Owner income$145K

Owner income$145KFluorescent Lamp Recycling Owner Income: $145K Pay And 9-Month Breakeven

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$145K  Net margin-19.6% to 38.7%

Net margin-19.6% to 38.7% Revenue for target pay$671K

Revenue for target pay$671K Business difficultyHard

Business difficultyHard

You’re planning owner pay in a compliance-heavy recycling route business, so revenue is not the same as cash you can take home This model separates $813K in Year 1 revenue, -$159K Year 1 EBITDA, the $145K CEO payroll assumption, reserves, fixed overhead, and later-stage profit potential

Owner income$145KNet margin-19.6% to 38.7%Revenue for target pay$671KBusiness difficultyHardWant to test your fluorescent lamp recycling owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Fluorescent Lamp Recycling Service model?

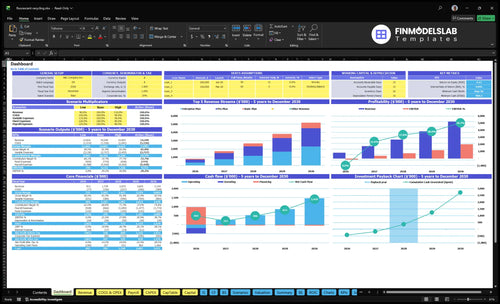

The Fluorescent Lamp Recycling Service Financial Model Template dashboard shows owner income, revenue build-up, costs, cash runway, and breakeven—open it.

Owner-income model highlights

- Owner take-home output

- Revenue, EBITDA, margin

- Pricing, CAC, runway

Is a fluorescent lamp recycling service profitable for an owner-operator?

Yes, Fluorescent Lamp Recycling Service can be profitable in the model, but not right away. The numbers point to month 9 EBITDA breakeven, a 32-month payback, and a $460K minimum cash need, so early strain is real. Owner-operated routes can save driver labor, but the provided plan still assumes a scaled team, including a $145K CEO role.

Why it can work

- Recurring fees support steady revenue.

- Route density improves labor efficiency.

- Compliance proof supports customer trust.

- Owner-operator routes can trim labor cost.

What can break it

- Poor documentation raises operating risk.

- Weak route density hurts margins fast.

- Rejected material can slow cash flow.

- Insurance gaps and weak reserves add danger.

How much does a fluorescent lamp recycling service owner make?

A Fluorescent Lamp Recycling Service owner is modeled to make $145K per year in pre-tax owner-operator pay through the Chief Executive Officer role; business profit is separate, as covered in What Are Operating Costs For Fluorescent Lamp Recycling Service?. EBITDA moves from -$159K in Year 1 to $2.009M in Year 5, so early cash is tight before scale improves.

Owner Pay

- $145K modeled annual pre-tax pay

- Paid through the CEO role

- Separate from business profit

- Not a guaranteed distribution

Profit Ramp

- Revenue grows from $813K to $5.193M

- EBITDA: -$159K in Year 1

- EBITDA: $376K in Year 2

- EBITDA: $743K, $1.183M, $2.009M in Years 3–5

What is the fluorescent lamp recycling profit margin?

The Fluorescent Lamp Recycling Service is modeled at a 805% gross margin in Year 1 and 845% in Year 5, but that’s before payroll, marketing, rent, software, insurance, admin, and compliance monitoring; see What Are Operating Costs For Fluorescent Lamp Recycling Service?. EBITDA margin is the tighter read, moving from about -196% in Year 1 to 387% in Year 5, and owner cash flow can still come down after taxes, capex, debt service, and reserve needs.

Gross margin view

- 805% in Year 1

- 845% in Year 5

- Uses container and partner fees only

- Excludes overhead and staffing

Cash profit view

- -196% EBITDA in Year 1

- 387% EBITDA in Year 5

- Payroll and marketing cut profit

- Owner draws can be lower

Want to see what drives fluorescent lamp recycling income?

1

$813K-$5.19MCommercial Volume

More recurring accounts push revenue from Year 1 to Year 5, and that sets the ceiling for owner take-home.

2

$250-$2.65KPlan Pricing

Higher monthly plan pricing lifts revenue without adding cost at the same pace, so small price gains flow through fast.

3

9 moRoute Density

Denser routes cut travel time and stop cost, which helps the model reach breakeven by Month 9.

4

80.5%-84.5%Processing Cost

Lower container and recycling fees protect gross margin, so take-home improves when downstream costs stay tight.

5

$440K-$1.37MLabor Mix

Payroll climbs fast as headcount scales, so staffing mix has a big effect on EBITDA and cash burn.

6

$2.5K/moCompliance Burden

Regulatory monitoring adds fixed drag each month, and any creep here comes straight out of owner profit.

