Owner income$1.3M to $8.9M

Owner income$1.3M to $8.9MHow Much Underground Fuel Tank Removal Owners Can Make: $13M EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$1.3M to $8.9M  Net margin43% to 65%

Net margin43% to 65% Revenue for target pay$3.1M

Revenue for target pay$3.1M Business difficultyHard

Business difficultyHard

You’re pricing risky permitted work, not selling simple excavation hours, so owner income has to start with job volume, margins, insurance, payroll, reserves, and the owner’s role This five-year planning view uses researched assumptions, including $3078M Year 1 revenue, $1316M Year 1 EBITDA, and a Month 4 breakeven It excludes tax advice, guaranteed salary claims, and environmental legal guidance

Owner income$1.3M to $8.9MNet margin43% to 65%Revenue for target pay$3.1MBusiness difficultyHardWant to test your owner income calculator assumptions?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, labor, overhead, marketing, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income will change with job mix, margins, labor, taxes, financing, reserves, and environmental results. This is not guaranteed salary, tax advice, or owner distribution advice.

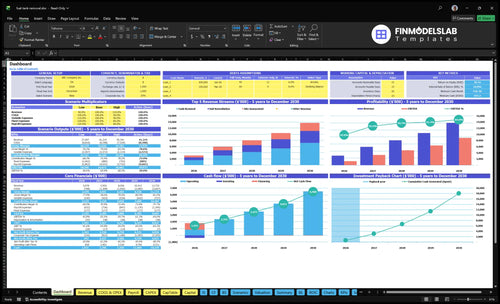

Want to check owner income in the Underground Fuel Tank Removal model?

The screenshot shows the dashboard, revenue assumptions, job mix, crew costs, disposal and testing costs, overhead, equipment, scenarios, and owner income outputs; open the Underground Fuel Tank Removal Financial Model Template to see the full range.

Owner-income model highlights

- Owner income by scenario

- Revenue, EBITDA, payback

- Month 4 breakeven

How many fuel tank removals per month to pay the owner?

For Underground Fuel Tank Removal, the owner-pay answer starts with the desired pre-tax draw, then adds overhead and operating costs. In the Year 1 model, 15 active customer-months with 85% tank-removal attach works out to about 128 tank removals a month, with about $171k in monthly revenue and roughly $121k in contribution before payroll and overhead. More removals only pay the owner if permits, crew time, disposal slots, and collections stay tight.

Volume needed

- 15 active customer-months

- 85% include tank removal

- About 128 removals monthly

- $171k monthly revenue

What keeps pay real

- $121k contribution before overhead

- Track permits before scheduling crews

- Limit disposal-slot and hauling delays

- Collect fast or owner pay slips

How much can a fuel tank removal business owner make?

An Underground Fuel Tank Removal owner can show EBITDA-based income capacity of $1.316M in Year 1, $4.806M in Year 3, and $8.865M in Year 5, before taxes, debt service, capex, reserves, and owner distributions. For margin levers, see How Increase Underground Fuel Tank Removal Profits?.

Owner Income

- Year 1: $1.316M EBITDA capacity

- Year 3: $4.806M EBITDA capacity

- Year 5: $8.865M EBITDA capacity

- Amounts are pre-tax and pre-debt

Cash Reality

- $547k minimum cash in Month 2

- $3.805M startup capex in the model

- Small crews keep overhead lower

- Licensed teams scale faster with referrals

What fuel tank removal profit margin is realistic?

For Underground Fuel Tank Removal, the model says Year 1 direct costs for disposal, waste, fuel, maintenance, permits, field supplies, and PPE run 295% of revenue, which leaves a 705% gross margin before payroll, overhead, marketing, insurance, and reserves. For the operating scorecard, see What Five KPIs Should Underground Fuel Tank Removal Business Track? Contaminated soil can lift the invoice, but it also lifts disposal, lab analysis, transport, subcontractor, working-capital, and reserve needs, so don’t treat it as automatic profit.

Margin math

- 295% direct costs in Year 1

- 705% gross margin before overhead

- $1,316M / $3,078M EBITDA data

- 42.8% EBITDA margin shown

Cost watch

- Price scope tightly, job by job

- Track contamination costs separately

- Watch lab and transport spend

- Keep reserve needs in view

Want the six main income drivers in one view?

1

$3.1M-$13.7MJob Volume

More permitted jobs and faster closes push revenue from $3.1M in Year 1 to $13.7M in Year 5, so this is the main take-home lever.

2

29.5%-23.5%Cost Load

Disposal, fuel, permits, and PPE start at a 29.5% variable load and ease to 23.5%, which drops straight into EBITDA.

3

$14.75K/moFixed Overhead

Rent, insurance, licensing, and back office costs run $14.75K a month, so weak volume keeps owner pay under pressure.

4

$10.5K-$13.6KTicket Size

Removal jobs at 60 hours and remediation jobs at 80 hours carry the most billable time, so higher ticket work lifts income fastest.

5

45-50 hrsCrew Utilization

Billable time per active customer rises from 45 to 50 hours a month, so better crew and equipment use turns the same team into more revenue.

