Owner incomeN/A

Owner incomeN/AHow Much Hydroelectric Power Generation Owners Make on $258M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeN/A  Net margin76.3%

Net margin76.3% Revenue for target pay$25.8M

Revenue for target pay$25.8M Business difficultyHard

Business difficultyHard

Key Takeaways

- More MWh and price drive most revenue.

- Outages cut cash before fixed costs can fall.

- Debt service can erase operating profit quickly.

- Reserves lower payouts but protect future cash.

Owner incomeN/ANet margin76.3%Revenue for target pay$25.8MBusiness difficultyHardWant to test your hydro plant owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Not guaranteed salary, tax advice, or owner distribution advice.

Checking owner income in the hydro cash-flow model?

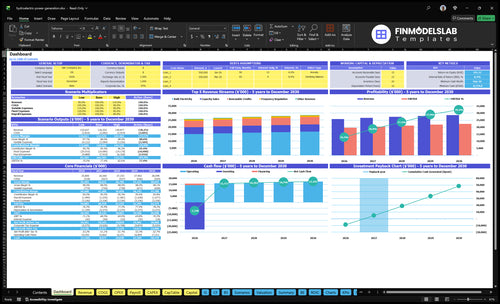

The dashboard shows $258M first-year revenue, $25282M gross profit, and 980% direct-cost margin; owner pay stays blank or editable where fixed costs and debt are missing. Open the Hydroelectric Power Generation Financial Model Template.

Owner-income model highlights

- Revenue mix chart

- Margin bridge chart

- Debt coverage chart

- Reserve funding chart

- Owner distributions chart

How big does a hydroelectric plant need to be to pay the owner?

The answer isn’t a universal MW number. For Hydroelectric Power Generation, the size depends on the owner’s cash target, annual MWh, capacity factor, contract price, leverage, reserves, and whether you self-operate or hire operators; the first-year model shows 300,000 MWh and 300,000 renewable credits, but no installed MW or capacity factor. Here’s the quick math: required annual cash = target owner pay + fixed O&M + debt + reserves - non-energy revenue, then divide by contribution per MWh.

Size drivers

- Target pay sets the floor

- 300,000 MWh is first-year volume

- Capacity factor drives output per MW

- Contract price sets cash per MWh

Cost load

- Fixed O&M cuts owner cash

- Debt must be covered

- Reserves reduce distributable cash

- 300,000 renewable credits are non-energy revenue

How much revenue does a hydroelectric plant generate?

For Hydroelectric Power Generation, revenue is mainly annual MWh sold × realized electricity price, plus renewable credits and grid services. Using the provided source math, first-year revenue is about $258M from $150M bulk electricity, $45M renewable credits, $10M frequency regulation, $300k spinning reserve, and $50M capacity sales. PPAs cut price swings, but merchant sales can move revenue materially.

Revenue drivers

- MWh sold drives base revenue

- Electricity price sets realized cash

- Renewable credits add extra income

- Ancillary services boost grid revenue

Price risk

- PPAs reduce volatility

- Merchant sales move with market prices

- Capacity sales can add $50M

- First-year source total: $258M

How much does a hydroelectric plant owner make?

A Hydroelectric Power Generation owner makes distributions only after fixed O&M, staffing, insurance, compliance, debt service, taxes, and capital reserves, not from top-line revenue; start with annual MWh and capacity factor using What Is The Main Indicator That Shows Hydroelectric Power Generation Efficiency?. Here’s the quick math: the first-year model lists $258M revenue and $518k direct costs, which leaves $257.482M before unlisted costs, so the stated about $25.282M gross profit needs reconciliation before owner take-home is modeled.

Earnings drivers

- Annual MWh produced

- Capacity factor achieved

- PPA price per MWh

- Ancillary grid revenue

Take-home limits

- Subtract fixed O&M

- Fund maintenance reserves

- Pay loan service

- Model taxes before distributions

Want to see what drives hydro owner income?

1

300K MWhGeneration

First-year output is 300,000 MWh, so every extra MWh feeds both bulk power and credit revenue.

2

$50/$15Price Mix

Year 1 bulk power sells at $50/MWh and credits at $15, so the contract mix sets most of the $25.8M revenue.

3

$518KPlant Uptime

When turbines run cleanly, the model stays near $518K of direct cost and protects the 98% gross margin before overhead.

4

$4.6MOverhead

Fixed costs and wages total about $4.63M a year, and that is what turns a strong plant into real owner cash or not.

5

-$8.3MFinancing

Cash bottoms at about -$8.335M in month 9, so debt terms and funding speed decide whether profit turns into cash.

6

$22.75MReserves

Planned capex totals $22.75M, and reserve policy decides how much cash stays in the plant instead of reaching owners.

