Owner income$145K

Owner income$145KHow Much Fire Partition Installation Owners Make on $75M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$145K  Net margin53%

Net margin53% Revenue for target pay$275K

Revenue for target pay$275K Business difficultyHard

Business difficultyHard

You’re pricing code-driven commercial work, so owner income depends on backlog, margin, overhead, and cash timing In the first-year planning case, the model shows $751M revenue, 761% gross margin, and about $437M operating profit before taxes, debt service, reserves, and owner distributions These are planning assumptions, not guaranteed earnings, tax advice, or required distributions

Owner income$145KNet margin53%Revenue for target pay$275KBusiness difficultyHardWhat owner pay can your fire partition business support?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Not guaranteed salary, tax advice, or owner distribution advice.

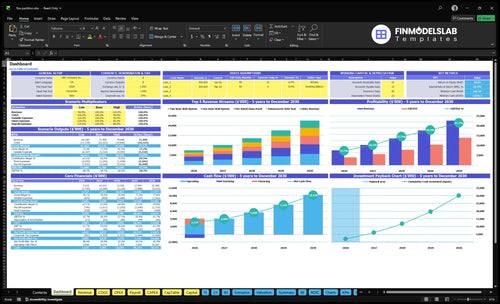

Can you check owner income in the Fire Partition Installation financial model?

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Fire Partition Installation Financial Model Template; open the model.

Owner-income model highlights

- Year 1 revenue $751M

- Gross margin 761%

- Overhead before reserves $6,734K / $437M

What profit margin does a fire partition installation business need?

Fire Partition Installation needs a big gap between gross and operating margin; in the Year 1 model, gross margin is 761%, contribution margin after 90% sales commissions and logistics is about 671%, and operating margin before taxes, reserves, debt, and distributions is about 582%. For the KPI lens, see What Are The Five KPIs For Fire Partition Installation Business?

Margin layers

- 761% gross margin in Year 1

- 671% after commissions and logistics

- 582% before taxes and debt

- Separate gross from operating margin

Margin leaks

- Underbid rated assemblies hurt fast

- Missed penetrations create rework

- Access delays raise labor hours

- Inspection failures cut owner income

How much revenue does a fire partition contractor need to pay the owner?

For Fire Partition Installation, the planning case says you need about $100M in revenue to fund owner pay, because you should size this on contribution margin, not top-line sales. The model uses a 67% margin, $5.284M of known overhead, and a $145K general manager salary before taxes, debt service, reserves, retainage exposure, and backlog gaps.

Revenue math

- Use contribution margin, not revenue.

- 67% funds overhead and owner pay.

- $5.284M comes before owner cash.

- $145K GM pay is separate.

Cash risks

- Add taxes and debt service.

- Keep reserves for retainage gaps.

- Watch backlog timing closely.

- Don't treat thin sales as pay.

Does adding crews increase fire partition contractor owner income?

Yes—adding crews can raise owner income in Fire Partition Installation, but only if utilization and quality stay high. Source volume rises from 48,700 units in Year 1 to 83,600 in Year 3 and 137,000 in Year 5, with revenue climbing from $751M to $1,360M to $2,259M. The catch is extra crews also add supervision, insurance, vehicles, tools, safety controls, working capital, and retainage risk, so owner income improves only when added gross profit beats those costs.

Income upside

- 48,700 units in Year 1

- 83,600 units in Year 3

- 137,000 units in Year 5

- Revenue scales with capacity

Cost pressure

- Supervision costs rise fast

- Insurance and vehicles add overhead

- Working capital gets tied up

- Retainage can delay cash

Want the six fire partition income drivers?

1

$7.5MAwarded Volume

More signed work lifts Year 1 revenue fast, and this model already shows $7.51M in the first operating year.

2

80%Job Margin

Keeping unit costs tight preserves gross margin, which is the biggest filter on what the owner can take home.

3

21xProject Mix

Shifting toward higher-value wall and glass work raises revenue per job because pricing runs from $45 to $950 a unit.

4

$983KOverhead Burden

Fixed rent, salaries, insurance, software, utilities, and admin costs add up fast, so every dollar of overhead cuts owner profit.

5

4xCrew Speed

Faster install cycles protect margin on the labor-heavy jobs, where direct labor ranges from $1.50 to $25.00 per unit.

6

1 moCash Discipline

Fast billing and collections matter because payback is 1 month and breakeven lands in month 2.