6

40%-60%Job Mix

Soil remediation grows from 40% to 60% of the mix, and that shifts the work toward larger, more labor-heavy jobs.

Underground Fuel Tank Removal Core Six Income Drivers

Permitted Job Volume

Permitted Job Volume

More completed permitted jobs is the first income lever here. The model points to about 15 active customer-months in Year 1 and 517 active customer-months in Year 5, but the cash payoff only shows up after variable costs, not from revenue alone. More permitted volume spreads fixed overhead and can lift EBITDA.

The bottleneck is not demand alone. Permit delays, inspection timing, crew gaps, disposal scheduling, and weather downtime can stall completions, so the owner’s take-home pay depends on how many jobs actually close in the month. One delayed permit can push profit into the next period.

Track permits to protect profit

Measure the flow from lead to permitted job to completed removal. Track permit cycle time, inspection date lag, crew idle days, and disposal slot availability so you can spot where volume breaks. Here’s the quick math: if fixed overhead stays high, every extra completed job helps cover it faster.

- Track permit-to-start days

- Watch inspection backlog weekly

- Lock disposal windows early

- Build weather buffer into schedules

What this estimate hides: a job that is permitted but not finished still ties up crew time and cash. If completion rates slip, EBITDA falls even when booked volume looks strong.

1

Average Project Revenue And Job Mix

Average Project Revenue Mix

Average project revenue rises when the scope is clear and the job mix includes site assessment, tank removal, and priced soil work. The model shows $171k average active customer-month revenue in Year 1 and $221k in Year 5, so bigger jobs can lift cash fast, but only if the extra hours are billed cleanly.

Here’s the quick math: site assessment runs $225 to $250 per hour, tank removal runs $175 to $200 per hour, and soil remediation runs $150 to $170 per hour. Soil work grows from 40% to 60% of the mix, which helps revenue, but contaminated jobs can hurt margin if disposal and lab work are underpriced.

Price the Scope, Not the Guess

Track each quote by service line and compare planned hours to billed hours. The owner should know the share of revenue from assessment, removal, and remediation, plus any pass-through costs for disposal and lab testing. If soil work is growing, build that into pricing before the job starts, not after the crew is in the ground.

- Log hours by task

- Separate disposal and lab fees

- Test margin on contaminated jobs

2

Crew And Equipment Utilization

Crew and Equipment Utilization

When the crew and machines stay on billable work, the owner keeps more of each job’s margin. Year 1 staffing is 1 operations manager, 1 senior environmental engineer, 2 certified field technicians, 1 project coordinator, and 1 sales and compliance officer; by Year 5, technician count rises to 6. One clean metric: billable crew hours per paid day.

Idle crews, truck downtime, and slow inspections eat cash fast because the business also carries $185k excavator and trailer capex, $110k for two trucks, and $22k for GPR gear. If routing is weak or jobs wait on approval, payroll and equipment costs keep running while revenue stalls. Better utilization lifts owner pay without chasing unpriced volume.

Track Billable Hours, Not Just Jobs

Measure billable hours per technician, truck days on site, GPR scans completed, and downtime by cause. Here’s the quick check: if a crew is staffed but not on a permitted site, the business is paying for capacity twice, once in payroll and once in lost margin. That hits EBITDA and slows owner draw.

Set routing by permit timing, not by geography alone. Keep a small bench for inspection delays, but don’t overhire ahead of demand. The goal is simple: more paid field time, fewer empty miles, and fewer days where expensive equipment sits still.

- Track paid hours by crew each week

- Log truck and excavator downtime

- Watch inspection delay days

- Match crew count to active permits

3

Disposal, Testing, And Subcontractor Cost Control

Disposal, Testing, And Subcontractor Cost Control

For an underground fuel tank removal job, this driver covers disposal and waste fees, fuel and maintenance, site permits, lab testing, transport, field supplies, PPE, and remediation subcontractors. Here’s the quick math: listed variable cost load is 295% of revenue in Year 1 and still 235% by Year 5, so weak scope control can turn a sold job into a cash drain and delay owner pay.

The biggest swing risks are contaminated soil, lab delays, hauling distance, and subcontracted remediation. If a job needs extra testing or disposal handling, cash gets tied up in work-in-process before the invoice clears. One line matters: price the waste path before you break ground.

Track disposal and testing cost per job

Measure each project by disposal fee, lab spend, permit cost, fuel, and subcontractor cost as a share of revenue. The benchmarks are stark: disposal and waste fees run 150% of revenue in Year 1 and 130% by Year 5; fuel and maintenance run 80% to 60%; permits run 40% to 30%; supplies and PPE run 25% to 15%.

- Quote soil testing before mobilizing

- Pre-approve remediation subcontractor rates

- Track haul distance and disposal fees

- Flag contaminated soil fast

- Invoice work-in-process sooner

If those costs drift, gross margin falls before overhead even hits. Tight scopes, clean bid sheets, and documented testing triggers protect cash and keep more profit available for the owner draw.

