Owner income$0 to $135K

Owner income$0 to $135KHow Much Can A Germicidal UV Light Systems Owner Make On $409K+ Revenue?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0 to $135K  Net margin-79% to 27%

Net margin-79% to 27% Target pay revenue≈$1.34M

Target pay revenue≈$1.34M Business difficultyHard

Business difficultyHard

You’re planning owner pay before the business has steady commercial installations, service work, and cash reserves This US planning view covers $409K in Year 1 revenue to $2769M in Year 5 revenue, with costs, margins, overhead, payroll, reserves, and the modeled $135K CEO and Lead Engineer salary It excludes personal taxes, debt terms, and any guaranteed distribution claim

Owner income$0 to $135KNet margin-79% to 27%Target pay revenue≈$1.34MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, debt, reserves, and distribution policy. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the full forecast view on owner income?

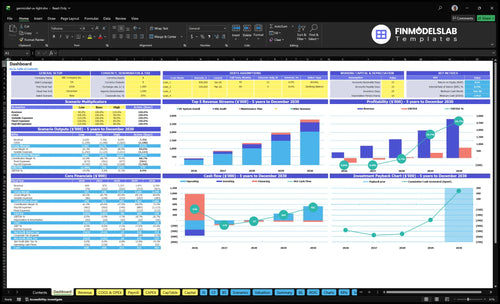

The Germicidal UV Light Systems Financial Model Template screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions—open the model.

Owner-income model highlights

- Owner income by scenario

- Assumptions drive each case

- Revenue: $409K, $870K, $1,337M, $1,971M, $2,769M

- Equipment, consumables: 180%-152%

- Commissions, vehicle costs: 100%-84%

- Overhead $1,122K; cash $179K

- Marketing $45K-$150K; capex $2,215K

What margins do germicidal UV light systems businesses make?

Germicidal UV Light Systems can show very high modeled margins: source assumptions put gross margin after UV lamps, hardware, and consumables at 820% in Year 1 and 848% in Year 5, while contribution margin after commissions, fuel, and vehicle maintenance rises from 720% to 764%; see How Increase Germicidal UV Light Systems Profitability? for the main margin levers.

Gross margin drivers

- 820% Year 1 gross margin

- 848% Year 5 gross margin

- Fixture cost changes the spread

- Lamp, ballast, and controls matter

Cash margin risks

- 720% Year 1 contribution margin

- 764% Year 5 contribution margin

- Shipping and subcontracted electrical work hit cash

- Markup is not pure income

Can UV disinfection maintenance contracts increase owner income?

Yes—maintenance contracts can add steadier income for Germicidal UV Light Systems, but they only work if labor stays tight. At 25 billable hours per service event and $125 an hour in Year 1, that’s about $31,250 before costs; at $145 in Year 5, it rises to $36,250. The catch is simple: recurring work cuts reliance on new installs, but it still carries payroll, overhead, and renewal risk.

Income stays steadier

- 25 hours per service event

- $31,250 Year 1 revenue

- $36,250 Year 5 revenue

- Less dependence on new installs

Labor still matters

- Maintenance plan allocation rises from 600% to 900%

- Includes lamp replacement and cleaning

- Includes output testing and compliance docs

- Includes inventory, travel, and scheduling risk

How much revenue does a UV disinfection business need to pay the owner?

If you want the owner to take $100K in Year 1 at Germicidal UV Light Systems, the business needs about $725K in revenue before taxes and debt, using 72% contribution margin and $265K payroll, $112K overhead, and $45K marketing. If owner pay rises to $135K, the need moves to about $774K. With planned Year 1 revenue at $409K, early owner pay depends on capital reserves; one 40-hour install block at $165/hour brings $6,600 before equipment and service add-ons.

Owner pay math

- $725K funds $100K owner pay.

- $774K funds $135K owner pay.

- 72% margin drives both estimates.

- Revenue is before taxes and debt.

Year 1 cash gap

- Planned revenue is only $409K.

- Owner pay likely needs reserves.

- One install block = $6,600.

- Equipment and service add-ons lift each job.

Want the six main income drivers?

1

$409K-$2.77MProject Volume

More installs and bigger jobs lift revenue from $409K in Year 1 to $2.77M in Year 5, so this is the main path to owner pay.

2

72%-76%Parts Margin

Better buying on lamps and hardware lifts contribution margin from 72% to 76%, so more of each sale reaches owner pay.

3

$2.5K-$1.6KLead Flow

Marketing rises from $45K to $150K while CAC falls from $2.5K to $1.6K, so each lead should cost less as scale builds.

4

12-18hRecurring Work

More maintenance-plan customers push billable hours per active customer from 12 to 18, so revenue keeps coming after install.

5

40h-32hInstall Speed

Install labor drops from 40 hours to 32 hours per job, so the same crew keeps more margin on each sale.

6

$179KCash Buffer

Cash bottoms at $179K in Month 30, so owner draw stays tight until the business clears its fixed overhead.

