Owner income$140k-$1.91M

Owner income$140k-$1.91MHow Much Home Insulation Business Owners Can Make: $140k EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$140k-$1.91M  Net margin19.4%-46.3%

Net margin19.4%-46.3% Revenue for target pay≈$720k

Revenue for target pay≈$720k Business difficultyHard

Business difficultyHard

You’re estimating owner pay before the company has steady job flow, crew output, and cash reserves This five-year planning model covers $720k to $4123M in annual revenue, EBITDA, labor, materials, overhead, marketing, startup cash, and owner take-home capacity These are planning assumptions, not salary promises, tax advice, or guaranteed distributions

Owner income$140k-$1.91MNet margin19.4%-46.3%Revenue for target pay≈$720kBusiness difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the full owner income model for Home Insulation Installation Service?

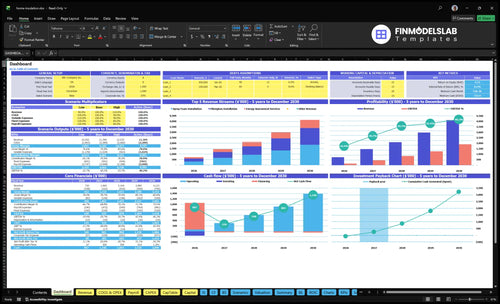

The screenshot shows revenue, EBITDA, cash, breakeven, payback, and owner income in the Home Insulation Installation Service Financial Model Template; open it.

Owner-income model highlights

- Owner pay before reserves

- Revenue and EBITDA ranges

- Assumptions and scenario tabs

How much can a home insulation business owner make?

A Home Insulation Installation Service owner can make $140k EBITDA on $720k revenue in Year 1, with modeled capacity rising to $191M EBITDA on $4,123M revenue by Year 5; see How Increase Profitability Home Insulation Installation Service? for the profit levers behind that spread.

Income drivers

- $140k Year 1 EBITDA

- $720k Year 1 revenue

- $8,350 monthly fixed overhead

- Owner pay is not fixed salary

Take-home limits

- $220k Year 1 wages

- $755k Year 5 wages

- Debt, taxes, reserves reduce cash

- Callbacks and reinvestment cut distributions

Can a home insulation business scale?

Yes—Home Insulation Installation Service can scale, but it gets cash-hungry before it gets easier for the owner. As crews grow from 1 lead technician and 1 junior assistant to 4 lead technicians and 6 junior assistants, revenue rises from $720k to $4.123M, while payroll jumps from $220k to $755k and marketing from $24k to $60k. Fixed overhead stays at $8,350 per month, but scaling also means vehicles, a spray foam rig, maintenance, insurance, inspections, warranty work, scheduling, and more working capital, so the owner shifts from selling and field work to estimating, crew supervision, quality control, and cash management.

What changes in scale

- Payroll climbs to $755k.

- Marketing rises to $60k.

- Fixed overhead stays at $8,350/month.

- Working capital gets tighter.

What the owner must do

- Buy and maintain vehicles.

- Add a spray foam rig.

- Handle inspections and warranty work.

- Focus on estimating and cash control.

What are typical insulation business profit margins?

If you’re pricing a Home Insulation Installation Service, the key point is that job-level margin can look strong, but company profit is lower once payroll and overhead hit. For a quick read on cost structure, see What Are Operating Costs Of Home Insulation Installation Service? — variable costs run from 30% of revenue in Year 1 to 26% in Year 5, so contribution stays at about 70% to 74% before fixed costs.

Job margin drivers

- Fiberglass jobs use 16 billable hours.

- Spray foam jobs use 24 billable hours.

- Assessments use 4 billable hours.

- Margin shifts with service mix and waste.

Cost pieces to watch

- Raw insulation materials: 18% to 16%.

- Job supplies: 4% to 32%.

- Fuel and vehicle operations: 45% to 37%.

- Commissions and referral fees: 35% to 31%.

Want the six drivers that move owner pay?

1

$330-$450Lead Quality

Lower CAC, from $450 to $330, and better close rates keep crews busy without letting marketing eat the margin.

2

$95-$205/hrJob Size

A better mix of spray foam and energy audits raises revenue per crew hour and lifts owner pay.

3

26%-30%Margin Mix

Cutting variable cost load from 30% to 26% leaves more of each job's billable dollars in the business.

4

12.5-14.0hCrew Utilization

More billable hours per active customer spread payroll and overhead across more revenue.

5

$8.35K/moOverhead Control

Holding fixed overhead near $8,350 a month helps extra sales turn into profit faster after Month 6 break-even.

6

HighRework

Fewer callbacks and warranty fixes protect labor time and materials, so more jobs turn into take-home.

