Owner income$180k

Owner income$180kHow Much Indie Film Production Owners Make: $180K Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180k  Net margin69%–79%

Net margin69%–79% Revenue for target pay$400k

Revenue for target pay$400k Business difficultyHard

Business difficultyHard

An indie film production company owner can make $180,000 per year in this model if project cash supports the CEO Executive Producer salary Company revenue is much larger than owner pay: $46 million in the first year, $72 million in the base case, and $118 million in the high case The key point is simple: film budget size is not owner income Take-home depends on producer compensation, completed projects, rights receipts, service work, overhead, reserves, and recoupment waterfalls

Owner income$180kNet margin69%–79%Revenue for target pay$400kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target owner pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Receipts can lag and recoupment can block distributions, so actual take-home can move a lot.

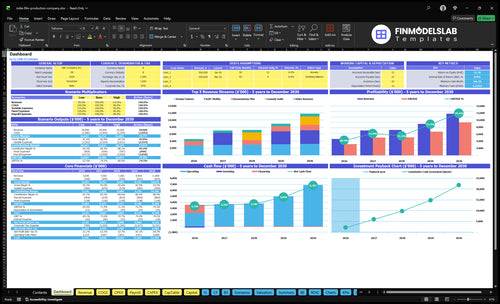

How does the Indie Film Production model turn messy film cash into owner pay?

This screenshot shows revenue, margin, costs, reserves, and take-home assumptions; open the Indie Film Production Financial Model Template.

Owner-income model highlights

- $46M to $118M revenue growth

- 3 to 5 projects tracked

- $180k pay, $138k overhead

- Assumptions, timing, recoupment tables

Can an indie film producer pay themselves from the budget?

Yes, an Indie Film Production producer can pay themselves from the budget if that pay is approved in the budget, financing plan, and investor documents; for this model, owner pay is $180,000/year through the CEO Executive Producer role, and What Is The Current Audience Engagement Level For Indie Film Production? matters because cash timing depends on sales and delivery. Do not treat investor funds as personal cash: separate producer fees, deferred pay, backend participation, production expenses, and investor recoupment.

Allowed Pay

- Approve pay before funds are raised

- Model salary at $180,000/year

- Use the CEO Executive Producer role

- Disclose terms in investor documents

Cash Risks

- Reserve $35,000 for project delivery

- Account for 55% revenue deal costs

- Track deferred compensation separately

- Expect income before cash receipts

Is an indie film production company more profitable with owned films or production services?

Owned films can be more profitable for Indie Film Production, but production services usually give steadier cash because fee income lands before rights income. Here’s the quick math: the owned-film slate grows from 3 projects and $46 million to 5 projects and $118 million, while owner pay stays at $180,000 a year. So the upside is bigger on owned films, but only if reserves are strong enough to handle timing gaps and distributions after obligations.

Owned films upside

- $46 million at 3 projects

- $118 million at 5 projects

- Rights income can be larger

- Cash arrives later than fees

Service work stability

- Fee income is steadier

- Helps between film launches

- Grants and incentives smooth cash

- Timing and compliance affect liquidity

How much revenue does an indie film production company need to pay the owner?

For Indie Film Production, first-year break-even revenue to cover $180,000 owner pay, $138,000 fixed overhead, and $105,000 of project delivery costs is about $507,000; here’s the quick math: ($180,000 + $138,000 + $105,000) ÷ 83.5%. The model says actual first-year revenue is $4.6 million, but that still doesn’t mean cash is free to pull out.

Break-even math

- $423,000 total modeled cost base

- 83.5% contribution before delivery costs

- $507,000 break-even revenue

- 3 projects in year one

Cash caution

- $4.6 million first-year revenue

- Add reserves before owner pay

- Pay debt service first

- Respect investor recoupment and financing

Want the six owner income drivers?

1

19 projSlate Volume

More projects spread fixed team cost across more revenue, so owner take-home moves up fast.

2

$46M-$118MRights Receipts

Scenario-based rights cash can lift take-home a lot, but it is not guaranteed profit.

3

50%-110%Cost Control

Keeping variable costs near the low end and delivery costs near $35K per project protects margin.

4

$138KOverhead Discipline

With fixed overhead around $138K a year, every lean month drops more cash to the owner.

5

5.5%Fee Structure

Deal fees, legal, delivery, admin, and residuals take a cut before gross receipts reach the owner.

6

$180KOwner Salary

The $180K salary is direct cash flow, but it can crowd out profit if the slate slips.

