Owner income$636k–$3.86M

Owner income$636k–$3.86MHow Much Footwear Manufacturing Owners Can Make From $187M Sales

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$636k–$3.86M  Net margin34%–61%

Net margin34%–61% Revenue for target pay$1.87M

Revenue for target pay$1.87M Business difficultyHard

Business difficultyHard

A footwear manufacturing owner’s income is best modeled from sales volume, gross margin, fixed costs, working capital, and the owner’s role Using the researched assumptions, the first year shows 4,600 pairs sold, $187M in revenue, an 860% gross margin, and about $133M in cash before owner pay, taxes, debt service, inventory buildup, and reserves By the fifth year, the forecast reaches 14,300 pairs, $634M in sales, and about $515M before those same deductions Actual take-home should be lower if the business keeps cash for inventory, equipment, payroll, and growth

Owner income$636k–$3.86MNet margin34%–61%Revenue for target pay$1.87MBusiness difficultyHardWant to test your own shoe factory pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Not guaranteed salary, tax advice, or owner distribution advice.

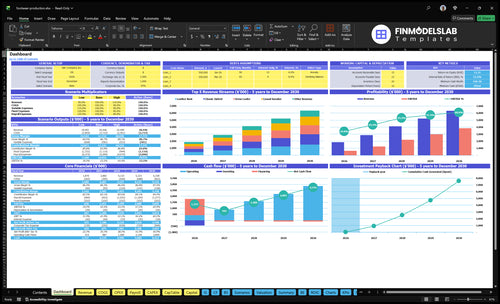

Need a footwear manufacturing financial model to check owner income?

Dashboard shows assumptions, product revenue, gross margin, fixed costs, and owner pay capacity; open the Footwear Manufacturing Financial Model Template for scenario testing.

Owner-income model highlights

- $187M to $634M revenue

- $210,000 fixed costs

- Owner cash before taxes

How does scaling a footwear manufacturing business change the owner’s role?

The owner shifts from hands-on production and selling to managing volume, cash, and quality. In Year 1, planned output is 4,600 pairs; by Year 5, it reaches 14,300 pairs, while fixed expenses stay at $210,000 a year. Here’s the quick math: fixed expense per planned pair drops from about $46 to about $15, so scaling helps only if sold units rise faster than overhead, payroll, working capital, and quality losses.

Role shift

- Move from making pairs to managing output

- Spend more time on purchasing

- Watch quality control every batch

- Handle account management and sales

Scaling risks

- Inventory can build up fast

- Receivables can strain cash flow

- Equipment deposits tie up cash

- Large wholesale orders raise concentration risk

How does gross margin change footwear manufacturing owner income?

Gross margin drives owner income in Footwear Manufacturing because every pair repeats the same cost load. For launch-cost context, see What Is The Estimated Cost To Open And Launch Your Footwear Manufacturing Business? The model’s listed 860% gross margin, plus $224,800 in unit COGS and $37,400 in revenue-based manufacturing costs, means every $5 extra cost across 4,600 pairs cuts cash by $23,000 before taxes and reserves.

Per-pair cost

- $34 Casual Sneaker cost per pair

- $66 Leather Boot cost per pair

- Leather, textiles, soles, components

- Direct labor, scrap, rework, freight prep

Cash swing

- 4,600 pairs repeat the cost move

- $5 extra cost cuts $23,000

- That hit lands before taxes

- That hit lands before reserves

How should you pay yourself as a footwear manufacturing business owner?

Pay yourself with a planned salary for the work you do, then use draws/distributions only if cash still stays positive after payroll, overhead, materials, taxes, and reserves. In Footwear Manufacturing, Year 1 modeled cash before owner pay is $133M, but inventory, equipment, receivables, and taxes can cut take-home fast. Keep retained earnings inside the business when you need cash for growth or a cushion.

Owner pay basics

- Salary pays for work performed.

- Draws pull from available cash.

- Distributions share profits out.

- Retained earnings stay in the business.

Cash test

- Set one target owner-pay amount.

- Check cash after payroll first.

- Then test overhead and materials.

- Hold reserves before taking more out.

Want the six main income drivers?

1

4.6K-14.3KUnit Volume

Output rises from 4,600 pairs in Year 1 to 14,300 in Year 5, and that scale is what spreads fixed costs and drives owner profit.

2

$407-$443Price Mix

Weighted ASP moves from about $407 in Year 1 to about $443 in Year 5, so a better mix lifts take-home on every pair sold.

3

$49Unit Cost

Year 1 direct materials and labor run about $49 per pair, so even small savings here drop straight to profit.

4

88%Yield

Keeping scrap low protects the near-88% gross margin, because waste and rework cut cash fast.

5

$210KFixed Overhead

The model carries about $210K a year in fixed factory costs, so weak utilization can erase a lot of margin.

