Owner income$120k base

Owner income$120k baseHow Much Rooftop Garden Installation Owners Make: $120k+ Pay

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$120k base  Net margin41%

Net margin41% Revenue for target pay$1.43M

Revenue for target pay$1.43M Business difficultyMedium

Business difficultyMedium

You’re pricing complex roof work before you know what the owner can safely pull out This guide covers $120,000 planned owner salary, project revenue, margins, costs, reserves, and EBITDA, meaning operating profit before interest, taxes, depreciation, and amortization, across a five-year model period

Owner income$120k baseNet margin41%Revenue for target pay$1.43MBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay. It also shows revenue, gross profit, EBITDA, retained cash, and owner take-home before taxes.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

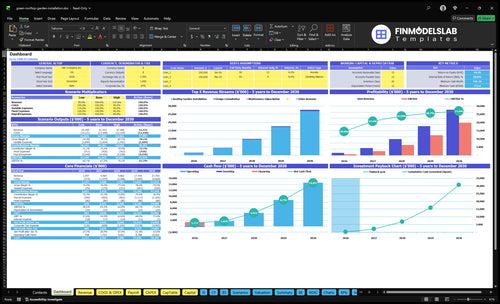

Want to check owner income in the full Rooftop Garden Installation model?

This dashboard shows revenue, margin, costs, reserves, and owner pay assumptions in the Rooftop Garden Installation Financial Model Template—open it.

Model highlights

- Owner pay and income outputs

- Revenue, pipeline, and direct costs

- Cash runway, Month 4 breakeven

- EBITDA, 10-month payback

- Minimum cash: $773,000

Can a rooftop garden installation business scale profitably?

Yes — Rooftop Garden Installation can scale profitably, but only if project volume, quality control, cash deposits, and labor scheduling improve together. The model reaches breakeven in Month 4 and payback in 10 months, but it also needs $773,000 minimum cash and $280,000 in first-year capex. A lean owner-operated setup protects margin, while a crew model adds capacity; installation technicians rise from 2 FTEs in Year 1 to 6 FTEs in Year 5.

What supports scale

- Push project volume up.

- Keep quality control tight.

- Use cash deposits early.

- Match jobs to labor schedules.

What can hurt profit

- Roof access can slow jobs.

- Weather can delay installs.

- Warranty callbacks add cost.

- Project management gets messy fast.

What is the profit margin for a rooftop garden installation business?

Rooftop Garden Installation can run at about 72% contribution in Year 1 before payroll, rent, marketing, admin, and owner pay, because direct costs are 28%. By Year 5, if direct costs fall to 22.6%, contribution rises to 77.4%; for startup cost context, see How Much Does It Cost To Open And Start Your Rooftop Garden Installation Business?. Here’s the quick math: 18% materials, 7% subcontracted labor, 2% equipment rental, and 1% travel and logistics.

Year 1 cost mix

- 18% materials

- 7% subcontract labor

- 2% equipment rental

- 1% travel and logistics

Main margin risks

- Underbidding kills profit

- Rooftop access delays add cost

- Plant replacement cuts margin

- Poor scheduling creates rework

How much can I pay myself from a rooftop garden installation business?

You can pay yourself a modeled $120,000 CEO / Lead Designer salary from a Rooftop Garden Installation business, but treat that as owner labor pay, not profit. Year 1 shows $578,000 EBITDA before taxes, debt, depreciation, and owner distributions; see What Is The Most Important Measure Of Success For Your Rooftop Garden Installation Business? before taking extra cash out. Cash is tighter than profit because Year 1 includes $280,000 capex and a $773,000 minimum cash need in Month 2.

Pay Yourself First

- Set salary at $120,000

- Book it as labor cost

- Keep distributions separate

- Pay taxes before profit draws

Protect Cash

- EBITDA: $578,000

- Capex: $280,000

- Month 2 cash need: $773,000

- Owner overwork can cap growth

Want the six main income drivers?

1

120hProject Volume

Each completed install is about 120 billable hours in Year 1, so more finished roofs push revenue and owner cash faster.

2

$18KContract Size

At 120 hours at $150, a Year 1 install lands near $18K, so pricing discipline keeps each job profitable.

3

72%Gross Margin

Direct costs run about 28% of install revenue, so protecting the 72% contribution is the fastest way to lift take-home.

4

$337.5KLabor Efficiency

Year 1 payroll is $337.5K, so crew mix and subcontract control decide how much revenue survives.

5

$7.1K/moOverhead Use

Fixed overhead is $7.1K a month, so filling that base cost with more project work raises cash left for the owner.

6

$120KOwner Draw

The $120K owner salary is direct take-home, but it only works if cash stays above the $773K minimum.

