Owner income$185k

Owner income$185kHeating Oil Delivery Owner Income: $185K Pay, Month 14 Break-Even

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$185k  Net margin-24% to 49%

Net margin-24% to 49% Revenue for target pay≈$375k

Revenue for target pay≈$375k Business difficultyHard

Business difficultyHard

This five-year US residential model shows $185,000 in planned annual owner-operator pay, but that salary is not the same as distributable profit The analysis covers revenue, gallons delivered, gross margin, payroll, overhead, capex, cash shortfalls, and scenario planning it excludes income taxes, debt service, fuel inventory financing terms, and local market differences

Owner income$185kNet margin-24% to 49%Revenue for target pay≈$375kBusiness difficultyHardWant to test your owner pay scenario?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margin, payroll, fees, reserves, taxes, and financing. This is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full forecast for Heating Oil Delivery Service owner income?

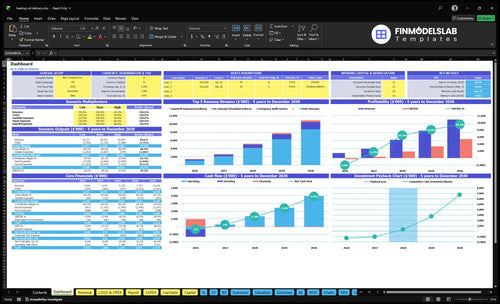

The screenshot shows the Heating Oil Delivery Service Financial Model Template with dashboard tabs for customer volume, gallons delivered, emergency refill jobs, pricing, fuel, logistics, payroll, overhead, reserves, and owner income. Open the model to see revenue, EBITDA, breakeven, payback, minimum cash, owner salary, and margin charts.

Owner-income model highlights

- Revenue is not take-home

- Track EBITDA and cash

- Test Year 1 to 5

How much revenue does a heating oil delivery business make?

A Heating Oil Delivery Service can scale fast on paper: revenue is $1,428 million in Year 1, $2,679 million in Year 2, $5,192 million in Year 3, $7,797 million in Year 4, and $10,935 million in Year 5. That top line comes from scheduled gallons and emergency refill fees, but Year 1 revenue does not mean profit. Here’s the catch: Year 1 EBITDA is -$340,000 after fuel procurement, logistics, fees, payroll, and $588,000 fixed overhead, while Year 5 EBITDA reaches $5,406 million before taxes, debt service, depreciation, and owner distributions.

Revenue drivers

- Sell scheduled gallons first.

- Use emergency refill fees.

- Price by gallons sold.

- Watch winter demand swings.

Profit and cash

- Year 1 EBITDA is -$340,000.

- Fixed overhead is $588,000.

- Year 5 EBITDA is $5,406 million.

- Working capital can block cash draws.

How many heating oil customers do I need to make a living?

You don’t need one universal customer count; for a Heating Oil Delivery Service, use customers needed = target annual gallons ÷ average annual gallons per household, and see How Increase Heating Oil Delivery Service Profits? for the profit levers. The model gives gallons, not accounts: Year 1 has 220,000 scheduled gallons and $1.428 million revenue, but -$340,000 EBITDA, so the $185,000 owner salary needs funding.

Use the formula

- Set target annual gallons first

- Divide by household annual gallons

- Do not invent account count

- Recheck after delivery mix changes

Profit test

- Year 2 revenue: $2.679 million

- Year 2 EBITDA: $427,000

- Breakeven comes after Month 14

- Keep routes dense, credit losses low, margin firm

Is a heating oil delivery business profitable as an owner operator?

A Heating Oil Delivery Service is not profitable in Year 1 under this plan, even with a $185,000 owner salary built in. EBITDA is -$340,000 in Year 1, and breakeven lands in Month 14. A lean owner-operator can reduce payroll pressure, but this model already assumes 4 drivers, 2 support reps, 1 operations manager, and 1 engineer in Year 1.

Year 1 pressure

- $185,000 owner salary included

- -$340,000 Year 1 EBITDA

- Breakeven in Month 14

- 4 drivers already on payroll

Scale tradeoffs

- Revenue grows to $10.935 million by Year 5

- Certified drivers rise from 4 to 20 FTE

- Dispatch and compliance get harder

- Cash reserves must cover fuel, fleet, and service load

Want the six drivers that move owner income most?

1

40K-220KActive Homes

More active homes lift repeat stops, and revenue rises from $1.428M in Year 1 to $10.935M in Year 5.

2

180K-1.25MGallons Per Home

Weather and household use move yearly gallons, so this line drives the volume behind the revenue run rate.

3

80.5%-84%Margin Spread

The direct cost stack leaves about 80.5% to 84.0% gross margin, so small price moves change cash fast.

4

3.0%-2.0%Route Density

Cutting logistics from 3.0% to 2.0% of revenue raises take-home by keeping trucks fuller and miles lower.

5

12%-10.5%Fuel Risk

Wholesale fuel still takes 12.0% to 10.5% of sales, and Month 13 cash bottoms at -$350K, so fuel swings can pinch owner pay.