Home Insulation Installation Service Core Six Income Drivers

Qualified Lead Flow And Close Rate

Qualified Lead Flow

Income here comes from sold jobs, not raw inquiries. With a $24k Year 1 online budget and $450 CAC (customer acquisition cost), the model buys about 53 sold jobs; at $60k and $330 CAC, it’s about 182 sold jobs. Better close rate and fewer wasted estimates lift cash flow, because more estimator time turns into paid work.

Cheap leads can look good and still hurt profit. If they raise cancellations, low-margin jobs, or unpaid estimate time, owner income falls even when lead volume rises. The real test is gross profit per lead source after fuel, follow-up, and the estimator’s time.

Track sold jobs, not clicks

Measure qualified homeowner leads, estimate close rate, sold jobs per month, and CAC per sold job by source. That tells you which channels pay back and which ones just create busy work.

- Review close rate by lead source weekly.

- Count wasted estimates and no-shows.

- Price by gross profit, not lead count.

- Cut sources that miss CAC targets.

One clean rule: if a channel fills the calendar but drops margin, it is not helping owner pay. Steadier lead quality keeps revenue more predictable and lowers cash stress when marketing spend rises from $24k to $60k.

1

Average Job Size And Service Mix

Average Job Size and Service Mix

Your income rises when each crew day sells for more than it costs to run. Here, the key input is revenue per crew day, driven by service type, billable hours, and pricing. Year 1 math puts fiberglass at $1,520 (16 hours × $95), spray foam at $3,960 (24 × $165), and energy assessments at $500 (4 × $125).

By Year 5, those tickets move to $1,840, $4,920, and $580. The mix also shifts from 55% fiberglass and 25% spray foam in Year 1 to 40% and 45% in Year 5, so average ticket should rise. That only helps if crew output, waste, and callbacks stay tight; otherwise the bigger ticket just hides margin leakage.

Track Ticket, Mix, and Rework

Watch sold jobs per service, billable hours per crew day, and callback hours. A spray foam day at $3,960 is about 2.6x a fiberglass day at $1,520, so shifting mix can lift revenue fast. But if rework climbs, the higher ticket won’t reach owner pay.

- Track ticket by service weekly

- Measure hours from estimate to close

- Separate rework from new work

- Review mix versus crew capacity

Use the mix to forecast cash, not just sales. When the book tilts toward spray foam, revenue per crew day rises, but labor, material, and equipment usage have to stay in line. That is the part that decides whether the owner sees more profit or just more busy days.

2

Material, Labor, And Job Gross Margin

Job Gross Margin

Job gross margin is what’s left after direct materials, labor, fuel, subcontractors, and referral commissions. In this model, direct and variable costs are 30% of revenue in Year 1, then 29%, 28%, 27%, and 26%, so every point of cost control lifts gross profit before overhead and owner pay.

Here’s the quick math: if revenue is $100,000, moving from 30% to 26% direct cost adds $4,000 of gross profit. That helps cover fixed overhead first; only the leftover can flow to EBITDA and then owner distributions. Gross margin is not EBITDA, and EBITDA is not take-home cash.

Track Direct Cost Drift

Measure the job, not just the month. Track estimate accuracy, material waste, labor hours per job, subcontractor percentage, and purchase price variance so you can see where margin leaks. One weak line item can erase the gain from better pricing.

- Insulation raw materials: 18% to 16%

- Fuel: 45% to 37%

- Referral and commission: 35% to 31%

- Consumables: verify 4% to 32%

Better buying, tighter crews, and less waste raise gross profit before overhead. If warranty or rework is high, this margin gets eaten fast, and owner pay shrinks even when sales look fine.

3

Crew Utilization And Jobs Completed

Crew Utilization And Jobs Completed

This driver is about how many billable crew days you sell and finish each month. In this model, staffing grows from 1 lead technician, 1 junior assistant, and 5 energy auditors in Year 1 to 4 lead technicians, 6 junior assistants, and 2 auditors in Year 5, while payroll rises from $220k to $755k. If jobs completed lag crew growth, owner pay gets squeezed fast.

Track jobs completed per month, billable hours per active customer, travel time, prep delays, failed access, and rework days. Billable hours per active customer rise from 125 to 140, so the business only wins if those hours stay paid. One bad week of failed access or rework can turn a full crew day into dead cost.

Measure Crew Time Like Cash

Use a simple check: sold jobs must cover payroll before you hire again. Here’s the quick math: more crew days help only if completion rate and billable hours rise with the team. Hiring ahead of demand drains cash because fixed payroll keeps running even when travel, prep, or access issues cut paid hours.

- Track paid hours, not just visits.

- Flag every failed-access job.

- Count rework as margin loss.

- Compare crew days sold to payroll.

Set a monthly target for completed jobs and review it against labor cost. If billable hours per active customer stay near 125 to 140 but completion slips, the owner feels it first in cash flow and then in take-home profit.

