Owner incomeY1 $2.6M

Owner incomeY1 $2.6MHow Much Intubation Mannequin Owners Can Make: $36M Year 1 Capacity

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeY1 $2.6M  Net margin50.1%

Net margin50.1% Revenue for target payY1 $5.18M

Revenue for target payY1 $5.18M Business difficultyHard

Business difficultyHard

You’re selling high-ticket medical training equipment, so revenue can look large before cash reaches the owner Under the researched first-year model, revenue is $518M, gross margin is 816%, and contribution after listed sales, shipping, and marketing costs is $358M before fixed overhead, inventory reserves, taxes, debt service, and distributions

Owner incomeY1 $2.6MNet margin50.1%Revenue for target payY1 $5.18MBusiness difficultyHardWant to test your owner-pay number?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margin, payroll, taxes, debt, and reinvestment.

Want to pressure-test owner income?

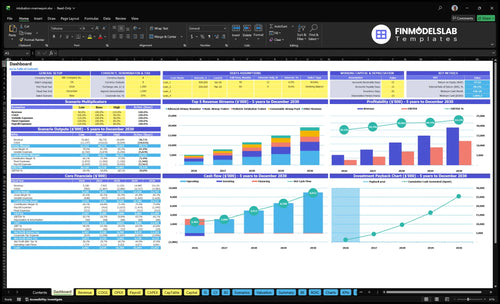

The dashboard in the Intubation Training Mannequin Sales Financial Model Template shows revenue, gross margin, contribution, cash flow, and owner-pay outputs. It also uses assumptions for unit volume, sale price, COGS, commissions, shipping, marketing, and reserves; open it to test lean, base, and high cases.

Owner-income model highlights

- Owner-pay capacity

- Revenue and margin

- Scenario-based ramp

Can an intubation mannequin sales business owner make more by scaling?

Yes—scale can lift owner income in Intubation Training Mannequin Sales, but only if volume, gross margin, and cash timing stay tight. Revenue rises from $518M in Year 1 to $1,499M in Year 4, while contribution before fixed overhead grows from $358M to $1,079M. The catch is simple: more sales reps, distributor deals, SKUs, and bigger purchase orders can trap cash, while direct institutional sales usually protect margin and distributors can add volume but cut take-home per order.

What helps

- Direct sales protect margin.

- Revenue reaches $1,499M by Year 4.

- Contribution reaches $1,079M.

- Keep cash tied up low.

What hurts

- More sales reps add overhead.

- Distributors can cut take-home.

- More SKUs need more stock.

- Larger orders use more cash.

How much revenue is needed to pay an intubation mannequin business owner?

Work backward from the owner’s pay target. Using Year 1 results of $358M contribution on $518M revenue, the implied contribution margin is about 69.1%, so each $100k of owner-pay capacity needs about $145k of revenue before fixed overhead, inventory reserves, and warranty reserves.

Owner pay math

- $358M contribution on $518M revenue

- Implied margin: about 69.1%

- $100k owner pay needs about $145k revenue

- Use revenue target, not profit alone

What to add in

- Add fixed overhead first

- Add inventory reserve next

- Add warranty reserve too

- Then divide by contribution margin

What profit margin do intubation training mannequins have?

If you’re pricing Intubation Training Mannequin Sales, the provided Year 1 gross margin is 816%, but that is a model figure, not a universal market margin. The real margin shifts by product mix and by unit costs like $177 plus 32% for the Basic Airway Trainer, and the planning math is here: How Do I Write A Business Plan To Launch Intubation Training Mannequin Sales?

Gross margin inputs

- Basic Airway Trainer: $177 plus 32%

- Advanced Airway Simulator: $670 plus 45%

- Pediatric Intubation Trainer: $295 plus 38%

- Neonatal Care Model: $282 plus 47%

Net margin drag

- Consumable Airway Pack: $29 plus 50%

- Commissions cut take-home.

- Freight, marketing, discounts add drag.

- Warranty replacements and distributor margin hit net.

Want to see what moves owner income most?

1

$5.18MOrder Volume

Year 1 revenue is $5.18M, so more units sold spreads fixed plant and salary costs across more orders and lifts owner take-home.

2

$849Product Mix

The year 1 blended selling price is about $849 per unit, but the $4.5K to $4.8K simulators drive most of the dollars, so mix changes cash fast.

3

81.6%Gross Margin

After production costs, about 81.6% of revenue stays to cover selling and overhead, so small COGS swings move profit fast.

4

12.5%Channel Mix

Commissions, shipping, and lead gen take 12.5% of revenue in year 1, so tighter direct sales and freight control raise take-home.

5

$1.0MCash Cycle

Minimum cash lands near $1.0M in Month 2, so slow inventory turns can trap cash and delay owner distributions.

6

$312KOverhead

Fixed overhead runs about $312K a year, so lean staffing and facility costs flow straight into EBITDA and owner draw.