6

$955KCash Reserve

Minimum cash bottoms out around $955K in Month 2, so inventory and reserves can slow the path to take-home pay.

Footwear Manufacturing Core Six Income Drivers

Production Volume And Capacity Utilization

Production Volume And Capacity Utilization

Capacity utilization is how much of the plant’s practical output turns into sellable pairs. In footwear, that matters because $210,000 of annual fixed costs still get paid whether you sell 626 pairs or 4,600 pairs. More volume spreads rent, insurance, software, accounting, and website costs across more units, so owner profit rises faster than output.

Here’s the quick math: fixed cost per pair is about $45.65 at 4,600 pairs, then drops to about $14.69 at 14,300 pairs. The catch is inventory risk. If production runs ahead of sell-through, cash gets tied up in unsold shoes, and owner draws can get delayed even when the factory looks busy.

Track Sell-Through, Not Just Output

Measure pairs produced, pairs sold, and sell-through rate each month. A high run rate only helps if finished pairs leave the warehouse and turn into cash. For this model, the key input list is simple: planned annual pairs, actual pairs sold, fixed overhead, and ending inventory. That tells you whether volume is lifting take-home pay or just building stock.

- Compare plan vs actual pairs

- Watch finished-goods inventory

- Freeze runs when sell-through slips

If demand is uneven, start smaller and scale only after orders hold. That protects cash, keeps fixed cost per pair moving down, and reduces the odds that strong production masks weak owner income.

1

Average Selling Price And Channel Mix

Average Selling Price and Channel Mix

Average selling price (ASP) is the average dollars earned per pair after the mix of wholesale and direct sales. In this model, ASP is $40652 in Year 1 and $44322 in Year 5. That only helps owner pay if the higher direct price beats the extra costs from platform fees, marketing, fulfillment, returns, and brand spend.

Here’s the quick math: variable selling costs are 35% of Year 1 revenue and fall to 25% by Year 5, so each $100 of revenue keeps $65 first, then $75. Private label can bring a lower selling price, but it may cut marketing risk and cash burn, which can protect take-home income even at a lower ASP.

Track ASP by Channel Weekly

Measure ASP separately for wholesale and direct, then compare it with selling costs, not just revenue. The owner should track units by channel, price per pair, platform fees, ad spend, fulfillment, returns, and brand spend. If direct sales lift ASP but push variable selling costs above the 35% to 25% range, profit and draw can shrink fast.

- Split price by channel.

- Track selling cost per pair.

- Watch return rates monthly.

- Test private label pricing.

Use channel mix to forecast cash, not just revenue. A bigger direct mix can lift price, but only if the extra margin covers the added fulfillment and marketing load. If wholesale volume steadies cash and direct raises margin later, blend both so owner pay stays predictable while the model scales.

2

Material And Direct Labor Cost Per Pair

Pair Cost Control

This driver is the all-in cost to make one pair: materials, soles, uppers, packaging, shipping prep, and direct labor. In Year 1, unit costs are $54 for Classic Oxford, $66 for Leather Boot, $34 for Casual Sneaker, $46 for Hiking Boot, and $50 for Dress Loafer. On 4,600 pairs, every $10 increase burns $46,000 of cash before taxes, reserves, and owner distributions.

Tighten Unit Cost

Track actual cost per style against the budgeted unit cost, plus labor minutes, scrap, and vendor pricing. If a pair runs even $2 over plan, that is $9,200 less cash on 4,600 pairs, which cuts gross margin and leaves less profit for owner pay.

3

Production Efficiency, Defects, And Rework

Production Defects and Rework

When yield slips, the owner pays twice: once in scrap and again in extra labor. This driver covers wasted leather, bad cuts, stitching rework, assembly delays, chargebacks, and returns. In the model, quality control is 0.3% of revenue, or $5,610 in Year 1, so the base case assumes defects stay tight enough to protect margin and cash.

Yield, or good pairs out of pairs started, is the key metric. If defect rates rise, labor minutes go up, wholesale shipments slow, and replacement inventory ties up cash. That can cut revenue quality and shrink owner pay even when total pairs produced looks fine.

Track yield before it hits cash

Measure the shop where the loss starts, not just where it shows up. Use a weekly defect log and tie it to each product line so you can see which step is breaking first.

- Yield by line

- Rework hours per pair

- Returns and chargebacks

- Late-order credits

Set a rework limit and review it with staffing and schedule. If one line starts missing ship dates, the fix is usually tighter cut control, better stitching checks, or slower release, because replacement inventory and late orders can delay owner distributions.

