Owner income$54.5k

Owner income$54.5kHow Much Hair Accessory Manufacturing Owners Make at $854K Sales

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$54.5k  Net margin92.7% to 93.3%

Net margin92.7% to 93.3% Revenue for target pay$71.2k to $465.4k

Revenue for target pay$71.2k to $465.4k Business difficultyMedium

Business difficultyMedium

For this US hair accessory manufacturing plan, researched assumptions show $854,000 in first-year revenue and about $653,990 in owner-income capacity before taxes, debt service, inventory reserves, and any separate owner salary The page covers revenue, gross margin, known fixed costs, channel costs, reserves, and target owner pay across a five-year model period Figures depend on sales volume, channel mix, production method, margins, payroll, inventory, and reinvestment needs

Owner income$54.5kNet margin92.7% to 93.3%Revenue for target pay$71.2k to $465.4kBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

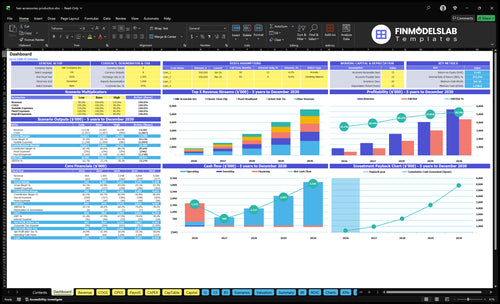

Can you check owner income in the financial model?

See the full forecast in the Hair Accessory Manufacturing Financial Model Template; this screenshot shows revenue, margins, costs, reserves, and owner take-home assumptions—open the model.

Owner-income model highlights

- Owner take-home capacity

- 93% gross margin

- 65k to 365k units

How much can a hair accessory business owner pay themselves?

A Hair Accessory Manufacturing owner can pay themselves from cash left after inventory, payroll, overhead, taxes, debt, and growth spend; in the researched first-year case, that capacity is about $653,990 pre-tax. That assumes 65,000 units and $854,000 revenue, and pay should be checked against customer quality signals like What Is The Current Customer Satisfaction Level For Hair Accessory Manufacturing?.

Cash Available

- $854,000 first-year revenue assumed

- 65,000 units sold assumed

- $653,990 pre-tax owner-income capacity

- After COGS, selling, fixed costs

Owner Pay Caveat

- Not a guaranteed salary

- Includes unpaid owner labor

- Hiring help may lower pay

- Capacity can rise with delegation

What revenue is needed to pay a hair accessory business owner?

No single revenue target fits Hair Accessory Manufacturing, because wholesale, direct-to-consumer, boutique, salon, marketplace, and private-label orders all carry different prices, discounts, fees, returns, and fulfillment costs. Here’s the quick math: using the Year 1 mix, cash margin before fixed costs is about 822% after COGS and variable selling costs, and fixed costs are $48,000 a year. That puts fixed-cost break-even at roughly $58,400 in annual revenue before owner pay, and about $180,000 to support $100,000 of pre-tax owner pay before inventory reserves and taxes.

Revenue mix drivers

- Wholesale lowers price fast.

- DTC keeps more margin.

- Boutique orders add margin pressure.

- Marketplace fees cut take-home.

Break-even pressure points

- $48,000 covers fixed costs.

- $58,400 covers fixed costs plus base mix.

- $180,000 supports $100,000 owner pay.

- More discounts or paid ads raise the target.

Can a hair accessory business support a full-time owner?

Yes—Hair Accessory Manufacturing can support a full-time owner if sell-through stays strong and cash keeps moving. In the case pattern, volume grows from 65,000 units to 365,000 units, or about 5.6x, so the business likely moves from owner-made batches into hired production help and outsourced steps. Full-time pay is safer when reorders repeat and cash conversion, or how fast materials turn back into cash, stays quick.

What has to scale

- 65,000 to 365,000 units needs more capacity.

- Owner-made batches stop working at scale.

- Hire help for repeat production steps.

