Owner income$180k

Owner income$180kHow Much Internal Communications Agency Owners Make: $180k Salary Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180k  Net margin-30% to 53%

Net margin-30% to 53% Revenue for target pay$608k

Revenue for target pay$608k Business difficultyHard

Business difficultyHard

You’re modeling owner pay, not an employee communications salary In this US internal communications agency model, owner compensation is planned around a $180,000 CEO / Lead Strategist salary, with EBITDA moving from -$129k in Year 1 to $19M in Year 5 Revenue, payroll, overhead, reserves, and distributions are separate planning lines

Owner income$180kNet margin-30% to 53%Revenue for target pay$608kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the gap to your target pay from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Need a deeper owner income forecast?

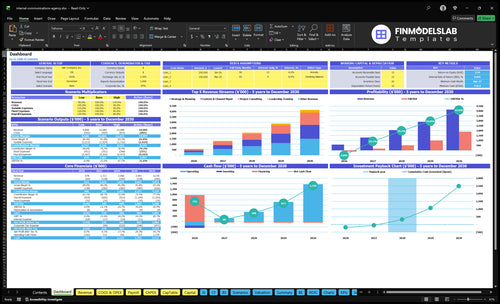

The screenshot in the Internal Communications Agency Financial Model Template shows dashboard, revenue assumptions, staffing costs, overhead, scenarios, cash flow, and owner pay—open the model.

Owner-income model highlights

- EBITDA by year

- Breakeven in Month 9

- Payback in 30 months

- Minimum cash $719k Month 16

- Year 5 EBITDA $19M

How much revenue does an internal communications agency need to pay the owner?

An Internal Communications Agency needs about $608k in annual revenue to pay the owner $180k inside payroll under the listed Year 1 cost structure; use What Is The Primary Goal Of Your Internal Communications Agency? to anchor that target to the business goal. At the implied Year 1 revenue of about $429k, EBITDA is about -$129k, so the owner pay is a target-pay model, not a guaranteed salary.

Quick Math

- Owner salary modeled: $180,000

- Fixed overhead plus payroll: $437.7k

- COGS plus variable costs: 28.0%

- Breakeven revenue: $608k

Pay Risk

- Year 1 revenue implied: $429k

- Year 1 EBITDA: -$129k

- Year 2 EBITDA: $185k

- Higher payroll raises the revenue hurdle

Can an internal communications agency owner make more by scaling?

An Internal Communications Agency can make more by scaling, but only if the extra work covers the added payroll and management load. If the founder stays billable at $250 to $330 per hour, the owner-led model keeps margin high; if the agency shifts to a team model, profit can rise, but so does execution risk. Here’s the quick math: a team-based model can move from -$129k in Year 1 to $19M in Year 5, but the owner still has to fund a $180k salary and reserves.

Owner-led profit

- $250 to $330 hourly keeps margin high

- Founder stays billable, not just managing

- Lower payroll, simpler delivery

- Best when demand is steady

Team scale risk

- -$129k to $19M EBITDA path

- Payroll grows with headcount

- Non-billable owner needs reserves

- Risk rises if utilization lags

How does retainer pricing affect recurring revenue for an internal communications agency?

Retainers make an Internal Communications Agency easier to run because they turn lumpy project income into steady monthly cash for payroll and fixed overhead. With hourly rates of $250 to $275 for Strategy & Planning, $200 to $220 for Content & Channel Mgmt, $300 to $330 for Leadership Training, and $225 to $245 for Project Consulting, Year 1 service units point to about $3,750, $4,000, $2,400, and $5,625 before scope changes. Recurring advisory and content support help stabilize cash; one-time change communications, intranet, culture, and leadership projects can raise revenue, but they may need contractors.

Recurring cash

- Retainers smooth monthly revenue

- Payroll becomes easier to plan

- Fixed overhead stays covered

- Advisory and content support fit well

Project upside

- One-time projects can lift revenue

- Scope changes can raise billings

- Contractors may be needed

- Project Consulting can add $5,625

What really drives owner income?

1

HighRetained Clients

Recurring accounts are what move EBITDA from -$129K in Year 1 to $1.9M in Year 5, so retention is the first lever on owner pay.

2

11%-7%Delivery Margin

Third-party specialist fees fall from 8% to 5% and software licenses from 3% to 2%, so more billed revenue stays after delivery cost.

3

$180KOwner Utilization

The CEO / Lead Strategist salary is $180,000, so every billable hour the owner sells instead of handling admin protects cash.

4

$200-$330/hrAvg Retainer

The rate card runs from $200 to $330 an hour across services, so small price lifts compound fast across retained work.

5

$5.85K/moOverhead + Reserves

Fixed overhead is $5,850 a month, marketing spend rises from $50K to $150K, and CAC falls from $2,500 to $1,600, so reserve discipline decides how much EBITDA turns into cash.

6

70%Project Mix

The mix shifts toward content at 70% and consulting at 40% by Year 5, so service mix changes capacity and cash per client.

