Owner income$394K to $24.47M

Owner income$394K to $24.47MHow Much Can An IoT Consulting Owner Make? $394K Year 1 View

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$394K to $24.47M  Net margin73% to 83%

Net margin73% to 83% Revenue for target pay$1.21M

Revenue for target pay$1.21M Business difficultyHard

Business difficultyHard

An IoT consulting owner can model pre-tax owner benefit from $394K in Year 1 to $2447M in Year 5 under the provided assumptions That equals the $180K CEO / Lead IoT Consultant salary plus modeled EBITDA, which rises from $214K to $2429M These are researched planning assumptions, not guaranteed distributions Delivery costs fall from 27% of revenue in Year 1 to 17% in Year 5, while payroll rises from $500K to $1395M

Owner income$394K to $24.47MNet margin73% to 83%Revenue for target pay$1.21MBusiness difficultyHardWant to test your IoT consulting owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This output is a researched planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Can you check owner income in the IoT Consulting model?

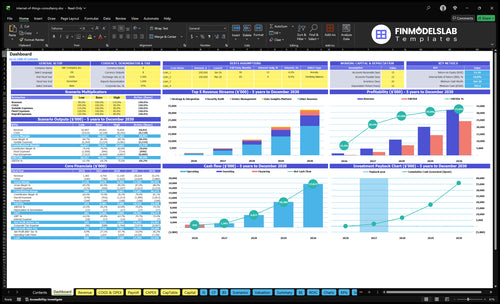

The IoT Consulting Financial Model Template shows the dashboard, income outputs, assumptions, revenue streams, staffing, expenses, cash, scenarios, and owner-pay outputs so you can see the path to a $703K minimum cash need, Month 6 break-even, 13-month payback, $214K Year 1 EBITDA, and $2429M Year 5 EBITDA.

Owner-income model highlights

- Owner pay output

- Revenue mix and margin

- Cash runway scenarios

How much revenue does an IoT consulting firm need to pay the owner?

If the owner needs $180K pay, IoT Consulting needs about $668K in annual revenue before reserves and marketing, using a 73% contribution margin. Here’s the quick math: year-one payroll is $500K including the CEO role, so non-owner payroll is $320K, and fixed overhead adds $168K a year. Required revenue = ($320K + $168K + marketing + reserves + owner pay, if not already in payroll) ÷ 0.73.

Core math

- $14K fixed overhead per month

- $168K fixed overhead per year

- 27% delivery-variable cost load

- 73% contribution margin

Revenue driver

- $500K Year 1 payroll

- $180K CEO role inside payroll

- $320K non-owner payroll

- ~$668K revenue before reserves

Can an IoT consulting business scale beyond the owner?

Yes, IoT Consulting can scale beyond the owner, but it stops being a solo service and becomes a managed delivery business. The starting team includes a $180K CEO, $140K Senior IoT Consultant, $150K Solutions Architect, and 0.5 admin FTE; by Year 5 it carries 3 senior consultants, 2 architects, 3 junior engineers, 15 sales FTE, and 1 admin FTE. That growth only works if delivery QA, sales pipeline, subcontractor control, and scope discipline stay tight, because payroll rises from $500K to $1395M.

Scale path

- Start with founder-led delivery

- Use senior staff first

- Add 3 junior engineers later

- Grow sales to 15 FTE

Margin risks

- Keep QA tight

- Feed hires with pipeline

- Control subcontractors hard

- Stop scope creep early

What profit margin can an IoT consulting business make?

An IoT consulting business can post strong margins if it keeps advisory work separate from implementation work. In the model, software licensing falls from 8% of revenue in Year 1 to 5% in Year 5, while subcontractors drop from 10% to 7%, travel from 5% to 3%, and storage from 4% to 2%; see How Much Does It Cost To Open And Launch Your IoT Consulting Business?. That lifts full contribution margin from 73% to 83%, and EBITDA rises from $214K to $2429M in the provided model.

Margin drivers

- Keep advisory work high margin.

- Charge implementation separately.

- Watch recurring licensing costs.

- Protect gross margin with scope control.

Cost mix shift

- Software licensing drops 8% to 5%.

- Subcontractors drop 10% to 7%.

- Travel drops 5% to 3%.

- Storage drops 4% to 2%.

Want the six IoT consulting income drivers?

1

$250-$300/hrPricing Mix

Charging $250-$300 per hour, with more strategy and integration work, lifts revenue fast without much extra overhead.

2

8-40hBillable Capacity

Booking more of the 8-40 service hours per project turns fixed salaries into profit instead of idle time.

3

13 moAdvisory Retainers

Recurring advisory retainers smooth cash between projects and help the business reach payback in about 13 months.

4

73%-83%Delivery Margin

Keeping contribution margin (money left after direct project costs) in the 73%-83% band protects take-home pay from subcontractor and software spend.

5

$2.5K-$1.5KCAC Efficiency

Cutting CAC from $2,500 to $1,500 leaves more room for marketing to turn into paid projects and owner income.

6

$703KScope Control

Tighter scope keeps the minimum cash cushion near $703K and stops margin leaks from dragging down profit.