Fire Partition Installation Core Six Income Drivers

Awarded Contract Volume

Awarded Contract Volume

Awarded contract volume is the work you actually win and schedule, not just bid. This model starts at 48,700 units and $751M in Year 1, then climbs to 83,600 units and $1.36B in Year 3, about 72% more units and 81% more revenue. If awards slow, owner pay slows too, even when job margins still look healthy.

Track Bid-to-Award Flow

Measure bid pipeline, win rate, awarded backlog, start dates, and contract value by source: general contractors, developers, facility owners, healthcare, industrial, education, and multifamily. Here’s the quick math: steady awards keep crews loaded and overhead covered before the next start month.

- Track awards by start month.

- Split pipeline by client type.

- Watch backlog coverage weekly.

1

Job Gross Margin

Job Gross Margin

Job gross margin is what’s left after direct job costs, before overhead. In this model, Year 1 disclosed gross margin is 761%, so even a small miss in estimating cuts owner distributions fast. At $751M revenue, each margin point is about $751K, so underbidding can burn a lot of profit before overhead is even paid.

To estimate it, you need the rated assembly, wall type, penetrations, access, labor hours, and materials. Direct unit costs include $32 one-hour wall systems, $55 two-hour systems, $95 three-hour systems, $182 glass panels, and $850 joint seals. Failed inspections, rework, waste, and missed scope all turn a good bid into weaker take-home income.

Protect Margin on Every Job

Track quoted vs. actual labor hours, inspection pass rate, and change orders by assembly type. If access is tight or penetrations change after bid, reprice fast. One clean rule: if the scope shifts, the margin should shift too.

Use a job margin review before payroll and owner draws so you pay yourself from confirmed gross profit, not hoped-for profit. That keeps cash from getting trapped in rework and fixes.

- Rated assembly and wall type

- Penetrations and access limits

- Actual labor hours by crew

- Material waste and rework

- Inspection fails and punch-list hours

2

Crew Productivity

Crew Productivity

Crew productivity is the share of paid installer time that turns into installed, inspected fire partition work. With direct labor assumptions of $6, $18, $25, $150, and $950 per unit by assembly type, wasted hours push unit cost up and can erode the stated 761% gross margin.

The owner feels this in take-home pay because labor waste hits gross profit before overhead. Better inspection pass rate, fewer punch-list hours, and fewer schedule gaps turn the same crew into more billed output, while downtime, blocked access, late inspections, weak supervision, and training gaps burn cash without adding revenue.

Track Labor by Assembly Type

Measure productive installer hours and utilization every job. Utilization means paid hours that become install output, not waiting time. Then compare actual labor to the planned direct labor by assembly type, so the owner can see where the $6 to $950 per-unit assumptions are holding and where they are drifting.

Also track inspection pass rate, punch-list hours, and schedule gaps. If crews are waiting on access or rework keeps piling up, profit leaks fast and owner draws get smaller. One clean rule: every avoided idle hour protects margin and helps cash move from job profit to the owner’s pocket sooner.

3

Project Mix

Project Mix

Project mix is the split across one-hour walls, two-hour walls, three-hour systems, glass panels, and joint seals. In Year 1, revenue is $216M, $208M, $113M, $102M, and $113M; those lines total about $752M, close to the stated $751M after rounding. Mix changes price, margin, paperwork, and when cash gets collected.

High-unit-price work is not always better. More complex systems can bring more inspection burden, schedule risk, and slower collections, so owner pay can lag even when sales look strong. Better mix beats bigger tickets.

Track mix by margin and cash timing

Track each job by system type and customer segment: healthcare, industrial, multifamily, education, and facility retrofit. Measure unit price, direct labor, inspection passes, change-order rate, and days to collect. The key question is simple: which mix adds the least rework and the fastest cash?

- Rank jobs by gross margin.

- Flag slow-paying project types.

- Watch inspection and rework hours.

- Prefer cleaner payment terms.

When two jobs pay the same, choose the one with cleaner docs and faster billing. That keeps profit out of retainage and helps fund payroll, taxes, and owner draws.

4

Overhead Burden

Overhead Burden

Overhead burden is the cost stack that sits above gross profit and decides what is left for owner pay. In this model, known fixed overhead is $282K per month, or $3,384K per year, and Year 1 payroll adds $335K, including a $145K general manager and two $95K project managers.

Add $42K per month for insurance and $25K per month for certification maintenance, plus variable commissions and logistics at 90% of revenue. Gross profit is not the same as owner income, so treating it that way will overstate take-home and can make a profitable job look cash-rich when it is not.