Indie Film Production Core Six Income Drivers

Project Slate Volume

Project Slate Volume

Project slate volume matters only when films are financed and completed. A slate of 3 projects in year one, 4 in the base year, and 5 in the mature year can raise producer fees and service revenue, but each project also adds about $35,000 in delivery cost and more cash timing risk. One clean metric is completed projects with collected receipts.

More projects can lift owner income, but only if overhead and recoupment stay controlled. If a project is still in development, it does not pay the owner. The real test is whether the slate turns into cash after delivery, fees, and paybacks. More volume without receipts can strain cash and delay owner draws.

Track Completed Cash, Not Ideas

Measure financed projects, completed projects, and collected receipts separately. That tells you how much of the slate actually turns into income. Also track per-project delivery cost at $35,000 and compare it to producer fees and service revenue so you can see if volume is adding profit or just work.

Keep the slate tight until recoupment timing is clear. A bigger slate helps only when cash comes back on schedule and fixed overhead stays covered. 3 projects is the first-year pace, 4 is the base case, and 5 is the mature target. If receipts slip, owner pay should be protected before taking on more projects.

- Track receipts by completed film

- Book $35,000 delivery cost each

- Separate development from funded work

- Watch recoupment timing closely

1

Producer Fee Structure

Producer Fee Structure

Owner pay is clearest when the producer fee is contracted upfront or tied to milestones. In this model, the CEO Executive Producer pay is $180,000/year, not a separate percentage fee. That matters because a paid fee covers living costs before rights revenue arrives, while deferred fees can make the budget look better on paper but tighten cash.

Backend participation is different from fee income and usually starts after recoupment, meaning project costs are paid back first. So the key inputs are fee amount, payment timing, and whether cash comes at signing, milestone, or delivery. If the fee slips into backend-only comp, owner take-home drops in the short term and cash strain rises.

Lock the Fee in Writing

Set the fee in the contract and tie it to milestones the budget can actually fund. Track fee earned, fee collected, and days to cash. With fixed overhead plus owner salary at $26,500/month, deferred payment can create a fast cash gap even when the project still looks profitable.

Keep backend participation separate in forecasts so it does not replace producer fee income. Use one line for producer fees, one for rights revenue, and one for recoupment. That split shows whether owner pay is funded by current production cash or by later distributions, which is the difference between steady pay and waiting on a waterfall.

- Track fee timing by milestone.

- Separate fees from backend payouts.

- Match pay to funded cash.

2

Distribution And Rights Revenue

Distribution Rights Cash

What matters here is actual receipts, not the headline license value. Gross rights revenue can model from $46 million to $118 million, but cash to the owner is reduced by sales agent commission, legal fees, delivery, collection, admin fees, residuals, marketing, and recoupment waterfalls. One clean line: gross deals do not equal spendable cash.

Owner pay stays separate at $180,000/year, so rights income helps distributions only after deductions and timing delays clear. If delivery or recoupment stalls, cash can lag even when revenue is booked. The key input set is gross sales, deduction stack, and payment timing, because those drive margin, cash flow, and how much profit can reach the owner.

Track Net Receipts, Not Headline Sales

Build the forecast from gross rights value down to net receipts. Track commission, legal, delivery, collection, admin, residuals, marketing, and recoupment by title. If the waterfall is unclear, cash timing gets messy fast. One missed deduction can erase a lot of paper revenue.

- Reconcile gross vs. net per deal

- Log delivery dates and acceptance

- Model payment lag by buyer

- Reserve cash for deductions

Test best case, base case, and delayed case. Rights income is high upside, but it is volatile. The owner should only count distributions after receipts clear and recoupment is settled, because that is what protects the $180,000/year pay plan.

3

Production Cost Control

Production Cost Control

Cost control protects the owner’s pay because this model carries 55% of revenue in direct costs, plus $35,000 per project for delivery work like legal review, metadata, quality control, and archiving. If those costs drift, producer fees and cash reserves get squeezed fast, even when the film looks profitable on paper.

Marketing and festival spend also matters: it runs at 110% in year one and drops to 50% in the mature year. Don’t underfund production just to fake margin. A delayed post-production finish can trap cash in the edit bay while receipts sit outside the bank account.

Track Budget Burn Before It Hits Cash

Measure cost control by project, not by the whole company. Track direct cost as % of revenue, the $35,000 delivery load, and the timing of marketing, festival, and post-production payments so you can see when cash will actually leave.

- Budget each project separately.

- Hold contingency for delays.

- Compare spend to revenue receipts.

- Protect reserve cash first.

The owner’s take-home improves when each completed film clears delivery costs and still leaves room for fees and draws. If one project slips, the fix is tighter spend control, not higher accounting margin. Keep a weekly check on committed spend, remaining post-production work, and cash due in the next 30 to 60 days.

