Owner income$120k

Owner income$120kFreelance Data Analyst Owner Income: $120K Pay, Month 22 Breakeven

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$120k  Net margin79%-82%

Net margin79%-82% Revenue for target pay$184k-$191k

Revenue for target pay$184k-$191k Business difficultyHard

Business difficultyHard

You’re planning owner income from client work, not an employee salary This model estimates $120,000 in annual founder pay, with breakeven in Month 22 and EBITDA moving from negative in the first year to positive by Year 3 It covers revenue, expenses, margin, reserves, contractors, software, and owner take-home planning

Owner income$120kNet margin79%-82%Revenue for target pay$184k-$191kBusiness difficultyHardWant to test your own owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Use it alongside the model's Month 22 breakeven and $657k minimum cash when setting reserves.

Want the full owner income projection for Freelance Data Analysis?

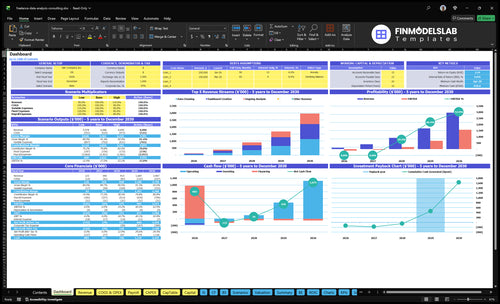

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Freelance Data Analysis Financial Model Template; open the model.

Owner-income model highlights

- Owner pay: $120k modeled

- Fixed overhead: $2,600 monthly

- EBITDA: -$121k to $1,571M

Soft next step: open the full model for dashboard, pricing, pipeline, utilization, payroll, cash flow, and low/base/high scenarios.

How much do freelance data analysts make in the United States?

In the United States, Freelance Data Analysis owner income is modeled at $120k, but cash flow can still be tight: Year 1 EBITDA is -$121k after payroll, marketing, fixed overhead, and delivery costs. For the key driver behind that gap, see What Is The Most Critical Measure For The Success Of Your Freelance Data Analysis Business?.

Base case

- Modeled owner pay: $120k

- Year 1 EBITDA: -$121k

- Breakeven timing: Month 22

- Year 3 EBITDA: $175k

Upside case

- Year 5 rates: $110-$130/hour

- Year 5 EBITDA: $1.571M

- Depends on client volume

- Protect collections and reserves

What expenses and profit margin shape freelance data analyst take-home?

The short answer is that Freelance Data Analysis take-home depends on whether pricing covers the full cost stack, not just billable work. Fixed overhead is $2,600/month or $31,200/year before any analyst pay, while contractor fees run 8% of revenue in Year 1 and ease to 6% by Year 5; for the launch side, see What Is The Estimated Cost To Open, Start, And Launch Your Freelance Data Analysis Business?. Higher revenue only helps if it also covers contractors, revisions, quality review, and unpaid admin time.

Year 1 cost stack

- Contractor fees take 8% of revenue.

- Tool licenses take 3%.

- Cloud and data storage take 4%.

- Referral fees take 6%.

Year 5 pressure points

- Contractor fees fall to 6%.

- Tool licenses fall to 2%.

- Cloud and data storage rise to 6%.

- Payroll grows from founder plus 0.5 analyst FTE.

Can a freelance data analyst scale beyond hourly work?

Yes, Freelance Data Analysis can scale beyond hourly work, but the model changes fast: ongoing analysis rises from 20% of customer allocation in Year 1 to 60% by Year 5, and dashboard creation rises from 30% to 50%. That supports recurring revenue and smoother cash flow, but it also raises revision risk, so scope and delivery control matter more as you grow.

Where scale comes from

- 20% to 60% ongoing analysis mix

- 30% to 50% dashboard work

- Recurring reporting improves cash flow

- Automation lifts owner income

What gets harder

- Scope creep increases revision risk

- Subcontractors add capacity, but fees stay 8% to 6% of revenue

- Quality control needs tighter checks

- Delivery timelines must stay tight

Want to see the six biggest income levers?

1

8-18 hrsBillable Utilization

More billable hours turn the same week into more revenue, so this is the cleanest lever on owner take-home.

2

$90-$130/hrPricing Model

Each rate step up raises revenue on every hour sold, and higher-rate work helps offset fixed overhead and the Month 22 break-even point.

3

$5K-$35KClient Pipeline

Marketing spend rises from $5,000 to $35,000 while CAC falls from $250 to $160, so pipeline quality decides how fast sales turn into cash.

4

21%-18%Delivery Costs

Keeping contractor, tool, cloud, and referral costs near the 21% to 18% load protects margin and speeds payback.

5

20%-60%Retainer Mix

Growing ongoing analysis from 20% to 60% makes revenue steadier and cuts the owner time lost to constant one-off projects.

6

$110-$130/hrService Specialization

Pushing more work into dashboard creation and ongoing analysis lifts the average rate and reduces low-value cleaning time.

