Owner income$18k–$349k

Owner income$18k–$349kHow Much Do Hostel Owners Make? $18k-$349k EBITDA Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$18k–$349k  Net margin2%–27%

Net margin2%–27% Revenue for target pay$817k–$1.3M

Revenue for target pay$817k–$1.3M Business difficultyHard

Business difficultyHard

A hostel owner in this model does not have much safe take-home in Year 1 because EBITDA is only $18k after operating costs By Year 3, EBITDA reaches $145k, and by Year 5 it reaches $349k, before taxes, debt service, reserves, and reinvestment If the owner also replaces the $70k general manager role, the business may support more owner pay, but that is pay for labor, not passive profit These are researched assumptions, not guaranteed hostel owner income

Owner income$18k–$349kNet margin2%–27%Revenue for target pay$817k–$1.3MBusiness difficultyHardWant to test your hostel profit calculator assumptions?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on demand, margins, payroll, debt, reserves, and taxes.

Want to see the Hostel financial model behind the numbers?

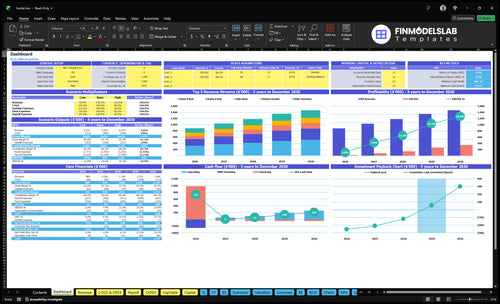

The dashboard in the Hostel Financial Model Template ties assumptions, revenue, staffing, fixed costs, capex, cash flow, EBITDA, owner pay, and scenarios together. It also charts occupancy, revenue, EBITDA, minimum cash, and payback, with outputs showing a $725k minimum cash need, Month 15 cash low point, Month 5 break-even, 48-month payback, and EBITDA from $18k to $349k. Open the model to check your own numbers.

Model highlights

- Owner pay assumptions built in

- Revenue, EBITDA, cash charts

- Scenario testing for funding

How many beds does a hostel need to be profitable?

A Hostel needs enough beds to cover lease, staffing, and reserves; in this model, that means starting with 90 rentable units and reaching break-even in Month 5 at 65% Year 1 occupancy. For the operating metric behind that threshold, see What Is The Most Important Indicator Of Success For Your Hostel Business?, because bed count only works when occupancy and ADR carry fixed costs.

Profitability threshold

- Start with 90 rentable units

- Reach break-even in Month 5

- Assume 65% Year 1 occupancy

- Track ADR and room mix tightly

Cash pressure

- Cover $246k/month fixed expenses

- Add $373k Year 1 wages

- Delay owner pay until cash clears

- Test $70k salary against EBITDA

What hostel operating costs reduce owner income most?

The biggest hit to Hostel owner income is payroll and property cost: Year 1 wages are $373k, and fixed expenses total $2,952k per year. For the startup-cost context, see What Is The Estimated Cost To Open And Launch Your Hostel Business? Direct and variable costs start at 16% and fall to 13.3%, so small margin changes matter when Year 1 EBITDA is only $18k.

Biggest cost drains

- $373k Year 1 wages

- $180k lease cost

- $216k cleaning cost

- $144k maintenance cost

Why margins stay thin

- $2,952k fixed expenses yearly

- $96k systems spend

- 16% to 13.3% cost range

- $18k Year 1 EBITDA

How much revenue can a hostel make?

Hostel revenue can be about $817k in Year 1 and $130M in Year 5, but that is revenue, not profit or owner take-home. The model also shows $25 to $41 dorm rates, $90 to $126 private family rates, and ancillary revenue rising from $111k to $212k. Here’s the quick math: Year 1 uses 16% direct and variable costs with $18k EBITDA, while Year 5 assumes 87% occupancy and 133% direct and variable costs.

Revenue drivers

- $817k Year 1 revenue

- $130M Year 5 revenue

- $25-$41 dorm rates

- $90-$126 private rates

Cost and mix

- 16% direct cost load

- 87% occupancy in Year 5

- 133% direct and variable costs

- $111k to $212k ancillary revenue

Want to see the six hostel income drivers?

1

65%-87%Occupancy

This is the biggest swing: fuller beds lift room revenue and owner cash after fixed costs and reserves.

2

$373K-$482KStaffing

Wages rise as the hostels scales, so labor control protects margin and take-home profit.

3

$295KLease Load

The lease and other fixed overheads sit near $295K a year, so they set the break-even floor each month.

4

$25-$126Bed Rate

Pricing across dorms and private rooms sets revenue per night, and small gains flow straight to cash.

5

90-94 BedsBed Capacity

More rentable beds raise the sales ceiling, but only if demand stays strong enough to fill them.

6

$11K-$21KAncillary

Food, tours, laundry, coworking, and merch add smaller but high-margin income after room costs.

