Time to Open2 monthsLaunch runway

Time to Open2 monthsLaunch runwayHow to Start a House Flipping Business With a 60–180 Day Launch Plan

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Time to Open2 monthsLaunch runway  Launch Sequence7 stagesEntity first

Launch Sequence7 stagesEntity first Key BottleneckDeal gapPricing before buy

Key BottleneckDeal gapPricing before buy First Revenue StepResale closingSale funds in

First Revenue StepResale closingSale funds in

To start a house flipping business, form the entity, open banking, line up financing, build a contractor and inspector bench, source deals, underwrite repairs, close on a viable property, renovate, list, and resell The researched planning assumptions show a first acquisition in Month 2, construction starting in Month 4, and first resale revenue in Month 15 A practical launch often takes 60–180 days before the first acquisition, depending on financing, deal flow, contractor availability, permitting, and local closing timelines The hard part isn’t opening the entity it’s buying at the right basis with repair pricing you can trust

Time to Open2 monthsLaunch runwayLaunch Sequence7 stagesEntity firstKey BottleneckDeal gapPricing before buyFirst Revenue StepResale closingSale funds inLaunch timeline

Short web summary of the launch plan; the XLSX export includes the detailed Gantt chart.

Launch scheduleMonth 1Month 2Month 3Month 4Month 5Month 6Month 7Month 8Month 9Month 10Month 11Month 12Month 13Month 14Month 15Month 16

Capital setup

- Entity setup

- Proof of funds

- Funding model

- Budget approval

Deal sourcing

- Lead list build

- Broker outreach

- Screen deal returns

- Offer package

Due diligence

- Title review

- Inspection scope

- Contractor bids

- Close first buy

- Later close prep

Construction

- Permit submission

- Demo start

- Rough-in work

- Finish work

- Punch list

Sales and exit

- Price analysis

- Listing prep

- Showings launch

- Offer review

- Sale close

Operations

- Chart accounts

- Cash forecast

- Monthly reporting

- Vendor roster

- Project lead hire

Can House Flipper survive the first flip?

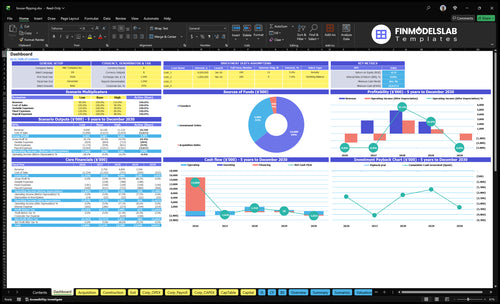

Before launch, the House Flipper Financial Model Template maps 60-month runway, acquisition, rehab, cash runway, and break-even—open it.

Financial model highlights

- Month 2, $450,000 buy

- $120,000 rehab, 7 months

- Month 15 resale timing

- Revenue ramp, active projects

- Overhead, staffing, fees

- Breakeven path, sensitivity

How long does it take to start flipping houses?

For a House Flipper, a practical pre-acquisition launch window is 60–180 days, with the first acquisition often in Month 2, construction starting around Month 4, and the first resale showing up around Month 15. Financing approval, deal flow, due diligence, closing, permits, contractor scheduling, rehab scope, inspections, listing time, and buyer financing all affect the clock. If bids or permits slip, the holding period gets longer and cash pressure rises, so don’t promise a guaranteed launch date.

What speeds launch

- 60–180 days is the launch range.

- Month 2 can close first deal.

- Month 4 can start rehab.

- Fast approval cuts idle cash burn.

What slows it down

- Permits can push the start date back.

- Contractor delays extend holding costs.

- Buyer financing can slow the resale.

- Rehab slips raise cash pressure fast.

How does first revenue from house flipping happen?

For House Flipper, the first revenue shows up at resale closing, not at purchase or when the renovation is done, and the first resale is modeled in Month 15; for startup cost context, see How Much Does It Cost To Start House Flipper Business? The path is simple: buy at the right basis, finish marketable repairs, price with comps, list through an agent or buyer channel, work through inspection issues, and close the sale. Selling costs and commissions are modeled at 65% in Year 2, 60% in Year 3, 55% in Year 4, and 50% in Year 5, but no resale price is provided, so profit is not calculated here.