Hydroelectric Power Generation Core Six Income Drivers

Annual Energy Generation

Annual Energy Generation

Annual MWh is the cash driver here. Nameplate capacity is not the billable output, so the owner gets paid on water that actually turns into power. In the model, generation starts at 300,000 MWh in Year 1 and rises to 320,000 MWh by Year 5, with first-year bulk electricity revenue of $150M before credits and ancillary income.

When streamflow drops, environmental flow limits tighten, turbines go down, or seasonal hydrology shifts, billable MWh falls and revenue falls with it. That hits cash flow before fixed costs adjust, so a 10% MWh shortfall is roughly a 10% revenue shortfall on the affected volume. The owner feels that drop first in profit and then in draw capacity.

Track the MWh gap early

Use a monthly MWh bridge: forecast vs actual, then split the gap into flow, outage, maintenance, and curtailment. The key inputs are river flow, environmental releases, turbine uptime, and seasonal pattern. If the plant keeps missing plan, the fix is usually timing maintenance better and tightening outage response, not waiting for higher water.

- Track actual MWh by month.

- Log outage hours and causes.

- Model low-flow downside monthly.

- Match maintenance to weak hydrology.

That matters because the owner’s pay comes from cash left after operating costs. If output stays near 300,000 MWh and rises toward 320,000 MWh, revenue quality improves. If it slips below plan, the shortfall cuts distributable cash right away, and the estimate hides weather swings and forced outages.

1

Realized Electricity Price

Realized Electricity Price

Realized electricity price is the dollars earned per MWh after contract terms and renewable credit value. In the source model, it starts at $50/MWh in Year 1 and rises to $5,250/MWh by Year 5, with renewable credits adding $15 per credit in Year 1 and $1,650 by Year 5. At 300,000 MWh, every $1/MWh moves annual revenue by $300,000.

Power purchase agreements (PPAs) can steady cash flow, while merchant pricing can swing fast. Do not assume a premium for renewable energy in every market. This driver sets gross revenue before fixed costs, so even a small price miss can cut owner pay hard when volume is this large.

Price Control Tips

Track realized $/MWh by contract, market, and credit value, not just the headline sale price. Build a simple bridge: MWh sold × realized price + credit revenue. That shows whether income is coming from the PPA, merchant sales, or credits, and where margin is leaking if market prices weaken or credit values fall.

Test how much volume sits under fixed pricing versus merchant exposure. If the plant sells 300,000 MWh, a $10/MWh price drop means about $3.0 million less revenue. Keep settlement dates, credit eligibility, and contract floors tight, because cash timing matters as much as price when you pay debt, staff, and owners.

2

Plant Efficiency And Availability

Plant Efficiency And Uptime

Plant efficiency and availability decide how much water becomes billable MWh. In the source model, output rises from 300,000 MWh in Year 1 to 320,000 MWh by Year 5, so even small uptime gains can lift revenue and owner cash. This is an operating cash-flow lever, not just an engineering metric.

The catch is simple: outages cut revenue, but some costs still run. Turbine condition, generator reliability, planned maintenance, sediment, controls, and grid interconnection availability all affect uptime. The model does not give outage rates or capacity factor, so the real income swing depends on how often the plant is down and how fast it returns to service.

Track Uptime, Not Just Output

Measure availability as hours online divided by hours scheduled, and tie it to lost MWh and lost revenue. Here’s the quick math: if a unit misses production during high-price hours, the cash hit is bigger than the same outage in a low-price hour. That matters for owner draw because fixed labor, insurance, and compliance costs keep going.

Watch the drivers that actually move billable power:

- Turbine efficiency by unit

- Forced outage hours

- Planned maintenance days

- Sediment and debris load

- Grid interconnection downtime

Use those logs to test whether maintenance timing, controls tuning, or parts replacement restores MWh faster than the downtime costs. If outages cluster in one season, that is usually where owner income is leaking.

3

Operating And Compliance Costs

Operating And Compliance Costs

This driver cuts distributable cash, even with no fuel expense. In Year 1, direct costs are about $518k, across power, renewable credits, frequency regulation, spinning reserve, and capacity sales. If output or market prices slip, those costs still sit there, so owner pay falls faster than top-line revenue.

The bigger risk is the cost stack you do not see in the direct line item: operators, insurance, monitoring, permits, dam safety, environmental studies, vegetation, sediment, and repairs. Uneven repair spikes can wipe out a month of distributions, so the real test is not just margin, but cash left after compliance and maintenance.

Track the full operating burden

Build a monthly cost bridge from fixed costs and per-unit costs. Separate costs tied to 300,000 MWh from costs that stay flat, then test how a lower MWh run rate changes cash available to the owner. If a repair, permit issue, or sediment event pushes costs above plan, distributions should be cut before cash runs thin.

Watch three inputs closely: availability, compliance spend, and repair reserves. If the plant misses generation, the revenue loss lands first, but compliance and staffing still need payment. Here’s the quick rule: protect cash before pay, because one unplanned dam or turbine repair can absorb the owner’s draw for the period.