- Use stronger supplier controls early.

What can break it

- Inventory sitting traps cash.

- Defects hurt margin and trust.

- Slow wholesale payments squeeze working capital.

- One channel controlling sales raises risk.

What most changes owner income?

1

$854KChannel Mix

Year 1 revenue is $854K across five products, so the split between clips, scrunchies, headbands, barrettes, and ties sets the base for owner take-home.

2

95% GMUnit Economics

Unit costs run from $0.38 to $1.23 against $8 to $29 prices, so pricing and product mix drive most of the cash left over.

3

5.6xProduction Efficiency

Total output grows from 65K units in Year 1 to 365K in Year 5, and higher throughput spreads factory cost over more sales.

4

$1.2MCash Buffer

Minimum cash sits near $1.196M in Month 1, so inventory timing and working capital decide how safely growth can be funded.

5

$244KPayroll Load

Year 1 wages and fixed overhead run about $244K before later hires, so headcount timing has a direct hit on take-home income.

6

$5.6MRepeat Demand

By Year 5, repeat wholesale or private-label demand can support about $5.6M in revenue, which helps fixed costs shrink as a share of sales.

Hair Accessory Manufacturing Core Six Income Drivers

Sales Channel Mix

Channel Mix and Owner Pay

Your sales channel mix decides whether growth turns into cash or just more work. In Year 1, source variable selling costs are 105% of revenue, so $100 of sales can cost about $105 in ads, influencer fees, e-commerce, and payment processing before fixed overhead. In the mature year, that drops to 65%, which still leaves only $35 per $100 of revenue to cover payroll, rent, and owner draw.

DTC can protect price, but it also adds ad spend, card fees, shipping work, and returns. Wholesale and salon retail can raise unit volume, but they usually cut price and delay cash. Private-label orders can improve batch size, yet one big customer can create concentration risk. Higher revenue does not always mean higher take-home income.

Track Margin By Channel

Measure each channel separately: selling price, discounts, return rate, fulfillment cost, payment fees, and days to cash. Here’s the quick math: if a channel cannot beat the 105% Year 1 selling-cost load, it is draining owner cash, not creating it. Break out DTC, boutique wholesale, salon retail, and private-label so you can see which mix actually funds owner pay.

Use channel tests to protect margin. Push the channels with the best net contribution, not just the biggest order count. One clean rule: chase contribution, not volume. If wholesale grows but cash comes in late, or DTC sales rise while ad costs outrun margin, the business can look busy and still pay the owner less.

- Track net revenue by channel

- Watch returns and shipping cost

- Compare cash timing by buyer type

- Limit customer concentration on private-label

1

Unit Economics

Unit Economics

Unit economics is the profit on each accessory before overhead. With 25% revenue-based factory costs added to unit COGS, the model keeps about 70% contribution on each SKU: $8.53 on a $12 clip, $17.52 on a $25 scrunchie set, $12.60 on a $18 headband, $6.93 on a $10 barrette, and $5.62 on an $8 tie.

That margin is what pays fixed overhead and owner draw. If one more dollar goes to labor, packaging, defects, or material waste, owner-income capacity falls by the same dollar. Lower-priced items still help volume, but only if the mix and cost stack keep contribution high enough to fund the rest of the business.

Track Margin by SKU

Measure unit economics as price, unit COGS, factory cost %, and sales mix by style. Use the formula contribution per unit = price - COGS - 25% of price. Then compare each SKU’s cash left after production against the work it takes to make and ship.

- Watch defects and rework weekly.

- Test price by SKU, not by brand.

- Shift volume toward stronger margin items.

The weak spots are easy to see. The $8 tie leaves $5.62 before overhead, while the $25 scrunchie set leaves $17.52. If scrap, overtime, or packaging creep up, fix that before scaling orders, because higher unit count with thin margin just creates more work, not more owner pay.