IoT Consulting Core Six Income Drivers

Pricing Power And Project Mix

Pricing Mix Drives Owner Pay

Owner income rises when more hours are sold in strategy, architecture, security, and implementation planning, not troubleshooting. Rates run from $200 to $300 per hour, so the same billable time can produce very different revenue. On 100 hours, that gap is $10,000 before delivery costs. One universal rate leaves money on the table.

Security Audit reaches $300 per hour by Year 5, while Strategy & Integration starts at $250 and reaches $275. Here’s the quick math: higher-rate work lifts gross profit and cash flow without adding the same extra delivery hours. The risk is simple: if low-value support crowds out advisory work, owner pay stalls.

Price by Service, Not One Rate

Track billable hours by service line, realized hourly rate, and troubleshooting share. If support work starts filling the calendar, it should be priced lower and capped, or it will pull time away from higher-rate advisory work. The goal is a mix that favors planning and security reviews, where the owner’s time earns the best return.

Use separate rates for each offer and document what is included. Measure the revenue per billable hour each month, then compare it with the service mix. If the team keeps one flat rate, high-value work gets underpriced and the owner pays for it in lower profit and weaker draw capacity.

- Track hours by service type.

- Separate advisory from troubleshooting.

- Review realized rate monthly.

- Cap low-value support work.

1

Billable Utilization And Capacity

Billable Utilization And Capacity

Billable utilization is paid client work divided by total work time. In this model, Year 1 service-hour assumptions are 40 hours for Strategy & Integration, 25 for Security Audit, 10 for Device Management, and 8 for Data Insights Platform.

By Year 5, those shift to 30, 20, 15, and 12 hours. That matters because owner income rises when delivery stays billable without crowding out sales, hiring, QA, and admin. If those nonbillable tasks get squeezed, revenue can grow while cash and profit stall.

Protect Paid Hours Before They Leak Away

Track billable hours, nonbillable hours, and hours by service line each week. The inputs that matter are client work, sales time, QA, admin, and hiring time, plus any backlog that delays delivery. Utilization = billable hours / total available hours.

Watch the mix, not just the headline rate. If Security Audit and Strategy & Integration stay booked, but owner time gets pulled into support and rework, take-home pay falls. Use caps on support, clear scopes, and scheduled sales time so paid delivery does not eat the hours needed to win the next job.

- Track hours by service line

- Separate billable and nonbillable work

- Protect sales and QA time

- Set weekly delivery caps

2

Recurring Advisory Revenue

Recurring Advisory Revenue

Recurring advisory revenue steadies owner pay when clients keep paying for roadmap governance, vendor coordination, security reviews, analytics reviews, and device-fleet oversight. The mix shifts over time: Device Management grows from 30% in Year 1 to 70% in Year 5, while the Data Insights Platform rises from 10% to 40%. That helps cash flow, but it is still service revenue, not pure software margin.

Here’s the quick math: owner income improves when monthly retainers cover delivery time, support, storage, and review work after direct costs. If those costs are ignored, the retainer looks richer than it is. The key input is monthly recurring clients times monthly fee, then subtract the labor and support needed to keep each account healthy. Stable revenue only helps if gross margin stays realistic.

Track Retainer Margin

Measure each retainer by hours, support load, and tool cost, not just by collected cash. A good file shows how much time goes to governance, device oversight, analytics, and security reviews, plus the monthly storage and support burden. If one account needs heavy review work, it can drain owner pay even when revenue is recurring.

- Track monthly retainer per client.

- Track delivery hours by service.

- Track storage and support costs.

- Track margin by client, not average.

Price to the workload mix, especially as Device Management climbs toward 70% and the Data Insights Platform reaches 40%. If those accounts start to need more support than planned, raise the fee or cut scope before cash flow slips. Retainers should fund owner pay after real delivery costs, not hide them.

3

Delivery Leverage And Subcontractor Margin

Subcontractor Margin

Subcontractors add delivery capacity, but they can quietly cut gross margin if your pricing does not fully cover their cost, software licenses, and rework. In this model, Third-Party Specialist Subcontractors run at 10% of revenue in Year 1 and 7% in Year 5, while software licensing adds another 8% to 5%.

What matters is the spread between client billings and delivery cost. Track subcontractor hours, billed revenue, license spend, and pass-through hardware separately. Hardware should sit outside consulting margin where possible, or it can make the practice look busier than it is and squeeze owner take-home pay.

Protect Delivery Margin

Price subcontracted work as a markup, not a cost pass-through. If a specialist is needed for security, integration, or analytics, the fee should cover labor, coordination, and profit. If it does not, the owner is buying revenue that pays less than it looks.

Use a simple check: subcontractor cost plus software licensing should stay well below project gross margin after employee payroll. Employees are separate from subcontractors, so do not hide internal labor inside vendor cost. Keep a clean line for pass-through hardware, then review margin by project, not just by top-line revenue.

