Owner income$80,000

Owner income$80,000How Much Gutter Cleaning Owners Make: $80K Pay, Month 30 Breakeven

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$80,000  Net margin82%-85.2%

Net margin82%-85.2% Revenue for target pay$94k-$98k

Revenue for target pay$94k-$98k Business difficultyHard

Business difficultyHard

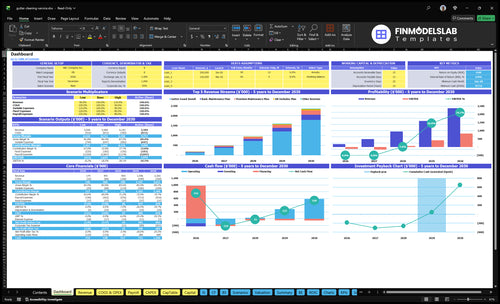

A gutter cleaning business owner can model $80,000 in before-tax owner pay, but that pay is not the same as profit In the researched assumptions, EBITDA is -$116,000 in Year 1 and -$150,000 in Year 2, with breakeven in Month 30 and Year 3 EBITDA of $66,000 The model uses $45, $75, and $110 monthly service plans, a $1,200 average installation project, 82% Year 1 gross margin before overhead, and $95,000 in startup capex Treat these as planning assumptions, not guaranteed salary

Owner income$80,000Net margin82%-85.2%Revenue for target pay$94k-$98kBusiness difficultyHardWhat would your gutter cleaning owner income be?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Want to test the full Gutter Cleaning forecast?

After you map income drivers, open the Gutter Cleaning Financial Model Template to test revenue, costs, cash, and owner take-home.

Owner-income model highlights

- Dashboard, assumptions, revenue build

- Pricing, plan mix, labor

- Marketing, fixed costs, capex

- Cash reserves, owner income

- Year 3 EBITDA: $66k

- Month 30 breakeven, 51-month payback

- $95k capex, $477k cash need

- $80k founder salary

How much revenue does a gutter cleaning business need?

Gutter Cleaning needs about $299,000 in annual revenue to hit EBITDA break-even, using $221,600 of Year 1 costs and a 74% contribution margin. That includes the modeled $80,000 Founder/CEO salary, but not taxes, debt service, or owner distributions. At a $75 monthly plan, that works out to about 333 active customer-month equivalents per month, before any $1,200 installation projects.

Cost base

- $36,600 fixed overhead

- $170,000 wages

- $15,000 marketing

- $221,600 total before variable costs

Revenue math

- 74% contribution margin

- $299,000 break-even revenue

- 333 monthly customer equivalents

- $1,200 installs add upside

Is a gutter cleaning business profitable?

Yes, a Gutter Cleaning business can be profitable, but not from day one in this model: Year 1 EBITDA is -$116,000, Year 2 EBITDA is -$150,000, and breakeven arrives in Month 30. Year 3 turns positive at $66,000 EBITDA, so funding, route density, and disciplined pricing matter; for KPI focus, see What Is The Most Important Metric For Measuring Gutter Cleaning Service Success?.

Profit Timing

- Year 1 EBITDA: -$116,000

- Year 2 EBITDA: -$150,000

- Breakeven: Month 30

- Year 3 EBITDA: $66,000

Profit Levers

- Build dense routes by zip code

- Protect pricing on repeat plans

- Control labor hours tightly

- Keep fixed overhead lean

What gutter cleaning business expenses reduce owner take-home?

Gutter Cleaning owner take-home gets squeezed first by labor, vehicle costs, and fee-heavy systems, and if you’re sizing startup cash, see How Much Does It Cost To Open And Launch Your Gutter Cleaning Business? The biggest drains are vehicle fuel and maintenance at 35% of revenue, supplies and minor parts at 15%, payment processing at 25%, and usage-based software at 15%; direct labor is 13% in Year 1, then salaried payroll reaches $170,000 before the larger Year 2 team.