Germicidal UV Light Systems Core Six Income Drivers

Commercial Installation Project Volume And Contract Size

Commercial Install Volume

More qualified installs lift revenue, but sales cycles, site assessments, facility access, and crew capacity cap how fast that turns into owner pay. The model’s source revenue rises from $409K in Year 1 to 2769M in Year 5, while install allocation moves from 450% to 350% as maintenance mix expands. One clean win beats three underpriced jobs that clog the schedule.

- Track qualified site assessments.

- Watch average installed contract value.

- Price complex facilities separately.

- Protect crew time from idle gaps.

Price the Hard Jobs Right

Here’s the quick math: install assumptions move from 40 hours at $165/hour to 32 hours at $185/hour. That is $6,600 per job before overhead, then $5,920 per job in the later case. Faster installs do not fix weak pricing; profit still depends on scope control, access windows, and avoiding rework on complex facilities.

- Measure quote-to-close by facility type.

- Separate standard from complex sites.

- Review margin after commissioning.

- رفض underpriced custom work.

1

Equipment Margin And Vendor Purchasing Power

Equipment Margin and Vendor Power

This driver is the gap between what you bill for a UV install and what the lamps, hardware, and consumables actually cost. In the model, UV lamps and hardware sit at 140% of revenue in Year 1 and ease to 120% by Year 5, while consumables fall from 40% to 32%, so vendor pricing has a direct line to gross profit and owner pay.

What can eat the gain is cash leakage: shipping, warranty parts, damaged fixtures, controls, and lamp replacements. If those creep up, the business can book sales but still feel tight on cash; the model’s contribution margin moves from 720% to 764% when pricing discipline holds.

Track Landed Cost Per Install

Measure landed equipment cost per job: vendor price, freight, damage, warranty swaps, and replacement parts. Compare that to quoted price on every install so you can see margin drift before it hits owner pay. One bad pricing cycle can wipe out the benefit of a stronger sales month.

- Log cost by install.

- Separate freight from equipment.

- Track warranty claims monthly.

- Requote if vendor prices move.

- Watch lamp replacement rates.

2

Installation Labor Productivity And Crew Utilization

Installation Labor Productivity

The key metric is crew utilization, meaning billable install hours divided by paid hours. Here’s the quick math: labor revenue per job moves from 40 × $165 = $6,600 in Year 1 to 32 × $185 = $5,920 in Year 5, a drop of about 10.3%. So the owner’s income depends on keeping travel, rework, and idle days from eating that spread.

Technician staffing grows from 1 to 5 FTE at $72K each, or $360K in annual payroll before subcontracted electrical work. Keep owner design and commissioning separate from field labor, or the job looks more profitable than it is. One stalled install day can erase a lot of gross margin.

Crew Utilization Controls

Track billable hours, drive time, access windows, and first-pass completion. Split each job into owner design, technician install, subcontract electrical, and commissioning. If commissioning slips or the site is not ready, payroll keeps running while cash collection waits, and that cuts owner draw fast.

- Book access windows before dispatch.

- Charge standby and rework time.

- Forecast payroll against booked jobs.

- Separate owner hours from field labor.

3

Recurring Service, Maintenance, And Lamp Replacement

Recurring Service, Maintenance, And Lamp Replacement

When new installs slow, recurring service keeps cash moving. At 25 billable hours, monthly service revenue is $3,125 at $125/hr and $3,625 at $145/hr. That steadier base helps the owner pay wages, cover travel, and draw profit, but only if retention stays high and technicians stay scheduled.

The model’s maintenance allocation rises from 600% in Year 1 to 900% in Year 5, so service matters more as the business matures. What this estimate hides is the cost of lamp inventory, site visits, and rework. If a contract loses even one visit, the gain in revenue can disappear fast.

Track the service mix and renewal rate

Track service hours by job type, not just total hours. Separate lamp replacement, cleaning, irradiance testing, documentation, and preventive maintenance so you can price each visit and see which ones actually cover labor, parts, and travel. If a route needs too many miles or parts pulls, the hourly rate won’t protect margin.

Hold a schedule of recurring visits and keep spare lamps on hand. The owner income lever is simple: more billable hours at $145 beats idle tech time at $125. Watch contract renewal rate, missed visits, and part usage per site; those three numbers tell you whether service is adding profit or just adding work.

4

Lead Generation, Channel Partnerships, And Close Rate

Pipeline Quality and Close Rate

Lead generation drives owner income by filling the pipeline with qualified commercial and regulated accounts, not just names. In this model, close rate means the share of qualified opportunities that become paying jobs. Marketing spend rises from $45K in Year 1 to $150K in Year 5, while CAC improves from $2,500 to $1,600; better conversion supports more revenue without the same spend growth.

Do not assume quick cash. Site audits, budget approvals, safety reviews, and procurement can stretch timing, so a strong pipeline matters as much as lead count. Channels like facility managers, HVAC contractors, healthcare buyers, labs, schools, and food processing accounts can improve fit, but weak qualification raises travel, bid, and follow-up work that does not pay back.

