Owner income$469k-$2.186M

Owner income$469k-$2.186MHow Much Does A Hot Dog Restaurant Owner Make? $469k Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$469k-$2.186M  Net margin28.5%-56.2%

Net margin28.5%-56.2% Revenue for target pay$1.64M-$3.89M

Revenue for target pay$1.64M-$3.89M Business difficultyHard

Business difficultyHard

A hot dog restaurant owner can make money only after revenue covers food, beverage, labor, rent, fixed overhead, reserves, debt, and taxes In the researched base model, Year 1 revenue is about $164M and EBITDA is $469k, or a 285% operating margin before taxes, debt service, and owner distributions By Year 5, revenue reaches $389M and EBITDA reaches $219M under the supplied assumptions That is cash flow potential, not a guaranteed salary

Owner income$469k-$2.186MNet margin28.5%-56.2%Revenue for target pay$1.64M-$3.89MBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

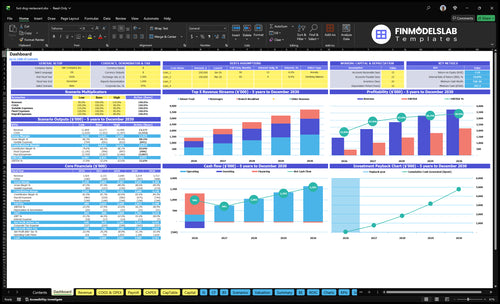

How do you check owner income in the Hot Dog Restaurant model?

This screenshot shows owner-income outputs in the Hot Dog Restaurant Financial Model Template. Test scenarios.

Owner-income model highlights

- Dashboard, sales, staffing

- Rent, startup, cash flow

- Revenue $164M, EBITDA $469k

- Minimum cash $767k

- Breakeven Month 3

- Payback 12 months

- Scenario testing, not promise

How much can a hot dog restaurant owner make per year?

A Hot Dog Restaurant owner can make an assumption-based range, not one fixed salary: the supplied model shows $469k EBITDA in Year 1 rising to $2.186M in Year 5, with revenue growing from $1.64M to $3.89M; for KPI context, see What Is The Most Important Measure Of Success For Hot Dog Restaurant?. Owner take-home is lower than EBITDA after taxes, reserves, debt service, and payroll choices.

Owner earnings range

- Year 1 EBITDA: $469k

- Year 5 EBITDA: $2.186M

- Take-home depends on tax structure

- Debt payments reduce cash available

Main profit levers

- Revenue: $1.64M to $3.89M

- Higher sales volume lifts EBITDA

- Higher beverage mix expands margin

- $80k general manager already included

How does owner-operated income compare with manager-run profit?

For a Hot Dog Restaurant, owner-operated income can be higher than manager-run profit because the manager-run setup carries full payroll, including a $80k general manager and a $70k head chef, inside $420k of Year 1 payroll. If the owner replaces the manager, cash flow can rise by up to $80k before taxes. The catch is simple: that lift comes from the owner’s unpaid time, so distributions fall unless sales volume supports the added payroll.

Manager-run payroll load

- $420k Year 1 payroll total

- $80k general manager cost

- $70k head chef cost

- Profit drops with full payroll

Owner-operated cash flow tradeoff

- Cash flow can rise up to $80k

- Owner labor is not free

- Distributions fall if payroll rises

- Sales must cover added labor

How much revenue is needed to pay a hot dog restaurant owner?

There isn’t one fixed revenue number; owner pay depends on the pay target, average ticket, days open, margin, fixed costs, and cash reserves. In the Year 1 model for a Hot Dog Restaurant, 390 weekly covers with $65 midweek AOV and $90 weekend AOV point to $316k weekly revenue and about $469k EBITDA before taxes and debt. Selling hot dogs alone is not enough, because combos, drinks, sides, and brunch or dinner mix all change the average ticket. The quick formula is: target owner pay ÷ distributable margin after fixed costs.

Revenue drivers

- 390 weekly covers

- $65 midweek AOV

- $90 weekend AOV

- Combos lift average ticket

Pay math

- Start with target owner pay

- Subtract fixed expenses first

- Use distributable margin next

- Hold a reserve for slow weeks

Want to see what changes owner income most?

1

390-750/wkOrder Volume

Year 1 starts at 390 weekly covers and Year 5 reaches 750, so traffic growth is the cleanest way to lift owner income.

2

$65-$110Average Ticket

Average ticket runs from $65 midweek to $110 on weekends, and every upsell lifts cash after fixed costs.

3

$420K-$573KLabor Model

Payroll rises from about $420K to $573K as staffing grows, so sales have to stay ahead of labor.

4

6%-7%Food Margin

Food cost moves from 7% to 6%, which keeps more gross profit on each sale and protects take-home.

5

$12K/moRent Load

Rent stays at $12K a month, so the site has to carry that fixed load before the owner sees strong cash flow.

6

35%-40%Add-ons

Beverage mix grows from 35% to 40% of sales, and later models should add packaging and delivery fee inputs.

