Owner income$185K

Owner income$185KHow Much Flood Risk Assessment Owners Make: $185K Salary To $689K EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$185K  Net margin-11% to 16%

Net margin-11% to 16% Revenue for target pay$1.28M

Revenue for target pay$1.28M Business difficultyHard

Business difficultyHard

You’re pricing expert work with high payroll, software, data, and liability costs, so owner income depends on volume and margin more than revenue alone This page uses a five-year US flood risk assessment business model with $128M to $442M revenue, -$137K to $689K EBITDA, and a modeled $185K principal hydrologist salary It is not a guaranteed salary, engineering, legal, or tax advice, or a substitute for local market research

Owner income$185KNet margin-11% to 16%Revenue for target pay$1.28MBusiness difficultyHardWant to test your owner-pay number?

Owner income calculator

Estimate monthly owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the full owner-income view?

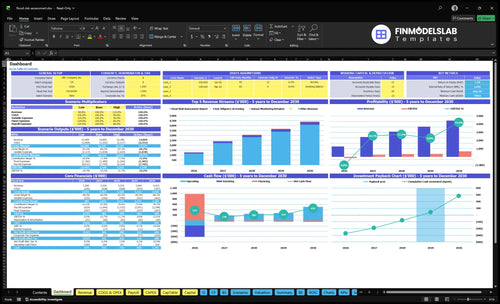

The dashboard shows income outputs, assumptions, revenue build, staffing, cost structure, owner compensation, cash flow, and scenario testing; revenue rises from $128M to $442M, EBITDA from -$137K to $689K, breakeven lands in Month 8, payback is 49 months, and minimum cash is $340K—open the Flood Risk Assessment Service Financial Model Template.

Owner-income model highlights

- Owner pay sensitivity

- Billable hours and rates

- Cash and breakeven view

Can a flood risk assessment business scale beyond the owner?

Yes. A Flood Risk Assessment Service can scale past the owner, but only if the business shifts from solo analysis to a staffed delivery model: 4 FTE and $545K payroll in Year 1 grow to 15 FTE and $1.845M payroll by Year 5, while revenue rises from $1.28M to $4.42M and EBITDA improves from -$137K to $689K. The owner stops doing most analysis and spends more time selling, managing QA, hiring, and protecting margin, because defensible reports still have to be right.

Scaling needs staff

- 4 FTE in Year 1

- 15 FTE by Year 5

- $545K payroll in Year 1

- $1.845M payroll in Year 5

Owner role changes

- Sell more, analyze less

- Run QA on every report

- Hire for GIS and technical depth

- Watch utilization risk closely

What profit margin can a flood risk assessment business earn?

If you’re pricing a Flood Risk Assessment Service, don’t use one universal margin; the model changes fast as delivery mix shifts. If you’re still building the plan, How Do I Write A Business Plan For Flood Risk Assessment Service? shows the structure, and the math here says direct costs start at 29% of revenue in Year 1, then jump to 185% in Year 5, so EBITDA moves from -$137K to $689K only if utilization and pricing hold. Minimum cash still matters, because the floor reaches $340K.

Margin pressure points

- Payroll is the biggest drag

- Data and satellite licensing adds cost

- Cloud modeling infrastructure scales with work

- Project travel cuts take-home cash

Overhead and cash risk

- $24,750 monthly fixed overhead before payroll

- External peer review protects quality

- Office lease and insurance stay fixed

- Minimum cash bottoms at $340K

How many flood risk assessments are needed to make a living?

A Flood Risk Assessment Service needs about 10 full-report equivalents per month to break even: $113K monthly revenue divided by $11,250 per full report. For setup detail, see How Do I Write A Business Plan For Flood Risk Assessment Service?; here’s the quick math: $80.2K monthly non-direct load ÷ 71% gross margin = about $113K.

Break-even volume

- $545K annual payroll load

- $297K annual fixed overhead

- $120K annual marketing spend

- 10 full reports per month

Mix risk

- $2,400 due diligence needs scale

- Screenings require much higher volume

- Retainers smooth monthly revenue

- Manage lead flow, speed, utilization, quality

Want the six income drivers?

1

$1.28M-$4.42MProject Volume

More assessments and screenings lift revenue from Year 1 to Year 5 and are the fastest path to better owner take-home.

2

$200-$310/hrPricing Mix

Higher hourly rates and a bigger share of monitoring work raise revenue per hour without the same jump in labor.

3

22.5-28.5hLabor Efficiency

More billable hours per active customer improve revenue per person and help EBITDA move from -$137K to $689K.

4

5%-9%Review Costs

Travel, site visits, and outside review take 5% to 9% of revenue, so tighter delivery keeps more gross profit.

