Owner income$145K+

Owner income$145K+How Much Hempcrete Construction Owners Can Make on $335M Year 1 Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$145K+  Net margin43% to 70%

Net margin43% to 70% Revenue for target pay$3.35M

Revenue for target pay$3.35M Business difficultyMedium

Business difficultyMedium

Key Takeaways

- Collected completed jobs drive cash, not signed leads.

- Margin only grows if crews and collections hold.

- Fixed overhead is $27K monthly before owner pay.

- Profits can trap in projects, so protect reserves.

Owner income$145K+Net margin43% to 70%Revenue for target pay$3.35MBusiness difficultyMediumWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want the full Hempcrete Building Construction forecast?

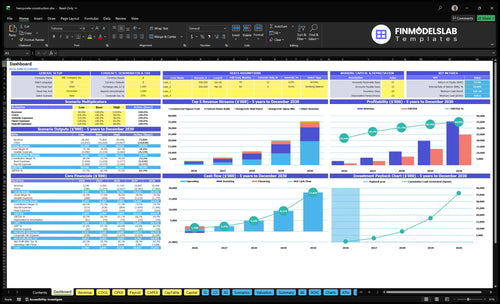

The dashboard shows $335M Year 1 revenue, $608M Year 2 revenue, 765% gross margin, $324K fixed overhead, $395K Year 1 payroll, and a $145K owner salary case; open the Hempcrete Building Construction Financial Model Template.

Owner-income model highlights

- Revenue, gross profit, operating profit

- $324K overhead, $395K payroll

- $145K owner pay case

- Project, cost, reserve flex

How much revenue does a hempcrete construction business need?

For Hempcrete Building Construction, there is no single revenue target. In the researched Year 1 model, $335M in revenue covers $145K owner pay, $324K fixed overhead, and $395K known payroll, and leaves about $157M before tax, debt, and reserves; that model also assumes a 765% gross margin, so every $100K collected creates about $765K gross profit before commissions, shipping, overhead, and payroll.

Year 1 math

- $335M revenue covers the model.

- $145K owner pay is included.

- $324K fixed overhead is covered.

- $395K known payroll is covered.

What changes the target

- Project mix changes the math.

- Gross margin drives cash left.

- Reserves change the needed revenue.

- No universal target applies.

How does scaling a hempcrete construction business affect owner income?

In Hempcrete Building Construction, scaling can raise owner income only when completed work, margin, and cash collection stay tight; otherwise higher volume just adds payroll, quality control, permitting, equipment, logistics, and reserve risk. In the hands-on owner mode, the CEO and operations role sits at $145K with direct project control, so income depends on what gets finished and collected.

Owner-led scale

- $145K CEO and ops role

- Year 2: 6 custom homes

- 25,000 commercial square feet

- $608M revenue at this scale

Project-managed scale

- Year 5: 22 custom homes

- 200,000 commercial square feet

- $3549M revenue at this scale

- Higher scale adds reserve risk

How do hempcrete project costs affect owner income?

Hempcrete project costs hit owner income fast because the direct cost base is already heavy: $125 on a $450 Year 1 panel before 20% revenue-based COGS, $90K on a $450K custom home before 20% COGS, and $17 per square foot on an $85 commercial price before 21% COGS. If you want the margin levers, How Increase Hempcrete Building Construction Profits? is the right next step. Better jobsite flow protects gross margin, but accounting profit still has to cover overhead and reserves.

Direct cost pressure

- $125 direct cost on a $450 panel

- 20% revenue-based COGS cuts income

- $90K direct cost on a $450K home

- 21% COGS on commercial jobs

What moves income

- Hemp hurds and lime binder swing cost

- Specialty labor and subcontractors add risk

- Drying or curing delays trap cash

- Rework eats gross margin fast

Want the six drivers that decide owner take-home?

1

4 homesProject Volume

Year 1 has 4 custom home builds, and owner pay rises only when more work is finished and billed, not just signed leads.

2

$450KContract Price

At $450K per custom home, small pricing gains add a lot of cash because each contract is large.

3

83.5%Gross Margin

The model's Year 1 gross margin is about 83.5%, so every point of cost control drops straight to profit.

4

$125Crew Productivity

Panel direct cost is $125 each, so faster crews, less waste, and fewer rework hours push income up.

5

$324KOverhead

Fixed overhead is $324K a year, so lean staffing and tight admin spend protect EBITDA fast.

6

$978KCash Reserves

The business needs a $978K cash floor in the weak month, so owner draws should wait until reserves are covered.