Intubation Training Mannequin Sales Core Six Income Drivers

Order Volume

Institutional Order Volume

Income starts with qualified institutional demand. Year 1 volume is 6,100 units across 1,200 Basic Airway Trainers, 400 Advanced Airway Simulators, 300 Pediatric Intubation Trainers, 200 Neonatal Care Models, and 4,000 Consumable Airway Packs, or about 508 units a month. More signed purchase orders (POs) lift revenue and contribution, but only if inventory, freight, and selling time stay controlled.

The risk is lumpy buying. A few nursing schools, EMS programs, hospitals, and simulation centers can place big orders, then go quiet. That makes cash flow uneven, so the owner’s take-home pay depends on steady conversion of qualified leads into shipped units, not just a strong yearly forecast.

Track PO Pipeline and Ship Dates

Measure order volume by qualified institutions, units per PO, and days from quote to payment. Here’s the quick math: if monthly units stay near 508 and mix holds, revenue follows demand. If a few large orders slip by a month, owner income drops fast even when the annual plan still looks fine.

Use a simple control list:

- Track open POs by month

- Flag orders above normal size

- Match stock to forecasted units

- Watch shipping and sales costs per order

- Collect deposits on large institutional deals

1

Average Order Value And Product Mix

Product Mix Drives AOV

AOV, or average order value, is the dollars per order. Here, mix moves revenue fast: 400 Advanced Airway Simulators at $4,500 each bring $1.8M, while 4,000 Consumable Airway Packs at $150 each bring $600k. The listed Year 1 mix totals $5.18M across five SKUs.

Higher-priced orders can raise owner pay, but only if support, freight, discounting, and warranty work stay in line. The inputs are unit price, units sold, mix by SKU, and order size. If a bigger bundle needs more demos or installs, revenue rises faster than profit unless gross margin holds.

Price the Mix, Not Just the Unit

Track revenue per order, units per order, and gross margin by SKU. Compare schools, hospitals, and simulation centers, since institutional buyers may take multi-unit quotes. Set a discount floor before bundling, so you do not trade a bigger ticket for weaker contribution.

Price the sales work too. If a high-ticket model needs long selling time or extra training, build that into the quote or the service plan. One clean test: if the added margin does not cover extra freight, setup, and support, the order is bigger on paper but not on owner draw.

2

Gross Margin

Gross Margin

Gross margin is the biggest bridge from sales to owner pay. With $518M of Year 1 revenue and $9.538M of COGS, blended gross margin is 81.6% before overhead. That leaves about $508.5M to cover sales costs, admin, inventory drag, and profit draw, so even small margin leaks matter fast.

Here’s the quick math: one margin point on $518M is about $518k. So discounts, warranty replacements, freight-in, or supplier price hikes can cut owner income hard, especially when product COGS already includes unit costs plus revenue-based production costs.

Protect Margin

Track margin by SKU, not just at the company level. The Advanced Airway Simulator carries $670 unit COGS plus 45% revenue-based COGS, while the Consumable Airway Pack has $29 unit COGS plus 50%. That mix can look strong on revenue but still leak cash if fulfillment or replacements rise.

Watch discount rate, freight-in, warranty rate, and supplier quotes each month. If blended gross margin slips by 1 point, owner income can fall by about $518k at this revenue base. Keep pricing floors, approve exceptions, and test whether bundles still hold margin after production and shipping are fully loaded.

3

Channel Mix

Channel Mix

Channel mix is the split between direct institutional sales and distributor or dealer sales. Direct sales can keep more gross profit per order, but they also carry commissions, lead generation, support, and procurement follow-up. With commissions at 50% of Year 1 revenue and 45% by Year 4, the real issue is not just volume; it’s how much cash stays after selling costs.

Here’s the quick math: if a channel grows revenue but payment is slow or repeat orders are weak, owner take-home can still fall. Distributors can widen reach, but they may cut margin and delay cash. So the best mix is the one with the strongest contribution margin, fastest payment timing, and highest repeat order value.

Track Margin by Channel

Measure each channel separately: revenue, commission rate, support time, days to collect cash, and repeat order rate. A channel that looks big can still be weak if it needs heavy follow-up or slow procurement. That’s where owner pay gets squeezed.

Test one clean rule: keep the channel that leaves the most cash after selling costs. If direct sales close faster and pay sooner, favor them. If distributors bring larger institutional orders, keep them only when the extra volume beats the lower margin and slower payment.

4

Inventory Cash Cycle

Inventory Cash Cycle

When cash gets stuck in stock, owner pay gets squeezed even if sales look strong. This business needs 2,100 mannequin units and 4,000 consumable packs in Year 1, so the cash conversion cycle matters: how long money stays tied up before it comes back from customers.

