Owner income-$1K to $4.27M

Owner income-$1K to $4.27MHow Much General Contractor Owners Make In A $150K Salary Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income-$1K to $4.27M  Net marginEBITDA: -39% to 71%

Net marginEBITDA: -39% to 71% Revenue for target pay≈$982K

Revenue for target pay≈$982K Business difficultyHard

Business difficultyHard

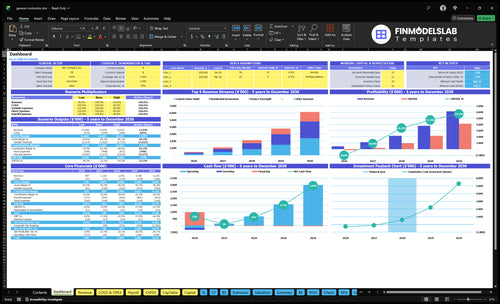

You’re planning owner pay before the jobs, payroll, and cash timing are fully proven In this five-year model, the Principal / Lead GC has a $150,000 annual salary, while EBITDA moves from -$151,000 in Year 1 to $4124 million in Year 5 These are researched planning assumptions, not guaranteed earnings, tax advice, or required distributions

Owner income-$1K to $4.27MNet marginEBITDA: -39% to 71%Revenue for target pay≈$982KBusiness difficultyHardWant to estimate contractor take-home pay?

Owner income calculator

Estimate owner take-home and target-pay gap from annual project revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It uses the model anchors for 76% to 85% contribution margin, $996K fixed overhead, $700K to $3.425M payroll, Month 15 breakeven, and $641K minimum cash need. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to test owner income in the General Contractor model?

Open the General Contractor Financial Model Template to test revenue, margin, costs, reserves, and owner take-home assumptions. EBITDA moves from -$151K in Year 1 to $4.124M in Year 5.

Owner-income model highlights

- Month 15 breakeven

- 29-month payback

- $641K minimum cash

- Scenario testing first

How much do small general contractor owners make?

Small general contractor owners can take home about the value of their own labor first, which in this model starts at $150K for the Principal / Lead GC in Year 1. But capacity is capped by estimating, site supervision, and admin time, so once you add a $110K Senior Project Manager, $50K Office Administrator, and half-time $65K Project Coordinator, short-term take-home gets tighter even as output grows.

Year 1 pay mix

- $150K Principal / Lead GC

- $110K Senior Project Manager

- $50K Office Administrator

- Half-time $65K Project Coordinator

Scale effect

- Owner labor replacement lowers cash pay

- Capacity rises with more payroll

- $700K total wages by Year 5

- Distributions depend on margin staying strong

Why do general contractors have cash flow problems?

General contractors run into cash flow problems because profit and cash arrive on different clocks: payroll, supplier bills, insurance, travel, quality control, and retainage can hit before client payments do. In this model, the source case shows month 15 breakeven but a $641K minimum cash need in month 16, so a job can look profitable and still strain cash. The first year also needs $153K in capex for office setup, hardware, vehicles, tools, website, collateral, and network infrastructure, and reserves usually cut current distributions but protect payroll and project delivery.

Why cash gets tight

- Payroll comes before payment.

- Supplier bills arrive fast.

- Retainage delays cash.

- Client timing can slip.

What the numbers show

- Month 15 is breakeven.

- Month 16 needs $641K.

- First-year capex is $153K.

- Reserves protect delivery.

How much revenue does a general contractor need to make money?

A General Contractor needs about $582K in annual revenue to break even, based on $442.1K of fixed overhead, non-owner payroll, owner salary, reserves, and debt service divided by a 76% contribution margin. To actually make money, the model needs to move closer to Year 2 revenue of $982K, which produces about $213K EBITDA; track this with What Is The Most Critical Measure To Gauge The Success Of Your General Contractor Business?.

Break-Even Math

- 76% contribution margin after variable costs

- $442.1K annual fixed cash needs

- $582K break-even revenue target

- $383K Year 1 revenue leaves a funding gap

Profit Target

- Cover margin leakage first

- Fund non-owner payroll before owner draws

- Include reserves and debt service

- $982K Year 2 revenue supports $213K EBITDA

Want to see the main income drivers?

1

$383K-$5.8MAnnual Volume

Signed work moves revenue from about $383K in Year 1 to $5.8M in Year 5, so pipeline depth is the main driver of owner take-home.

2

76%-85%Bid Margin

Holding contribution margin in the 76% to 85% band turns sales into owner cash instead of just more payroll.

3

4%-7%Job Costs

Project software and outside quality control run 4% to 7% of revenue, so cost slips hit take-home fast.

4

$343K-$700KLabor Load

Fixed overhead is about $99.6K a year, but payroll rises from roughly $343K to $700K, so staffing choices move profit most.

5

$135-$160/hrMix Capacity

The mix shifts toward higher-rate custom home work and oversight, lifting the blended billable rate and keeping crews scheduled.