Internal Communications Agency Core Six Income Drivers

Retained clients

Retained clients

Retained clients are the accounts that keep paying month after month. Here, they lift recurring retainer revenue and make owner pay easier to plan. If marketing spend rises from $50k to $150k while CAC drops from $2,500 to $1,600, acquisition gets cheaper and the book should grow faster, but only if onboarding, strategist time, content, and admin capacity can absorb it.

At those figures, the same budget would buy about 20 clients at the old CAC and about 94 at the new CAC. That looks like better efficiency, but the real test is churn. If service depth runs past the team’s hours, retained revenue turns into rework, and profit, not sales, decides owner income.

Track retention before you scale

Track retained accounts, monthly churn, and hours per client. Tie client count to delivery load so every new retainer covers acquisition plus ongoing strategist, content, and admin labor. One clean rule: if a client needs more hours than priced, raise the retainer or cut scope before you add more accounts.

Build the forecast around recurring revenue, not just new wins. A healthy retainer base smooths cash flow and makes profit draws steadier, but onboarding delays or broad service scope can cancel the gain. Review account health each month and watch for clients that need extra leadership support, revisions, or channel management.

1

Average monthly retainer

Average Monthly Retainer

Average monthly retainer lifts owner income only when the scope stays tight. In this model, pricing should map to hourly rates: $250 to $275 for Strategy & Planning, $200 to $220 for Content & Channel Mgmt, $300 to $330 for Leadership Training, and $225 to $245 for Project Consulting.

Larger accounts can absorb planning, writing, channel support, and leadership messaging, so the retainer can rise without breaking the sale. But if scope creeps, the premium turns into low-margin labor. The key driver is not just price per month; it’s price per hour delivered. One clean rule: raise retainer only when scope and hours are controlled.

Price by Scope, Not Hope

Track active clients, monthly hours by service, and the margin on each retainer. Estimate income from retainer revenue minus delivery labor and overhead, then test whether each account still fits the rate card. If a client wants strategy, writing, channel support, and leadership training, price each layer separately instead of blending it into one flat fee.

- Cap hours in the contract.

- Track scope creep weekly.

- Reprice add-on work fast.

- Split strategy from execution.

What this hides: bigger retainers can improve cash flow, but only if delivery time stays inside the budgeted hours. If senior staff spend too long on low-rate content or channel tasks, owner pay drops even when revenue rises. A higher retainer should buy more value, not more unpriced labor.

2

Project mix

Project Mix

Project mix is the split between strategy, consulting, leadership training, and content or channel work. It changes owner income because each project type has a different rate and cost profile. Project consulting is the largest modeled service-unit revenue, at 25 hours × $225 = $5,625 in Year 1 and 30 hours × $245 = $7,350 in Year 5, while leadership training carries the highest hourly rate at $300–$330.

One clean rule: higher rate does not always mean higher take-home. Strategy-heavy work can be high value but founder-dependent, while content and channel work is steadier but more labor-heavy. If subcontractors or creative production are added, gross margin drops unless pricing rises too, so the owner may see more revenue but less cash left for pay.

Price the Mix by Margin

Track each project by hours sold, rate, direct labor, and subcontractor cost. That tells you which work actually funds owner pay. If a project needs senior strategy time plus outside creative help, build that into the fee instead of treating it as extra.

- Measure margin by service line.

- Separate founder time from team time.

- Price subcontractors into the job.

- Favor repeatable work for steadier cash.

Use leadership training to lift rate, but keep a cap on custom revisions and prep time. Use content and channel work to smooth revenue, but watch labor load closely. The key is not just filling the calendar; it is keeping billable hours and delivery cost aligned so the owner can actually draw more profit.

3

Delivery labor margin

Delivery Labor Margin

Delivery labor margin is the gap between what the client pays and the true cost to deliver the work. It includes strategist time, writers, content managers, junior consultants, project support, and contractors. When the team prices above that cost, gross margin improves and the owner has more room to pay themselves after payroll, software, and other overhead.

If senior people spend time on low-rate tasks, or contractors get added without a price reset, margin leaks fast. That risk grows as payroll excluding the owner expands. The key inputs are billable hours, blended rate, contractor fees, project software, and utilization. One weak project can drag the whole month.

Price the work to the real delivery cost

Build each project from the bottom up: strategist hours, writing hours, content management, junior support, and contractor cost. Then compare that true cost to the client price. If third-party specialist fees move from 80% to 50%, and project software from 30% to 20%, more revenue stays as gross profit and cash for owner pay.

Track utilization weekly, meaning billable hours divided by paid hours. If senior staff are doing junior work, reassign it or reprice it. If contractor use rises, update the quote before delivery starts. Keep a floor for margin by role and by project so the agency does not grow revenue while shrinking take-home income.

- Track hours by role.

- Compare price to delivery cost.

- Flag senior time on low-rate work.

- Reprice when contractors increase.

- Watch software and specialist fees.