4

Insurance, Compliance, Overhead, And Reserves

Insurance, Compliance, and Reserves

Insurance, compliance, overhead, and reserves take cash before owner pay. The monthly fixed items shown are $65k rent, $42k environmental liability insurance, $11k licensing, $15k professional services, $850 utilities, and $600 software and ground-penetrating radar (GPR) subscriptions. That adds to about $134.5k/month; the stated $1,475k total should be reconciled before you set distributable income.

Year 1 payroll is $547k, and the model flags $547k minimum cash need in Month 2. Reserves protect against claims, permit delays, equipment repairs, and slow collections, so they directly affect whether the owner can take a draw or has to hold cash in the business.

Protect Cash Before Owner Draw

Track each overhead line monthly and tie it to completed jobs, not booked jobs. If insurance or rent rises faster than permit volume, owner income falls. Watch the cash balance against the $547k Month 2 need, plus open receivables, before approving distributions.

No reserve, no draw. Keep claims files, renewal dates, and repair spend documented, then update the cash forecast every week. That way, slow collections or a stuck project do not hit payroll first and wipe out the owner’s take-home pay.

5

Lead Generation And Owner Role

Lead Generation and Owner Time

This driver covers lead flow, close rate, and how much the owner stays in the field versus selling and managing. Marketing budget rises from $45k in Year 1 to $110k in Year 5, while CAC improves from $1,500 to $1,300. That helps revenue, but only if qualified leads turn into permitted jobs and crew time stays booked.

Here’s the tradeoff: owner-operated field work can preserve cash because replacement labor is lower, but it can cap estimating, scheduling, and sales. If the owner shifts to selling and managing, revenue capacity can rise, yet crew utilization has to stay high or fixed overhead and payroll will eat profit. The key inputs are lead source, qualified opportunities, conversion, and owner hours.

Track Source, Close Rate, and Owner Hours

Measure leads by source: property-transfer work, environmental consultants, real estate professionals, and commercial site owners. Then track cost per acquired customer (CAC), estimate time, close rate, and the share of jobs the owner touches. If one source brings cheap leads but slow closes, it can still hurt cash flow and owner pay.

Use a simple rule: if the owner is in the field, sales time shrinks; if the owner is selling, field coverage must not slip. The best test is booked jobs per month per marketing dollar and per owner hour. That shows whether more spend is buying real profit, not just busier calendars.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Income shifts with crew utilization, permit work, and how fast larger jobs fill the calendar. Early cash is strong, but owner pay still depends on compliance costs and equipment uptime.

| Scenario | Low CaseCash-heavy | Base CaseCompliance-sensitive | High CaseUtilization-driven |

|---|---|---|---|

| Launch model | This is the early-ramp case, where Year 1 EBITDA capacity is about $1.316M. | This is the modeled middle path, where Year 3 EBITDA capacity is about $4.806M. | This is the stronger earnings path, where Year 5 EBITDA capacity reaches about $8.865M. |

| Typical setup | Revenue is about $3.078M, volume is around 128 tank removals a month, gross margin is near 70.5%, and minimum cash sits near $547k. | Revenue reaches about $8.056M, volume is around 295 tank removals a month, gross margin is near 73.3%, and the team is sized for more permitting and field work. | Revenue climbs to about $13.722M, gross margin is near 76.5%, and crew, engineer, and coordinator capacity expands to keep jobs moving. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $1.316MEarly ramp | $4.806MCore case | $8.865MUpside case |

| Best fit | Use this to stress-test launch-month cash and slow ramp-up. | Use this as the planning case for normal growth and steady utilization. | Use this to test upside when jobs stay full and compliance bottlenecks stay light. |

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or owner distributions. They are before taxes, debt service, reserves, and owner-specific draws.

Related Products

- Underground Fuel Tank Removal Porter's Five Forces Analysis

- Underground Fuel Tank Removal BCG Matrix

- Underground Fuel Tank Removal Business Model Canvas

- What Five KPIs Should Underground Fuel Tank Removal Business Track?

- Underground Fuel Tank Removal Business Plan Template in Pre-Written Word

- How Increase Underground Fuel Tank Removal Profits?

- What Are Operating Costs For Underground Fuel Tank Removal?

- Underground Fuel Tank Removal Startup Costs: $547K Cash Need

- Underground Fuel Tank Removal Financial Model Template in Excel

- How To Start An Underground Fuel Tank Removal Business In 60-120 Days

- How To Write An Underground Fuel Tank Removal Business Plan?

- Underground Fuel Tank Removal Marketing Mix

- Underground Fuel Tank Removal Marketing Plan

- Underground Fuel Tank Removal Business Proposal

- Underground Fuel Tank Removal PESTEL Analysis

- Underground Fuel Tank Removal Pitch Deck Example Editable PPTX

- Underground Fuel Tank Removal Business SWOT Analysis

- Underground Fuel Tank Removal Value Proposition Canvas

Frequently Asked Questions

Under the researched assumptions, the business reaches $3078M revenue and $1316M EBITDA in Year 1 By Year 5, revenue reaches $13722M and EBITDA reaches $8865M That is pre-tax operating profit capacity, not guaranteed owner take-home, and it excludes debt service, reserves, capex, and owner-specific distributions