6

$641KWorking Capital

Breakeven lands in Month 15, but cash still dips to $641K in Month 16, so reserves decide how smoothly growth runs.

General Contractor Core Six Income Drivers

Annual Project Volume

Annual Project Volume

Annual project volume is the number of jobs finished and billed in a year. It lifts owner pay only when each project clears direct cost, supervision, and overhead; otherwise, more work just adds strain. The model implies revenue rises from about $383K in Year 1 to $579M in Year 5, while EBITDA (cash-style operating profit) moves from -$151K to $4.124M.

Track signed backlog, completed revenue, average contract value, and active project count. The risk is chasing low-margin volume that ties up project manager time and cash, which can leave less for owner distributions after overhead and reserves.

Track Volume That Pays

Use a simple test: if one more job raises revenue but cuts margin, cash, or schedule control, it is not good volume. Count jobs started, finished, and delayed, then compare those counts to margin by project type. That shows whether growth is creating profit or just activity.

Set a monthly cap on active projects per project manager and reject bids that do not cover supervision and cash timing. Here’s the quick math: higher completed revenue helps owner income only after overhead and reserves are funded, so volume should be managed for profit, not just top-line growth.

- Measure backlog against finish rate

- Watch margin by project type

- Limit active jobs per manager

- Protect cash before adding volume

1

Bid Pricing And Gross Margin Discipline

Bid Pricing Discipline

Your bid sets owner pay before the job starts. A solid bid covers direct job costs, contingency, supervision, overhead contribution, and profit. In this model, direct COGS falls from 7% of revenue in Year 1 to 4% in Year 5, so gross margin rises from 93% to 96%. If pricing misses any layer, EBITDA and owner draws shrink fast.

After marketing and travel, contribution margin improves from 76% to 85%. That is the cash left to pay office costs and the owner. A markup is not net profit; it is just the add-on above direct cost. Missed scope, weak change orders, and underpriced supervision are the usual leak points.

Price the Work, Not the Guess

Track bid price against these inputs: direct labor, subcontractors, materials, contingency, supervision, marketing, travel, and fixed overhead. One clean formula helps: bid price = direct job costs + contingency + supervision + overhead contribution + profit. If actual job cost runs 1% high, the hit comes straight out of gross profit and owner pay.

- Log scope gaps before signing.

- Price supervision as a real cost.

- Approve change orders in writing.

- Review job cost weekly.

Use change-order logs and job-cost reports weekly. Write scope in plain language, and refuse work that cannot clear your target gross margin. One line to remember: if the bid cannot fund the project manager, it is underpriced.

2

Direct Job Cost Control

Direct Job Cost Control

Direct job cost control is the grip on subcontractor pricing, materials, labor timing, project software, external quality control, rework, and change orders (scope changes billed to the client). When these costs drift, gross profit drops fast: a 1% cost overrun cuts profit by about $98K at Year 2 revenue and $579K at Year 5 revenue, which directly reduces cash available for owner pay.

The main inputs are contract value, subcontract bids, material takeoffs, labor hours, QC spend, software spend, and rework rate. The model puts project-specific software at 4% to 2% of revenue and external quality control at 3% to 2%. One-liner: small cost leaks become big owner-income leaks.

Track the cost leak weekly

Use a job-cost sheet that compares budget vs actual for labor, subs, materials, software, QC, and rework. Track cost overrun %, change-order recovery, and gross profit by job so you can see which projects protect owner distributions and which ones quietly burn cash.

- Lock subcontractor quotes early.

- Match buys to the schedule.

- Approve change orders before work starts.

- Check rework on every closeout.

If software and QC stay inside the 4% to 2% and 3% to 2% ranges, the business keeps more gross profit and the owner can take steadier draws without starving the next job.

3

Overhead And Staffing Structure

Overhead And Staffing Load

Owner take-home is what is left after gross profit pays office rent, utilities, insurance, software, professional services, vehicles, and payroll. The model sets fixed overhead at $83K per month or $996K per year, so the business must clear that before owner pay starts. One clean rule: if gross profit slips, the owner gets paid last.

The staffing plan adds project management, estimating, coordination, admin, and marketing. The model lists payroll at $3,425K in Year 1 and $700K in Year 5, so check the ramp carefully because headcount changes cash needs fast. More staff helps capacity, but it also locks in monthly cash outflow.

Track Overhead Before You Add Headcount

Measure overhead as a share of monthly gross profit, not revenue. Here’s the quick math: gross profit - fixed overhead = cash available for the owner. If that spread stays thin, hiring another estimator or coordinator can push owner pay out even when sales look strong.

- Track rent, software, vehicles.

- Approve hires from backlog coverage.

- Budget payroll by role.

- Review monthly cash, not annual profit.

