Owner income$1.46M

Owner income$1.46MHow Much Can An Independent Music Label Owner Make? $110k+ Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$1.46M  Net margin72.5%

Net margin72.5% Revenue for target pay$1.82M

Revenue for target pay$1.82M Business difficultyHard

Business difficultyHard

You’re building catalog value, but owner pay depends on cash timing This 5-year model shows $110,000 in annual CEO pay, Year 1 EBITDA of -$140,000, breakeven in 14 months, and Year 5 EBITDA of $4837 million It covers revenue, costs, reserves, reinvestment, and owner take-home planning, not tax or legal advice

Owner income$1.46MNet margin72.5%Revenue for target pay$1.82MBusiness difficultyHardWant to test your label owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margin, payroll, taxes, debt, reserve policy, and owner distribution rules; it is not guaranteed salary, tax advice, or owner distribution advice.

Want to see the full Independent Music Label forecast and owner pay?

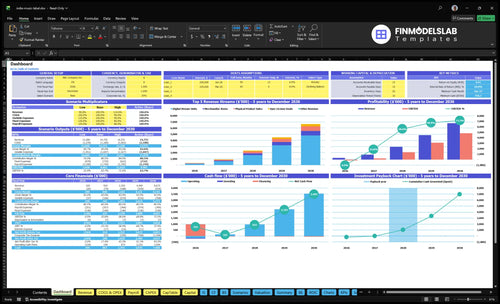

This screenshot shows revenue, margins, costs, reserves, and owner take-home; open the Independent Music Label Financial Model Template. It’s planning-led, not a promise.

Owner-income model highlights

- Owner pay is modeled

- Four-channel revenue build

- EBITDA: -$140k to $4.837M

- Month 13 needs $757k

- Breakeven lands Month 14

- Payback lands Month 25

How many artists does an indie label need to make money?

There isn’t one magic roster number for an Independent Music Label; the real test is whether your active artists, releases per year, revenue per release, and recoupment status can cover spend. A solo founder can protect cash, but once you add A&R, marketing, project coordination, accounting, and royalty work, overhead rises fast, so the label has to earn on each release, not just grow the roster.

What drives profit

- Count active artists, not total signings.

- Track releases per year.

- Measure revenue per release.

- Watch recoupment status closely.

Year 1 cost plan

- CEO: $110k

- A&R: $75k at 0.5 FTE

- Marketing: $65k at 0.5 FTE

- Coordinator: $50k from Year 2

Can an independent music label make money?

Yes, an Independent Music Label can make money, but the base case turns profitable only after catalog income, sync, merch, and releases outrun artist costs, promotion, payroll, and overhead; see How To Write A Business Plan For Independent Music Label? for the planning steps. Here’s the quick math: $320k revenue still loses $140k EBITDA in Year 1, then reaches $237k EBITDA in Year 2 with breakeven in Month 14.

Money works when

- Catalog revenue compounds across releases

- Sync and merch gain traction

- Marketing spend creates repeat streams

- Costs stay below release income

Cash risk

- Year 1 EBITDA: -$140k

- Year 2 EBITDA: $237k

- Breakeven: Month 14

- Modeled CEO pay: $110k

How much revenue does an indie label need to pay the owner?

For an Independent Music Label, owner pay has to be modeled separately: the $110k CEO salary is not covered by revenue until the business clears the early loss phase. In this plan, $320k of Year 1 revenue still produces -$140k EBITDA, while $920k of Year 2 revenue supports $237k EBITDA after modeled costs. Here’s the quick math: with 80% COGS, 115% variable costs, reserves, and artist payouts, breakeven lands around Month 14.

Year 1 reality

- $320k revenue still loses money.

- -$140k EBITDA in Year 1.

- $110k owner pay stays separate.

- Taxes are excluded from this model.

Year 2 setup

- $920k revenue supports profit.

- $237k EBITDA after modeled costs.

- Month 14 is breakeven timing.

- Artist payouts and reserves cut cash left.

Want the six income drivers?

1

$320K-$6.7MCatalog Revenue

Revenue scales from $320K in Year 1 to $6.675M in Year 5, so catalog growth is the biggest lift to owner income.

2

19.5%Rights Mix

Direct fees and variable spend take about 19.5% of revenue, so rights terms and payout timing decide how much cash reaches the label.

3

4 linesRevenue Mix

Digital, physical, sync, and merch spread risk across four income lines, which steadies cash when one channel slows.

4

5K-120KRelease Pace

Digital stream units rise from 5,000 to 120,000, so a steady release calendar keeps discovery and royalties compounding.

5

10%Promo ROI

Targeted marketing and DSP promotion run at 10% of revenue, so each paid dollar has to bring back more streams or merch than it costs.