2

Production Efficiency

Production Efficiency

Production efficiency matters because it lowers labor cost per unit and frees the owner from low-value work. In this model, labor sits in assembly for clips, sewing for scrunchie sets and ties, adornment for headbands, and finishing for barrettes. If throughput rises from 65,000 units in Year 1 to 365,000 in the mature year, the owner’s income only improves if labor stays controlled and margin does not leak into overtime or rework.

The key question is whether batch size, workstation setup, tooling, standard designs, supplier consistency, and quality checks can support the ramp. Higher output helps take-home pay only when each added unit still carries healthy contribution margin. If defects, late orders, or owner burnout rise, gross profit may grow on paper while cash available for owner draw stays flat.

Track Labor Per Unit

Measure labor by product line and by step, not just by total payroll. Track assembly, sewing, adornment, finishing, overtime hours, defect rate, and rework rate each week. The owner should also watch units per batch and setup time, because slow changeovers eat capacity and push labor cost per unit up.

Use a simple control sheet: units produced, labor hours used, overtime, late orders, and owner production hours. If one style needs too much handwork, standardize it or cut it back. The goal is cleaner throughput, fewer errors, and more owner time for sales, planning, and profit draw.

- Track units per labor hour.

- Flag overtime before it repeats.

- Measure defect and rework rates.

- Separate owner work from crew work.

- Review setup time by product batch.

3

Inventory And Cash Reserves

Inventory and Cash Reserves

Inventory eats cash before it shows up as income. This business buys plastic, metal springs, silk fabric, elastic, headband bases, faux pearls, metal, velvet fabric, packaging, and inbound freight, so cash can sit on shelves even when the margin looks fine. Owner pay should follow cash flow, not just accounting profit.

Finished goods can also trap cash when seasonal colors or slow-moving styles do not sell through. Minimum order quantities may cut unit cost, but they can also raise cash tied up in stock, so the reserve rule should hold back cash before any distribution. The reserve percentage is not given here, so make it an editable input.

Track Stock Before You Pay Yourself

Measure inventory on hand, sell-through, and days inventory by style. Separate raw materials from finished goods, because a low-cost batch can still block owner income if it sits unsold. One clean rule: if stock is rising faster than sales, cash risk is rising too.

- Track raw materials cash tied up.

- Track finished goods by style.

- Flag slow seasonal colors early.

- Test smaller reorder quantities.

- Hold back cash before draws.

Use the reserve input to set a floor for cash after buying materials and paying freight. That keeps distributions tied to actual collections, not just revenue booked on paper, and it protects owner pay when reorder timing or weak sell-through slows cash conversion.

4

Labor, Payroll, And Overhead

Labor and overhead

Labor and overhead are what’s left after gross margin, and this business has both direct labor in COGS and fixed overhead after that. With $4,000/month in office rent, utilities, internet, software, insurance, and legal or accounting fees, overhead alone is $48,000/year before founder pay. If the owner also covers production, packing, sales, design, admin, and management, take-home income depends on what that labor would cost to replace.

Estimate it with units sold, labor hours per unit, contractor rates, and owner time by task. The key test is whether added labor removes a bottleneck or just adds idle cost. Production labor belongs inside COGS; production assistants, fulfillment help, equipment upkeep, and admin support belong below gross margin. If hiring does not lift output or cut rework, it reduces distributable income.

Track each labor bucket

Split hours into making, packing, selling, design, admin, and management. Then compare each role to output: units shipped, defect rate, and on-time orders. Here’s the quick math: $4,000 fixed overhead plus owner replacement pay sets the floor sales must clear before profit reaches the founder.

Before adding staff, test the gap first with small batches, standard work, and clear handoffs. If a contractor or assistant frees the founder from low-value tasks and raises throughput, owner income can improve. If not, the hire becomes another fixed cost and pushes cash out faster than it comes in.