Test each new role against booked work, not hoped-for work. If project volume slows, trim discretionary spend first and protect the roles tied to estimating, project control, and collections so overhead supports delivery without starving the owner’s draw.

4

Project Mix And Scheduling Capacity

Project Mix and Schedule Load

Project mix drives owner income because it changes how much revenue each job can support, how much supervision it needs, and how many jobs can run at once. In this model, the mix shifts from 60% residential renovation, 25% custom home build, and 15% project oversight in Year 1 to 40%, 45%, and

Here’s the quick math: weighted priced hours rise from about $7,455 to $12,790 per customer unit using model hours and hourly prices. That helps revenue, but only if subcontractor availability, owner approvals, and schedule gaps stay tight. If jobs stall, cash comes in later and the owner’s draw gets squeezed even when booked revenue looks strong.

Track Capacity, Not Just Backlog

Measure concurrent active jobs, approval cycle time, and subcontractor fill rate on every project. If a renovation needs fewer priced hours but more hand-holding, it can still hurt margin by tying up the owner and project manager. The goal is to keep the mix that lifts revenue per job without creating dead time between trades.

Use a simple schedule test: when a job slips, log the cause, the days lost, and the cash delay. Then compare planned versus actual hours by project type. A one-line rule helps: more custom-home work means more supervision, more timing risk, and bigger cash swings, so price that load before it hits owner pay.

- Track approved hours by project type.

- Watch subcontractor gaps weekly.

- Price owner approvals into the schedule.

5

Reserves And Working Capital

Working Capital Reserve

Owner pay here depends on how much profit must stay in the business to cover payroll timing, supplier bills, retainage (cash held back until closeout), warranties, future bids, and slow collections. The model shows Month 15 breakeven, a 29-month payback, and a $641K minimum cash need in Month 16. That means profit on paper is not fully available for draw.

Cash first, owner draw second. First-year capex of $153K, including two company vehicles and office setup, also pulls cash out before it can reach the owner. If billing lags or collections stretch, take-home income drops even when projects are profitable, because the reserve has to stay in the business to keep jobs moving.

Track the Cash Gap

Build the reserve from the timing inputs that actually move cash: billings by month, collect days, retainage %, payroll dates, supplier due dates, warranty holdback, and capex. Days sales outstanding (DSO) is the average days from invoice to cash, and it matters here because slower cash-in means less owner income available now.

- Watch weekly cash balance

- Separate reserve from draw

- Pause draws if cash dips

- Track retainage aging closely

- Forecast payroll before billing

Use the $641K Month 16 cash need as the floor, not the target for extra spending. If collections speed up, reserve pressure eases and owner pay can rise; if they slow, profit must stay inside the business so you don’t miss payroll or delay jobs.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner pay swings a lot here because the model starts with a Year 1 loss, then scales to strong EBITDA as revenue climbs from about $383K to $5.79M.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | The owner stays near a funded salary path while the business runs at a Year 1 loss. | The owner gets a modeled salary plus growing profit as the business moves into positive EBITDA. | The owner takes a stronger income path as the business reaches mature-year scale and larger EBITDA. |

| Typical setup | Revenue is about $383K, contribution margin is about 76%, and fixed wage load is about $442.1K, so cash support is still needed. | Revenue rises to about $1.96M, contribution margin is about 80.5%, and fixed wage load is about $624.6K, which supports a steadier draw. | Revenue reaches about $5.79M, contribution margin is about 85%, and fixed wage load is about $799.6K, leaving more room for owner pay and reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $150,000Low income | $150,000 - $300,000Base income | $300,000 - $600,000High income |

| Best fit | Use this if you want a conservative start-up case with funding still required. | Use this as the main planning case for a staffed, growing contractor. | Use this to test upside if volume stays strong and overhead stays controlled. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- General Contractor Porter's Five Forces Analysis

- General Contractor BCG Matrix

- General Contractor Business Model Canvas

- 7 Essential KPIs for General Contractor Success

- General Contractor Business Plan Template in Pre-Written Word

- 7 Strategies to Increase General Contractor Profitability

- Calculating the Monthly Running Costs for a General Contractor Business

- General Contractor Startup Costs: $153K Assets And $641K Cash Need

- General Contractor Financial Model Template in Excel

- How to Start a General Contractor Business in 8–16 Weeks

- How to Write a General Contractor Business Plan in 7 Steps

- General Contractor Marketing Mix

- General Contractor Marketing Plan

- General Contractor Business Proposal

- General Contractor PESTEL Analysis

- General Contractor Pitch Deck Example Editable PPTX

- General Contractor Business SWOT Analysis

- General Contractor Value Proposition Canvas

Frequently Asked Questions

In this model, the owner role is planned at a $150,000 annual salary Business profit is separate: EBITDA is -$151,000 in Year 1, $213,000 in Year 2, and $4124 million in Year 5 Extra distributions depend on cash reserves, debt, taxes, and reinvestment needs