Owner income$0-$1.3M

Owner income$0-$1.3MHow Much Can a Foreign Trade Zone Owner Make by Year 5?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0-$1.3M  Net margin23%-27%

Net margin23%-27% Revenue for target pay$405k/mo

Revenue for target pay$405k/mo Business difficultyHard

Business difficultyHard

A foreign trade zone operation owner should not expect reliable distributions during the early ramp in this model EBITDA is negative in Year 1 at -$1363M and Year 2 at -$802k, then turns positive at $12M in Year 3 The planned monthly zone fees total $405k across six zones, but owner take-home depends on payroll, facility costs, compliance systems, reserves, and financing If the owner fills the modeled Operations Director role, the salary budget is $180k per year, but that is payroll, not business profit distribution

Owner income$0-$1.3MNet margin23%-27%Revenue for target pay$405k/moBusiness difficultyHardWhat would your FTZ operation pay you?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Exclude importer duty savings unless billed as operator revenue.

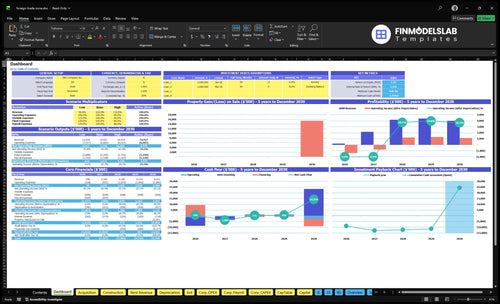

How do you check owner income in the five-year FTZ model?

The screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Foreign Trade Zone Operation Financial Model Template. It’s a planning tool, not guaranteed earnings.

Owner-income model highlights

- Month 25 breakeven

- Month 26 cash: -$3.459M

- EBITDA moves negative to positive

- Payback at 60 months

How does a foreign trade zone operation make money?

A Foreign Trade Zone Operation makes money by charging recurring zone administration and facility fees, plus activation, onboarding, storage, handling, staging, labeling, consulting, and logistics service fees. In the modeled case, those fee lines total $405k a month, made up of $85k, $45k, $110k, $60k, $70k, and $35k. The duty deferral benefit usually belongs to the importer, so the operator only captures it if it is built into stated service fees; rented sites also hurt margin because they add $47k a month.

Revenue streams

- Recurring admin and facility fees

- Activation and onboarding fees

- Storage and handling charges

- Labeling, staging, consulting, logistics

Margin drivers

- $405k modeled monthly fees

- $47k added rent cost

- Importer keeps duty savings

- Operator wins on service fees

Can a foreign trade zone operation scale owner income?

Yes, but not right away: a Foreign Trade Zone Operation can scale owner income only after it absorbs more payroll, systems, facility commitments, and compliance work. Here’s the quick math: zones start across Month 1, 3, 6, 13, 17, and 21, with construction lasting 5 to 12 months, so take-home gains lag buildout. EBITDA peaks at $1304M in Year 4 then falls to $1135M in Year 5, which shows scale can compress earnings if revenue does not outpace overhead.

Scale adds cost

- Month 1 to 21 launch timing

- 5 to 12 months to build

- Payroll rises before cash does

- Compliance adds ongoing workload

Where income improves

- Year 5 staffing grows fast

- 2 leasing managers by Year 5

- 3 facility supervisors by Year 5

- 2 admin coordinators by Year 5

How many clients does a foreign trade zone operation need to pay the owner?

Foreign Trade Zone Operation needs about 3 average-fee active zones to cover ongoing overhead, but owner pay is not reliable until Month 25 breakeven and the cash trough is handled; see How To Write A Business Plan To Launch Foreign Trade Zone Operation? for the plan structure.

Quick math

- $675k/month average planned zone fee

- 3 zones produce about $2.025M/month

- Fixed load is about $1.689M/month

- Breakeven lands in Month 25

Owner-pay guardrails

- Cover $54k fixed overhead first

- Cover $47k rented-zone cost first

- Cover about $679k Year 5 payroll first

- Do not ignore the $3,459M cash trough

Want the six drivers that move FTZ owner income?

1

$405K/moTenant Base

This is the total monthly fee base across all six zones, so occupancy is the fastest path to owner cash.

2

$35K-$110KAdmin Fees

The per-zone fee band sets pricing power, and every step up drops straight to margin before fixed costs.

3

6 zonesThroughput

More inventory movement and customs work lift billable activity, so the same staff can produce more income.

4

3/3 mixSpace Mix

The owned-versus-rented split changes cash burn, because rented zones add $47K a month in cost.

5

$515K-$815KLabor Efficiency

Payroll rises from Year 1 to Year 5, so staffing discipline matters before EBITDA turns positive.

6

-$3.5MReserve Discipline

The model bottoms out at Month 26, so weak reserves can block owner distributions before breakeven in Month 25.

