Discipline

When fixed overhead is this tight, the firm’s income depends on covering $8,750 per month before any owner distribution. That overhead includes $4,500 rent, $1,200 IT and CRM, $900 legal and accounting, $550 insurance, and $450 compliance, so annual fixed cost is about $105,000. If office and software spend creep up, owner pay gets squeezed fast.

Here’s the quick math: lower COGS from 7% to 5% over five years helps margin, but only if overhead stays controlled. The model says tight overhead helps the firm reach breakeven by Month 7, which means cash starts supporting salary and profit draw sooner. One line says it all: fixed cost discipline protects take-home income.

Track Overhead Before You Pay Yourself

Measure overhead as a share of monthly revenue, then review each line item against the $8,750 baseline. Track rent, software, legal/accounting, insurance, and compliance separately so software sprawl or a bigger office does not hide in one lump sum. The key inputs are client count, billable hours, realized fees, and recurring fixed costs.

- Review recurring spend every month.

- Kill unused software fast.

- Hold office cost flat.

- Protect compliance and reserve cash.

- Pay owners only after overhead.

What this estimate hides is staffing growth: if payroll rises before revenue does, distributions fall even if top-line sales look good. Keep breakeven timing on the forecast, and test whether each new tool or office commitment still works at the current client load.

5

Growth Spend and Reserve Policy

Growth Spend and Reserve Policy

This driver covers marketing spend, launch capex, and the cash reserve needed before owner draws. Marketing rises from $15,000 in Year 1 to $100,000 in Year 5, while customer acquisition cost (CAC) improves from $500 to $350; the tradeoff is lower current take-home in exchange for more future capacity and a stronger 17-month payback case.

The cash risk is real: minimum cash is $801,000 in Month 6, and launch capex totals $100,000. Pulling distributions too early can squeeze hiring, compliance, and billable growth, which cuts owner income later by slowing revenue ramp and forcing extra funding.

Reserve First, Spend Second

Track monthly cash, booked clients, realized revenue, and CAC before any draw. If CAC stays near $500 early and only improves toward $350 later, keep reserves intact until the Month 6 cash floor is covered.

Set a rule for distributions only after payroll, compliance, and planned growth spend are funded. That keeps reinvestment tied to capacity, not hope, and protects owner pay from a cash crunch.

6

Scenario objective: Compare lean solo, stable boutique, and growth-team owner income planning cases

Owner income scenarios

Owner income shifts fast here because cash must cover a $180,000 lead advisor role, $105,000 fixed overhead, and hiring. Lean solo keeps pay tighter; growth pushes more earnings into payroll and marketing.

| Scenario | Low CaseLean solo | Base CaseBase case | High CaseScale-up |

|---|---|---|---|

| Launch model | The low case assumes a lean solo setup with slower hiring and tighter marketing. | The base case models the planned operating path with the $180,000 lead advisor role and steady scale. | The high case assumes stronger revenue growth and a larger team, but most gains get reinvested. |

| Typical setup | The owner does more of the work, keeps payroll light, and waits on scale before adding staff. | It mixes the Year 1 $18,000 EBITDA start with Month 7 breakeven, $801,000 minimum cash, and measured hiring. | Payroll scales toward $775,000 by Year 5, marketing rises to $100,000, and short-term distributions stay light. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Lower owner payLean pay band | $180,000Planned pay | Higher long-term payReinvestment mode |

| Best fit | Best for founders stress-testing a service-led practice that stays small longer. | Best for a balanced service-led practice that follows the model as written. | Best for testing an aggressive growth plan with conservative cash and delayed owner payouts. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Financial Advisory Firm Porter's Five Forces Analysis

- Financial Advisory Firm BCG Matrix

- Financial Advisory Firm Business Model Canvas

- 7 Essential KPIs for a Financial Advisory Firm

- Financial Advisory Firm Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Financial Advisory Firm Profitability

- How To Run A Financial Advisory Firm: Essential Monthly Costs

- Financial Advisory Firm Startup Costs: $100K Setup Plus Runway

- Financial Advisory Firm Financial Model Template in Excel

- How To Open A Financial Advisory Firm In 8–20 Weeks

- How to Write a Financial Advisory Firm Business Plan (7 Steps)

- Financial Advisory Firm Marketing Mix

- Financial Advisory Firm Marketing Plan

- Financial Advisory Firm Business Proposal

- Financial Advisory Firm PESTEL Analysis

- Financial Advisory Firm Pitch Deck Example Editable PPTX

- Financial Advisory Firm Business SWOT Analysis

- Financial Advisory Firm Value Proposition Canvas

Frequently Asked Questions

The base case models $180,000 for the owner if they fill the lead advisor role, plus any approved distributions after reserves Year 1 EBITDA is $18,000, so extra cash is limited early Owner take-home depends on revenue scale, payroll timing, taxes, debt service, and the $801,000 minimum cash need