Fluorescent Lamp Recycling Service Core Six Income Drivers

Recurring commercial account volume

Recurring Commercial Accounts

Recurring account volume is the base of owner pay because it turns one-off jobs into steady monthly cash. In this model, active accounts rise from about 88 in Year 1 to about 316 in Year 5, with monthly plans at $250, $750, and $2,200. Offices, schools, warehouses, hospitals, retailers, and facility managers matter because low churn and fast onboarding keep revenue stable enough to support a consistent draw.

What this estimate hides is timing risk. If new accounts take too long to activate, or if retention slips, monthly revenue gets uneven and the owner sees delayed pay. The key inputs are active accounts, plan mix, retention rate, and onboarding speed. One clean rule: more live recurring accounts usually means more reliable take-home income.

Track Live Accounts, Not Just Leads

Measure how many customers are actually billed each month, then break that by plan. A small base of Enterprise accounts can matter more than many low-value accounts, but only if they renew. Track monthly churn, days to first pickup, and the share of accounts still active after 90 days so you can see whether growth is real or just churn replacement.

- Count active accounts by plan.

- Watch onboarding days to go-live.

- Track monthly churn and renewals.

- Test pricing by customer type.

- Forecast owner draw from live accounts.

1

Pricing and average revenue per pickup

Per-Pickup Pricing

Monthly account pricing sets revenue before any route or processing cost is paid. The owner’s cash flow depends on average revenue per pickup holding up after per-lamp charges, container fees, minimum pickup fees, and documentation fees are applied.

The model’s weighted revenue per account per month rises from $76,750 in Year 1 to $136,900 in Year 5 as Enterprise mix grows from 15% to 35%. That helps margin, but weak service-level pricing can still crush owner pay if smaller accounts get underbilled.

Price Every Stop Properly

Track revenue by account type and pickup type, not just total monthly sales. Compare average revenue per pickup to route labor, recycling, and compliance cost, then reprice accounts that rely on too many low-value stops.

- Separate lamp, container, and doc fees.

- Test minimums by service level.

- Push Enterprise mix higher.

- Watch discounts by account.

One-line test: if a pickup does not cover handling, documentation, and transport, it is not priced right. Better pricing shows up fast in gross margin and in the owner’s monthly draw.

2

Route density and pickup efficiency

Route Density

Route density is how many paying accounts and pickups one route can cover in a day. In this model, the margin lift comes from partner recycling and logistics fees moving from 100% of revenue in Year 1 to 80% in Year 5. Fewer miles, fewer empty returns, and fuller trucks mean each pickup costs less to serve.

The key inputs are accounts per route, pickup frequency, route miles, stop time, and vehicle fill rate. Scattered customers can make revenue look solid but still leave the owner with weak take-home pay after fuel, labor, and recycler charges.

Batch More Pickups

Track revenue per route, stops per day, miles per pickup, and truck utilization. Here’s the quick math: when the same route serves more clustered accounts, logistics cost falls as a share of revenue, and more cash stays after payroll and compliance. If the fee line stays near 100% of revenue, the route is burning margin instead of creating it.

- Group stops by ZIP code.

- Set minimum route density.

- Batch pickups on fixed days.

- Price sparse routes higher.

- Review miles per dollar monthly.

3

Downstream processing and recycler costs

Downstream recycling cost control

Downstream processing is the cost to sort, package, document, and move used fluorescent lamps through certified recyclers. It hits gross margin first, so owner pay only grows when monthly fees stay ahead of direct recycler and logistics costs. On $100,000 of revenue, a 20-point drop in certified container cost is a $20,000 swing before overhead.

The key inputs are lamp type mix, packaging rules, documentation load, vendor minimums, and rejected-material risk. In the model, certified container procurement falls from 95% to 75% of revenue, and partner recycling and logistics fees fall from 100% to 80% of vendor minimums. That gap is what protects owner income.

Price from true processing costs

Build each quote from the bottom up: expected lamp mix, pickup frequency, packaging needs, and documentation time. Then test every vendor’s minimums against route volume, because a small account with odd lamp types can wipe out margin fast. Track cost per lamp, rejected loads, and certificate time.

Do not use weak handling or skipped compliance as a savings lever. Verify local rules and vendor specs before pricing accounts, and bake rework or rejection risk into the fee. If downstream costs rise faster than the monthly charge, gross margin shrinks and the owner’s draw gets squeezed.

4

Labor model and owner involvement

Owner Labor vs. Payroll

If the owner runs sales, dispatch, or admin work themselves, short-term take-home can look better because hired labor gets replaced. But that is owner labor, not pure profit. In year 1, the model already includes $145K CEO pay, $90K operations manager pay, $75K compliance specialist pay, and 2 sales executives at $65K each, or $440K before later support staff.