Revenue timing

- Cash comes at closing

- Month 15 is the first resale

- Purchase does not create revenue

- Renovation finish does not create revenue

Deal sequence

- Buy at the right basis

- Complete marketable repairs

- Price with comps

- Close after inspection talks

What mistakes hurt beginner house flippers at launch?

Beginner House Flipper mistakes at launch are usually the same: overpaying, trusting loose repair estimates, and closing before contractor capacity is confirmed. On a first deal with a $450,000 purchase and $120,000 construction budget, small underwriting misses can turn into big cash gaps, especially with $15,100 in monthly fixed overhead before Month 13 and core payroll starting in Month 1. The fix is simple: underwrite the price, repairs, permits, and cash buffer before you sign.

Deal math errors

- Don’t overpay on day one

- Use tight resale comps

- Stress-test repair estimates

- Check permit needs early

Cash flow traps

- Confirm contractor capacity first

- Count holding costs from launch

- Plan for $15,100 fixed overhead

- Keep a cash buffer ready

Confirm whether the house flipping business is ready to launch

Launch readiness checklist

Use this go-live approval checklist to confirm the business is ready before opening and buying its first property.

Entity and bank

- Entity formed and bank openCritical

You need a legal entity and a business account before deposits, draws, and sale proceeds move.

- Ownership records are filedHigh

Clear ownership records reduce bank, tax, and signing delays when a deal closes.

- Signing authority is setHigh

Defined signers keep purchases, draws, and closing wires from stalling.

Rules and cover

- State, county, city rules mappedCritical

Zoning, permit, and disclosure rules must be clear before any property work starts.

- Required permits are confirmedCritical

Permit gaps can stop work and push sale timing past plan.

- Property insurance is boundCritical

The model assumes $900 per month in business insurance, so coverage must start on day one.

Capital and systems

- Funding sources are lined upCritical

You need committed funding before you tie cash to earnest money or rehab spend.

- Proof of funds is readyCritical

Sellers and brokers move faster when they can see available cash.

- Deal tracking system is liveHigh

You need one system to track leads, bids, budget, and sale status.

Sourcing and bids

- Deal source channels are activeHigh

Active sourcing keeps the pipeline full enough to reach target volume.

- Comparable sales are currentCritical

Current comps protect the resale price and keep bids grounded in the market.

- Offer pricing is stress-testedCritical

The deal must work after purchase cost, rehab budget, fees, and delay risk.

Rehab delivery

- Crew roles are assignedHigh

Clear owners cut rework when multiple trades touch the same property.

- Contractor bids are signedCritical

Signed bids lock scope and help avoid surprise cost creep.

- Change-order process is setHigh

A change process keeps repairs, permits, and budget shifts under control.

Exit and close

- Listing package is readyHigh

A ready listing speeds the first sale and keeps days on market down.

- Closing funds flow is testedCritical

The payment path must work before you rely on sale proceeds.

- Go-live signoff is completeCritical

Final signoff confirms the team can buy, rehab, and resell without open gaps.

What really drives a house flipping launch?

1Acquisition Pipeline

Month 2No deal means no launch, so repeatable sourcing must be ready before Month 2.

2Capital Readiness

$320K-$750KCapital must cover the owned buys from $320K to $750K plus rehab draws.

3Contractor Capacity

5-12 moA ready crew keeps 5-12 month builds moving and stops scope gaps from pushing resale back.

4Due Diligence Discipline

Go/no-goGo/no-go checks stop rough repair guesses from getting locked in as final pricing.

5Renovation Execution

Month 4The first build starts in Month 4, so tight project control is what keeps resale on schedule.

6Resale And Exit Strategy

Month 15First cash comes at Month 15, and pricing discipline decides how much value survives closing.

Acquisition Pipeline

Acquisition Pipeline

No viable property means no launch. The business can’t open on time, or operate from day one, until it has a repeatable way to find and win deals through the multiple listing service (MLS), wholesalers, agents, auctions, direct mail, foreclosure leads, and estate sales.