Rooftop Garden Installation Core Six Income Drivers

Completed Project Volume

Completed Project Volume

Completed, billed, and collected installs are what pay the bills. In a rooftop garden installation business, more finished projects spread the $7,100 monthly fixed overhead and the $25,000 Year 1 marketing cost across more revenue, so owner income rises only when jobs actually close and cash comes in. Leads alone do not change pay.

Here’s the risk: weather, roof access, permits, and client approvals can push completion into later months, which delays profit and owner draw. Track projects per month, close rate, installation capacity, deposit timing, and collection timing so you can see whether volume is real or just pipeline noise.

Track Cash, Not Just Leads

Use a simple weekly roll-forward: sold, started, completed, billed, and collected. That shows where income is stalling. If completed jobs pile up but invoices lag, cash flow stays tight even when sales look strong.

- Count completed jobs only.

- Separate billed from collected.

- Watch deposit timing.

- Match crew capacity to installs.

One clean rule: if volume rises but completion slips, margin can look fine on paper while owner pay gets delayed. Tight scheduling and faster approvals protect monthly cash more than more leads do.

1

Average Contract Size

Average Contract Size

Average contract size is the average revenue per rooftop garden job, and it drives how fast owner income grows. In Year 1, the model starts at $18,000 per project from 120 billable hours × $150. By Year 5, it rises to $32,400 from 180 hours × $180, so bigger jobs can lift revenue without more project count.

That only helps if margin holds. Larger commercial roofs, design-build packages, irrigation, and maintenance add-ons can raise ticket size, but complex access, structural coordination, and longer schedules can push labor and subcontract costs up. One clean rule: price for margin and crew capacity, not just top-line sales.

Price by hours, not hope

Track billable hours, realized hourly rate, and gross margin per job. Here’s the quick math: $18,000 ÷ 120 hours = $150 per billable hour in Year 1, and $32,400 ÷ 180 hours = $180 per billable hour in Year 5. If a larger roof adds hours faster than price, owner pay gets squeezed even when sales look stronger.

Use a job sheet that separates base install, design-build, irrigation, and maintenance add-ons. Price each scope item against crew time, subcontractor use, and schedule risk. If access is tight or structural coordination is heavy, build in more labor and contingency. That protects cash flow and keeps profit from slipping into rework and delay.

- Track hours by job type

- Price add-ons separately

- Test margin on larger roofs

2

Gross Margin Control

Gross Margin Control

Gross margin is what’s left after direct job costs like plants, soil media, irrigation, drainage, subcontracted labor, equipment rental, and travel. For rooftop garden installs, the Year 1 benchmark is 28% direct cost, so 72% of revenue is left before overhead. That’s the pool that pays rent, payroll, and owner draw. One bad job can erase several good ones fast.

By Year 5, the disclosed direct costs rise to 226% of revenue, which means the job loses money before fixed costs. Here’s the quick math: every $1.00 billed needs more than $2.00 in direct spend, so callbacks, rework, plant loss, and underbidding hit cash flow hard. If payroll and rent stay fixed, the owner’s take-home drops fast.

Track Job Cost, Not Just Sales

Measure each project’s direct cost % from quote to closeout: plants, materials, labor, rentals, travel, and callbacks. Track the gap between estimated and actual cost on every install, plus waste, access delays, and membrane coordination issues. If a job needs more than the quoted labor or material budget, margin is already leaking.

Use simple controls: price rework separately, require change orders for scope creep, and review finished jobs against the 72% Year 1 contribution benchmark. Keep a running view of gross profit dollars per project, not just revenue, because owner pay comes from what survives after direct costs and fixed overhead.

- Track actual plants and material waste

- Log callbacks by job and cause

- Price travel and equipment separately

- Stop work on scope changes without approval

3

Labor And Subcontractor Efficiency

Labor Mix and Subcontractor Cost

Owner income moves fast with the labor model. Year 1 payroll is $337,500 across the owner, project manager, two installation technicians, and part-time admin, while subcontracted installation labor adds 7% of revenue in Year 1 and drops to 5% by Year 5. That mix changes gross margin, cash left after jobs, and how much the owner can pay themselves.

Here’s the quick math: if jobs slip, subcontractors still get paid, and payroll stays fixed. In-house crews improve control, but the fixed payroll load makes low volume hurt faster. Owner-performed labor saves cash, but it can cap sales and project management time, which can lower completed work and delay owner draw.

Track Labor by Job, Not by Feel

Measure labor as a share of revenue, hours per install, and subcontractor use by project. The key check is whether each job covers its direct labor plus the $337,500 fixed payroll base. If subcontracted work stays above 7% of revenue, or crews wait on access and approvals, margin leaks fast.

- Track labor % of revenue weekly

- Log install hours by role

- Flag rework and idle time

- Keep owner on sales, not field labor

4

Overhead Utilization

Overhead Utilization

Overhead utilization means how much of your fixed monthly costs are covered by billed, collected work. Here, fixed overhead is $7,100 per month, made up of $4,000 rent, $800 design software, $500 insurance, $600 utilities, $700 accounting and legal, $300 website and IT, and $200 admin supplies, before payroll and marketing. If project volume is low, this overhead hits profit and owner pay hard.