5

Repeat Demand And Account Quality

Repeat Demand Quality

Repeat wholesale and private-label orders make owner income steadier because production, buying, and staffing can follow a known reorder cycle. The key inputs are reorder frequency, minimum order quantities (MOQs), sell-through data, seasonal launches, and how much volume sits in one account.

That matters more as volume ramps from 65,000 units to 365,000 units. A boutique or salon that reorders can smooth batches and cash flow, but one large private-label customer can create a cash and profit shock if it slows, cuts volume, or pushes price down. Owner pay gets easier when demand is recurring, not one-off.

Track Reorders and Concentration

Measure how often each account reorders, what each order covers versus MOQ, and how fast product sells through. That tells you whether demand is stable enough to support payroll, materials, and owner draws.

- Track reorder gap by account.

- Watch top-customer volume share.

- Test seasonal launch repeat rates.

- Compare sell-through by style.

If one account drives too much volume, spread risk before adding staff or inventory. If reorders are steady, you can plan batches with less markdown risk and less cash tied up in slow stock, which keeps take-home income cleaner.

6

Compare low, base, and high owner-income outcomes

Owner income scenarios

Owner income moves with unit volume, mix, and how fast fixed payroll and marketing spread across production. Early years are tight, while later years earn more as volume climbs and margins stay strong.

| Scenario | Low CaseEarly ramp | Base CaseScaling operations | High CaseUpside capacity |

|---|---|---|---|

| Launch model | Lower earnings path with 65,000 units, about $854,000 revenue, and about $653,990 pre-tax owner-income capacity before reserves. | Modeled scaling case with 180,000 units, about $2,597,500 revenue, and about $2,159,613 pre-tax owner-income capacity before reserves. | Stronger upside case with 365,000 units, about $5,585,000 revenue, and about $4,797,200 pre-tax owner-income capacity before reserves. |

| Typical setup | 65,000 units at a blended average sale price near $13.14, about $48,000 of known fixed costs, and about 92.7% gross margin. | 180,000 units at a blended average sale price near $14.43, about 93.0% gross margin, and a wider operating setup than the early case. | 365,000 units at a blended average sale price near $15.30, about 93.3% gross margin, and a capacity-heavy operating mix. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $653,990Early ramp | $2,159,613Scaling operations | $4,797,200Upside capacity |

| Best fit | Best for founders stress-testing an early ramp and tighter cash use. | Best for planning a steady scale-up with hiring and broader distribution. | Best for testing a strong sell-through case with heavy capacity use. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Hair Accessory Manufacturing Porter's Five Forces Analysis

- Hair Accessory Manufacturing BCG Matrix

- Hair Accessory Manufacturing Business Model Canvas

- Tracking 7 Core KPIs for Hair Accessory Manufacturing

- Hair Accessory Manufacturing Business Plan Template in Pre-Written Word

- Increase Hair Accessory Manufacturing Profitability with 7 Financial Strategies

- Analyzing Monthly Running Costs for Hair Accessory Manufacturing

- Hair Accessory Manufacturing Startup Costs for a $854K Year 1 Plan

- Hair Accessory Manufacturing Financial Model Template in Excel

- How to Start a Hair Accessory Manufacturing Business in 8 to 16 Weeks

- How to Write a Business Plan for Hair Accessory Manufacturing

- Hair Accessory Manufacturing Marketing Mix

- Hair Accessory Manufacturing Marketing Plan

- Hair Accessory Manufacturing Business Proposal

- Hair Accessory Manufacturing PESTEL Analysis

- Hair Accessory Manufacturing Pitch Deck Example Editable PPTX

- Hair Accessory Manufacturing Business SWOT Analysis

- Hair Accessory Manufacturing Value Proposition Canvas

Frequently Asked Questions

The researched first-year plan shows about $653,990 in pre-tax owner-income capacity, not guaranteed take-home That comes from $854,000 in revenue, $62,340 in COGS, $89,670 in selling costs, and $48,000 in known fixed costs Taxes, debt service, inventory reserves, and any formal owner salary still need to come out