Owner income$200K

Owner income$200KHow Much Hospital Construction Owners Make: $200K Salary Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$200K  Net margin24% to 4%

Net margin24% to 4% Revenue for target pay$5.8M

Revenue for target pay$5.8M Business difficultyHard

Business difficultyHard

A hospital construction company owner can model a $200K salary, but distributions only appear after project profit covers overhead, payroll, marketing, reserves, and cash timing In the researched base case, Year 3 revenue is about $314M, contribution profit is about $230M, and operating profit before taxes, reserves, and debt service is about $839K Year 1 and Year 2 show losses after the planned owner salary, so early take-home may need startup capital Bonding capacity, retainage, payment delays, and reinvestment needs can hold back cash even when accounting profit looks strong

Owner income$200KNet margin24% to 4%Revenue for target pay$5.8MBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want the full income forecast?

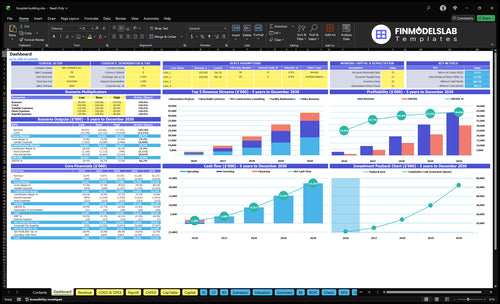

This dashboard in the Hospital Construction Financial Model Template covers assumptions, revenue build-up, direct costs, payroll, fixed overhead, marketing, CAC, owner income, scenarios, and cash timing. It charts revenue from $5,798K to $722M, contribution margin from 710% to 755%, and operating profit from -$5,609K in Year 1 to $205M in Year 4; it’s a planning tool, not a promise of income.

Owner income model highlights

- Owner income is shown

- Revenue and margin charts

- Scenarios and cash timing

How much does a hospital construction company owner make per year?

A Hospital Construction owner’s modeled pay is $200,000 per year as CEO/founder salary, but real owner income equals salary plus any distributions the company can safely pay. For context, What Is The Current Growth Rate Of Hospital Construction Projects For Your Business? matters because growth can raise backlog, yet Year 1 shows $5.798M revenue and -$5.609M operating profit after salary, so that paycheck may need funding.

Owner pay

- $200K modeled CEO/founder salary

- Distributions depend on profit and cash

- Year 1 profit: -$5.609M

- Salary may need outside funding

Cash reality

- Year 3 revenue reaches $314M

- Operating profit hits $8.391M

- Profit is before taxes and debt

- Retainage means held-back project cash

How much revenue does a hospital construction company need to pay the owner?

For Hospital Construction, the right question is margin and overhead, not a simple revenue multiple. With about $146M of Year 3 overhead, a $200K owner salary, and a 732% contribution margin, break-even revenue is about $199M; add a $300K pre-reserve distribution, and required revenue rises to about $240M.

Owner pay floor

- $146M Year 3 overhead

- $200K owner salary

- $199M break-even revenue

- $240M with $300K distribution

Scale limits to watch

- $314M modeled Year 3 revenue

- $8.391M operating profit before reserves

- Staff and project management capacity

- Insurance, bonding, and reserve needs

How do cost overruns affect construction owner income?

Cost overruns cut owner income dollar for dollar once the contract margin is set. In Hospital Construction, a 1 margin point on $314M Year 3 revenue is about $314K of profit, and on $519M Year 4 revenue it is about $519K; for build-cost context, see How Much Does It Cost To Open The Hospital Construction Business?. The biggest hits come from change orders not billed, scope creep, labor escalation, subcontractor buyout misses, materials pricing, schedule delays, compliance work, and warranty exposure, so margin control is the main income lever.

Where income leaks

- Unbilled change orders cut profit fast

- Scope creep adds cost without revenue

- Labor and materials can reset margin

- Delays raise compliance and warranty costs

What the model shows

- Direct and project-variable costs drop from 290% to 245%

- That shift makes margin control the key lever

- $314K rides on one point at Year 3 revenue

- $519K rides on one point at Year 4 revenue

Want to see what moves owner income?

1

↑20%-40%Backlog

More booked work fills the crew, and the new-build share rises from 20% in Year 1 to 40% in Year 5.

2

↑$150-$300/hrProject Mix

A shift toward new builds and consulting lifts bill rates, while more maintenance pulls them down.

3

↓20%-18%Margin Control

Keeping material and subcontractor fees tight keeps more of each project dollar in EBITDA as the model moves from 20% to 18%.

4

↓$700K-$1.34MLabor Spend

Payroll rises fast from Year 1 to Year 4, so underused labor cuts owner take-home quickly.