4

Overhead Discipline

Overhead Discipline

Overhead is the money that leaves the business before the owner gets paid: rent, insurance, utilities, software, equipment maintenance, accounting, and professional services. In this model, fixed overhead is $8,350 per month, while marketing adds $24k to $60k per year and payroll is the largest load at $220k to $755k per year. That mix directly cuts owner take-home.

The key metric is overhead as a percent of revenue. Here’s the quick math: if overhead rises faster than sales, monthly break-even revenue climbs and cash gets tight. One clean rule: lean overhead improves cash resilience during slow months, because there’s more room to cover labor, fuel, and the owner’s draw after the bills are paid.

Keep Fixed Costs Tight

Track monthly overhead, admin cost per job, vehicle cost per crew, and software cost per user. Tie each cost to a job count or crew count, so you can see if a new hire or tool actually lowers cost per completed project. If overhead per job keeps rising while sold j obs stay flat, owner pay gets squeezed fast.

Test each cost against revenue, not gut feel. Build a monthly check on break-even revenue and flag any cost that does not support a booked job, faster install, or cleaner close. Keep software and professional services lean, and trim unused vehicles or office space before they turn into permanent cash drag.

- Measure overhead as a percent of revenue.

- Match admin cost to sold jobs.

- Track vehicle cost per active crew.

- Review software seats monthly.

5

Callbacks, Warranty Work, And Rework

Callbacks And Rework

When a crew has to come back for failed inspections, moisture issues, air sealing misses, or an under-scoped job, that day stops earning. These costs hit gross margin first, then EBITDA and owner pay, because the original sale already booked the revenue. The calculator should let you enter a warranty reserve as a percentage or dollar amount per job, since quality slips turn paid labor into unpaid labor.

Track callback rate, rework hours, failed inspection count, warranty cost per job, and customer complaint trend. The core math is gross margin leakage = rework labor + return trips + fix materials. If spray foam mistakes tie up crews, equipment, and cash, reported profit can look fine while take-home income quietly drops.

Control Warranty Leakage

Build the reserve into each estimate and compare it with actual callbacks every month. If the reserve is too low, owner draws come out of cash; if it is too high, pricing may need to move up. One clean rule: log every callback by cause, crew, and cost so training, scope checks, and pricing can fix the weak spots.

- Track cost by job.

- Tag every rework cause.

- Review failed inspections weekly.

- Price reserve into estimates.

6

Owner income scenario table objective

Owner income scenarios

Owner income rises as the crew scales, CAC falls, and the mix shifts toward higher-value spray foam and energy assessments. Early years carry heavier marketing and payroll, so cash use is front-loaded.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lean owner-income case with the slowest modeled earnings path. | This is the modeled owner-income case for a steadier operating pace. | This is the stronger owner-income case with the best modeled earnings path. |

| Typical setup | Year 1 model at $720k revenue and $140k EBITDA, with 30% variable costs, $24k marketing, $450 CAC, and about $220k payroll before the crew fully scales. | Year 3 model at $2.104M revenue and $834k EBITDA, with 28% variable costs, $40k marketing, $390 CAC, and $441k payroll as the mix shifts toward spray foam and assessments. | Year 5 model at $4.123M revenue and $1.910M EBITDA, with 26% variable costs, $60k marketing, $330 CAC, and $755k payroll on a mature crew and stronger spray foam mix. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $140kLow Case | $834kBase Case | $1.91MHigh Case |

| Best fit | Use this to stress-test a launch with one core crew and heavier startup cash use. | Use this as the main planning case for a stabilized third-year operation. | Use this to test upside if sales efficiency holds and capacity stays filled. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Related Products

- Home Insulation Installation Service Porter's Five Forces Analysis

- Home Insulation Installation Service BCG Matrix

- Home Insulation Installation Service Business Model Canvas

- What Are The 5 KPI Metrics For Home Insulation Installation Service Business?

- Home Insulation Installation Service Business Plan Template in Pre-Written Word

- How Increase Profitability Home Insulation Installation Service?

- What Are Operating Costs Of Home Insulation Installation Service?

- Home Insulation Business Startup Costs: $727K Cash Plan

- Home Insulation Financial Model Template in Excel

- How To Open A Home Insulation Installation Service In 6 To 12 Weeks

- How To Write A Business Plan For Home Insulation Installation Service?

- Home Insulation Installation Service Marketing Mix

- Home Insulation Installation Service Marketing Plan

- Home Insulation Installation Service Business Proposal

- Home Insulation Installation Service PESTEL Analysis

- Home Insulation Installation Service Pitch Deck Example Editable PPTX

- Home Insulation Installation Service Business SWOT Analysis

- Home Insulation Installation Service Value Proposition Canvas

Frequently Asked Questions

This model shows a $727k minimum cash need, with the low point in Month 2 Startup capex totals $1633k, including a $68k spray foam rig, $52k box truck, and $145k fiberglass blowing machine The rest of the cash cushion covers payroll, rent, insurance, marketing, materials, and early ramp-up losses before breakeven