- Track subcontractor cost as % revenue

- Separate hardware from consulting margin

- Review license spend every deal

- Test markup before scope starts

4

Client Acquisition Efficiency

Funded-Niche Acquisition

Owner income improves when the firm sells into funded niches and skips long unpaid sales cycles. Here’s the quick math: at $50K of marketing spend and $2,500 CAC, that supports about 20 marketing-acqui red clients a year. By Year 5, $600K of spend at $1,500 CAC implies about 400 clients. Better conversion lifts revenue without tying up as much cash.

The risk is weak pipeline quality. If the team chases unbudgeted deals, sales labor rises, utilization drops, and cash reserves thin out before payback. The key timing issue is the 13-month payback: if close rates slip or cycle time runs long, owner draws get delayed even when booked revenue looks strong. One clean rule: funded leads beat hopeful leads.

Track CAC by niche and payback

Measure acquisition by niche, not as one blended number. Track marketing spend, qualified leads, close rate, CAC, and months to payback for each target segment. For this model, the useful inputs are funded pipeline size, sales-cycle length, client count, and the cash needed to hold delivery staff before invoices catch up.

Cut unpaid work early. Use a simple filter: if the buyer has no budget, no timeline, or no owner, stop spending. Then compare each niche against the current benchmark of $2,500 CAC in Year 1 and $1,500 by Year 5. Push spend into the segments that reach payback fastest and keep sales time from crowding out delivery.

5

Scope Control And Margin Protection

Scope Control And Margin Protection

Scope creep turns good IoT consulting revenue into low-margin work fast. In this model, variable delivery costs are 27% of revenue in Year 1 and 17% in Year 5, so every $100k billed leaves $73k or $83k before fixed overhead and owner pay. One loose project can erase the margin from several clean ones.

The biggest leak is unpriced work around implementation complexity, device integration, and cybersecurity reviews. If the scope does not spell out hardware exclusions, cloud-cost limits, security-review boundaries, and support caps, extra hours show up as unpaid labor, slower billing, and weaker take-home income. One sentence in the contract can protect weeks of profit.

Price the edge cases before kickoff

Build every proposal from the real inputs: client sites, device count, integration points, review hours, support hours, cloud usage, and hardware pass-through. Price the hard parts before work starts, then use change orders for anything outside the signed scope. Milestone billing also helps cash flow by tying invoices to completed work, not open-ended effort.

- Exclude hardware from consulting margin.

- Cap cloud usage in writing.

- Set support hours per month.

- Approve change orders before extra work.

Track billed hours against approved hours, plus delivery cost as a percent of revenue. If a project is running above the 27% Year 1 cost pattern, stop and reprice before margin gets crushed. A single unpriced security review or device fix can turn strong revenue into break-even work.

6

Compare low, base, and high IoT consulting income scenarios

Owner income scenarios

Owner income rises fast as the model moves from Year 1 to Year 5, but cash needs stay heavy early. These cases show how $703K minimum cash and Month 6 break-even shape the plan.

| Scenario | Low CaseDownside case | Base CaseCore case | High CaseUpside case |

|---|---|---|---|

| Launch model | Early case with first-year scale and a modest owner draw. | Scaled operating case with Year 2 momentum and much higher owner benefit. | Mature case with the strongest owner benefit and full team capacity. |

| Typical setup | Year 1 uses $214K EBITDA, $180K CEO pay, 73% contribution margin, $500K payroll, and $50K marketing, with $703K minimum cash and Month 6 break-even. | Year 2 pairs $2.385M EBITDA with $2.565M pre-tax owner benefit as staffing, delivery, and service mix expand. | Year 5 uses $24.290M EBITDA and about $24.4M owner benefit as device management and data insights carry more of the mix. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $394KCash floor | $2.565MCore plan | $24.4MUpper bound |

| Best fit | Use this to stress-test launch-month cash and the gap before scale. | Use this as the main planning case if client wins and delivery stay steady. | Use this to test mature pricing, full staffing, and heavier device work. |

Planning note: Ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- IoT Consulting Porter's Five Forces Analysis

- IoT Consulting BCG Matrix

- IoT Consulting Business Model Canvas

- 7 Essential KPIs to Track IoT Consulting Profitability and Scale

- IoT Consulting Business Plan Template in Pre-Written Word

- 7 Strategies to Increase IoT Consulting Profitability and Scale Margins

- How Much Does It Cost To Run An IoT Consulting Firm Monthly?

- IoT Consulting Startup Costs: $165K CAPEX And $703K Cash Need

- IoT Consulting Financial Model Template in Excel

- How To Start An IoT Consulting Business In 6 To 12 Weeks

- Writing the IoT Consulting Business Plan: 7 Actionable Steps

- IoT Consulting Marketing Mix

- IoT Consulting Marketing Plan

- IoT Consulting Business Proposal

- IoT Consulting PESTEL Analysis

- IoT Consulting Pitch Deck Example Editable PPTX

- IoT Consulting Business SWOT Analysis

- IoT Consulting Value Proposition Canvas

Frequently Asked Questions

The provided model supports $180K in CEO salary from Year 1, plus possible profit distributions if cash allows If all EBITDA were available, pre-tax owner benefit would be $394K in Year 1 and $2565M in Year 2 Actual draws should wait until reserves, taxes, debt, and working capital are covered