Owner income$292k–$1.74M

Owner income$292k–$1.74MHow Much Can a Homemade Ice Cream Shop Owner Make? $292k Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$292k–$1.74M  Net margin24%–53%

Net margin24%–53% Revenue for target pay$1.23M–$3.29M

Revenue for target pay$1.23M–$3.29M Business difficultyHard

Business difficultyHard

Key Takeaways

- Traffic volume drives most revenue, especially on weekends.

- Ticket size lifts sales only when demand holds.

- Labor and ingredients can erase sales if uncontrolled.

- Fixed costs and off-premise sales shape break-even timing.

Owner income$292k–$1.74MNet margin24%–53%Revenue for target pay$1.23M–$3.29MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see how owner income is built?

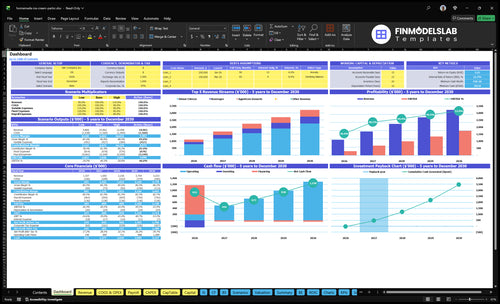

This screenshot in the Homemade Ice Cream Shop Financial Model Template shows how revenue assumptions flow into cash flow, EBITDA, reserves, and owner take-home. Open the model to see the full forecast.

Owner-income model highlights

- Revenue spans $123M to $329M

- EBITDA ranges $292k to $1,738M

- Breakeven lands Month 3

- Payback hits 14 months

- Weekday traffic drives AOV

- COGS and payroll squeeze cash

- Capex can delay payback

- Not guaranteed distributions

How much does a homemade ice cream shop owner take home?

A Homemade Ice Cream Shop owner’s Year 1 take-home capacity is $292k of EBITDA, but that’s before taxes, debt, reserves, and actual distributions; for what to track first, see What Is The Most Important Indicator Of Success For Your Homemade Ice Cream Shop?. The quick math is 770 weekly customers × $30.65 weighted ticket × 52 weeks = about $1.23M revenue, with an 85.0% gross margin after ingredients and packaging.

Owner cash reality

- $292k Year 1 EBITDA pool

- Not the same as sales

- Not guaranteed owner draw

- Taxes and debt come first

Cash guardrails

- Hold working cash for slow months

- Reserve for equipment repairs

- Fund reinvestment before expansion

- Year 5 EBITDA: $1.738M on $3.29M

Does an ice cream shop make more if the owner works in it?

Yes—an owner-operator can make the Homemade Ice Cream Shop look more profitable, because replacing a $60k restaurant manager can lift EBITDA by up to $60k before taxes. But those hours are not free; the owner is buying a job, and if they step out, the shop still needs paid coverage for counter, prep, and dishwashing. Seasonal staffing gaps can also cut hours or service quality, so the gain only holds if scheduling stays tight.

Owner-operator upside

- Replace the $60k manager role.

- Lift EBITDA by up to $60k.

- Keep payroll lean at first.

- Work the floor, then watch cash flow.

Owner cost and scale

- Unpaid hours still have real value.

- Absentee ownership needs paid coverage.

- Seasonal gaps can hurt service quality.

- Scaling needs managers and tighter schedules.

What profit margin does an ice cream shop need?

The Homemade Ice Cream Shop needs a very high gross margin, and homemade production only works if portion control protects gross profit. The provided Year 1 model shows 140% food and beverage cost, 10% packaging, and another 45% for online commissions and marketing, so profit gets tight fast; for startup cost context, see What Is The Estimated Cost To Open Your Homemade Ice Cream Shop?

Cost stack

- 140% food and beverage cost

- 10% packaging cost

- 45% commissions and marketing

- 805% before labor and fixed costs

Margin leaks

- $401k payroll in Year 1

- 327% of Year 1 revenue

- $1,356k fixed overhead

- Over-scooping, wasted batches, freezer loss

Want to see what moves owner income most?

1

770/wkCustomer Volume

Year 1 volume is the main income engine, because more covers spread the shop's fixed costs faster.

2

$30.65Ticket Size

A higher weighted ticket lifts revenue from each visit without needing more foot traffic.

3

85%Gross Margin

Strong scoop margin keeps more cash from each sale before labor and rent hit.

4

$401KLabor Control

Payroll is the biggest cost block, so staffing to demand changes owner take-home quickly.

5

$136KFixed Overhead

Rent and other fixed bills set the break-even floor, so they decide how much volume you need.

6

4.5%Online Sales

Online orders can add sales, but commissions and promo spend will trim each dollar if they run too hot.

Homemade Ice Cream Shop Core Six Income Drivers

Customer Volume And Seasonality

Customer Volume And Seasonality

Traffic is the top revenue lever for a homemade ice cream shop. In the model, Year 1 runs from 50 customers on Monday to 200 on Saturday, or about 770 per week; by Year 5, that climbs to 1,730 per week. As daily volume rises, revenue moves from $123M to $329M, so every extra customer matters most on weekends because the ticket is higher.