Add $15,000 in Year 1 marketing, plus 4% variable marketing, $900 per month in insurance, and $3,050 per month in fixed overhead, so cash stays tight before owner distributions because capex starts at $95,000.

Main cost drains

- 35% fuel and maintenance

- 25% payment processing

- 15% supplies and parts

- 15% usage-based software

Fixed cash drag

- 13% direct labor in Year 1

- $170,000 salaried payroll later

- $900/month insurance cost

- $3,050/month fixed overhead

Want to see what drives gutter cleaning owner income?

1

$45-$1.32KTicket Mix

Mixing monthly plans, install projects, and property unit work lifts average ticket and pushes more revenue into owner take-home.

2

0.5h/moJob Volume

At 0.5 billable hours per active customer in Year 1, small swings in job count and seasonality decide how much cash comes in.

3

2-10 FTELabor Load

Direct labor starts at 13% while technician headcount scales from 2 to 10, so scheduling and overtime control matter a lot.

4

3.5%-2.7%Route Density

Packed routes cut fuel and maintenance from 3.5% to 2.7%, which keeps more gross profit on each service day.

5

$120-$90Marketing CAC

CAC falling from $120 to $90 helps more of a rising $15K to $100K budget turn into paid work, not wasted spend.

6

$477KCash Buffer

With $3,050 of fixed overhead, $95K of capex, and Month 30 breakeven, the cash buffer sets how long the business can breathe.

Gutter Cleaning Core Six Income Drivers

Average Ticket And Pricing

Ticket-Based Pricing

If every home is priced like a simple stop, owner income gets squeezed fast. The model price ladder runs from $45 basic monthly to $75 premium, $110 all-inclusive, $1,200 average installation work, and $60 per property-management unit each month. Price should move with property size, stories, debris level, access, downspout clearing, and add-on work.

Here’s the quick math: one $1,200 installation equals 16 premium monthly plans at $75. If a hard job gets underpriced, it eats technician time and fuel, so gross profit per crew-day drops even if lead flow stays the same. That’s the risk to owner pay.

Track Price by Job Difficulty

Measure realized ticket by service line, not as one blended number. Use property size, stories, debris load, access, and downspout clearing as pricing inputs, then compare ticket to labor hours, fuel, and callbacks. The Year 1 mix is disclosed as 60% basic, 30% premium, 5% all-inclusive, 15% installation, and 5% property management, so treat it as a planning assumption and check it before forecasting.

Raise prices when the stop takes more crew time, more ladder work, or more drive time. Track margin on monthly plans, installs, and unit-based work separately, because one clean rule protects cash flow: if the job is harder, the ticket should be higher. That keeps owner income tied to better pricing, not just more leads.

1

Job Volume And Seasonality

Seasonal Job Volume

Completed work drives revenue, but seasonality decides whether owner pay feels smooth or lumpy. The model uses 0.5 billable hours per active customer per month in Year 1, easing to 0.4 by Year 5. That means the real income driver is not just new leads; it’s how many recurring jobs stay on the schedule when demand swings.

Spring and fall must carry the slow months. The plan shows Month 30 breakeven and a $477,000 minimum cash need, so weak periods can’t be funded from hope. If fixed payroll keeps running while recurring customers drop, owner pay gets delayed or cut, even if annual demand looks fine on paper.

Protect Cash Through Recurring Routes

Track active customers, billable hours per customer, and booked work by month. Here’s the quick math: more repeat plans mean steadier utilization, which supports cleaner cash flow and makes owner draws less volatile. One line says it all: fill the schedule before you raise pay.

- Watch monthly work by season.

- Measure recurring customer count.

- Reserve cash for slow months.

- Limit fixed payroll in weak periods.

What this estimate hides is timing risk: if onboarding lags or repeat plans are thin, the business still pays labor and overhead. So the goal is to lock in enough recurring work early to cover off-season demand and keep owner income stable.