6

$588K+$960KOverhead Load

Fixed overhead runs $588K a year, and the $960K capex build plus payroll growth can swamp EBITDA if volume stalls.

Heating Oil Delivery Service Core Six Income Drivers

Active Residential Customer Base

Active Residential Customer Base

A bigger active base lifts repeat gallons, emergency refill volume, and route fill. This model should be read by scheduled gallons, not just account count: 220,000 in Year 1 and 147 million in Year 5. More accounts help owner pay only when they are nearby, stay active, and pay on time.

What this estimate hides is churn, credit risk, and territory density. Adding homes outside the core area can raise revenue but hurt delivery cost per gallon, so the same customer count can produce very different take-home income.

Track active gallons by route

Measure active accounts, gallons per route, late-pay rate, and emergency fills. If a route stays dense, trucks run fuller and labor cost per gallon falls. If it stretches into thin territory, cash and profit both slip even when sales rise.

Use a simple rule: add accounts only when they fill nearby routes and pay fast. Test whether each new cluster lowers cost per gallon, then keep the ones that improve margin and owner draw.

- Watch churn by zip code.

- Track on-time payment rate.

- Compare core vs. fringe routes.

1

Annual Gallons Delivered Per Customer

Annual Gallons per Customer

Annual gallons per customer is the volume each active home uses in a year. It matters because more gallons per account raise revenue and spread dispatch effort over more product, but only if wholesale cost and delivery timing stay tight. The core math is total gallons ÷ active customers.

In this model, scheduled gallons rise from 220,000 in Year 1 to 147 million in Year 5, so small gains per home scale fast. Demand changes with weather, home size, insulation, tank size, and auto-delivery. Cold winters can lift usage; mild winters can leave trucks and payroll underused.

Track Gallons by Home and Season

Measure this by route and by month, not just in one company total. The owner should watch gallons per active account, auto-delivery share, and route-level cost per gallon. That shows whether higher volume is helping gross profit or just creating more delivery work.

- Active customers

- Gallons per customer

- Winter severity

- Tank size mix

- Auto-delivery enrollment

Use those inputs to test which homes and routes buy more gallons without extra service cost. If gallons rise but dispatch gets messy, owner pay can still shrink. The best setup is steady per-home usage, full trucks, and fuel buys timed so the higher volume turns into cash, not just sales.

2

Gross Margin Per Gallon

Gross Margin Per Gallon

Gross margin per gallon is the spread between what the customer pays and the direct cost to deliver that gallon. In this model, scheduled pricing runs $6 to $8 per gallon and emergency refills run $150 to $170, so owner pay depends on keeping direct costs below those prices. If variable cost load is 195% of revenue in Year 1, the spread is underwater before fixed overhead.

Here’s the quick math: 195% means direct costs are $1.95 for every $1.00 of sales, and 160% in Year 5 still means costs exceed revenue. That is not net profit, because payroll, insurance, facility rent, software, marketing, and reserves still come out. So even strong gallons can leave little or no cash for the owner if supplier pricing or delivery cost stays high.

Track the spread, not just the sale

Measure gross margin per gallon by delivery type: scheduled, automatic, and emergency. Track gallons sold, customer price per gallon, wholesale fuel cost, and delivery cost on every route. If emergency calls carry a higher selling price, they still need a positive spread after truck time, labor, and fuel.

Watch these inputs to protect owner income:

- Price per gallon by order type

- Direct cost per gallon

- Supplier terms and fuel volatility

- Route mix of scheduled vs. emergency stops

- Competitive local pricing pressure

If wholesale prices jump faster than your selling price, gross margin compresses fast. If onboarding or routing costs rise, the owner’s take-home falls even when revenue looks healthy.

3

Route Density And Delivery Cost Per Gallon

Route Density And Delivery Cost Per Gallon

Route density is how many gallons you deliver per mile, stop, and dispatch hour. It includes route miles, driver time, truck wear, and fuel used to reach each home. In the model, direct delivery logistics cost drops from 30% of revenue in Year 1 to 20% in Year 5, so denser routes protect EBITDA and owner take-home.

Same gallons do not mean same profit. Ten homes on one road can cost less than ten homes across three towns because miles, missed turns, and dispatch waste shrink. Emergency calls, bad tank-level data, and scattered service areas push cost per gallon back up fast.

Keep Routes Tight

Track gallons per stop, miles per delivered gallon, emergency-call share, and failed-delivery rate each week. Group accounts by road and zip first, then layer in auto-fill customers so the truck fills up on one run. If an added territory increases miles faster than gallons, it can lift revenue but still cut owner pay.

- Cut scattered service areas.

- Verify tank levels before dispatch.

- Reduce emergency-only deliveries.

- Fix missed-stop patterns fast.

Here’s the quick math: moving logistics cost from 30% to 20% keeps 10 cents of every revenue dollar before overhead. That extra spread is what helps cash flow, EBITDA, and owner distributions hold up in winter.

4

Inventory Financing And Wholesale Cost Risk

Cash Gets Trapped Fast

This driver is about how much cash sits in oil inventory, receivables, and supplier payments before it turns into owner income. The model shows wholesale fuel procurement at 120% of revenue in Year 1 and still 105% in Year 5, so accounting profit can look fine while cash stays tight.