Freelance Data Analysis Core Six Income Drivers

Pricing Model

Pricing Model

Pricing is the first take-home lever. In Year 1, hourly rates are $90 for data cleaning, $110 for dashboard creation, and $100 for ongoing analysis; by Year 5, they rise to $110, $130, and $120. Higher rates lift gross profit only if scope stays tight, because extra revision time can erase the gain.

Fixed-fee dashboard work can improve the realized hourly rate if the scope is controlled. Retainers help cash planning, but value-based pricing only works when the client sees clear business use. Here’s the quick math: price, scope, and revision load decide whether higher fees become owner pay or unpaid rework.

Track Rate Realization and Scope

Measure quoted rate, realized hourly rate, and revision hours on every job. Track how often dashboard work stays inside the agreed scope, because one extra round of edits can turn a strong fee into weak margin.

- Set deliverables before pricing.

- Cap revisions in writing.

- Price retainers by output.

- Test higher rates by service.

1

Billable Capacity And Utilization

Billable Capacity and Utilization

Paid delivery hours drive revenue here, not total hours worked. Utilization means the share of available work time that is billable. In the model, service hours rise from 8 to 10 for data cleaning, 12 to 16 for dashboards, and 10 to 18 for ongoing analysis from Year 1 to Year 5. That is 25%, 33%, and 80% growth in billable delivery load.

Here’s the catch: utilization has to leave room for sales, proposals, admin, learning, and rework. Push every hour into delivery and short-term revenue can rise, but burnout and quality risk go up too. Owner income improves when repeatable work cuts unpaid time, because more of each paid hour turns into cash instead of revision time.

Track Paid Hours by Service

Measure billable hours, non-billable hours, and rework hours by service line each month. Use the simple formula: billable hours × hourly rate = revenue. Watch dashboards separately from cleaning and ongoing analysis, since each one grows at a different pace and can hide where time is leaking. A higher utilization rate only helps if quality stays steady.

Set a cap that protects delivery quality and owner pay. Keep a fixed buffer for proposals, admin, and learning, then standardize repeat tasks so more hours stay billable. If rework rises with utilization, the extra revenue is fake. The better signal is more paid hours, flat rework, and faster turnaround on client work.

- Billable hours by service

- Non-billable hours each month

- Rework and revision time

- Utilization rate by project

- Hourly rate by service

2

Retainer Mix

Retainer Mix

When more work shifts into monthly retainers, owner income gets steadier and less tied to chasing the next project. In this model, ongoing analysis rises from 20% in Year 1 to 60% in Year 5, which helps cover $2,600 in monthly fixed overhead and the $10,000 founder pay target.

Here’s the quick math: recurring dashboards, KPI reporting, data checks, and monthly analysis reduce sales pressure and smooth cash flow. The catch is scope creep. If meetings, refreshes, and ad hoc requests are not capped, retainer hours get eaten fast and the hourly return falls.

Retainer Scope Controls

Track retainer revenue, included hours, response time, and overage work. Each agreement should define hours, outputs, refresh timing, and response limits so the monthly fee matches the real workload.

- Cap meeting time.

- Limit ad hoc requests.

- Price extra analysis separately.

If the scope is open-ended, it is not a retainer. Tight terms protect margin, keep recurring revenue useful for cash planning, and make founder pay more dependable.

3

Service Specialization

Specialization Premium

Specialized work raises income because clients pay for a harder problem, not just hours. In this model, dashboard creation is $110/hour in Year 1 and $130/hour by Year 5, above data cleaning, so a tighter mix of executive KPI work, forecasting, automation, and advanced reporting lifts revenue per client. Niche focus also narrows marketing and improves proposal fit.

The risk is delivery drag. If quotes do not include discovery, dirty data cleanup, testing, and stakeholder revisions, the realized rate falls and owner pay gets squeezed. Specialized jobs should be scoped as full projects, not just build time, because hidden rework can turn a premium price into low-margin hours.

Price the Full Scope

Track service type, quoted hours, and revision rounds on every job. That shows whether dashboard and executive KPI work really beat generic cleanup. If a client wants forecasting, automation, or monthly reporting, price the discovery and QA steps up front so the project protects margin, not just revenue.

Keep the offer narrow enough to sell fast. A clear niche cuts wasted proposal time and helps support the $2,600 monthly fixed overhead and the $10,000 monthly founder pay target. What this estimate hides: if the client data is messy or the stakeholder group is large, the extra coordination time must be billed or the owner’s take-home falls.

- Estimate cleanup hours first

- Set revision limits

- Bill testing separately

- Use case-specific proposals

4

Client Acquisition Pipeline

Client Acquisition Pipeline

Pipeline quality is what turns data skills into cash. With a $5,000 Year 1 marketing budget and $250 CAC (customer acquisition cost), the model buys about 20 customers; by Year 5, $35,000 at $160 CAC supports about 219 customers. Strong proposals, higher conversion, bigger deal size, and faster closes improve revenue and lower idle time.