This driver is built from customer count, open days, and weekday vs. weekend mix. Warm weather, school breaks, tourist flow, and neighborhood density can lift demand fast, but rain and winter can cut it hard. More traffic helps owner pay only if the shop can handle it without long lines, freezer limits, or staff shortages.

Track Traffic By Day

Measure covers by day, weekend share, and sales per open day. That tells you if growth is real or just noisy. Here’s the quick math: if Saturday checks are bigger, then one extra Saturday customer does more for profit than one extra Monday customer, so weekend staffing and stock should be tighter.

Watch for rainy days, winter demand, and school-break spikes. If lines get long, add labor before you lose sales. If freezer space runs tight, cut low-velocity flavors first. Keep a weather and event log, then compare it to traffic so you can forecast cash and protect owner draw.

- Track covers by daypart

- Separate weekday and weekend checks

- Log weather and school breaks

- Match labor to peak traffic

- Monitor freezer and prep limits

1

Average Ticket And Upsells

Average Ticket And Upsells

For this shop, average ticket is the revenue from each guest before you count fixed costs. It turns the same foot traffic into more cash, so if midweek AOV moves from $28 in Year 1 to $34 in Year 5, every 100 orders adds $600 more sales. Weekend AOV rises from $32 to $38, so upsells matter most when traffic is already strong.

Upsells include sundaes, flights, shakes, pints, cones, toppings, premium flavors, and take-home packs. Here’s the quick math: higher ticket helps owner income only if orders still hold up. If pricing pushes guests away, service slows, or mix-ins and discounts eat margin, the extra sales can miss the mark and leave less profit to pay the owner.

Track Ticket, Mix, and Margin

Measure orders, AOV by daypart, add-on rate, and gross margin by item. Midweek and weekend checks should be tracked separately, since the model assumes $28 midweek and $32 on weekends in Year 1, rising to $34 and $38 by Year 5. That split shows whether upsells are real or just discount-driven volume.

- Test toppings and premium flavors first.

- Watch service time during rushes.

- Limit discounts that cut owner income.

- Price take-home packs above ingredient cost.

2

Gross Margin And Ingredient Control

Ingredient Control

Gross margin here is the cash left after cream, sugar, stabilizers, inclusions, and packaging. In the model, Year 1 food and beverage cost is 140%, packaging is 10%, and gross margin is 850%; by Year 5, it improves to 862%. That gap matters because every heavy scoop or wasted pint cuts the owner’s draw.

The risk is simple: over-scooping, freezer burn, wasted batches, supplier price jumps, and low-yield recipes can turn strong sales into weak cash. One clean line: sell less waste, keep more profit. If portions drift or yields fall, the shop can look busy while take-home income still gets squeezed.

Tighten Portions

Track recipe cost per batch, target yield, and actual portion weight for cones, cups, pints, and spoons. Use the same standard scoop and log shrink from melting, freezer burn, and prep loss. The key inputs are ingredient cost, packaging cost, and how many servings each batch really produces.

- Weigh random scoops each shift.

- Reprice after supplier jumps.

- Flag low-yield recipes fast.

- Write portion rules for every item.

If a batch yields less than planned, the fix is not more sales, it’s tighter prep control. Honest math beats guesswork: a small cost leak on every serving hits gross margin all day, then shows up in slower cash flow and a smaller owner paycheck.

3

Labor, Owner Hours, And Staffing

Labor, Owner Hours, And Staffing

Payroll is the biggest cash cost after product, so this driver decides how much sales turn into owner pay. In Year 1, payroll is $401k; by Year 5, it rises to $6,095k. Staffing covers the chef, sous chef, prep cooks, manager, servers, host, and dishwasher. Owner-run shifts can cut paid labor, but that time is still work.

Here’s the quick math: more breakfast, brunch, dinner, and dessert traffic needs more prep and service hours, while slow winter days can leave labor idle. The pressure points are overtime, manager coverage, and training churn. If the schedule misses daypart demand, labor eats profit and shrinks the cash left for the owner’s draw.

Schedule To Traffic

Build schedules from actual traffic by daypart and season. Match prep time to production, and keep a lean backup plan for weekends, school breaks, and slow winter shifts. Track labor as a share of sales, sales per labor hour, and overtime hours. That tells you if each shift is creating enough cash to support owner pay.

- Track sales by hour.

- Review overtime weekly.

- Log owner hours worked.

- Watch winter labor waste.

- Measure training churn costs.

Use owner-operated shifts when they replace paid labor on busy days, but treat that time as real cost, not free labor. If staffing is too thin, lines get longer, prep slips, and manager coverage breaks down. If staffing is too heavy, payroll rises faster than sales and the owner feels it in lower take-home income.