5

↓$223KOverhead

Fixed overhead runs about $223K a year before the $200K owner salary, so idle capacity hurts income fast.

6

↑$663KCash Buffer

Cash bottoms at $663K in Month 4, and breakeven also lands in Month 4, so billing delays hit hard.

Hospital Construction Core Six Income Drivers

Annual Project Backlog

Annual Project Backlog

Annual backlog is the signed work lined up for the year, but it is not owner income until crews finish work, billings get approved, and cash is collected. In this model, revenue rises from $5,798K in Year 1 to $314M in Year 3 and $519M in Year 4, driven by customers, mix, hours, and rates.

The key test is delivery capacity. If backlog grows faster than project managers, subcontractors, or working capital, profit can look strong on paper while cash stays tight. Backlog is not cash. The owner only benefits when backlog turns into contribution profit, not just signed contracts.

Track Deliverable Backlog

Measure backlog by customers, project mix, billable hours, and rates, then tie it to approved progress billings and cash collection timing. That tells you how much backlog can become real owner pay. Also watch project manager load and subcontractor availability, because those are the usual bottlenecks.

Use a simple rule: do not add work that pushes backlog past delivery capacity. If completed work, billing approvals, and cash receipts slip, operating profit may not reach the owner. More backlog helps only when it converts to cash, so forecast by month, not just by signed contract value.

1

Average Project Size And Mix

Project Mix Drives Margin Quality

Average project size and mix change income more than top-line alone. In the model, new builds move from 200% to 400%, renovations from 500% to 550%, pre-construction consulting from 700% to 500%, and facility maintenance from 100% to 300%. New builds bring more hours and revenue per customer, but they also pull more project management time and cash before the job closes.

Owner pay improves when the mix matches delivery capacity. Consulting can earn higher hourly rates, but it uses fewer hours. Renovations and maintenance can smooth backlog and billing, while too many large new builds can strain crews and delay cash. Mix that fits capacity usually turns more revenue into usable profit.

Track Mix by Hours and Cash

Measure average contract value, billable hours per project, gross margin by project type, and days from invoice to cash. Here’s the quick math: if a larger project needs more labor, more subcontractor time, and longer billing cycles, the owner may see slower draws even when revenue rises.

Push more work into the mix that your team can finish and bill on time. Use renovations and maintenance to fill gaps between large hospital builds, and price consulting so senior time is covered. If onboarding or approvals run long, cash risk rises before profit reaches the bank.

- Track revenue by project type.

- Track hours per contract.

- Track billing delay and retainage.

- Track PM capacity weekly.

- Track margin by mix.

2

Gross Margin And Change-Order Control

Change-Order Margin Control

Owner income moves fast when estimating, scope control, subcontractor buyout, and change-order billing hold the line on margin. In the model, gross margin after material, subcontractor, and project software costs improves from 770% to 800%, and contribution margin rises from 710% to 755% after project sales and compliance costs.

Here’s the quick math: one margin point is worth about $314K at Year 3 revenue and $519K at Year 4 revenue. The risk is simple: unpaid change orders, vague scopes, rework, and compliance delays turn booked work into weaker cash and thinner owner draw.

Track the margin leak

Track four things on every job: scope freeze date, change-order approval lag, rework dollars, and unbilled extras. If a change order is not signed before work starts, treat it as margin at risk, not profit. That keeps the owner from mistaking revenue growth for real take-home income.

- Price scope gaps before mobilization.

- Bill changes the same week.

- Lock subcontractor buyout early.

- Escalate compliance delays fast.

What this estimate hides: even strong project volume can miss owner pay if margins slip on a few large jobs. The fix is tighter estimating and faster billing, because every recovered point protects cash and makes distributions more reliable.

3

Subcontractor, Labor, And Materials Cost Management

Direct Cost Control

In hospital construction, this driver is the gap between billed revenue and direct job costs. When material and subcontractor fees fall from 200% to 180% of revenue, project software drops from 30% to 20%, and sales and compliance costs drop from 60% to 45%, more of each dollar stays in gross profit. That lifts owner income because overhead has less profit to consume.

It depends on subcontractor quotes, labor hours, material takeoffs, project software, and compliance scope. Better buyout, fewer coordination misses, tighter purchasing, and clearer scopes raise contribution margin and reduce the need for contingency reserves. One line: small cost leaks hit take-home pay fast.

Track the Cost Leaks

Measure this weekly at the job level: bid vs. buyout, labor hours vs. estimate, material variance, and change-order recovery. If these drift, profit gets trapped in rework, extras, and reserve padding instead of reaching the owner.

- Compare buyout to estimate.