Hostel Core Six Income Drivers

Bed capacity

Bed Capacity

Capacity sets the revenue ceiling, not profit. This model starts with 48 eight-bed dorm units, 30 six-bed dorm units, 4 private twins, 6 private doubles, and 2 private family rooms, for 90 rentable units in Year 1 and 94 by Year 4. More beds only help if demand, layout, licensing, bathrooms, and cleaning can support occupancy.

Here’s the quick math: room revenue comes from available units × occupied nights × rate. If extra units sit empty, or if poor reviews cut bookings, the owner still carries the added cleaning, utility, and wear load. So capacity lifts income only when the hostel can keep units sellable and guest experience strong.

Track Sellable Beds

Measure sellable beds, not just total beds. Track out-of-order rooms, cleaning turnaround, bathroom pressure, and review scores every week. If a unit cannot stay open, clean, and well rated, it is not real capacity and should not be counted as income-producing space.

- Check licensing before adding beds.

- Track downtime after every turnover.

- Watch reviews after layout changes.

- Forecast occupied nights, not bed count.

1

Occupancy rate

Occupancy Rate

Occupancy is the share of beds sold, and it is the main utilization lever here. The model moves from 65% in Year 1 to 87% in Year 5, so each point of fill turns empty beds into revenue without changing the lease. That matters because Year 1 EBITDA is only $18k; if occupancy slips, owner pay gets squeezed fast.

Fixed property and payroll costs still run when beds sit empty, so low occupancy hits cash flow first and profit second. Track occupied bed-nights, seasonal lows, and weekday versus weekend fill. Here’s the quick math: more occupied nights lift room revenue, but if the hostel can’t cover fixed costs plus wages, the owner’s draw stays thin.

Test the low case first

Before adding front desk or housekeeping staff, model a low-case occupancy below plan. If seasonal softness pulls occupancy down, payroll becomes a fixed drag and the small Year 1 EBITDA can disappear. Build the forecast from bed capacity, occupancy rate, ADR (average daily rate), payroll, and fixed costs so you can see what is left for the owner.

- Track occupancy weekly by room type.

- Separate weekday and weekend fill.

- Stress-test winter and shoulder seasons.

- Hold hiring until demand proves out.

- Watch EBITDA after payroll each month.

If cleaning hours or front desk coverage rise before demand does, margin gets thinner. Tie staffing to occupancy bands, not hope, so the business can keep more cash for debt service, reserves, and owner pay.

2

Average bed rate

Average bed rate

Average bed rate is the average nightly price you collect per sold dorm or private room night. It drives room revenue fast: Year 1 dorms run at $25 to $28 midweek and $35 to $38 on weekends, while private rooms range from $60 to $110. If pricing holds and occupancy stays strong, owner cash flow improves; if rates rise too far, occupancy can drop and erase the gain.

Here’s the quick math: room revenue = occupied room-nights × average bed rate. Private rooms matter because they lift the average more than dorm beds, but only if reviews, amenities, location, and local lodging demand support the price. Year 5 private room rates of $72 to $126 show upside, but the risk is clear: pushing price too hard can cut bookings and weaken profit draw.

Track rate by room type

Measure realized rate by weekday, weekend, dorm, and private room. Compare that to occupancy, because a higher rate only helps if room nights still sell. Use simple checks: booked nights, average collected price, review score, and pickup pace by date. That tells you whether a rate change is adding cash or just slowing demand.

Test price in small steps, not big jumps. Raise rates only when demand is firm, then watch whether occupancy stays within plan. If private rooms hold at $60 to $110 in Year 1 and move toward $72 to $126 in Year 5, the extra revenue can help pay fixed costs and staffing. If booking pace slips, cut back fast.

- Track booked nights by room type.

- Watch weekday versus weekend pricing.

- Compare rate changes to occupancy.

- Check reviews after each increase.

3

Ancillary revenue

Ancillary revenue

Ancillary revenue covers F&B sales, events and tours, laundry and luggage, co-working passes, and merchandise. It lifts profit per guest only when direct costs stay tight. In this model, ancillary revenue rises from $111k in Year 1 to $212k in Year 5, up 91%. The real test is net contribution, not gross sales.

Here’s the quick math: if food and tour costs rise with sales, top-line revenue can overstate cash available for owner pay. Keep extras separate from core dorm bed revenue, so you can see whether higher bar sales or more tours actually improve EBITDA and free cash flow. If service slips, add-on sales can fall even when occupancy holds.

Measure add-on margin

Track each add-on against occupied guests, not total beds. Measure revenue per guest, event ticket count, laundry and luggage use, co-working pass sales, and merchandise margin. Then subtract direct costs like F&B supplies and tour operator fees. A small margin lift can matter more to owner pay than a bigger but weaker sales push.

Use separate P&Ls for bar, events, tours, and services, and forecast them monthly because guest mix changes by season and weekday. If an add-on depends on outside vendors, lock fee splits before launch. Keep core bed revenue clean, so you can see whether extras are adding cash or just adding work.

- Occupied guests per month

- Average spend per guest

- Event and tour ticket volume

- Direct cost per sale

- Staff hours by department

4

Staffing model

Staffing model

Labor is a cash-flow tradeoff. Year 1 payroll includes a $70k general manager, $70k front desk, $60k housekeeping, $45k F&B manager, $56k F&B staff, $40k community manager, and $32k security, for $373k in wages. By Year 5, wages rise to $482k. If the owner runs some of these roles, cash available can improve, but only if the owner truly covers the work.