2

Route Density And Travel Efficiency

Route Density

When homes are clustered, more of the crew day turns into paid work. In this model, vehicle fuel and maintenance run at 35% of revenue in Year 1 and improve to 27% by Year 5, so shorter drives can lift owner take-home without changing the ticket. A dense route with nearby homes can protect margin even if each job is modest.

The risk is chasing distant one-off jobs. They look like revenue, but deadhead time (unpaid drive time), fuel, and schedule gaps cut cash flow and lower completed jobs per crew-day. Track callbacks too, because a bad route plus rework is the fastest way to lose profit on a busy day.

Track the Route, Not Just the Sales

Measure completed jobs per crew-day, drive time between stops, callbacks, and same-neighborhood bookings. Those inputs show whether the route is dense enough to raise billable work from the same crew hours and keep fuel and maintenance from eating margin.

- Book nearby homes first.

- Group stops by zip code.

- Reject low-density one-offs.

- Price far jobs for travel.

If the schedule has long gaps or scattered stops, the owner pays for time that never bills. Tight routing is what turns the same labor into more profit, which is what funds owner pay.

3

Labor Model And Crew Productivity

Crew Productivity

Labor sets the gap between revenue and owner income. In this model, direct labor runs at 13% of revenue in Year 1 and improves to 11% by Year 5, while salaried payroll grows from $170,000 in Year 1 to $470,000 in Year 3. Owner pay is modeled at $80,000, but early EBITDA (earnings before interest, taxes, depreciation, and amortization) stays negative.

The inputs that matter are crew count, completed jobs, billable hours, and payroll per route. The plan starts with 2 service technicians and reaches 10 by Year 5, so hiring before route volume and pricing support the crew can burn cash fast. Scale only works when each crew adds profitable completed jobs, not just headcount.

Track Jobs Per Crew

Measure completed jobs per crew-day, labor as a percent of revenue, and salary load per route. If labor drifts above the 13% to 11% path, owner pay gets squeezed first. No filled route, no extra draw.

Keep staffing tied to booked, repeatable route volume. Use weekly targets for billable hours, completed stops, and callbacks. If the schedule cannot support another tech, delay hiring or raise prices on larger homes, heavy debris, or hard-access jobs.

- Track completed jobs per crew-day.

- Watch labor as % of revenue.

- Hire after route volume, not before.

4

Marketing Cost And Lead Quality

Marketing Cost And Lead Quality

Marketing helps owner income only when leads turn into booked jobs, repeat cleanings, and add-ons. In this model, the annual budget climbs from $15,000 in Year 1 to $100,000 in Year 5, while CAC (customer acquisition cost) falls from $120 to $90 and variable marketing drops from 4% of revenue to 3%. That works only if leads fit dense routes and higher-value plans.

The risk is buying low-margin one-off jobs that do not repeat. Here’s the quick math: if marketing brings in customers who stay on subscription or add services, contribution margin rises; if it only fills the calendar with scattered cleanups, owner pay gets squeezed by travel and sales cost. Lead quality beats lead volume .

Track Repeat Jobs, Not Just Leads

Measure CAC, booked-job rate, repeat rate, average ticket, and distance from existing routes. If one channel brings cheap leads but weak repeat work, cut it fast. If another source drives premium or all-inclusive plans in the same neighborhood, scale it. That’s how marketing turns into more profit, not just more calls.

- Track booked-job rate weekly.

- Compare CAC by source.

- Split repeat and one-off jobs.

- Favor nearby, dense routes.

- Test premium plan offers.

If marketing fills routes with repeat cleanings and add-ons, the same crew hours earn more. If it pulls in far-away jobs, fuel and idle time eat margin. Dense routes plus higher tickets is the cleanest path to better owner take-home.