Foreign Trade Zone Operation Core Six Income Drivers

Active Zone Users and Tenants

Active Tenant Density

More active zone users mean the same compliance team, security, and planning work gets spread across a bigger recurring fee base. That matters here because six zones enter the model at Month 1, 3, 6, 13, 17, and 21; a $110k monthly zone with steady activity can out-earn several low-scope accounts. Idle tenants still consume setup time, so booked revenue is not the same as earned margin.

The owner’s take-home income improves when tenant density lifts EBITDA after breakeven in Month 25. Here’s the quick math: more active sites raise recurring fees without adding the same amount of compliance overhead, while inactive sites can leave admin and facility planning costs in place. Idle leases hurt twice: they use staff time and delay cash that could fund distributions.

Price for Activity

Track active tenants, monthly fee per zone, onboarding days, and compliance hours per account. Use those inputs to test whether one high-activity zone is better than several light users. If a zone sits near $110k per month, it needs strict activity rules and clear service scope so the fee matches the workload. Busy zones should pay for busy work.

Measure active users, onboarding time, and compliance labor per zone every month. If a tenant goes inactive, reprice or tighten scope before it drags on planning and cash. With six zone starts staged through Month 21, the forecast should show when recurring fees outrun fixed overhead. That is what protects EBITDA and owner pay.

1

Monthly Administration and Management Fees

Monthly Administration and Management Fees

Monthly fees matter because this business is not just renting space; it is also selling compliance work, reporting, and day-to-day zone management. With $35k to $110k monthly zone fees and $405k of planned monthly fee capacity, the pricing mix has to cover real labor and risk, or owner pay gets squeezed by unpaid admin work.

Here’s the quick math: one high-workload tenant can cost more in customs coordination, inventory reporting, and rework than it brings in if the fee is too low. So the real question is not just occupancy; it’s whether each account pays for its own support load. A better fee schedule turns activity into profit instead of hidden overhead.

- Monthly admin fee: recurring zone management charge

- Onboarding fee: setup and compliance start work

- Inventory reporting: ongoing tracking and filings

- Handling charges: special service and labor events

Price for workload, not just space

Track each tenant’s compliance hours, reporting volume, and handling events before you set the fee. If one account needs more labor, its monthly price should rise or the margin disappears. In this model, separate line items matter because bundled pricing hides cost and makes EBITDA look better than it is.

Use a simple test: compare monthly fee collected versus admin labor, rework, and facility use tied to that tenant. If the fee does not cover the support load, the owner is funding the client’s operations. Price onboarding, monthly administration, inventory reporting, and handling as separate lines so each account pays its own way.

2

Transaction and Inventory Activity

Transaction and Inventory Activity

This driver covers admissions, withdrawals, inventory moves, and reporting. It lifts revenue only when each event is billed, because busy zones add labor and customs work. Since variable expenses aren’t provided, model transaction margin as an editable assumption: activity fee minus labor, rework, and compliance cost. If pricing is flat while movement rises, EBITDA and owner pay shrink even when the top line looks busy.

Track event count, reporting hours, exception rate, and fee per event. A high-volume tenant can look strong on revenue but still be weak on cash if the team spends too long fixing inventory records. One clean rule: more movement should only pay more when the fee covers the extra work.

Price Activity, Not Just Space

Price admissions, withdrawals, and inventory reporting separately when activity varies. Here’s the quick test: per-event revenue must cover direct labor plus compliance review. If a tenant creates heavy movement, don’t tuck it into a flat monthly fee. That turns growth into hidden cost growth and puts owner distributions at risk.

- Monthly admissions and withdrawals

- Inventory lines and report volume

- Labor hours per exception

- Fee per event and surcharge rules

- Rework and compliance error rate

When movement rises, cash flow should rise too; otherwise the owner funds extra work out of pocket.

3

Facility Utilization and Logistics Service Mix

Facility Utilization and Logistics Service Mix

This driver is the share of space and work you actually sell: storage, handling, staging, labeling, and related logistics. With three owned zones, three rented zones at $47k/month, $75M tied up in purchases, $21M in construction, and $745k of capex, low occupancy turns fixed facility cost into owner-income drag. Empty bays cut gross profit and slow the cash move toward owner pay, even before the Month 26 trough eases.

Fill Zones With Billable Work

Track occupancy by zone and split revenue by service line, so you can see whether storage is carrying the rent or whether handling and labeling are doing the work. The goal is higher-yield mix, not just more tenants. If billed activity rises while the $47k monthly rent stays spread across more work, gross margin improves and cash conversion gets better after the Month 26 cash trough.

4

Compliance Labor Efficiency

Compliance Labor Efficiency

Compliance labor efficiency is about doing the required customs and inventory work with less manual effort, fewer errors, and less rework. In this model, the labor base grows from $515k to $815k per year, so even small gains matter. A $110k Compliance Officer and a $150k Customs IT Integration can protect margin if they cut reporting time and keep one team serving more tenants.