Understaffing is not a free win. In a hostel, missing labor shows up fast in cleaning, safety, guest reviews, and repeat bookings. That can hit occupancy and ancillary sales, so payroll savings can disappear in lower revenue. Here’s the quick math: the staffing plan only helps owner income if each saved dollar of p ayroll is worth more than the lost revenue from worse guest experience.

Track labor against guest load

Use labor inputs that match demand: occupied beds, check-ins, room turns, F&B covers, events, and night coverage. Watch payroll as a share of revenue, labor hours per occupied bed, and housekeeping time per turnover. If those ratios climb while reviews fall, the model is too thin and owner pay will suffer.

- Staff to occupancy, not hope.

- Protect cleaning and night security.

- Test owner coverage before hiring.

- Separate F&B labor from room labor.

Owner-operated can lift cash flow, but only if the owner can safely replace paid labor with real work. If the owner takes on front desk, community, or manager tasks, model that time cost honestly. If not, the hostel may save payroll on paper and lose repeat bookings in practice.

5

Property and fixed costs

Fixed cost floor

Annual fixed costs are $2,952k, or about $246k per month. That is the break-even floor before the owner sees pay, because the hostel must first cover lease, utilities base, property taxes, cleaning, maintenance, insurance, systems, and internet. These costs do not fall much when rooms sit empty, so weak occupancy hits take-home income fast.

Here’s the quick math: $180k lease, $30k utilities base, $24k property taxes, $216k cleaning, $144k maintenance, $12k insurance, $96k systems, and $36k internet. If revenue does not clear this floor, plus payroll, variable costs, reserves, and debt service, owner draw stays at zero.

Track the fixed load

Build the model from the actual lease, city taxes, utility base charge, cleaning plan, maintenance contract, insurance, software, and internet bill. Track each line monthly and compare it to room revenue and occupancy. One clean rule: if fixed costs rise, owner pay needs more bed nights.

- Test lease terms before signing.

- Stress occupancy at low season.

- Watch cleaning and maintenance drift.

- Separate fixed and variable costs.

Cutting price too hard can hurt occupancy, but cutting fixed costs after signing a lease is much harder. So the real control point is location choice, lease structure, and cost discipline before opening. If the monthly fixed base stays near $246k, the hostel needs steady revenue just to protect owner income.

6

Compare low, base, and high hostel owner income scenarios

Owner income scenarios

Owner income moves with occupancy, ADR, direct bookings, and payroll control. The model starts at $18k EBITDA in Year 1 and climbs to $349k by Year 5, but cash stays tight early.

| Scenario | Low CaseCash tight | Base CaseOn plan | High CaseUpside |

|---|---|---|---|

| Launch model | Owner income stays thin at launch and distributions wait for cash to recover. | Owner income follows the plan as EBITDA ramps year by year. | Owner income rises faster when the hostel beats the plan on demand and payroll. |

| Typical setup | Year 1 EBITDA is only $18k, and weaker occupancy or ADR leaves little room after the fixed lease, payroll, and OTA fees. | Occupancy rises from 65% to 87%, and EBITDA moves from $18k in Year 1 to $82k, $145k, $261k, and $349k. | Occupancy, ADR, direct bookings, and staffing efficiency all improve, so EBITDA can outrun the base path and cash builds faster. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Deferred owner drawsDraws delayed | $18k to $349k EBITDAModeled path | Above modeled EBITDA pathUpside case |

| Best fit | Use this to stress-test a slow start, weak demand, and slower cash recovery. | Use this as the planning baseline for the model's assumed operating case. | Use this to test what strong demand and tighter labor control could do to owner income. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or actual distributions; the model breaks even in Month 5, hits a $725k minimum cash point in Month 15, and shows a 48-month payback.

Related Products

- Hostel Porter's Five Forces Analysis

- Hostel BCG Matrix

- Hostel Business Model Canvas

- Tracking 7 Critical Financial KPIs for Your Hostel Business

- Hostel Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Hostel Profitability and Boost Margins

- How Much Does It Cost To Run A Hostel Each Month?

- How Much Does It Cost To Start A 90-Bed Hostel In The US?

- Hostel Financial Model Template in Excel

- How To Open A Hostel In 4–9 Months With A Guest-Ready Launch Plan

- How to Write a Profitable Hostel Business Plan in 7 Steps

- Hostel Marketing Mix

- Hostel Marketing Plan

- Hostel Business Proposal

- Hostel PESTEL Analysis

- Hostel Pitch Deck Example Editable PPTX

- Hostel Business SWOT Analysis

- Hostel Value Proposition Canvas

Frequently Asked Questions

In this model, owner income is best viewed through EBITDA first EBITDA is $18k in Year 1, $145k in Year 3, and $349k in Year 5 before taxes, debt service, reserves, and distributions Actual take-home can be lower if cash is kept for maintenance, seasonality, loan payments, or growth