Hempcrete Building Construction Core Six Income Drivers

Completed Hempcrete Project Volume

Completed And Collected Project Volume

Income comes from finished, inspected, and collected work, not signed leads. Year 1 assumes 1,200 wall panels, 4 custom homes, 10,000 commercial square feet, 800 spray mix units, and 12 consulting packages; Year 2 rises to 1,800 panels, 6 homes, 25,000 square feet, 1,200 units, and 20 packages. More volume only lifts owner pay if crew capacity, inspection timing, and collections stay on pace.

Here’s the quick math: if jobs sit in progress or invoices lag, cash gets trapped in materials, labor, and retainage. The owner’s take-home improves only when gross margin holds and collected revenue keeps up with direct job costs. One clean rule: booked work is not spendable cash.

Track Completion To Cash

Measure completed units, invoiced units, and collected units separately for each line: panels, homes, commercial square feet, spray mix, and consulting. That shows where volume slips between field work and cash. If collections slow, owner draw should slow too, because profit on paper does not pay payroll or freight.

Use a weekly job log with crew hours, inspection dates, billing dates, and days sales outstanding (days to collect cash). If completion rises from Year 1 to Year 2 but rework or delays rise too, income can stall even with higher revenue. Volume only helps when delivery and cash conversion stay tight.

- Track completed, not booked, units.

- Bill right after inspection.

- Watch collections by project type.

- Compare rework hours by crew.

1

Average Contract Value And Scope Mix

Average Contract Value and Scope Mix

Scope mix decides how fast sales grow. A job mix built on $450 panels, $450K custom homes, $85 per commercial square foot, $120 spray mix units, and $5K consulting packages can lift revenue fast, but bigger tickets do not automatically lift owner pay. Larger contracts raise revenue, but profit only improves if scope stays tight.

Price by scope, not by hope

Track average contract value by job type, then compare it with the hours needed to deliver each scope. Commercial work can add scale, and consulting can be high-margin support if delivery hours stay controlled. If a bigger home or envelope adds too much redesign, site time, or follow-up, the extra revenue can vanish into labor and slower cash collection.

2

Gross Margin After Direct Job Costs

Gross Margin After Direct Job Costs

Gross margin is what’s left after direct job costs but before overhead and owner pay. In the model, $335M of revenue and about $256M of gross profit implies roughly 76.5% gross margin. That spread funds rent, admin, and the owner’s draw, so even small cost creep can cut take-home fast.

For panels, direct cost examples total $125 per unit: $45 hemp hurd, $30 lime binder, $25 timber framing, $15 direct labor, and $10 freight. If scope, testing, rework, or subcontractor work runs above plan, the gap between revenue and profit closes quickly. One clean rule: protect the job margin, or the owner pays for it later.

Protect Job Margin

Track each job by material, labor, freight, testing, equipment, and rework. Price change orders before work starts, and lock subcontractor scope in writing so direct costs don’t leak into overhead. Gross margin only improves when the team keeps every unit close to the planned cost base.

Use unit math on every quote: if a $450 panel carries $125 of direct cost, the gross profit is $325 and the gross margin is 72.2%. Compare that margin to actuals weekly, then fix the biggest drift first. The fastest leaks are usually freight overruns, extra site visits, and rework from poor mix or bad sequencing.

- Track actual cost per panel.

- Approve change orders first.

- Limit rework and extra freight.

- Lock subcontractor scope in writing.

3

Crew Productivity And Specialized Labor Efficiency

Crew Productivity And Specialized Labor Efficiency

Hempcrete labor hits owner pay through install speed, mix consistency, formwork coordination, curing time, and rework. In Year 1, custom home labor is $35K inside a $90K direct unit cost, so slow crews or bad sequencing can eat most of the job margin before overhead.

Commercial work is even tighter: $3 installation labor plus $1 onsite supervision per square foot. Here’s the quick math: if trained crews stay on plan, more square feet turns into more profit; if schedules slip, a high-revenue job can turn into cash tied up in payroll, delays, and fixes.

Track Labor Yield by Job Type

Measure labor hours per unit, rework rate, and installed square feet per crew day. Use the same scorecard for custom homes and commercial work, then compare actual labor cost to the $35K home benchmark and the $4 per square foot commercial benchmark. That tells you where labor is protecting margin and where it is leaking it.

Set crews, not just jobs. Tighten scheduling so mixing, placement, curing, and inspections happen in order, with no idle time. If volume rises without trained labor, margin drops fast; if the team is consistent, the owner keeps more take-home from each completed and collected project.

4

Fixed Overhead And Operating Costs

Fixed Overhead Before Owner Pay

Fixed overhead is the cost that shows up before the owner gets extra take-home. Here, it runs $27K per month or $324K per year, and Year 1 payroll adds $395K. That means the business needs about $719K a year just to cover overhead and payroll before any extra owner draw.

