Owner income$243k

Owner income$243kHow Much Does A Salad Bar Owner Make? $50k Pay Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$243k  Net margin51%

Net margin51% Revenue for target pay$476k

Revenue for target pay$476k Business difficultyHard

Business difficultyHard

You’re separating sales from take-home, which is the right move This model shows $31,460 average monthly revenue in the first year, a $50,000 owner-operator salary, and $193,000 EBITDA before personal taxes, debt service, and reserves Owner income depends on what profit is kept in the business versus drawn out

Owner income$243kNet margin51%Revenue for target pay$476kBusiness difficultyHardWant to test your salad bar owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, operating costs, reserves, and your pay goal.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Want to pressure-test Salad Bar owner income?

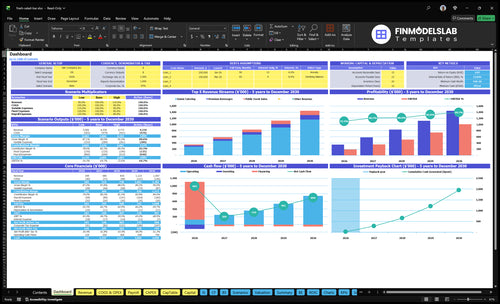

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Salad Bar Financial Model Template; open it.

Owner-income model highlights

- $50,000 owner salary

- $31,460 monthly revenue

- $193,000 Year 1 EBITDA

- Month 2 breakeven

- 12-month payback

- Year 5 EBITDA: $1008 million

- Dashboard and assumptions tabs

- Revenue, COGS, payroll, cash flow

- Scenarios stress-test the forecast

What profit margin does a salad bar have?

A Salad Bar can post a very strong margin: the first-year gross margin is 87% because ingredient-related cost is 13%, and after 8% in variable costs, contribution is about 79%. On the provided model, first-year EBITDA margin is about 51% ($193,000 divided by $377,520 revenue), and How Much Does It Cost To Open A Salad Bar Business? helps frame the startup cost side. No separate waste line is shown, so spoilage and portion swing should be built into ingredient cost or tracked as a waste input.

Gross margin math

- 13% ingredient-related cost

- 87% gross margin

- 8% variable costs

- 79% contribution margin

Profit watchouts

- $193,000 EBITDA

- $377,520 revenue

- 51% EBITDA margin

- Model waste inside ingredient cost

Does a salad bar make more money if the owner works there?

Yes—Salad Bar makes more money when the owner runs management, prep, buying, and service, because the model already includes a $50,000 owner-operator salary each year; if you replace that with paid management and still want owner draws, distributable profit falls by about that wage. Year 1 EBITDA is $193,000, and Year 5 EBITDA is $1.008 million, so the gain only holds if traffic, prep flow, and manager accountability stay tight.

Owner-run math

- $50,000 owner salary is built in.

- Owner covers key daily control.

- Paid management cuts free cash.

- Draws can shrink by that wage.

Scale only if systems hold

- Year 1 EBITDA: $193,000.

- Year 5 EBITDA: $1.008 million.

- Traffic must support added staff.

- Prep systems must stay fast and clean.

How many customers does a salad bar need to make money?

A Salad Bar needs about 18 customers per day to hit salary-level breakeven, while the first-year model targets 480 weekly customers, or about 69 per day, at a $15.13 weighted AOV; pair that volume target with What Is The Most Important Metric To Measure Customer Satisfaction At Salad Bar?. Here’s the quick math: $7,907 ÷ $15.13 ÷ 30 = 17.4 customers per day, rounded to 18, and the model reaches breakeven in Month 2.

Breakeven volume

- Need 18 customers/day

- Use $15.13 AOV

- Reach $7,907/month

- Apply 79% contribution margin

Operating target

- Plan for 480 customers/week

- Serve about 69 customers/day

- Build lunch rush capacity

- Drive office repeat visits

Want the six drivers that move salad bar income?

1

480/wkCustomer Volume

More covers lift revenue fast and spread the $2.08K monthly overhead and owner salary across more sales.

2

$12-$18Average Ticket

A bigger ticket from weekend mix and add-ons raises revenue per guest without much extra labor.

3

13% COGSIngredient Margin

Keeping food cost near 13% leaves more gross profit for the owner's take-home.

4

8% varLabor Efficiency

Tighter prep and staffing keep variable labor and service costs from growing as fast as sales.

5

Low wastePortion Control

Smaller portions and less spoilage protect margin because every ounce saved stays in cash.

6

$2.1K/moOccupancy Cost

Lean fixed overhead protects cash in slow weeks and makes break-even easier to hit.