4

Fixed Overhead Discipline

Fixed Overhead Discipline

Fixed overhead discipline means keeping company burn at $11,500/month, or $138,000/year, before the $180,000 owner salary. The key inputs are office rent, legal and accounting, software, insurance, utilities, internet, travel, and entertainment. Keep these company costs separate from direct film budgets and personal spend, or you’ll blur the real cash picture.

Here’s the quick math: overhead plus owner pay is $26,500/month, or $318,000/year. If burn creeps up, cash gets tight even when a film looks healthy on paper. Lower fixed burn doesn’t create revenue, but it does raise the odds that cash can cover owner pay between films.

Tra ck Burn by Month

Measure fixed overhead against funded work, not against total project revenue. Use a 13-week cash forecast and review it before every greenlight so company costs don’t eat the next owner draw.

- Separate company and film spend.

- Review recurring costs monthly.

- Cut unused software fast.

- Cap travel and entertainment.

5

Service, Incentive, And Grant Cash Flow

Service And Incentive Cash Flow

This income driver is the bridge income from production services, branded content, grants, rebates, and tax incentives. It matters because owned films pay in waves, but fixed overhead plus owner salary is $26,500/month, so cash timing can decide whether the owner gets paid on time.

The key inputs are eligible spend, award rate, reimbursement lag, and collection timing. No guaranteed grant or incentive revenue is in the source data, so this should be modeled as an editable scenario, not assumed income. If cash arrives after spend, liquidity tightens and owner draws should wait until reserves are in place.

Track Cash Before You Distribute

Measure each deal by approved amount, cash received, and days to reimbursement. That shows whether service work and incentives really smooth the gap between films or just create paper profit. One clean rule: don’t pay owner distributions from money that is still waiting on audit or eligibility review.

Build a monthly cash forecast that separates earned revenue from reimbursable revenue. Track filings, backup docs, and payment status by project, and keep reserves sized for $26,500/month before owner pay. If a rebate or grant slips, the business still needs enough cash to cover overhead without forcing a cut to production budgets.

6

Compare lean, base, and high owner income scenarios

Owner income scenarios

Owner take-home moves with project count, slate mix, and how fast film cash recoups. The model keeps salary at $180,000, but distributions depend on timing and reserves.

| Scenario | Lean CaseCash timing risk | Base CaseRepeatable slate | High CaseRights upside |

|---|---|---|---|

| Launch model | This is the lower-income path where first-year output is small and cash lands unevenly. | This is the modeled middle path where project flow is steady and owner income tracks a repeatable slate. | This is the stronger earnings path where more projects and tighter overhead support upside. |

| Typical setup | It assumes three first-year projects, about $4.6 million of revenue, about $138,000 of fixed overhead, and a $180,000 modeled owner salary. | It assumes four projects, about $7.2 million of revenue, a stronger release mix, and a $180,000 owner salary. | It assumes five projects, about $11.8 million of revenue, better rights sales, and a $180,000 owner salary. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $180,000 salary baseLean take-home | $180,000 salary baseBase take-home | $180,000 salary plus upsideHigh upside |

| Best fit | Use this to stress-test slow recoupment and tight cash timing. | Use this as the core operating case for planning. | Use this to test stronger recoupment and more efficient overhead use. |

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution amounts; actual take-home changes with taxes, debt, reserves, and recoupment.

Related Products

- Indie Film Production Porter's Five Forces Analysis

- Indie Film Production BCG Matrix

- Indie Film Production Business Model Canvas

- 7 Critical KPIs to Measure Indie Film Production Success

- Indie Film Production Business Plan Template in Pre-Written Word

- 7 Proven Strategies to Increase Indie Film Production Profitability

- Analyzing Monthly Running Costs for Indie Film Production Operations

- Indie Film Production Startup Costs For A 3-Film Year 1 Slate

- Indie Film Production Financial Model Template in Excel

- How to Start an Indie Film Production Company in 8–20 Weeks

- How to Write an Indie Film Production Business Plan

- Indie Film Production Marketing Mix

- Indie Film Production Marketing Plan

- Indie Film Production Business Proposal

- Indie Film Production PESTEL Analysis

- Indie Film Production Pitch Deck Example Editable PPTX

- Indie Film Production Business SWOT Analysis

- Indie Film Production Value Proposition Canvas

Frequently Asked Questions

The model shows $180,000 in annual owner pay through the CEO Executive Producer role That is not the same as company revenue, which ranges from $46 million in the first year to $118 million in the mature year Extra distributions depend on reserves, debt, taxes, investor recoupment, and actual cash receipts