- Watch labor hours every week.

- Audit material takeoffs early.

- Lock compliance scope in writing.

Use these controls before overhead lands. If direct costs stay down, gross margin improves, cash pressure eases, and the owner can draw more profit without gambling on late fixes.

4

Overhead, Bonding, Insurance, And Management Capacity

Overhead and Capacity Fit

Overhead only helps the owner if it stays aligned with completed revenue. In this model, fixed operating costs are stated at $1,855K per month and $2,226K per year, business insurance is $2K per month, and payroll rises from $700K in Year 1 to $1055M in Year 3 and $134M in Year 4, so the payroll schedule should be reconciled before use.

Bonding capacity should sit in its own input because no bonding percentage is given. That matters in hospital construction, where estimators, project managers, safety, compliance, accounting, and office staff must support profitable backlog without outrunning billings. If support costs grow faster than work completed, owner pay drops even when backlog looks strong.

Track Fixed Cost Coverage

Use a simple test: fixed overhead, insurance, and payroll should be covered by gross profit from completed work, not signed backlog. One clean rule: if m onthly gross profit cannot pay the support team and insurance, the owner should slow hiring or push for higher-margin work.

- Separate bonding from overhead.

- Review staffing against backlog monthly.

- Match PMs to billable work.

- Watch payroll before revenue grows.

5

Cash Flow Timing, Retainage, And Reserves

Cash Timing And Retainage

Cash available to the owner is not the same as operating profit. In hospital construction, money can sit in progress billings, retainage (cash the client holds back), equipment, and project reserves. Even with $8,391K Year 3 operating profit, owner draws can lag if billing approvals are slow or cash is still tied up in jobs.

Billing delay, retainage timing, reserve percentage, debt service, and reinvestment needs are the inputs that matter here. If the model does not include them, it will overstate take-home pay and understate working capital strain. That usually means lower near-term owner income, but safer delivery capacity on complex healthcare projects.

Track Cash Release, Not Just Profit

Build a cash schedule by project. Track when invoices go out, when cash lands, how much is held as retainage, and how much stays back as a reserve. Also separate debt service from reinvestment cash so owner draws do not compete with payroll, subcontractors, or equipment payments.

- Billing delay in days

- Retainage percent and release date

- Reserve cash by project

- Monthly debt service

- Planned reinvestment spending

6

Compare lean, base, and high-performance owner income scenarios

Owner income scenarios

Owner income moves with contract mix, staffing, and how much profit stays in the business for reserves and debt service. Bigger projects lift profit fast, but take-home still depends on funding and reinvestment.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the downside path, where the business stays funded but owner take-home is limited. | This is the modeled operating path, where the company runs on steady project flow and planned overhead. | This is the upside path, where scale and margin expansion drive very high owner earnings. |

| Typical setup | Revenue stays at the low end of the model, operating profit remains negative, and the founder only draws a $200K salary if funding is available. | Revenue reaches $314M, contribution margin holds at 732%, and operating profit is $8.391M before taxes, reserves, debt service, and reinvestment. | Year 4 revenue reaches $519M, contribution margin holds at 745%, and operating profit before exclusions reaches $205M, with Year 5 revenue at $722M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $200KLow income | $8.4MModeled income | $205MUpside income |

| Best fit | Use this to test what happens if project wins are slow and profit stays under pressure. | Use this as the core plan if you expect a funded CEO role and stable project execution. | Use this to test upside, but do not treat take-home as guaranteed. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Hospital Construction Porter's Five Forces Analysis

- Hospital Construction BCG Matrix

- Hospital Construction Business Model Canvas

- 7 Critical KPIs for Hospital Construction Profitability

- Hospital Construction Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Hospital Construction Profitability

- Running Costs: How Much To Operate A Hospital Construction Business

- Hospital Construction Startup Costs: $440K CAPEX Plus Cash Runway

- Hospital Construction Pro Forma & 5-Year Financial Model Template in Excel

- How To Start A Hospital Construction Company In 6 To 12 Months

- How to Write a Hospital Construction Business Plan in 7 Steps

- Hospital Construction Marketing Mix

- Hospital Construction Marketing Plan

- Hospital Construction Business Proposal

- Hospital Construction PESTEL Analysis

- Hospital Construction Pitch Deck Example Editable PPTX

- Hospital Construction Business SWOT Analysis

- Hospital Construction Value Proposition Canvas

Frequently Asked Questions

The researched case shows operating profit of -$5609K in Year 1, -$1640K in Year 2, $8391K in Year 3, and $205M in Year 4 before taxes, reserves, debt service, and reinvestment The owner salary is modeled separately at $200K, so distributions depend on cash left after project needs