6

$757KCash Runway

Fixed overhead is about $12.2K a month, breakeven lands in Month 14, and the $757K cash floor decides how long growth can keep running.

Independent Music Label Core Six Income Drivers

Catalog Revenue

Catalog Revenue

Catalog revenue is the money a label keeps earning after a release has recouped. In this model, Year 1 starts at 5,000 digital stream units at $40, then grows to 120,000 by Year 5. The catch is simple: gross streaming receipts are not owner income, because distribution fees, artist royalties, and reserves get paid first.

This driver matters because a strong back catalog smooths cash flow and reduces pressure to fund constant new launches. If catalog decay is weak, the label has to keep spending on new releases just to stand still. Monthly royalty statements help only when older releases keep earning enough to cover the fee stack and leave real profit for owner draw.

Track Recoupment And Decay

Measure net catalog cash, not gross receipts. Here’s the quick math: track each release’s gross streaming income, then subtract distribution fees, artist payouts, and reserve holds before counting what can reach the owner. A release only helps pay you if it keeps earning after those layers.

Watch the recouped catalog share, monthly royalty timing, and how fast older titles fade. If Year 1 units don’t keep compounding toward Year 5, cash gets pulled back into launch spend instead of owner pay. Use these inputs in the forecast:

- 5,000 Year 1 digital units

- 120,000 Year 5 digital units

- Fees, royalties, and reserves

1

Royalty And Rights Structure

Master Royalty Split

For an independent label, the master royalty split is the main cash lever. It decides how much of each release stays with the owner after the label share, artist royalty rate, advances, and recoupable expenses are paid. In this model, 20% digital aggregator fees and 60% physical manufacturing/distribution costs hit receipts first, so gross revenue is not owner income.

Without a set artist payout percentage, owner pay cannot be sized cleanly. The inputs that matter are label ownership share, license terms, net-profit split, royalty timing, and recoupment rules. If royalty statements lag, cash can look healthy on paper but still be tied up before distributions. That delay matters most when launches are frequent and overhead keeps running.

Track Recoupment Before Payouts

Build each release around cash available to owner, not just reported revenue. Track gross receipts, the 20% aggregator fee, 60% physical costs, artist royalties, advances, and any spend that must be recouped first. If a digital release brings in $1,000, only $800 remains before the artist split and recoupment.

- Test artist payout rates in scenarios.

- Model advances as delayed cash recovery.

- Age royalty statements by month.

- Block owner draws until recoupment clears.

2

Release Frequency And Roster Productivity

Release Volume

If the roster stays active, each release creates more shots at streams, physical sales, sync, and merch. In the model, output grows from 5,000 digital units, 2,000 physical units, 5 sync deals, and 1,500 merch items in Year 1 to 120,000, 30,000, 75, and 25,000 by Year 5. That is volume growth, not automatic profit.

The catch is cost. More releases mean more admin and more campaign spend, and that can drain cash before royalties land. If cadence outruns quality or control, owner pay falls even while the roster looks busier. More artists do not equal more profit. The quick test is simple: each extra release must earn more than its added launch cost and cash delay.

Track Per Release Economics

Count every launch before you approve it. Track release count, units by format, sync deals, merch items, and the admin plus campaign spend tied to each release.

- Watch revenue per release.

- Watch spend per release.

- Compare cash collected vs. spent.

Use a release-by-release forecast to see whether added volume improves owner cash. If a release cannot cover its own cost fast enough, slow the cadence, trim the roster, or tighten spend. The owner gets paid from disciplined output and margin, not from a bigger roster label alone.

3

Marketing Efficiency

Marketing Efficiency

Owner income rises when marketing turns each release into durable streams, fan growth, sync interest, and merch demand. In this model, 100% of revenue goes to targeted marketing and promotion, plus 15% for artist content support, so cash only reaches the owner if post-campaign revenue outruns spend.

Here’s the quick math: if PR, videos, playlist pitching, or ads cost more than the release earns back after launch, margin disappears before owner distributions. Track cost per release against post-campaign revenue. Paid promotion is a sensitivity variable, not a guarantee, so weak campaigns should not be scaled.

Control release payback

Measure whether each campaign lifts streaming, merch, and sync income after launch. Compare that lift to the full marketing bill and the 15% artist content support load. One clean rule: if a release does not pay back, do not increase spend on the next one.