The buy box has to be set before any offer goes out. Every deal should be underwritten with maximum allowable offer (MAO) against after repair value (ARV), repair scope, fees, and hold time. The model assumes the first acquisition in Month 2 and nine more acquisition events through Month 23.

Repeatable Deal Flow

Before opening, test whether sourcing really works. That means a live list of leads, clear buy-box rules, and a fast check on repair and resale assumptions before earnest money goes hard. If the deal fails the numbers, walk away early. That keeps cash from getting tied up in weak contracts.

Readiness shows up when the founder can replace one deal with the next without pause. Use a simple screen: ARV, repair scope, fees, and hold time must all fit the MAO. If sourcing is slow or sloppy, the launch stalls because there’s nothing to renovate, list, or sell.

- Define the buy box first.

- Underwrite every deal the same way.

- Check repairs before earnest money.

- Track lead sources by response time.

- Reject deals that miss MAO.

1

Capital Readiness

Capital Ready Before Offers

If capital is not lined up before offers, the launch slows fast. A house flipper has to close on time, fund rehab draws, and carry interest without waiting on new money, or the deal can stall before day one. With owned purchases modeled at $450,000, $380,000, $620,000, $510,000, $320,000, and $750,000, each offer needs a clear funding path, not a hope-and-see plan.

Here’s the quick math: acquisition and deal sourcing fees are modeled at 15% in Year 1 and 18% in Year 2. That is $67,500 on a $450,000 buy and $112,500 on a $750,000 buy, before rehab carry and draw timing. The real bottleneck is slow closing or underfunded rehab draws, because both can delay construction starts and push the first resale back.

Line Up Funds, Then Offer

Before the first contract, verify lender relationships, private money, proof of funds, down payment capacity, rehab draw rules, interest carry, and backup capital. If any one of those is missing, the closing timeline can slip and the job site sits idle.

- Confirm proof of funds first.

- Match draw timing to contractor needs.

- Reserve cash for carry costs.

- Test backup funding before earnest money.

Use one funding file per deal with lender terms, draw schedule, and cash reserve notes. That way, when a property comes up, you can move fast without starving the rehab budget mid-project.

2

Contractor Capacity

Contractor Capacity

Contractor capacity decides whether the first flip starts on time or sits idle after closing. This business needs a crew that can begin work the day title transfers and hold the schedule through a 5 to 12 month build. If the team is not ready, the property can close cleanly but still miss the resale window, which ties up cash and delays day-one operations.

The first rehab budget is $120,000, and later jobs run from $85,000 to $250,000. That means the contractor has to price scope clearly, cover labor, and pass quality checks without surprise adds. The real risk is not just a bad bid; it is a crew that starts late, underprices the work, or keeps changing the plan while the resale clock keeps running.

Vet the crew before closing

Lock contractor capacity before you go hard on a deal. Get a scope walkthrough, written repair estimate, labor availability, insurance, references, milestone schedule, and change-order rules. One clean test matters: can the crew start when the property closes, hit each milestone, and finish without pushing the resale date?

- Confirm start date at closing.

- Match estimate to scope walkthrough.

- Verify insurance and references.

- Set milestone dates in writing.

- Define change-order approval rules.

If any of those pieces are missing, the launch is not ready. A crew that cannot staff the job on day one forces delays, extra carrying costs, and weaker buyer experience later, especially when the project size can swing from $85,000 to $250,000.

3

Due Diligence Discipline

Due Diligence Discipline

If the numbers are loose, the flip is already at risk before closing. Due diligence checks comps, after repair value (ARV), inspection findings, permit needs, structural issues, title concerns, neighborhood demand, and contingency assumptions. On the first model deal, that matters a lot because the file starts with a $450,000 purchase cost and a $120,000 construction budget.

ARV means the expected resale value after planned repairs. If that value is built on weak comps or missed defects, the deal can lock in a bad basis and stall the rehab before day one. Rough repair numbers are not final pricing, so the underwriting has to be tight before earnest money goes hard.