4

Rent, Utilities, And Fixed Costs

Fixed Overhead Hurdle

Fixed costs set the monthly hurdle before owner pay. In this model, fixed overhead is $113k per month or $1,356k per year, and breakeven occurs in Month 3. The listed fixed items include $8k rent, $15k utilities, $600 cleaning, $500 property taxes, $300 insurance, $150 POS, $50 website, and $200 admin supplies.

This driver hits owner income fast: every month below that hurdle delays profit and leaves less room for a draw. What this estimate hides is the seasonal cash squeeze from freezer power use, HVAC load, equipment repairs, lease escalations, and slow months, which can turn a profitable year into a tight cash year.

Track the Fixed-Cost Run Rate

Measure fixed costs monthly, not yearly. Track rent, utilities, repairs, and admin spend against the $113k overhead target, then flag any drift early. If utilities spike from freezer or HVAC load, or a lease step-up hits, the owner’s take-home drops unless sales rise enough to cover it.

Build a cash buffer before owner pay. Stress-test the model for slow weeks and repair bills, then hold back draw until fixed costs are covered with room to spare. A simple rule helps: if recurrin g overhead keeps rising, owner pay should wait, because the business is still funding the building, the equipment, and the monthly bill stack.

- Track rent and utility spikes

- Budget repairs every month

- Watch lease escalation dates

- Protect cash for slow months

5

Off-Premise Sales Channels

Off-Premise Sales Channels

Off-premise sales can smooth slow weeks and use more of each batch, but they only raise owner pay if the extra revenue beats packaging, delivery, and labor. This channel includes catering carts, local events, packaged pints, ice cream cakes, preorders, delivery, and local wholesale. Online ordering commissions are 25% of Year 1 revenue, improving to 20% by Year 5, so every $1,000 in online sales leaves $750 before other direct costs.

The real test is batch utilization. If off-premise orders fill planned production without overtime, spoilage, or freezer overflow, they lift cash flow and spread fixed costs over more sales. If they add lower wholesale margin, melt claims, or extra prep time, the owner can sell more and still take home less.

Measure margin by channel, not just sales

Track off-premise revenue by channel, then separate commission, packaging, delivery, and labor per order. If a channel cannot cover its own direct costs and still leave room for overhead, it is hurting owner income even when sales look strong. Watch freezer space, prep lead time, and on-time delivery rate; those are the pressure points.

- Test preorders before delivery.

- Cap wholesale to spare capacity.

- Price packaging into each order.

- Schedule batches to demand peaks.

6

Compare low, base, and high owner-income cases

Scenario table

Weekly customer count, ticket size, payroll, and overhead move owner-income capacity fast in this shop. These cases show how the earnings path changes from Year 1 to Year 5.

| Scenario | Low CaseLower earnings | Base CaseModeled core | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lower-earnings case built from Year 1 traffic and the lowest modeled EBITDA. | This is the modeled middle case built from Year 3 traffic and the midpoint EBITDA path. | This is the stronger-earnings case built from Year 5 traffic and the highest modeled EBITDA. |

| Typical setup | About 770 weekly customers, a lower ticket path, and Year 1 payroll and overhead support about $292k of EBITDA capacity. | About 1,300 weekly customers, a stronger ticket mix, and a larger staff load support about $994k of EBITDA capacity. | About 1,730 weekly customers, the highest ticket mix, and the largest payroll run rate support about $1.738M of EBITDA capacity. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $292kPlanning floor | $994kCore plan | $1.738MUpside view |

| Best fit | Use this to stress-test the business if demand starts slower than planned. | Use this as the main planning case for budgeting and hiring decisions. | Use this to test upside if traffic, pricing, and throughput all hold. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Homemade Ice Cream Shop Porter's Five Forces Analysis

- Homemade Ice Cream Shop BCG Matrix

- Homemade Ice Cream Shop Business Model Canvas

- 7 Essential KPIs to Track for a Homemade Ice Cream Shop

- Homemade Ice Cream Shop Business Plan Template in Pre-Written Word

- Increase Homemade Ice Cream Shop Profitability with 7 Key Strategies

- How to Calculate Monthly Running Costs for a Homemade Ice Cream Shop

- How Much It Costs To Open A Homemade Ice Cream Shop: $240k+ Plan

- Homemade Ice Cream Shop Financial Model Template in Excel

- How to Open a Homemade Ice Cream Shop in 3 to 9 Months

- How to Write a Business Plan for a Homemade Ice Cream Shop

- Homemade Ice Cream Shop Marketing Mix

- Homemade Ice Cream Shop Marketing Plan

- Homemade Ice Cream Shop Business Proposal

- Homemade Ice Cream Shop PESTEL Analysis

- Homemade Ice Cream Shop Pitch Deck Example Editable PPTX

- Homemade Ice Cream Shop Business SWOT Analysis

- Homemade Ice Cream Shop Value Proposition Canvas

Frequently Asked Questions

The modeled owner-income pool is $292k EBITDA in Year 1 before taxes, debt, reserves, and distributions That comes from about $123M in revenue, 850% gross margin, $401k payroll, and $1356k fixed overhead Actual take-home depends on how much cash the owner keeps inside the business