The fixed load includes a $12K manufacturing facility lease, $35K lab maintenance, $28K professional liability insurance, $5K marketing and trade shows, $12K administrative utilities, and $25K software licenses and ERP. Overhead is survivable when backlog is real and collections are current; if cash comes in late, owner pay gets squeezed first.

Track the Burn Rate Weekly

Measure fixed overhead, payroll, and days to collect cash every week. The key test is simple: do signed jobs and collected billings cov er the $719K annual fixed load before owner draws start? If not, pause hiring, trim nonessential spend, and keep the backlog tied to cash-in, not just signed work.

Build the forecast from four inputs: lease, lab costs, insurance, and staffing. Then test how long the business can absorb delayed collections. One clean rule helps: no new owner pay until overhead is covered and customer cash is landing on schedule.

- $27K monthly overhead floor

- $395K Year 1 payroll load

- $719K total before owner draw

5

Cash Reserves And Reinvestment Discipline

Cash Reserves And Reinvestment Discipline

Cash draw is not the same as accounting profit. This model shows about $157M of Year 1 operating profit before taxes, debt, and reserves, but cash can still get stuck in deposits, progress payments, delayed inspections, retainage, materials, freight, equipment rental, and payroll timing.

Owner pay should wait until working capital is funded, meaning the cash needed to keep day-to-day jobs moving. The reserve percentage is not provided, so the key rule is simple: if cash conversion is slow, profit does not equal safe distributions.

Pay yourself after the cash buffer

Track cash by job, not just by month. Measure deposits collected, progress billings, retainage due, material buys, freight, rental, and payroll timing so you can see how much cash is trapped in each project.

- Compare profit to bank cash monthly.

- Age retainage and unpaid progress bills.

- Set a project reserve before draws.

- Fund equipment and rework first.

Here’s the quick test: if profit is strong but collections lag, keep owner draw low until cash is actually in the bank. That protects payroll, supplier terms, and the next project start.

6

Compare lean, base, and high owner income scenarios

Owner income scenarios

Owner income moves with project volume, staffing, and cash timing here, so the same business can support very different pay levels across slow, modeled, and scale-up paths.

| Scenario | Low CaseCash risk | Base CaseMargin watch | High CaseStaffing strain |

|---|---|---|---|

| Launch model | This case assumes slower volume and keeps owner pay at the $145,000 role level only if cash stays healthy. | This is the modeled path that supports the core operating plan and the owner role from Year 1. | This case assumes later-scale demand and stronger execution across panels, builds, spray work, and consulting. |

| Typical setup | Revenue stays below plan, the owner stays in the CEO and Operations Director role, and hires stay light so cash can cover core overhead. | The model runs near Year 1 revenue of about $3.35M, with about $1.45M EBITDA, $324K fixed overhead, and $395K known payroll. | The business scales toward Year 3 revenue of about $11.14M and Year 5 revenue of about $35.49M, which means more staff, more project management, and more cash tied up in execution. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $145,000Pay capped | $145,000 - $250,000Modeled pay | $250,000 - $450,000Upside pay |

| Best fit | Use this to stress-test a slow sales start, delayed installs, or tighter cash. | Use this as the main planning case for budgets, hiring, and lender talks. | Use this to test upside if execution stays strong and staffing keeps up. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Hempcrete Building Construction Porter's Five Forces Analysis

- Hempcrete Building Construction BCG Matrix

- Hempcrete Building Construction Business Model Canvas

- What 5 KPI Metrics Should Hempcrete Building Construction Business Track?

- Hempcrete Building Business Plan Template in Pre-Written Word

- How Increase Hempcrete Building Construction Profits?

- What Are Hempcrete Building Construction Operating Costs?

- Hempcrete Construction Startup Costs: $560K CAPEX Plus Runway

- Hempcrete Construction Financial Model Template in Excel

- How to Start a Hempcrete Construction Business in 4-9 Months

- How To Write A Business Plan For Hempcrete Building Construction?

- Hempcrete Building Construction Marketing Mix

- Hempcrete Building Construction Marketing Plan

- Hempcrete Building Construction Business Proposal

- Hempcrete Building Construction PESTEL Analysis

- Hempcrete Building Construction Pitch Deck Example Editable PPTX

- Hempcrete Building Construction Business SWOT Analysis

- Hempcrete Building Construction Value Proposition Canvas

Frequently Asked Questions

The researched model supports a $145K CEO and operations salary if the owner fills that role It also shows $335M in first-year revenue and about $157M operating profit before taxes, debt, and reserves Extra owner take-home depends on cash needs, reinvestment, and project timing