4

Fixed Factory Overhead And Operating Expenses

Fixed Factory Overhead

Fixed factory overhead is the monthly spend that does not change with pairs sold: $17,500 for rent, insurance, accounting and legal, software, office supplies, and website hosting. That is $210,000 a year before owner pay. Here’s the quick math: at 4,600 pairs, overhead is about $45.65 per pair; at 14,300 pairs, it falls to about $14.69. More pairs can raise take-home income if fixed spend stays flat.

Keep Overhead Flat Until Sales Prove Out

Track overhead monthly and tie new spend to sold pairs, not production hopes. Set a trigger before adding a supervisor, machine, or extra space, because each fixed dollar needs more volume to protect owner cash. One clean rule: keep the $17,500 base stable until pair sales justify the jump. If sales miss plan, overhead hits profit first and delays distributions.

Put every fixed cost in a simple forecast with pairs sold, then update it each month. That shows when operating leverage improves, meaning more sales are spread over the same fixed costs, and when it stalls. The owner should know overhead per pair at the current run rate, because a strong-looking factory can still be cash poor if fixed costs rise faster than sales.

5

Working Capital, Inventory, Receivables, And Reserves

Working Capital and Cash Timing

Working capital is the cash trapped between paying for leather, soles, labor, freight, and deposits, and collecting money from buyers. In footwear, that also includes minimum order quantities, finished goods, wholesale receivables, equipment deposits, and debt service. Profit can look solid while owner pay stays thin if cash sits in inventory or unpaid invoices.

That matters here because the model leaves out taxes, debt service, inventory buildup, and reserves, so $133M Year 1 cash is not the same as take-home pay. A profitable wholesale order can still delay distributions if the customer pays after production costs are already out the door. Profit on paper does not fund payroll.

Protect Owner Pay from Cash Gaps

Track the cash conversion cycle the gap between paying suppliers and collecting from customers. Measure inventory on hand, open purchase orders, wholesale payment terms, and cash reserves by product line. If finished pairs are building faster than cash comes back, owner draws should wait.

- Inventory days on hand

- Wholesale receivable days

- Supplier deposit terms

- Debt service due dates

Use smaller production runs, ask for deposits on large orders, and match leather and sole buys to confirmed demand. If a line has strong margins but slow sell-through, it can still starve the owner of cash. The fix is not just higher sales; it is faster cash recovery.

6

Compare lean, base, and high footwear manufacturing income scenarios

Owner income scenarios

Income shifts with pairs sold, price, and fixed overhead. Early years are tied to setup load, while later years show more cash before owner pay as volume scales.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path, anchored to Year 1 output and pricing. | This is the modeled middle path, anchored to Year 3 operating output. | This is the stronger earnings path, anchored to Year 5 scale and pricing. |

| Typical setup | Year 1 volume is 4,600 pairs, revenue is $187M, gross margin is 860%, known fixed costs are $210,000, and modeled cash before owner pay and exclusions is $133M. | Year 3 volume is 9,700 pairs, revenue is $413M, gross margin is 866%, and modeled cash before exclusions is $324M. | Year 5 volume is 14,300 pairs, revenue is $634M, gross margin is 870%, and modeled cash before exclusions is $515M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $133M pre-owner-pay cashLow cash band | $324M pre-owner-pay cashBase cash band | $515M pre-owner-pay cashHigh cash band |

| Best fit | Use this to stress-test the model if volume stays near Year 1 levels. | Use this as the mid-case planning number if the business tracks Year 3 output. | Use this to test upside if Year 5 volume, price, and cash generation hold. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; taxes, debt, working capital, reserves, and reinvestment are not included.

Related Products

- Footwear Manufacturing Porter's Five Forces Analysis

- Footwear Manufacturing BCG Matrix

- Footwear Manufacturing Business Model Canvas

- 7 Essential KPIs for Footwear Manufacturing Success

- Footwear Manufacturing Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Footwear Manufacturing Profitability

- How to Manage Monthly Running Costs for Footwear Manufacturing

- Footwear Manufacturing Startup Costs for a 4,600-Pair Launch

- Footwear Manufacturing Financial Model Template in Excel

- How To Open A Footwear Manufacturing Business In 6 To 12 Months

- How to Write a Footwear Manufacturing Business Plan in 7 Steps

- Footwear Manufacturing Marketing Mix

- Footwear Manufacturing Marketing Plan

- Footwear Manufacturing Business Proposal

- Footwear Manufacturing PESTEL Analysis

- Footwear Manufacturing Pitch Deck Example Editable PPTX

- Footwear Manufacturing Business SWOT Analysis

- Footwear Manufacturing Value Proposition Canvas

Frequently Asked Questions

Under the researched first-year assumptions, the business shows about $133M in modeled cash before owner pay, taxes, debt service, inventory buildup, and reserves That comes from 4,600 pairs, $187M in revenue, and an 860% gross margin Actual owner take-home depends on how much cash stays in the company