Track these inputs:

- Campaign cost per release

- Revenue at 30, 60, 90 days

- Repeat plays and fan growth

- Merch and sync lift

4

Diversified Revenue

Diversified Revenue

Diversified revenue adds sync, physical sales, merch, publishing participation, and partnerships so the label is not depending only on streaming. In Year 5, the model shows 75 sync deals x $5,000 = $375,000, 30,000 physical units x $25 = $750,000, and 25,000 merch items x $30 = $750,000, or $1.875 million gross before costs and splits.

This helps owner income only if the label actually owns or participates in the rights. No rights, no cash. Physical sales also carry heavy cost drag; with 60% manufacturing and distribution, a $750,000 physical line can shrink fast before artist payouts, reserves, and overhead hit profit.

Track rights before you count cash

Measure each stream on its own: deal count, units sold, average price, rights share, and direct cost. For sync, confirm the fee and split before you book it. For merch and physical, track gross margin by item, not just sales volume. $25 and $30 price points look strong, but margin decides owner pay.

Build the forecas t from settled money, not headline revenue. Watch contract timing, recoupable costs, and reserve holds, since those can delay distributions even when top-line sales look healthy. Revenue owned is income earned; revenue borrowed from someone else’s rights is not.

5

Overhead, Reserves, And Reinvestment

Overhead, Reserves, and Owner Pay

Cash discipline decides what can safely become owner pay. Fixed overhead is $122k per month for rent, software, legal/accounting, travel, insurance, and internet, and payroll adds $2.175M in Year 1. That means base recurring cost is about $3.639M in the first year before later staff growth, so profit on paper is not the same as cash you can take home.

The real constraint is liquidity, not just income. Minimum cash need reaches $757k in Month 13, so available cash is not automatically distributable cash. Owner draw should wait for royalty accounting, reserves, campaign reinvestment, and payback timing, or the business can pay the owner too early and starve the next release cycle.

Track Cash Before You Draw

Measure owner pay against a simple rule: cash after royalty settlements, fixed overhead, payroll, and reserved marketing spend. If a campaign has not paid back yet, keep that cash in the business. The key inputs are monthly overhead, payroll run rate, cash reserve target, and the lag between release income and statement payment.

Build a 13-month cash forecast and update it every release cycle. Watch for gaps between earned royalties and cash collected, because that gap is where owner draws get overpaid. One clean test: if the business cannot stay above the $757k minimum cash mark, owner pay should stay capped until the next royalty cycle clears.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income moves with the mix of streams, physical sales, sync deals, and merch, plus heavy upfront payroll and fixed overhead. Early cash strain can cap draws, while later revenue widens room.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | The owner stays on a lean draw while the label sees slower catalog traction and fewer sync checks. | The owner follows the model case, with pay anchored to the $110k CEO salary and room opening after breakeven. | The owner gets a stronger income path if release volume and sync wins run ahead of plan, but take-home still lags gross growth. |

| Typical setup | Digital streams, physical sales, and merch stay below plan, so payroll, marketing, and fixed overhead absorb most cash. | This path uses $320k Year 1 revenue, $920k Year 2 revenue, and $6.675m by Year 5, with EBITDA rising from -$140k to $4.837m. | This case assumes stronger catalog pull and licensing volume, while still carrying 8.0% COGS, 11.5% variable costs, and 146.4k fixed overhead. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $75,000Low Case | $110,000 - $160,000Base Case | $180,000 - $300,000High Case |

| Best fit | Use this to test cash strain, thin distributions, and reinvestment needs. | Use this as the main planning case for owner pay and cash timing. | Use this to test upside pay if growth beats the model and cash stays healthy. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Independent Music Label Porter's Five Forces Analysis

- Independent Music Label BCG Matrix

- Independent Music Label Business Model Canvas

- What Are The 5 Core KPI Metrics For Independent Music Label Business?

- Independent Music Label Business Plan Template in Pre-Written Word

- How Increase Profits For Independent Music Label?

- What Are Operating Costs For Independent Music Label?

- How Much It Costs To Start An Independent Music Label: $757K Plan

- Independent Music Label Financial Model Template in Excel

- How To Open An Independent Music Label In 8–16 Weeks

- How To Write A Business Plan For Independent Music Label?

- Independent Music Label Marketing Mix

- Independent Music Label Marketing Plan

- Independent Music Label Business Proposal

- Independent Music Label PESTEL Analysis

- Independent Music Label Pitch Deck Example Editable PPTX

- Independent Music Label Business SWOT Analysis

- Independent Music Label Value Proposition Canvas

Frequently Asked Questions

The modeled owner can receive $110,000 in annual CEO pay if they run the label, but Year 1 EBITDA is still -$140,000 That means early pay depends on startup cash, not surplus profit By Year 2, EBITDA reaches $237,000 on $920,000 revenue, so distributions become more realistic if reserves and artist payouts are covered