Track Qualified Pipeline by Channel

Measure qualified leads, stage-to-stage conversion, CAC, and days from audit to close. If CAC drops from $2,500 to $1,600, the owner keeps more margin only when the team stops chasing low-fit sites and ties spend to a ccounts with budget, access, and clear compliance needs.

Keep a simple forecast by channel: facility managers, HVAC contractors, healthcare buyers, labs, schools, and food processing. One clean rule: no audit, no forecast. That protects cash flow, because close timing can lag marketing spend by weeks or months in regulated sites.

- Track audit-to-close days.

- Score budget and access.

- Separate CAC by channel.

- Log lost deals by reason.

5

Overhead, Compliance, Insurance, Reserves, And Owner Role

Overhead, Reserves, And Owner Draw

Operating profit is not owner take-home here. With fixed overhead at $935K per month and professional liability insurance at $14K per month, the business has a heavy fixed load before any owner pay. Payroll starts at $400K in Year 1 and rises to $856K in Year 5, so the owner’s income depends on margin staying above these recurring costs.

Capex totals $2.215M for vehicles, testing tools, inventory, demo units, IT, and systems, and minimum cash must hold at $179K in Month 30. That reserve protects warranty claims, inventory buys, payroll, and slow collections. If cash drops first, owner draws get cut even when the income statement still shows profit.

Protect Cash Before Paying the Owner

Track owner pay against fixed overhead, insurance, payroll, and the $179K cash floor. The owner should only take draws after those costs and reserve targets are covered. If receivables slow or warranty work spikes, cash can tighten fast even when jobs are booked and reported profit looks fine.

- Separate draw from operating profit.

- Review reserves every month.

- Forecast payroll 12 months ahead.

- Hold cash for slow collections.

Use a simple test: if one large customer pays late, can the business still fund payroll, insurance, and vendor bills without touching owner pay? If not, the draw is too high and the reserve plan is too thin.

6

Scenario objective: Compare lean, base, and high owner-income outcomes for a UV disinfection business

Owner income scenarios

Owner income changes fast here because revenue ramps over time, payroll scales with installs, and fixed overhead is heavy early. Break-even arrives around month 30, so cash support matters before draw room opens.

| Scenario | Low CaseCash strain | Base CaseBreak-even turn | High CaseMature capacity |

|---|---|---|---|

| Launch model | The early ramp keeps owner pay under pressure and may not support a full draw. | The modeled base case reaches a steadier owner pay path as the business crosses break-even. | The high case assumes a mature operating year with stronger earnings and room for distributions. |

| Typical setup | Year 1 revenue is about $409K, contribution margin is 72.0%, fixed overhead is about $1.122M, with $45K marketing and about $400K payroll, so EBITDA is roughly -$263K. | Year 3 revenue is about $1.337M, contribution margin is 74.2%, marketing is $90K, payroll is about $604K, and EBITDA is about $50K. | Year 5 revenue is about $2.769M, contribution margin is 76.4%, marketing is $150K, payroll is about $856K, and EBITDA is about $741K. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary at riskDownside case | $135,000 salaryLimited draw room | Salary plus distributionsUpside case |

| Best fit | Use this to test a funded launch and the downside if sales lag. | Use this for a funded plan that supports owner salary but leaves little room for distributions. | Use this to test mature operations with cash left after taxes, debt, reserves, and reinvestment. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Germicidal UV Light Systems Porter's Five Forces Analysis

- Germicidal UV Light Systems BCG Matrix

- Germicidal UV Light Systems Business Model Canvas

- What Are The 5 KPIs For Germicidal UV Light Systems Business?

- Germicidal UV Light Systems Business Plan Template in Pre-Written Word

- How Increase Germicidal UV Light Systems Profitability?

- What Are Germicidal UV Light Systems Operating Costs?

- Germicidal UV Light Systems Startup Costs: Plan On $2215K CAPEX

- Germicidal UV Light Systems Financial Model Template in Excel

- How To Open A Germicidal UV Light Systems Business In 8–16 Weeks

- How To Write A Business Plan For Germicidal UV Light Systems?

- Germicidal UV Light Systems Marketing Mix

- Germicidal UV Light Systems Marketing Plan

- Germicidal UV Light Systems Business Proposal

- Germicidal UV Light Systems PESTEL Analysis

- Germicidal UV Light Systems Pitch Deck Example Editable PPTX

- Germicidal UV Light Systems Business SWOT Analysis

- Germicidal UV Light Systems Value Proposition Canvas

Frequently Asked Questions

The model includes a $135K CEO and Lead Engineer salary, but that does not mean the business can always fund it from operations Year 1 revenue is $409K, and estimated EBITDA is about -$263K By Year 5, revenue reaches $2769M with about $997K estimated EBITDA before taxes, debt, reserves, and distributions