Here’s the quick math: minimum cash falls to -$350,000 in Month 13. That means owner draws should wait until reserves cover buying fuel, waiting on customer payment, and paying suppliers. Prepay plans can smooth cash timing, but they also add pricing and service obligations.

Protect Cash Before Pay

Track gallons purchased, days inventory on hand, customer collection speed, and supplier credit limits. The key inputs are selling price per gallon, purchase price, payment terms, and how fast delivered gallons get billed and collected. If collections slow, cash gets trapped even when revenue looks strong.

Use prepay only when the contract covers price swings and service demand. Test whether the prepaid cash offsets the obligation to deliver later at a possibly higher wholesale cost. Better cash timing raises safe owner pay; weak terms can wipe out it fast.

5

Fixed Overhead And Fleet Costs

Fixed Overhead And Fleet Costs

Fixed overhead has to be paid before owner take-home, so this driver sets the floor for cash pressure. Here, recurring overhead is $49,000 per month or $588,000 per year, plus $780,000 in Year 1 payroll that grows with drivers, support, operations, and engineering. If routes, gallons, and pricing do not cover those costs, EBITDA stays negative.

The fleet side matters too. $960,000 of capex across trucks, tanks, hardware, app development, office IT, and routing software is a cash drain before profit shows up. That is why the model sits at -$340,000 Year 1 EBITDA; disciplined overhead and fleet use speed the move to positive EBITDA after breakeven.

Track the spend that actually blocks pay

Measure fixed cost per gallon, not just total spend. Track storage lease, hosting, insurance, marketing, office rent, software, security, and the payroll split across drivers, support, operations, and engineering. Add fleet data on truck use, downtime, and routing software so you can see whether added equipment is raising delivery capacity or just raising burn. The key test is simple: does each added dollar help cover overhead faster?

Use a monthly runway view tied to EBITDA and cash. If overhead runs $49,000 a month and payroll starts at $780,000, owner draw should wait until gross profit reliably clears those layers. Watch capex timing on trucks and software closely, because cash tied up in fleet assets can delay pay even when revenue is growing. One clean rule helps: buy or hire only when route volume can absorb it.

6

Compare lean, base, and high-scale owner income scenarios

Owner income scenarios

Breakeven lands in Month 14 and payback in Month 35, but trucks, payroll, and working capital hit first, so owner income changes fast with volume.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is a capital-funded launch year with 220,000 scheduled gallons, 450 emergency refill jobs, $1.428M revenue, and -$340k EBITDA. | This is the modeled run-rate path with Year 3 revenue of $5.192M and $1.880M EBITDA as volume and pricing improve. | This is the mature path with Year 5 revenue of $10.935M and $5.406M EBITDA, plus 1.47M scheduled gallons and 2,500 emergency jobs. |

| Typical setup | The model carries $588k fixed overhead, $780k payroll, and a 19.5% variable cost load, so the CEO's $185k salary needs capital support. | The business reaches 700,000 scheduled gallons, 1,200 emergency refill jobs, and a larger driver and support team while variable costs ease to 18.0%. | At this scale the business runs 20 drivers, 10 customer support FTEs, 2 operations managers, and a 49.4% EBITDA margin. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $185,000 salaryLow case | $1.880M EBITDABase case | $5.406M EBITDAHigh case |

| Best fit | Use this to stress-test launch-year cash burn and whether the owner can stay on payroll while cash bottoms near Month 13. | Best for checking the mid-scale case after routes, staffing, and service levels are stable. | Best for owners testing upside once fleet, tech, and support are fully scaled. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Heating Oil Delivery Service Porter's Five Forces Analysis

- Heating Oil Delivery Service BCG Matrix

- Heating Oil Delivery Service Business Model Canvas

- What Are The 5 KPIs For Heating Oil Delivery Service Business?

- Heating Oil Delivery Business Plan Template in Pre-Written Word

- How Increase Heating Oil Delivery Service Profits?

- What Are Operating Costs For Heating Oil Delivery Service?

- Heating Oil Delivery Startup Costs: $960K CAPEX Plus $350K Cash Gap

- Heating Oil Delivery Financial Model Template in Excel

- How To Start A Heating Oil Delivery Business In 3 To 6 Months

- How To Write A Business Plan For Heating Oil Delivery Service?

- Heating Oil Delivery Service Marketing Mix

- Heating Oil Delivery Service Marketing Plan

- Heating Oil Delivery Service Business Proposal

- Heating Oil Delivery Service PESTEL Analysis

- Heating Oil Delivery Pitch Deck Example Editable PPTX

- Heating Oil Delivery Service Business SWOT Analysis

- Heating Oil Delivery Service Value Proposition Canvas

Frequently Asked Questions

In this model, owner pay is planned at $185,000 per year before taxes That does not mean the company can distribute extra cash right away Year 1 EBITDA is -$340,000, breakeven arrives in Month 14, and minimum cash falls to -$350,000 in Month 13