5

$24.8K/moOverhead Load

Fixed overhead sits at about $24.8K per month, so the business needs enough volume to clear break-even by Month 8.

6

$545K-$1.845MPayroll Load

Payroll scales hard as staff grows, so utilization and delegation decide whether revenue growth turns into owner income or wage drag.

Flood Risk Assessment Service Core Six Income Drivers

Project volume

Project volume

Completed, paid assessments create the revenue base. At the stated pace of $1,067K/month and $11,250 per full report, the model needs about 95 full-report equivalents each month before client mix. One clean line: if projects slow, income drops fast while payroll, insurance, office, software, and admin costs keep running.

That makes volume a cash flow driver, not just a sales metric. Month 8 breakeven depends on lead sources, turnaround time, and receivables staying tight. Faster delivery helps revenue, but quality control has to hold or rework will eat margin and owner pay.

Track volume, not just leads

Watch utilization, backlog, receivables, and rework every week. Here’s the quick math: more completed reports raise revenue only when paid work clears billing fast and does not trigger extra review hours. If volume rises but collections slip, cash can still tighten.

Set a floor for monthly completions, then test whether screening work or report work fills the pipeline better. Track projects completed, days to deliver, and days to collect; those three numbers tell you whether volume is lifting owner income or just adding stress.

1

Average project fee and client mix

Average fee mix

When the mix leans toward full reports, owner income moves up fast. At $11,250 for a Flood Risk Assessment Report, $2,400 for Due Diligence Screening, and $900 for a monitoring cycle, the Year 1 mix of 65% / 25% / 10% nets a blended fee of about $8,003 per engagement.

If the mix shifts toward more screening and monitoring, revenue per job drops unless volume or pricing rises. Commercial, lender, municipal, and development projects can support higher fees when the scope, credentials, data needs, and review steps are heavier. This is why one high-value project can lift profit faster than several low-fee cycles.

Price by scope, not just lead count

Track realized fee by job type, not just quotes. Use the quick math: (65% × 11,250) + (25% × 2,400) + (10% × 900) = $8,002.50. That number is the cleanest check on whether the client mix is supporting owner pay or drifting toward low-margin work.

Set separate price floors for reports, screenings, and monitoring. Then watch scope creep, review time, and conversion from screening into follow-on work. If the team keeps the same overhead, a better mix improves cash flow first and gives the owner more room to pay themselves.

2

Delivery labor efficiency

Delivery Labor Efficiency

When each report or screening takes fewer analyst hours, more of the fee stays above direct labor. In this model, report time falls from 45 hours in Year 1 to 38 in Year 5, and screening time from 12 to 8, while rates rise from $250 to $310 for reports and $200 to $250 for screenings.

That matters for owner income because gross margin is expected to improve from 71% to 81.5%. The gain only holds if the team keeps technical quality intact; rework, weak documentation, or unsupported conclusions can erase the margin lift fast.

Track Hours, Rework, and Scope

Track billable hours per report, billable hours per screening, and rework rate every month. Templates, GIS workflows, data access, QA checklists, and a tight scope reduce wasted analyst time and keep delivery repeatable.

Here’s the quick math: lower hours at a higher rate means more gross profit from each job, so there’s more left for overhead, owner salary, and profit draw. The key control is simple: no extra work without a signed scope or change order.

3

Subcontractor and technical review costs

Subcontractor and Review Costs

Specialized review protects quality, but it cuts owner income if the fee does not cover it. In Year 1, 4% of revenue goes to external peer review and validation and 5% goes to project travel and site visits, so 9% of sales can leave before overhead. On a $100,000 project, that is $9,000 in direct cost.

By Year 5, those costs fall to 2% and 3%, or 5% total, but only if scopes stay tight and the work stays repeatable. Hydrologic modeling, stamped deliverables, civil engineering review, and complex site analysis should sit in direct project costs, not overhead, or gross margin and owner pay get squeezed.

Price the Review Work Up Front

Track every job at the project level: subcontractor cost, travel cost, and the share of work needing stamps or outside validation. If those costs run near 9% in Year 1, the fee needs to absorb them before the first invoice goes out.

- Track review cost as a revenue percent.

- Track travel as a revenue percent.

- Flag stamped or engineer-reviewed work.

- Use change orders when scope shifts.

Subcontractor-heavy jobs need clearer scope and higher fees. Tight billing keeps direct cost from eating gross margin, which protects cash flow and the owner’s draw.

4

Fixed overhead and compliance costs

Fixed overhead and compliance costs

Fixed overhead hits owner pay before any draw. Here, monthly overhead is $24,750, made up of office lease $12,500, professional liability insurance $3,200, GIS software $2,500, telecom $850, admin/legal $4,500, and journals/database access $1,200. These costs run even when project volume slows, so they lower operating profit fast.