Here’s the quick math: the payroll step-up is $300k per year. If better procedures and systems let the same staff handle more zone users, EBITDA improves and owner pay gets safer. If labor rises but accuracy does not, the extra cost just eats c ash. The key test is whether each added tenant or inventory event adds work slowly, not one-for-one.

Track labor per tenant

Measure manual reporting hours, rework rate, and compliance touches per tenant. Also track admissions, withdrawals, inventory changes, and exception cases, since those drive workload. If one zone user creates much more admin time than others, price the workload or tighten the process. Efficiency means accuracy plus capacity, not weaker controls.

Use standard procedures, trained staff, and system checks to keep inventory controls repeatable. That matters most when tenants scale, because a stable process lets one team handle more users without proportional headcount. The owner should watch labor cost as a share of fees, since lower compliance overhead supports higher EBITDA and more reliable distributions.

5

Fixed Overhead, Reserves, and Reinvestment

Fixed Overhead and Cash Reserves

Fixed overhead of $54k per month — property taxes, security, maintenance, insurance, marketing, and utilities — must be paid before the owner sees any real take-home pay. That is $648k a year before growth spend. Add $745k capex, $21M construction, $75M owned-zone purchases, and the disclosed $3,459M minimum cash deficit, and EBITDA stops looking like cash you can distribute.

Reserve policy changes the payout story. If cash is not set aside before distributions, the owner can pull money from a business that looks profitable on paper but is still funding buildout and operating cover. The practical rule is simple: hold reserves first, then pay yourself, especially before the 60-month payback mark.

Track Cash Before Draws

Use a cash plan that separates operating profit, reserve needs, and owner distributions. Track monthly overhead, capex timing, construction spend, and zone purchase funding in one schedule so EBITDA does not get mistaken for spendable income.

- Set a monthly reserve floor.

- Block draws until reserves fund.

- Model overhead at $54k monthly.

- Stress-test cash before 60 months.

If spend runs ahead of lease cash, owner pay should wait. That protects the balance sheet, reduces forced borrowing, and keeps distributions tied to real free cash, not just reported profit.

6

Compare lean, base, and high FTZ owner-income cases

Owner income scenarios

Owner income swings hard here because zone count, fees, staffing, and reserve needs move faster than revenue in the early years. Cash stays tight in the lean case, then improves after breakeven in Month 25.

| Scenario | Low CaseLean cash | Base CaseModeled path | High CaseUpside case |

|---|---|---|---|

| Launch model | Owner income stays near zero while the model absorbs early losses and cash burn. | Owner income turns positive after breakeven and follows the modeled EBITDA recovery. | Owner income is strongest when utilization rises and the zone base scales faster than overhead. |

| Typical setup | Year 1 EBITDA is -$1.363M and Year 2 EBITDA is -$802k, so distributions are unlikely and any owner pay depends on payroll budget. | The model reaches breakeven in Month 25, then Year 3 EBITDA is $1.2M before taxes, debt service, reserves, and reinvestment. | Year 4 EBITDA reaches $1.304M, then Year 5 eases to $1.135M as staffing expands and costs catch up. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0Cash tight | $1.2MPost-breakeven | $1.1M - $1.3MUtilization upside |

| Best fit | Use this to stress test the first two operating years and a no-distribution path. | Use this as the main operating case for lender, investor, and owner planning. | Use this to test upside when throughput improves but payroll and compliance remain controlled. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Foreign Trade Zone Operation Porter's Five Forces Analysis

- Foreign Trade Zone Operation BCG Matrix

- Foreign Trade Zone Operation Business Model Canvas

- What 5 KPIs Matter For Foreign Trade Zone Operation Business?

- Foreign Trade Zone Operation Business Plan Template in Pre-Written Word

- How Increase Foreign Trade Zone Operation Profitability?

- What Are Operating Costs For Foreign Trade Zone Operation?

- Foreign Trade Zone Startup Costs: $103M+ Launch Budget

- Foreign Trade Zone Financial Model Template in Excel

- How To Open A Foreign Trade Zone Operation In 6–12+ Months

- How To Write A Business Plan To Launch Foreign Trade Zone Operation?

- Foreign Trade Zone Operation Marketing Mix

- Foreign Trade Zone Operation Marketing Plan

- Foreign Trade Zone Operation Business Proposal

- Foreign Trade Zone Operation PESTEL Analysis

- Foreign Trade Zone Operation Pitch Deck Example Editable PPTX

- Foreign Trade Zone Operation Business SWOT Analysis

- Foreign Trade Zone Operation Value Proposition Canvas

Frequently Asked Questions

In this model, distributions are not realistic in the first two years because EBITDA is -$1363M in Year 1 and -$802k in Year 2 EBITDA turns positive at $12M in Year 3 and reaches $1135M in Year 5 That is before taxes, debt service, reserves, and owner-specific financing