Here’s the quick math: if leads slow down, billable hours sit empty, collections slip, and the owner gets pushed to discount rates. Referrals and niche positioning reduce acquisition drag, while weak close timing hurts cash flow even when demand exists. One clean line: no pipeline, no pay.

Track Leads to Cash

Measure lead volume, proposal-to-close rate, average deal size, and da ys to close. Those four inputs tell you whether marketing spend is creating usable work or just noise. Track CAC by channel, then compare it with realized hours so you know which sources pay back.

Push referrals and niche offers first, because they usually cut acquisition cost and improve fit. Tight scopes, clear pricing, and fast follow-up help proposals close faster and protect cash flow. If close time stretches, owner pay gets squeezed even when booked demand looks healthy.

- 20 Year 1 customers at $250 CAC

- 219 Year 5 customers at $160 CAC

- Fast closes improve cash timing

5

Delivery Cost Structure

Delivery Cost Structure

Margin here is the gap between project revenue and delivery spend. At the current mix, contractor fees at 8%, tool licenses at 3%, cloud at 4%, and referral fees at 6% total 21% of revenue. By Year 5, those fall to 6%, 2%, 6%, and 4%, or 18%.

On $100,000 of revenue, that is $21,000 versus $18,000 in delivery cost. The owner keeps more cash only if subcontractor hours, cloud use, and rework are priced into proposals. This matters because extra delivery cost comes straight out of gross margin and can delay the owner’s $10,000 monthly pay target.

Price the full delivery load

Track delivery cost by job: contractor hours, cloud spend, software, referral fees, and rework hours. Keep the full load near the modeled 21% early and 18% later, then test whether fixed-fee dashboards and retainers still cover revisions. One clean rule: if the scope grows, the fee must grow too.

- Log contractor cost per project.

- Cap cloud usage by client.

- Price revision rounds upfront.

- Recover setup time with repeat work.

Automation helps only when setup time is recovered across enough billable work. If a tool saves 5 hours but takes 8 hours to set up, margin drops instead of rising. Use scoping notes and clear limits so subcontractors, cloud usage, and rework do not quietly eat owner profit.

6

Compare low, base, and high owner income scenarios

Owner income scenarios

Owner income changes with hourly rates, variable cost load, overhead, and how fast the client base scales. The low case stays cash tight; the high case only works after the model gets much more efficient.

| Scenario | Low CaseLean case | Base CaseModeled case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the tight-cash path where profit stays negative and owner pay needs to be deferred or kept very light. | This is the modeled path where the business reaches breakeven in Month 22 and supports normal owner pay. | This is the upside path where stronger pricing and scale support higher owner income. |

| Typical setup | Year 1 rates sit at $90 to $110 per hour, variable costs run about 21%, fixed overhead is $2,600 a month, and $5,000 marketing still leaves EBITDA at -$121k. | The core model reaches breakeven in Month 22, posts $175k EBITDA in Year 3, and supports $120,000 of modeled founder pay as the team scales. | Year 5 rates rise to $110 to $130 per hour, variable costs ease to 18%, marketing reaches $35,000, and EBITDA climbs to $1.571M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No sustainable owner drawCash tight | $120,000 founder payModeled pay | Higher than founder payStrong upside |

| Best fit | Use this to stress test reserve need, slow sales, and the risk of paying the owner before the business is ready. | Use this as the main planning case if you want a realistic target for owner income and cash timing. | Use this if you want to test the upside case, but keep a bigger reserve because the growth path is harder to execute. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Related Products

- Freelance Data Analysis Porter's Five Forces Analysis

- Freelance Data Analysis BCG Matrix

- Freelance Data Analysis Business Model Canvas

- 7 Critical KPIs to Measure for Freelance Data Analysis

- Freelance Data Analysis Business Plan Template in Pre-Written Word

- Increase Freelance Data Analysis Profitability: 7 Essential Strategies

- How to Manage Monthly Running Costs for Freelance Data Analysis

- Freelance Data Analysis Startup Costs: $43K Launch Budget Guide

- Freelance Data Analysis Financial Model Template in Excel

- How To Start A Freelance Data Analysis Business In 2 To 6 Weeks

- How to Write a Business Plan: Freelance Data Analysis (7 Steps)

- Freelance Data Analysis Marketing Mix

- Freelance Data Analysis Marketing Plan

- Freelance Data Analysis Business Proposal

- Freelance Data Analysis PESTEL Analysis

- Freelance Data Analysis Pitch Deck Example Editable PPTX

- Freelance Data Analysis Business SWOT Analysis

- Freelance Data Analysis Value Proposition Canvas

Frequently Asked Questions

The model uses $120,000 in annual founder pay, but early profit does not support that cleanly EBITDA is -$121,000 in Year 1 and -$54,000 in Year 2, then turns positive at $175,000 in Year 3 Treat this as pre-tax owner pay capacity, not guaranteed income