Salad Bar Core Six Income Drivers

Customer Volume

Customer Volume

Customer volume is the biggest income driver here because each extra order keeps 79% of first-year sales as contribution margin before fixed overhead and payroll. Revenue still depends on average ticket, but more covers matter most for owner pay because they spread the same rent, admin, and management costs over more checks.

The plan starts at 480 weekly customers in Year 1 and rises to 1,620 weekly customers by Year 5. The risk is thin weekday traffic: Monday and Tuesday begin at 30 customers each, so weak lunch flow can cap cash flow even if weekends are strong. One slow day can pull down the whole week.

Track Traffic by Daypart

Measure covers by weekday, weekend, lunch rush, and repeat visits, not just weekly total. Pair customer counts with average ticket and speed of service, because office density and health-focused local demand only turn into income if guests can get served fast enough to come back.

- Track covers by day and hour.

- Watch repeat visits weekly.

- Test lunch speed against demand.

- Protect Monday and Tuesday traffic.

If Monday-Tuesday stays near 30 customers each, fix traffic before adding payroll. More bodies in seats lift revenue, but the owner only feels it if added volume arrives without extra labor that eats the margin gain.

1

Average Ticket

Average Ticket

Average ticket is the average spend per guest, and it matters because each extra dollar lifts revenue without adding another customer. In Year 1, the plan uses $12 midweek AOV and $18 weekend AOV; by Year 5 that rises to $14 and $20. If ingredient cost does not rise faster, the owner keeps more gross profit per transaction.

Use weighted AOV, not menu sticker price: day mix, add-ons, and beverage attach rate all change the real check. The risk is value pushback if guests think the bowl is overpriced, which can slow traffic and cut owner draw.

Track the ticket mix

Measure ticket by daypart, not just by menu. Track weekday AOV, weekend AOV, proteins, beverages, and sides, then compare that mix to 13% COGS and 87% gross margin so upsells do not erode profit. If add-ons lift price but push food cost up faster, the owner makes less, not more.

Here’s the quick math: a higher ticket only helps if the extra dollars stay above food cost. Watch comped items, portion size, and upsell conversion weekly; if the check rises and guest counts hold, cash flow improves and owner pay gets easier to fund.

2

Ingredient Margin

Ingredient Margin

Ingredient margin is the cash left after greens, proteins, toppings, dressings, and packaging. With 13% first-year COGS, every $100 of sales keeps about $87 for gross profit before labor and overhead; by Year 5, 10% COGS lifts that to $90. That extra 3 points flows straight into gross profit and earnings before interest, taxes, depreciation, and amortization (EBITDA), so it can raise owner draw fast.

The biggest swing comes from order mix. Protein-heavy bowls, bigger topping scoops, and produce inflation can cut margin fast, while premium add-ons help only if their price clears their true cost. One clean rule: if ticket size rises but ingredient margin falls, the owner is paying for growth with less cash.

Track mix, portions, and supplier price

Measure ingredient margin by daypart and item, not just by month. Track order count, average ticket, protein mix, portion sizes, packaging cost, and supplier changes so you can see which bowls hit target and which ones miss. If a menu item sells well but pushes COGS above 13%, it is hurting take-home income.

Use portion tools, recipe specs, and add-on pricing to protect the spread. Test smaller protein portions, bundled premium add-ons, and alternate suppliers before produce spikes hit. The goal is simple: keep gross margin moving from 87% toward 90% without slowing line speed or losing guests.

3

Labor Efficiency

Labor Efficiency

Labor is a direct hit to owner income in this model. The first-year plan carries 6% variable staff wages plus a $50,000 owner-operator salary, so every wasted prep hour, slow counter handoff, or bad shift plan cuts cash that could have become profit or draw.

Here’s the quick math: if weekday staffing runs too heavy, payroll eats margin; if lunch rush is understaffed, you lose covers and speed. The model also adds a $50,000 coordinator in Year 2 and operations support in Year 3, so labor must scale with sales, not just headcount. Better throughput should lift income without giving back margin.

Measure Labor by Covers and Peak Hours

Track labor against daily covers, lunch rush speed, prep hours, and manager coverage. The useful inputs are orders per shift, wage dollars per daypart, and sales by weekday versus weekend. If a shift adds payroll but does not raise covers or speed, it is probably hurting owner pay.

- Watch labor percent by daypart.

- Match staff to lunch peaks.

- Cut overstaffing on slow weekdays.

- Protect speed at busy counters.

Separate owner labor savings from manager-run profit. If a coordinator or ops lead reduces the owner’s hours, that helps only if payroll stays in line and service still holds. If onboarding or scheduling slips, labor can rise faster than sales, and cash flow tightens fast.