Pre-Close Go/No-Go Rules

Set a hard go/no-go check before closing. Verify the comp set, confirm ARV, review the inspection, look for title and permit issues, and add a real contingency line before you approve the buy. One clean rule: if the repair scope is still a guess, do not close yet.

- Match ARV to closed comps.

- Flag structural risk early.

- Check title before earnest money.

- Confirm permit needs now.

- Document contingency assumptions.

That keeps the project from stalling after closing, when cash and contractor time are already committed. If due diligence is thin, you can still buy the property, but you may not be able to start rehab on time or protect the resale margin you need.

4

Renovation Execution

Renovation Execution

For a fix-and-flip, the launch only works if the rehab moves on schedule. A 7-month build that starts in Month 4 leaves little room for permit delays, missed inspections, or slow material orders, and longer jobs at 8, 9, or 12 months tie up cash even more. If trades sit idle, resale slips and buyer-facing quality drops.

This driver covers scope lock, permit confirmation, trade sequencing, draw inspections, quality checks, and change-order approval. One bad handoff can turn a clean remodel into a late close, more interest carry, and a harder buyer inspection. The main risk is not the work itself; it is the gap between planned work and actual field execution.

Lock the build plan before cash goes out

Before work starts, confirm permits, order long-lead materials, and map the trade order so each crew knows when to show up and what they need. Track lender draws and inspect each milestone before paying the next invoice. That keeps the rehab moving and protects working capital.

- Freeze scope before demo starts

- Confirm permit status and inspection dates

- Order materials with lead times

- Set change-order approval rules

- Document quality checks by stage

If a crew misses its slot, reset the schedule the same day. Idle days are the silent cost here, and they compound fast on a short flip.

5

Resale And Exit Strategy

Exit Plan First

The first flip does not create cash until the home is listed, sold, and closed, so the exit plan has to be set before the project finishes. The model assumes the first resale in Month 15, then Months 18, 25, 27, 31, and 38; if pricing slips, the next purchase can stall because cash recovery happens at closing.

This driver covers the listing channel, comp-based pricing, staging, buyer inspections, negotiation limits, and financing risk. The model applies 65% selling costs and commissions in Year 2, so weak resale control can compress margin fast and delay the next launch.

Lock the Sale Path Early

Before opening, pick the sale channel, set the list price from comps, and define the lowest acceptable offer. Since cash recovery happens at closing, the business needs enough working capital to carry taxes, insurance, debt service, and staging through buyer inspections and lender review.

If the buyer depends on shaky financing, the deal can slip after the rehab is done. That hurts day-one operations because finished inventory sits idle, resale cash is delayed, and the next acquisition can’t move on schedule.

- Choose agent or buyer channel early.

- Price from recent comparable sales.

- Stage for photos and inspections.

- Set negotiation limits before listing.

- Screen buyer financing risk fast.

6

Related Products

- House Flipper Porter's Five Forces Analysis

- House Flipper BCG Matrix

- House Flipper Business Model Canvas

- 7 Critical KPIs to Track for House Flipper Success

- House Flipper Business Plan Template in Pre-Written Word

- Boost House Flipper Profitability with 7 Financial Strategies

- How Much Does It Cost To Run A House Flipper Business Each Month?

- House Flipping Startup Costs: $106M Cash Need Through Month 60

- House Flipper Financial Model Template in Excel

- How Much Does A House Flipper Make? 6-Flip Owner Income Plan

- How to Write a House Flipper Business Plan in 7 Actionable Steps

- House Flipper Marketing Mix

- House Flipper Marketing Plan

- House Flipper Business Proposal

- House Flipper PESTEL Analysis

- House Flipper Pitch Deck Example Editable PPTX

- House Flipper Business SWOT Analysis

- House Flipper Value Proposition Canvas

Frequently Asked Questions

Start by setting the business entity, bank account, financing path, deal criteria, contractor bench, inspector access, insurance, and resale plan In the model, the first acquisition is Month 2, construction starts Month 4, and resale happens Month 15 That sequence only works if funding, repair estimates, and buyer demand are checked before closing