4

Owner billable utilization

Founder billable utilization

If the founder stays billable, the agency can sell premium expertise and help support the $180k salary. Here’s the quick math: owner revenue comes from billable hours × hourly rate, so every hour on client work lifts income now, but it also steals time from sales, hiring, and quality control.

What this driver includes is the founder’s bil lable hours, rate, client mix, and how much work the team can deliver without escalation. If the founder goes non-billable too soon, team margin has to cover pay, $5,850/month fixed overhead, reserves, and growth spend. Scale only works when delivery stays strong without the founder on every account.

Protect founder billable time

Track billable hours, hourly rate, retained clients, and delivery labor cost every month. If founder time is spent on low-rate admin or rescue work, margin drops fast. Keep the founder on the highest-value strategy, leadership, and client-facing support work so the rate stays high enough to fund owner pay.

- Measure founder hours billed monthly.

- Track work shifted to staff.

- Watch client quality without founder rescue.

- Reprice scope before hours creep up.

If onboarding takes too long or every account needs founder approval, utilization stays high but the business stays stuck. The better move is to test one account with a clean handoff, then see whether the team can keep quality up while the founder frees time for sales and higher-margin work.

5

Overhead and reserves

Overhead and reserves

$5,850 a month in fixed overhead is the first drag on owner pay. That covers rent, software, insurance, accounting/legal, utilities, supplies, and website upkeep, or about $70,200 a year before growth spend. Add a marketing budget that rises from $50k to $150k, and cash gets tied up fast.

The key risk is timing. A $719k minimum cash balance in Month 16 and a 30-month payback window mean the business can look busy but still leave less cash for the owner. Cut waste, yes, but do not starve sales or delivery quality, or profit growth slows.

Control overhead and protect cash

Track overhead against monthly billings and reserve needs before any owner draw. If overhead rises faster than retained profit, take-home income gets squeezed even when revenue grows. The clean rule: spend where it shortens payback, not where it just adds activity.

- Watch rent, software, legal, utilities.

- Test marketing payback at 30 months.

- Hold the $719k cash floor.

- Measure reserve burn monthly.

What this estimate hides is simple: cutting overhead helps, but underinvesting in sales or delivery quality can slow profit growth. Keep the reserve model tied to client growth, then review spend before distributions, not after.

6

Compare low, base, and high owner-income cases

Owner income scenarios

Owner income changes fast in this agency because retainers, project work, and team payroll don't scale at the same pace. Early draws can come from cash, but higher pay only holds if utilization and retention stay high.

| Scenario | Low CaseEarly ramp-up | Base CaseModeled base | High CaseUpside case |

|---|---|---|---|

| Launch model | The owner keeps income low or fully funded by starting cash while the agency builds clients and closes its first projects. | The owner can pay a steady salary and a modest distribution once the agency moves through the Year 2 to Year 3 EBITDA range. | The owner takes a strong salary and distributions when retention, pricing, and volume stay high. |

| Typical setup | This model assumes early revenue near $429k, EBITDA at negative $129k, limited retained clients, and a $180k owner salary funded by starting capital or a cash buffer. | This case assumes stronger retention, a balanced mix of retainers and projects, EBITDA from $185k to $509k, and enough reserve discipline to keep owner pay stable. | This assumes a mature client book, higher average retainers, more project revenue, strong gross margin, overhead spread across a larger team, and reserves held before owner distributions. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $180,000Cash-funded draw | $180,000 - $350,000Steady owner pay | $500,000+Upside draw |

| Best fit | Use this to stress-test the first operating year when the business is still below break-even and the owner draw may not come from operating cash. | Use this as the working case for a growing agency with a real delivery team and room for pay above the starting draw. | Use this to test upside if the agency runs near capacity and the owner stays in a leadership role instead of handling most delivery work. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Internal Communications Agency Porter's Five Forces Analysis

- Internal Communications Agency BCG Matrix

- Internal Communications Agency Business Model Canvas

- 7 Critical KPIs for an Internal Communications Agency

- Internal Communications Agency Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Internal Communications Agency Profitability

- Analyzing the Running Costs for an Internal Communications Agency

- Internal Communications Agency Startup Costs: $719K Funding Plan

- Internal Communications Agency Financial Model Template in Excel

- How to Open an Internal Communications Agency in a Few Months

- How to Write an Internal Communications Agency Business Plan

- Internal Communications Agency Marketing Mix

- Internal Communications Agency Marketing Plan

- Internal Communications Agency Business Proposal

- Internal Communications Agency PESTEL Analysis

- Internal Communications Agency Pitch Deck Example Editable PPTX

- Internal Communications Agency Business SWOT Analysis

- Internal Communications Agency Value Proposition Canvas

Frequently Asked Questions

The researched model carries a $180,000 CEO / Lead Strategist salary EBITDA starts at -$129k in Year 1 and reaches $19M by Year 5, but EBITDA is not automatic take-home Owner distributions depend on reserves, taxes, reinvestment, debt service, and cash timing