Hot Dog Restaurant Core Six Income Drivers

Daily Order Volume

Daily Order Volume

Daily order volume is the first cap on income. In Year 1, the model ranges from 25 orders on Monday to 100 orders on Saturday; by Year 5, it moves to 60 and 180. Weekly covers rise from 390 to 750. If weekdays stay soft, rent and labor get spread over fewer checks, so the break-even burden climbs fast.

Here’s the quick math: revenue is orders × average ticket, so more traffic matters before margin can help. One clean line: a busy Saturday can hide a weak Monday, but cash still has to cover the week.

Track Throughput, Not Just Traffic

Build the forecast by daypart, not by one weekly average. Track orders per hour, lunch rush volume, weekend demand, location, hours, and service speed so the kitchen and front counter can keep up. If open hours or staffing can’t support the peak, the store loses orders it already attracted.

- Split Monday through Saturday.

- Measure lunch and dinner separately.

- Watch order time by shift.

- Test staffing against peak volume.

1

Average Ticket And Combo Sales

Average Ticket And Combo Sales

Average ticket, or average order value (AOV), is what each guest spends per visit. In Year 1, the model uses $65 midweek and $90 on weekends; by Year 5, that rises to $85 and $110. That lifts revenue without needing the same jump in customer count, so it can improve owner pay if food cost, labor, and promos stay in line.

Here’s the quick math: the model says each extra $1 across 390 Year 1 weekly covers adds about $203k in annual revenue. Combo sales, drinks, fries, specialty toppings, and the brunch or dinner mix all push that number. The catch is simple: a higher check only helps if the added items carry solid margin, not discount-driven volume.

Raise the Check Without Hurting Margin

Track AOV by daypart, not just by day. Split midweek and weekend checks, then measure attach rate for drinks, fries, and toppings. If a combo lifts ticket but adds labor or waste, it can hurt cash flow instead of helping it. The goal is more revenue per cover, with the same or better gross margin.

- Track AOV by midweek and weekend.

- Measure combo attach rate weekly.

- Watch margin on add-on items.

- Test brunch and dinner mix.

- Price toppings to protect profit.

Use simple menu tests: one premium combo, one beverage bundle, and one topping upsell. If the check rises but food cost, packaging, or labor also climbs too fast, owner draw will not improve much. What matters is revenue per guest after variable cost, not ticket size alone.

2

Food, Beverage, Packaging, And Waste Margin

Food, Beverage, Packaging, And Waste Margin

This driver is the gap between sales and what it costs to serve each hot dog, drink, and side. Food cost moves from 7% to 6%, and beverage cost from 6% to 5%, while beverage mix rises from 35% of sales in Year 1 to 40% in Year 5. If portions drift, toppings get too complex, or waste rises, owner take-home drops fast.

Packaging is a separate cost per order, so it needs its own line in the model. Here’s the quick math: even small leaks in ingredient yield, drink pours, and thrown-away product hit gross margin first, then cash flow, then the owner’s draw. The model also shows payment processing falling from 25% to 2%, so every saved point matters more when fixed costs stay high.

Control Cost Per Order

Track food cost per order, beverage cost, packaging per check, and waste by shift. Build recipes with exact portions, limit topping sprawl, and count comps and spills daily. If a menu item can’t hold its margin at the target mix, reprice it or simplify it.

Use the mix shift from 35% to 40% beverages to test drink attach rate, but only if the beverage margin stays intact. What this estimate hides is simple: the owner only keeps what survives waste, packaging, and prep mistakes, so small controls protect profit better than a big sales day.

3

Labor Model And Owner Shifts

Labor Model

Labor decides whether profit turns into owner cash. Year 1 payroll is $420k, and the model rises to $5,725k in Year 5. That covers one $80k general manager, one $70k head chef, plus servers, bartenders, kitchen staff, and host-cashier coverage. If sales don’t grow fast enough, payroll eats the margin before the owner can draw cash.

Owner-run income can improve cash flow if the owner replaces paid management, especially the $150k tied to the GM and head chef roles. But the tradeoff is control: the owner must handle hiring, training, labor scheduling, and quality checks. Manager-run profit is cleaner for scale, but only works if volume is high enough to carry the fixed wage load.

Control Labor Hours

Track payroll as a share of sales, plus overtime, shift coverage, and owner hours. The key inputs are sales by daypart, hourly wages, and how many paid management hours you keep on the schedule. If weekday traffic is light, trim labor there first and protect lunch and weekend peaks.

- Compare owner-run and manager-run weeks.

- Watch payroll before overtime starts.

- Match staffing to actual covers.

Test the owner shift plan against service speed and errors. If the owner can cover GM and chef duties without hurting guest flow, the business keeps more cash. If not, the saved salary can disappear into slower service, more mistakes, and weaker repeat visits.

4

Rent, Location, And Occupancy Cost

Rent and Occupancy Cost

For a fast-casual hot dog shop, $12k monthly rent is a fixed bet on traffic. It only works if weekday covers and average ticket stay high enough to spread that cost. In this model, rent is $144k a year and about 88% of Year 1 revenue, so weak volume can wipe out owner pay fast.