Track burden before owner pay

Measure overhead against collected revenue, not booked work. Use these inputs: revenue, commission and logistics rate, fixed overhead, payroll, insurance, certification upkeep, and owner draw target. One clean test: if overhead plus revenue-based costs rise faster than gross profit, owner pay gets squeezed even when the backlog looks full.

- Track overhead as a monthly percent.

- Separate payroll from owner draw.

- Price for insurance and certification.

- Forecast commissions on actual revenue.

Here’s the quick math: every added dollar of revenue must cover the 90% variable burden first, then support the $282K fixed base. If the monthly run rate slips, the overhead burden per job jumps fast, and cash available for the owner drops before the income statement shows the pain.

5

Cash-Flow Discipline

Cash-Flow Discipline

Cash flow decides when profit turns into owner pay. In Year 1, the job plan needs about $149M in direct unit costs plus $3.004M in revenue-based production costs, before overhead. Even profitable installs can trap cash if retainage is held, contractor payments run slow, change orders sit disputed, or payroll hits before billing clears.

The owner’s income depends on collected cash, not accounting profit. If billed work sits in backlog or change orders are not approved, distributions lag. That means the business can show margin on paper and still keep the owner waiting for pay.

Track Cash Before You Pay Yourself

Track collections against billed backlog every week, not just month-end. Watch change-order approval rate and retainage balance, because both can block cash even after the work is done. Keep a cash buffer for payroll and materials so one slow-paying contractor does not freeze owner draws.

Use a weekly cash forecast that starts with billings, expected collections, retainage release, and payroll dates. If collections slip behind billed work, delay distributions first, not operations. That keeps the job moving and protects owner pay later.

- Measure collections vs. billed backlog.

- Approve change orders fast.

- Track retainage by job.

- Set a minimum cash buffer.

6

Compare assumption-driven fire partition owner income scenarios

Owner income scenarios

Owner income shifts with volume, product mix, and overhead. Year 1 looks tighter, Year 3 is steadier, and Year 5 shows the stronger capacity case.

| Scenario | Low CaseEarly scale | Base CaseGrowth case | High CaseMature capacity |

|---|---|---|---|

| Launch model | This is the lower-income path, with Year 1 volume and pricing as the starting point. | This is the modeled middle path, with Year 3 output and pricing as the core case. | This is the stronger earnings path, with Year 5 scale as the upside case. |

| Typical setup | Year 1 revenue is $7.510M across 48,700 units, with 76.1% gross margin and $6.734M of visible overhead before reserves, taxes, debt, and collections. | Year 3 revenue is $13.595M across 83,600 units, with 77.0% gross margin and visible overhead carrying the operation at scale. | Year 5 revenue is $22.588M across 137,000 units, with 77.8% gross margin and later-year payroll detail still needed before a final owner-income quote. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0.4M pre-reserveDownside check | $0.9M pre-reserveCore case | Final quote pendingUpside check |

| Best fit | Use this to stress-test the launch year when cash timing and overhead pressure matter most. | Use this as the main planning case for a steady growth build. | Use this to test upside once staffing, reserves, and collection timing are fully set. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Fire Partition Installation Porter's Five Forces Analysis

- Fire Partition Installation BCG Matrix

- Fire Partition Installation Business Model Canvas

- What Are The Five KPIs For Fire Partition Installation Business?

- Fire Partition Installation Business Plan Template in Pre-Written Word

- How Increase Fire Partition Installation Profits?

- What Are Operating Costs For Fire Partition Installation?

- Fire Partition Installation Startup Costs: $65K+ Opening Month

- Fire Partition Installation Financial Model Template in Excel

- How To Start A Fire Partition Installation Contractor In 8–16 Weeks

- How To Write A Business Plan For Fire Partition Installation?

- Fire Partition Installation Marketing Mix

- Fire Partition Installation Marketing Plan

- Fire Partition Installation Business Proposal

- Fire Partition Installation PESTEL Analysis

- Fire Partition Installation Pitch Deck Example Editable PPTX

- Fire Partition Installation Business SWOT Analysis

- Fire Partition Installation Value Proposition Canvas

Frequently Asked Questions

In the first-year planning case, the owner can plan around a $145K manager salary if they fill that role The model also shows about $437M operating profit before taxes, reserves, debt service, and distributions That pool is not guaranteed take-home pay because retainage, reinvestment, and cash timing come first