5

Overhead, Equipment, Insurance, And Reserves

Overhead, Equipment, And Cash Reserves

This driver is the cash you keep in the business before owner pay. Fixed overhead is $3,050 per month, including $300 general liability insurance and $600 fleet vehicle insurance. It also covers equipment replacement, repairs, callbacks, and slow months. If you pull cash out too early, owner income looks higher on paper but turns into a cash crunch fast.

The model’s $477,000 minimum cash need, Month 30 breakeven, and 51-month payback show how long this business can stay cash-tight. Here’s the quick math: if reserves are treated like spendable profit, the owner may underfund vehicles and working capital. That pushes pay back or delays it, even when revenue is growing.

Protect Cash Before Owner Pay

Track overhead as a fixed monthly run rate, not a leftover bucket. Separate reserve cash for safety, vehicles, and weak months from profit draw. Build a rule that owner pay starts only after $3,050 fixed overhead, planned equipment replacement, insurance, repairs, and callback costs are funded.

Review cash weekly and flag any drop below the reserve target. Stress-test the plan for a long slow season and a vehicle repair at the same time. If cash is thin, hold owner draws, delay nonessential buys, and protect the schedule so the business reaches breakeven without starving operations.

6

Scenario objective for gutter cleaning income projection

Owner income scenarios

Owner income shifts fast as marketing, CAC, technicians, and payroll scale. The low, base, and high cases show where cash strain keeps pay down before profit starts to improve.

| Scenario | Low CaseCash-heavy ramp | Base CaseHiring risk | High CasePost-breakeven profit |

|---|---|---|---|

| Launch model | This is the lower-owner-income path built around a Year 1 ramp and weak EBITDA. | This is the modeled expansion path that mirrors Year 2 hiring and still runs negative EBITDA. | This is the stronger earnings path after breakeven, with profit showing up in Year 3. |

| Typical setup | Year 1 runs near $143,000 revenue at 82% gross margin, with 2 service technicians, $170,000 payroll, $95,000 startup capex, and an $80,000 modeled owner salary. | Year 2 reaches about $395,000 revenue with 4 service technicians, added management roles, and about $380,000 payroll, but EBITDA stays negative. | Year 3 scales to about $815,000 revenue with 6 service technicians, $470,000 payroll, $50,000 marketing, and $66,000 EBITDA after breakeven. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $80,000 modeled salaryCash-heavy ramp | Draw under cash pressureHiring risk | $80,000 salary plus profitPost-breakeven profit |

| Best fit | Use this to test early cash strain and whether owner pay holds while revenue ramps. | Use this to test the expansion year when payroll and management add the most pressure. | Use this to test the post-breakeven path where owner pay can sit on top of profit. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Gutter Cleaning Porter's Five Forces Analysis

- Gutter Cleaning BCG Matrix

- Gutter Cleaning Business Model Canvas

- 7 Core Financial KPIs for Gutter Cleaning Services

- Gutter Cleaning Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Gutter Cleaning Profitability and Margin

- What Are The Monthly Running Costs For A Gutter Cleaning Business?

- Gutter Cleaning Startup Costs: $95K CAPEX And $477K Cash Plan

- Gutter Cleaning Financial Model Template in Excel

- How To Start A Gutter Cleaning Business In 2 To 6 Weeks

- How to Write a Gutter Cleaning Business Plan: 7 Steps

- Gutter Cleaning Marketing Mix

- Gutter Cleaning Marketing Plan

- Gutter Cleaning Business Proposal

- Gutter Cleaning PESTEL Analysis

- Gutter Cleaning Pitch Deck Example Editable PPTX

- Gutter Cleaning Business SWOT Analysis

- Gutter Cleaning Value Proposition Canvas

Frequently Asked Questions

This model pays the owner $80,000 before tax as Founder/CEO salary, but that is not guaranteed profit EBITDA is -$116,000 in Year 1 and -$150,000 in Year 2, so early pay needs funding Profit turns positive after breakeven in Month 30, with Year 3 EBITDA of $66,000