Total fixed expenses are $166k per month, or $1,992k per year. By Year 5, rent falls to about 37% of revenue, so scale can help. Still, if the site does not produce enough lunch and weekend demand, the lease turns into a cash drain instead of a profit base.

Track weekday demand first

Measure weekday covers, weekend covers, average ticket, and fixed expenses before you sign or renew. Here’s the quick math: rent is fixed, so every slow Monday costs the same. If the site cannot carry the lease on weak days, busy weekends will not save owner income.

- Track covers by day

- Compare rent to revenue

- Watch cash after fixed costs

Use those checks to test location quality. A better corner only helps if it brings enough steady weekday demand to pay the rent and still leave profit for the owner draw. If rent rises faster than sales, take-home income drops even when the dining room looks full.

5

Catering, Delivery, Events, And Seasonality

Off-Premise Sales Margin

Catering, events, late-night takeout, and seasonal foot traffic can raise revenue, but they need separate margin lines. For delivery, model fees, packaging, labor, and payment processing as real costs; the source model uses 25% payment processing in Year 1 and 35% marketing promotions, so gross sales can shrink fast before owner pay.

The key test is not sales volume, it’s contribution after channel costs. If an off-premise order needs extra prep or a separate shift, the margin can disappear. A busy Saturday catering run that looks strong on paper can still lower take-home if labor, promos, and delivery fees eat the spread.

Track Channel Profit by Order Type

Split sales into in-store, takeout, delivery, catering, and events. Track average check, fee rate, packaging cost, labor minutes, and promo spend per channel. That tells you which orders actually help profit and which just add work.

Price off-premise orders so they cover their own cost stack. If a channel needs extra shifts or heavy promos to run, cap volume or raise prices until contribution stays positive. Otherwise, the owner is funding busy sales with thinner cash.

- Track margin by channel weekly

- Separate delivery fees from sales

- Log promo spend by campaign

- Count labor minutes per order

6

Compare low, base, and strong owner income scenarios without treating them as predictions

Owner income scenarios

Low volume tracks Year 1 ramp, base uses Year 3 scale, and high reflects Year 5 volume. Owner take-home shifts with covers, payroll, and rent, then gets trimmed by reserves, taxes, debt, and reinvestment.

| Scenario | Low CaseRamp risk | Base CaseScalable base | High CaseVolume upside |

|---|---|---|---|

| Launch model | This is the low ramp path, where Year 1 volume and early overhead still दबown owner income. | This is the modeled middle path, where Year 3 traffic supports steadier owner income. | This is the stronger earnings path, where Year 5 volume lifts owner income the most. |

| Typical setup | It assumes about 390 weekly covers, about $1,643,200 revenue, $469,000 EBITDA, $420,000 payroll, and $144,000 annual rent. | It assumes about 600 weekly covers, about $2,821,000 revenue, $1,440,000 EBITDA, $475,000 payroll, and $144,000 annual rent. | It assumes about 750 weekly covers, about $3,887,000 revenue, $2,186,000 EBITDA, $572,500 payroll, and $144,000 annual rent. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $469,000Year 1 ramp | $1,440,000Year 3 base | $2,186,000Year 5 scale |

| Best fit | Best if you want a stress test for a slow opening and tighter cash. | Best for a steady plan built around the model's middle case. | Best if you expect strong volume and can keep labor and waste in check. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution forecasts.

Related Products

- Hot Dog Restaurant Porter's Five Forces Analysis

- Hot Dog Restaurant BCG Matrix

- Hot Dog Restaurant Business Model Canvas

- 7 Critical KPIs to Drive Profitability in Your Hot Dog Restaurant

- Hot Dog Restaurant Business Plan Template in Pre-Written Word

- How to Increase Hot Dog Restaurant Profitability in 7 Practical Strategies

- How to Calculate Monthly Running Costs for a Hot Dog Restaurant

- Hot Dog Restaurant Startup Costs: Plan For $767K Funding

- Hot Dog Restaurant Financial Model Template in Excel

- How To Open A Hot Dog Restaurant In 3 To 9 Months With A Launch Plan

- How to Write a Business Plan for a Hot Dog Restaurant

- Hot Dog Restaurant Marketing Mix

- Hot Dog Restaurant Marketing Plan

- Hot Dog Restaurant Business Proposal

- Hot Dog Restaurant PESTEL Analysis

- Hot Dog Restaurant Pitch Deck Example Editable PPTX

- Hot Dog Restaurant Business SWOT Analysis

- Hot Dog Restaurant Value Proposition Canvas

Frequently Asked Questions

The supplied model shows $469k of Year 1 EBITDA on about $164M of revenue EBITDA is operating cash flow before taxes, interest, depreciation, amortization, debt service, and owner distributions By Year 5, EBITDA reaches $2186M on $389M of revenue, but those are planning outputs, not guaranteed owner pay