Here’s the quick math: that base overhead equals about $297,000 a year before annual marketing, which starts at $120K and rises to $220K. The model also says cash reserves must cover deductibles, renewals, slow receivables, and compliance costs, with a $340K minimum cash need in Month 8. That is the real guardrail for owner income.

Track cash burn before owner pay

Measure overhead as a share of monthly revenue and compare it with gross profit after direct labor. If gross profit cannot cover $24,750 plus marketing and compliance spend, owner take-home gets delayed even when sales look healthy. One slow collections cycle can hurt more than one weak week of sales.

Build reserves for insurance deductibles, software renewals, and slow receivables, then test them against the $340K Month 8 cash need. Also watch whether marketing stays at $120K or climbs toward $220K; if lead flow does not improve, that spend acts like fixed pressure, not growth.

5

Owner role and scaling model

Principal Hydrologist Pay Mix

If the founder fills the Principal Hydrologist seat, the model includes a $185K salary. Owner income then comes from salary plus profit draw, but the cap is founder time if the owner also sells, manages QA, and reviews reports. In that setup, capacity becomes the bottleneck, so higher take-home pay only shows up when utilization stays high and rework stays low.

Hiring analysts and project managers raises delivery capacity, but payroll also rises from $545K in Year 1 to $1,845M in Year 5 in the model. That can support more revenue and later distributions, but only if the added headcount stays busy and quality control holds on every report.

Track Capacity Before You Hire

Measure utilization, billable hours, QA rework, and backlog before adding staff. If the founder’s review time is the choke point, hire to protect throughput, not just to grow headcount. The key test is simple: added payroll must lift completed, paid work enough to cover the extra cost and still leave room for owner pay.

- Watch founder review hours weekly.

- Track rework on every report.

- Forecast payroll against revenue.

- Hold hiring until capacity is clear.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income changes as the mix shifts from one-off flood reports to retainers, margins improve, and payroll scales. Early cash is tight, then operating leverage shows up by Year 3 and Year 5.

| Scenario | Low CaseCash-tight launch | Base CaseStaffed growth | High CaseMature operating leverage |

|---|---|---|---|

| Launch model | This is the lower-income launch case with tight cash and a first-year loss. | This is the modeled mid-case where the business has steady income and positive operating profit. | This is the stronger-income case with the highest operating leverage and owner upside. |

| Typical setup | Year 1 revenue is $1.28M with 71% gross margin, $120K marketing, about $545K payroll, and the principal hydrologist salary included. | Year 3 revenue reaches $3.076M with 76.5% gross margin, $180K marketing, about $1.25M payroll, and $344K EBITDA. | Year 5 revenue reaches $4.423M with 81.5% gross margin, $220K marketing, about $1.845M payroll, and $689K EBITDA. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | EBITDA -$137KLaunch risk | EBITDA $344KCore case | EBITDA $689KUpside scale |

| Best fit | Use this to stress-test a slow start with minimum cash near $340K and breakeven in Month 8. | Use this as the steady operating case once retainers grow and the team is fully staffed. | Use this to test the upside if repeat work and retainers keep growing without margin erosion. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or owner distributions.

Related Products

- Flood Risk Assessment Service Porter's Five Forces Analysis

- Flood Risk Assessment Service BCG Matrix

- Flood Risk Assessment Service Business Model Canvas

- What Are The 5 Core KPIs For Flood Risk Assessment Service Business?

- Flood Risk Assessment Service Business Plan Template in Pre-Written Word

- How Increase Flood Risk Assessment Service Profits?

- What Are Operating Costs For Flood Risk Assessment Service?

- Flood Risk Assessment Service Startup Costs: $420k CAPEX Plan

- Flood Risk Assessment Service Financial Model Template in Excel

- How To Open A Flood Risk Assessment Service In 8 To 16 Weeks

- How Do I Write A Business Plan For Flood Risk Assessment Service?

- Flood Risk Assessment Service Marketing Mix

- Flood Risk Assessment Service Marketing Plan

- Flood Risk Assessment Service Business Proposal

- Flood Risk Assessment Service PESTEL Analysis

- Flood Risk Assessment Pitch Deck Example Editable PPTX

- Flood Risk Assessment Service Business SWOT Analysis

- Flood Risk Assessment Service Value Proposition Canvas

Frequently Asked Questions

The model supports a salary-plus-profit view The principal hydrologist role is budgeted at $185K, but Year 1 EBITDA is -$137K, so distributions are not safe early By Year 5, EBITDA reaches $689K before taxes, reserves, debt service, and reinvestment, creating room for owner distributions if cash is stable