As the team grows, drivers, admin support, and sales staff help scale accounts and pickups, but they also cut distributable cash. The key question is not “Can the owner do more?” It’s “Does the extra labor create more margin than it costs?” If the owner replaces a paid role, cash flow improves; if they just add staff faster than revenue grows, owner pay gets squeezed.

Track Role Cost per Account

Measure fully loaded payroll by function, then tie it to active accounts, pickups, and sales close rate. Here’s the quick check: if one hired role can be covered by the owner, compare that saved salary to the value of the owner’s time and the risk of slower sales or weaker compliance.

- Track payroll by role monthly

- Separate owner draw from labor

- Test hires against account growth

- Watch admin backlog and pickup delays

- Keep compliance work fully covered

5

Compliance, insurance, and reserves

Compliance, insurance, and reserves

This driver is pure cash drag on owner pay. The model assumes $25K per month for legal and regulatory compliance monitoring plus $12K per month for professional liability insurance, so $37K per month or $444K per year leaves the business before any owner distribution. Add the $460K minimum cash need in Month 8, and reserve planning becomes a direct limit on what the owner can safely take out.

What this estimate hides is the cost of documentation, training, storage practices, permits where applicable, rejected loads, and claims. Those costs rise fast if onboarding slips, records are incomplete, or loads get turned back. This is a planning input to verify locally, not legal advice, but the income effect is clear: more compliance spend and bigger reserves mean less free cash for draws, even when revenue is growing.

Build the reserve before you raise owner draws

Track compliance spend as a fixed monthly line and watch it against active account count, since more sites usually mean more records, training, and claim exposure. Here’s the quick math: $37K/month in compliance and insurance already consumes cash that could have gone to the owner. If claims or rejected loads spike, distributions should slow first, not last.

- Fund the $460K Month 8 reserve

- Review permits and storage logs monthly

- Track rejected loads and claim costs

- Train staff before account growth

Use a simple trigger: if reserve coverage drops below the Month 8 need, hold owner draws until cash rebuilds. That keeps compliance from turning a strong revenue month into a weak personal payout.

6

Compare low, base, and high fluorescent lamp recycling income scenarios

Owner income scenarios

Owner income rises as revenue scales, but early years keep cash tight because fixed payroll and compliance costs come first. Higher-case income depends on how much profit stays after reserves and reinvestment.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | Owner income stays at salary only in the launch year because Year 1 revenue is $813K, EBITDA is -$159K, and breakeven lands in Month 9. | Owner income is still salary-led at scale, with Year 3 revenue at $2.67M and EBITDA at $743K. | Owner income turns more attractive in Year 5, when revenue reaches $5.193M and EBITDA hits $2.009M. |

| Typical setup | A new launch is still absorbing compliance, lease, payroll, and software costs, so profits are thin and distributions are off the table. | The business has enough scale to cover fixed costs and hold a $145K owner salary, but most cash still supports growth and compliance. | The business is larger, cash generation is stronger, and the owner can keep $145K payroll plus possible distributions after reserves, taxes, and reinvestment, with more compliance to manage. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary onlyLow Case | Salary onlyBase Case | Salary plus distributionsHigh Case |

| Best fit | Use this to stress-test launch cash and regulatory load. | Use this as the main operating plan for steady growth. | Use this to test upside if larger accounts scale and cash stays disciplined. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Fluorescent Lamp Recycling Service Porter's Five Forces Analysis

- Fluorescent Lamp Recycling Service BCG Matrix

- Fluorescent Lamp Recycling Service Business Model Canvas

- What 5 KPI Metrics For Fluorescent Lamp Recycling Service Business?

- Fluorescent Lamp Recycling Service Business Plan Template in Pre-Written Word

- How Increase Fluorescent Lamp Recycling Service Profits?

- What Are Operating Costs For Fluorescent Lamp Recycling Service?

- Fluorescent Lamp Recycling Startup Costs: $460K Cash Need

- Fluorescent Lamp Recycling Service Financial Model Template in Excel

- How To Open A US Fluorescent Lamp Recycling Service In 90–180 Days

- How To Write A Business Plan For Fluorescent Lamp Recycling Service?

- Fluorescent Lamp Recycling Service Marketing Mix

- Fluorescent Lamp Recycling Service Marketing Plan

- Fluorescent Lamp Recycling Service Business Proposal

- Fluorescent Lamp Recycling Service PESTEL Analysis

- Fluorescent Lamp Recycling Service Pitch Deck Example Editable PPTX

- Fluorescent Lamp Recycling Service Business SWOT Analysis

- Fluorescent Lamp Recycling Service Value Proposition Canvas

Frequently Asked Questions

The researched model carries $145K in annual pre-tax owner-operator pay through the Chief Executive Officer role That is payroll, not a guaranteed distribution Business EBITDA is -$159K in Year 1, then reaches $376K in Year 2 and $2009M in Year 5 if the revenue, cost, and staffing assumptions hold