4

Debt Service And Financing

Debt Service Load

Debt service is the loan payment stack: interest, principal, and any required r eserve funding. For a hydro plant, the same $258M first-year revenue can leave very different owner cash depending on purchase price, construction cost, interest rate, amortization, grants, tax credits, and lender coverage rules.

Here’s the key split: project profit before debt is not cash in the owner’s pocket. If annual debt payments are high, they can absorb most operating cash and turn a strong plant into a low-distribution asset. The real risk is a good water year still failing to create enough free cash after loans.

Cut Payment Drag

Track debt service coverage ratio, or DSCR, which is operating cash flow divided by annual debt service. Build cases for base, low-water, and outage years, because lower billable MWh hits cash before lenders relax. Also separate project profit from cash available after loans, reserves, and covenant limits.

- Test fixed vs variable rates.

- Match amortization to PPA term.

- Apply grants and tax credits first.

- Stress cash after debt and reserves.

To raise owner pay, reduce borrowed capital where you can, lock cheaper rates when possible, and avoid a structure that depends on perfect output. If debt is too heavy, the plant may look profitable on paper but still pay the owner poorly.

5

Capital Reserves And Reinvestment

Capital Reserves And Reinvestment

If you pay out every spare dollar, the plant can look strong today but hurt owner income later. Capital reserves are cash set aside for turbine overhauls, generator repair, dam rehabilitation, relicensing, and hydrology shock events, so one big repair does not become a forced capital call.

Here’s the quick math: owner take-home equals operating cash flow minus debt service minus reserve funding. The model shows 300,000 MWh in Year 1 rising to 320,000 MWh by Year 5, with direct costs of about $518k in Year 1. What this estimate hides is the size and timing of major civil works, control-system replacement, and outage costs.

Reserve Before You Distribute

Set the reserve rule before owner draws start. Tie the funding target to the maintenance calendar, permit timing, and outage history, then test whether the plant can still cover debt and normal ops. One major repair can erase months of pay if the reserve is too thin.

Track separate buckets for turbine overhaul, generator repair, dam safety, environmental mitigation, and unexpected outage costs. If annual generation slips, keep the reserve transfer intact anyway. That protects the asset and lowers the chance of a forced capital call later.

6

Compare low, base, and high hydro owner-income scenarios

Owner income scenarios

Owner income moves with output, realized price, and the light direct-cost layer, while debt service and reserves can still cut cash fast. Keep low and high cases editable.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path, where output and realized price both come in soft. | This is the modeled run-rate case, using the stated output and pricing assumptions. | This is the stronger earnings path, where output, price, and cash conversion all improve. |

| Typical setup | Production and credit sales run below base, merchant pricing weakens, and debt or reserve needs take a bigger bite out of cash. | The model uses 300,000 MWh of bulk power, 300,000 renewable credits at $15, plus the other listed sales for about $25.8M of revenue and $518k of direct costs. | Output and realized price improve, operating drag stays lean, and reserves or debt service stay manageable. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | User-edited downsideLow Case | $19.7M EBITDABase Case | User-edited upsideHigh Case |

| Best fit | Use this to stress-test hydrology risk, price risk, and tighter cash coverage. | Use this as the main planning case for underwriting and owner take-home checks. | Use this to test upside from better water flow, stronger merchant pricing, and cleaner cash flow. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Hydroelectric Power Generation Porter's Five Forces Analysis

- Hydroelectric Power Generation BCG Matrix

- Hydroelectric Power Generation Business Model Canvas

- 7 Critical KPIs to Measure Hydroelectric Power Generation

- Hydroelectric Power Generation Business Plan Template in Pre-Written Word

- 7 Proven Strategies to Boost Hydroelectric Power Generation Margins

- Analyzing Monthly Running Costs for Hydroelectric Power Generation

- Hydroelectric Power Generation Startup Costs for a $258M Year 1 Plant

- Hydroelectric Power Generation Financial Model Template in Excel

- How to Open a Hydroelectric Power Generation Business in 2 to 7+ Years

- How to Write a Hydroelectric Power Generation Business Plan

- Hydroelectric Power Generation Marketing Mix

- Hydroelectric Power Generation Marketing Plan

- Hydroelectric Power Generation Business Proposal

- Hydroelectric Power Generation PESTEL Analysis

- Hydroelectric Pitch Deck Example Editable PPTX

- Hydroelectric Power Generation Business SWOT Analysis

- Hydroelectric Power Generation Value Proposition Canvas

Frequently Asked Questions

It can pay the owner only after fixed O&M, debt service, reserves, taxes, and reinvestment The provided first-year model shows $258M revenue, about $518k listed direct costs, and roughly $25282M gross profit before missing cash-flow items That gross profit is not a guaranteed distribution