4

Occupancy Cost

Occupancy Cost

Occupancy cost is the monthly rent and location charge tied to the site. In this model, $2,080 is fixed overhead, but rent is not separated, so treat occupancy as an editable input. The real test is sales per location dollar: a high-traffic site can raise owner income if lunch and weekend orders cover the lease, but weak traffic can sink profit fast.

Here’s the quick math: if occupancy rises and sales do not, take-home income falls dollar for dollar. A cheap lease still hurts when traffic is thin, because fixed costs eat the margin before the owner can pay themselves. The risk is signing a lease before repeat demand is proven.

Track Occupancy Against Sales

Use occupancy as a share of monthly sales, not a stand-alone number. For this salad bar, track monthly sales per site, lunch and weekend order counts, and the lease amount together, then test whether the site can support the fixed load.

- Enter rent as an editable fixed cost.

- Test lunch and weekend traffic first.

- Delay long leases until repeat demand shows.

If sales per location dollar do not rise faster than occupancy, owner draw gets squeezed even when the menu sells well. High-foot-traffic sites only help when the order count is strong enough to absorb the lease.

5

Waste And Portion Control

Waste And Portion Control

Fresh produce spoilage and uneven scoops quietly hit owner pay. With 13% first-year COGS, every extra 1 point of waste cuts contribution margin from 79% to 78% before payroll and overhead, so the same sales bring home less cash.

Model waste as higher COGS or a separate was te rate. The key inputs are prep pars, inventory rotation, portion size, and daily sales by daypart. The biggest risk is over-prepping for slow Mondays and Tuesdays, which turns fresh food into sunk cost and weakens the owner’s draw.

Control Pars, Portions, and Spoilage

Track waste weekly as a share of food spend, then tie prep to actual sales. Use first-in, first-out rotation, portion tools, and item-level sales checks so scoops stay consistent and spoilage stays visible.

- Set pars by weekday demand

- Weigh high-cost proteins

- Write off spoilage daily

- Review top waste items weekly

Here’s the quick math: if waste rises, gross profit falls first, then cash for payroll, rent, and owner pay. The fix is simple discipline, not bigger menus.

6

Compare low, base, and high salad bar owner income scenarios

Owner income scenarios

Weekly traffic, order value, and margin drive owner income here, while labor and fixed overhead decide what's left after salary. The low, base, and high cases track Year 1 to Year 5.

| Scenario | Low CaseDownside | Base CaseModeled | High CaseUpside |

|---|---|---|---|

| Launch model | This is the lower earnings path, where the owner mostly relies on salary and small distributions. | This is the modeled middle path with steady traffic, tighter costs, and room for salary plus distributions. | This is the stronger path, where higher weekly traffic and order value create more cash for salary plus distributions. |

| Typical setup | Year 1 stays lean, with 480 weekly customers, $31,460 monthly revenue, 13% COGS, 8% variable costs, and $193,000 EBITDA. | Year 3 reaches 990 weekly customers, $68,770 monthly revenue, 11.5% COGS, 7% variable costs, and $508,000 EBITDA. | Year 5 reaches 1,620 weekly customers, $120,380 monthly revenue, 10% COGS, 6% variable costs, and $1,008,000 EBITDA. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $50k-$243kTake-home floor | $50k-$558kCore take-home | $50k-$1.06MTake-home upside |

| Best fit | Use this to stress-test a slow launch, owner-heavy operations, and tighter cash use. | Use this as the working plan for a steady ramp from Year 3 volume and margin. | Use this to test a scaled shop with stronger traffic, better order value, and more distribution room. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Salad Bar Porter's Five Forces Analysis

- Salad Bar BCG Matrix

- Salad Bar Business Model Canvas

- 7 Critical KPIs to Scale Your Salad Bar Business

- Salad Bar Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Salad Bar Profitability and Cash Flow

- How to Manage Monthly Running Costs for a Salad Bar Business

- Salad Bar Startup Costs: $114k CAPEX Plus $836k Cash Need

- Salad Bar Financial Model Template in Excel

- How To Open A Salad Bar In 3 To 6 Months With A Launch-Ready Plan

- How to Write a Business Plan for a Mobile Salad Bar Concept

- Salad Bar Marketing Mix

- Salad Bar Marketing Plan

- Salad Bar Business Proposal

- Salad Bar PESTEL Analysis

- Salad Bar Pitch Deck Example Editable PPTX

- Salad Bar Business SWOT Analysis

- Salad Bar Value Proposition Canvas

Frequently Asked Questions

Yes, the model shows profitability, but it depends on traffic and cost control First-year revenue is about $377,520, EBITDA is $193,000, and breakeven is listed in Month 2 That assumes 480 weekly customers, 13% ingredient-related cost, 8% variable costs, and $2,080 monthly fixed overhead before taxes and reserves