Inventory carrying costs also hit margin. Inventory management labor adds 15%, warehouse overhead adds 20%, barcoding logistics adds 4%, and consumable bulk storage adds 6%. Slow-moving SKUs and minimum order rules can trap cash, delay distributions, and force the owner to wait for cash, not just profit.

Control Reorder Timing

Track cash tied up by SKU, supplier minimums, and days on hand. If a model moves slowly, cut the next buy or negotiate smaller batches so cash is not locked in units that sit too long.

- Watch days on hand by SKU.

- Set reorder points from sales pace.

- Negotiate smaller supplier batches.

- Separate fast and slow movers.

Better terms and tighter reorder points protect owner draws because cash turns faster. One clean rule: do not restock just because a minimum order looks cheap if it pushes cash into dead stock.

5

Operating Overhead

Operating Overhead

Operating overhead is the spend that sits below gross profit, like warehouse rent, sales payroll, website systems, trade shows, customer support, admin, returns, and warranty handling. Here, the disclosed Year 1 variable selling costs total 125% of revenue: 50% commissions, 35% shipping and logistics, and 40% marketing and lead gen. At that le vel, sales do not leave room for owner pay unless the model is rechecked.

The key inputs are revenue, order volume, cash collection timing, and any fixed overhead you add separately. One clean rule: if overhead grows faster than repeat orders, profit shrinks fast. Scaling headcount before repeat purchase volume is proven is the trap, because it turns booked sales into thin or negative contribution.

Keep Fixed Costs Tied to Orders

Track overhead as a % of revenue and as cost per order. Here’s the quick math: 125% variable selling cost means each $1 of sales carries $1.25 of selling expense before fixed overhead, so you need either better pricing, lower channel costs, or a different mix. The owner’s draw only works if cash comes in fast and support costs stay lean.

Test staffing and spend against order density and repeat purchase rate. Keep sales payroll, support, and trade-show spend tied to collected cash, not booked orders. Watch for return and warranty work early; those costs can erase margin fast in a durable goods model.

- Measure overhead per order monthly

- Hold headcount until repeat orders prove out

- Match marketing spend to cash collected

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income changes with volume, mix, and selling costs. Higher sales can still leave less cash for the owner if inventory, payroll, or receivables absorb more working capital.

| Scenario | Low CaseDownside case | Base CaseCore case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lower-earnings case, where demand and margin stay soft. | This is the modeled core case, with Year 1 revenue at $5.18M and EBITDA at $2.60M. | This is the stronger scale case, with Year 4 revenue at $14.99M and EBITDA at $9.06M. |

| Typical setup | Sales lean toward basic units, growth is slower, and higher commissions, shipping, and marketing take a bigger share of revenue. | A mixed product plan supports 81.6% gross margin, 12.5% variable selling costs, and $3.58M of contribution before fixed overhead and reserves. | Later scale lifts volume and trims selling costs to 9.8%, but inventory, payroll, distributors, and payment timing can still hold back take-home cash. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $2.6MLow income band | $2.6M - $6.9MBase income band | $9.1M - $12.3MHigh income band |

| Best fit | Use this to test downside cash needs if sales ramp slowly or payments come late. | Use this as the main operating plan for budgeting, hiring, and owner draw decisions. | Use this to test upside capacity if growth stays fast and cash stays tightly managed. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or owner distributions.

Related Products

- Intubation Training Mannequin Sales Porter's Five Forces Analysis

- Intubation Training Mannequin Sales BCG Matrix

- Intubation Training Mannequin Sales Business Model Canvas

- What Are The 5 KPIs For Intubation Training Mannequin Sales Business?

- Intubation Training Mannequin Business Plan Template in Pre-Written Word

- How Increase Intubation Training Mannequin Sales Profitability?

- What Are Operating Costs For Intubation Training Mannequin Sales?

- Cost to Start Intubation Mannequin Sales: $518M Year 1 Plan

- Intubation Training Mannequin Sales Financial Model Template in Excel

- How To Open An Intubation Training Mannequin Sales Business In 6–12 Weeks

- How Do I Write A Business Plan To Launch Intubation Training Mannequin Sales?

- Intubation Training Mannequin Sales Marketing Mix

- Intubation Training Mannequin Sales Marketing Plan

- Intubation Training Mannequin Sales Business Proposal

- Intubation Training Mannequin Sales PESTEL Analysis

- Intubation Training Mannequin Sales Pitch Deck Example Editable PPTX

- Intubation Training Mannequin Sales Business SWOT Analysis

- Intubation Training Mannequin Sales Value Proposition Canvas

Frequently Asked Questions

Revenue is the top line, not the owner’s paycheck In the researched Year 1 model, revenue is $518M, gross profit is $423M, and contribution after listed commissions, shipping, and marketing is $358M Owner income comes after fixed overhead, inventory reserves, taxes, financing, and reinvestment