The key inputs are completed projects, average contract size, gross margin, and cash collection timing. The quick test is simple: monthly gross profit has to clear $7,100 just to fund overhead. Repeat maintenance work and tighter scheduling help because they add revenue without adding the same fixed cost load.

Lif t Coverage With Repeat Work

Track monthly gross profit vs. $7,100 overhead and watch how many jobs are needed to cover it. If one slow month leaves the shop under that line, owner draws should wait because payroll and rent still go out.

- Fill gaps with maintenance visits.

- Schedule installs to cut idle days.

- Invoice fast and collect deposits early.

- Price jobs for overhead coverage.

What helps most is not more leads alone, but more billed work per month. One clean rule: if the crew and admin team are busy but cash is thin, the schedule is not covering fixed overhead well enough.

5

Owner Role And Reserves

Owner Pay After Cash Reserve

If you pull owner pay before cash is safe, the business can look profitable and still miss payroll or vendor bills. Here, the model salary is $120,000, but actual distributions should wait until EBITDA (earnings before interest, taxes, depreciation, and amortization), deposits, material buys, and payroll timing all line up. The plan shows a $773,000 minimum cash need in Month 2, so early draws can strain working capital fast.

Cash pays the owner, not paper profit. The key inputs are customer deposits, project collection timing, callbacks, and reinvestment needs. With $280,000 of first-year capex, reserve pressure stays real even if sales are moving. If weather or client approvals slow billing, hold distributions and protect job cash first.

Protect Cash Before Taking Draws

Track a weekly reserve floor, not just month-end profit. Compare cash on hand to the $773,000 Month 2 need, then layer in the next payroll, material orders, and any callback risk before approving owner pay. If deposits are light or suppliers need upfront payment, delay the draw and keep cash inside the company.

Use a simple rule: no distribution unless forecast cash still covers operations after EBITDA-based profit, open work, and near-term reinvestment. That keeps the $120,000 salary target realistic without risking crews, materials, or schedule slippage when weather or access moves against the plan.

6

Scenario objective: compare lean, base, and high-performing rooftop garden owner-income outcomes without treating them as guaranteed

Owner income scenarios

Owner income shifts with project volume, collections, and reserve needs. The base case already covers a $120,000 salary target, but the low case can get tight fast.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | Lower project volume and slower collections keep owner pay near the edge of cash coverage. | The modeled case supports the planned owner salary if the business stays on its current path. | Only a user-edited upside case with more jobs or better pricing would lift income beyond the base salary. |

| Typical setup | Fewer rooftop installs, slower receivables, and tighter reserves make the $120,000 salary target hard to fund. | A $18,000 Year 1 install project, 72% contribution, $447,700 of Year 1 payroll plus marketing plus fixed overhead, $578,000 EBITDA, $773,000 minimum cash, Month 4 breakeven, and 10-month payback support the salary target. | Higher volume, better pricing mix, and faster cash conversion can leave room for salary plus possible distributions once reserves stay intact. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $120,000Cash first | $120,000Modeled pay | $120,000+Upside pay |

| Best fit | Use it to stress-test thin pipelines or delayed collections. | Use it as the planning case for lender, investor, and owner pay decisions. | Use it to test upside after you edit the model for scale or better pricing. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Rooftop Garden Installation Porter's Five Forces Analysis

- Rooftop Garden Installation BCG Matrix

- Rooftop Garden Installation Business Model Canvas

- 7 Core KPIs for Rooftop Garden Installation Success

- Rooftop Garden Installation Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Rooftop Garden Installation Profitability

- How Much Does It Cost To Run A Rooftop Garden Installation Business?

- Rooftop Garden Installation Startup Costs: $773K Cash Plan

- Rooftop Garden Financial Model Template in Excel

- How To Start A Rooftop Garden Installation Business In 8–16 Weeks

- How to Write a Rooftop Garden Installation Business Plan

- Rooftop Garden Installation Marketing Mix

- Rooftop Garden Installation Marketing Plan

- Rooftop Garden Installation Business Proposal

- Rooftop Garden Installation PESTEL Analysis

- Rooftop Garden Installation Pitch Deck Example Editable PPTX

- Rooftop Garden Installation Business SWOT Analysis

- Rooftop Garden Installation Value Proposition Canvas

Frequently Asked Questions

The model includes a $120,000 annual owner salary for the CEO / Lead Designer role Extra take-home depends on distributions after cash reserves, taxes, debt, and reinvestment Year 1 EBITDA is $578,000, but the business also needs $773,000 of minimum cash and $280,000 of first-year capex, so profit is not the same as available cash