Owner income$150k base

Owner income$150k baseHow Much Does an Inventory Management Software Owner Make at $150k?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k base  Net margin-44% to 81%

Net margin-44% to 81% Revenue for target pay$363k ARR

Revenue for target pay$363k ARR Business difficultyHard

Business difficultyHard

Key Takeaways

- Paid accounts fund recurring revenue and owner pay.

- Higher ARPA lifts revenue without huge customer growth.

- Churn control protects MRR, EBITDA, and distributions.

- Lower CAC and gross margin improve cash for owners.

Owner income$150k baseNet margin-44% to 81%Revenue for target pay$363k ARRBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, operating costs, reserves, and target owner pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

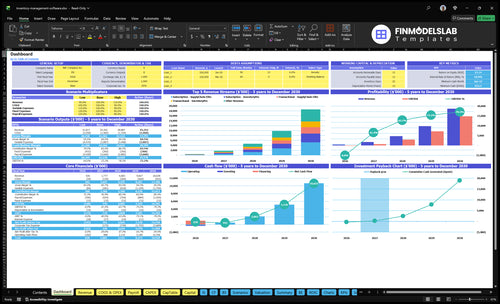

Want to check owner income in the Inventory Management Software model?

Yes—this Inventory Management Software Financial Model Template screenshot shows revenue, EBITDA, cash need, payback, breakeven, and owner-income outputs; open the model.

Owner-income model highlights

- Owner take-home output

- Revenue and EBITDA

- Assumptions and scenarios

How many customers does inventory management software need to pay the owner?

Inventory Management Software does not have one universal customer count. Using the Year 2 math here, weighted ARPA is about $215/month before churn, and contribution after COGS, commissions, and payment fees is about $183 per customer per month, so a $150,000 owner salary needs about 68 full-year customers. If you also cover Year 2 fixed overhead, non-owner payroll, and marketing, the need rises to about 315 full-year customers before reserves, and churn pushes that number higher.

Owner pay math

- $215 monthly ARPA before churn

- $183 contribution per customer per month

- $150,000 salary needs about 68 customers

- Churn raises the needed count

Full-cost math

- 315 full-year customers covers full Year 2 load

- Includes overhead, payroll, and marketing

- Before reserves, not after them

- Model by scenario, not one count

Does an inventory management software owner make more by staying lean or hiring a team?

If cash is tight, stay lean. In Inventory Management Software, payroll rises from $342,500 in Year 1 to $815,000 in Year 5, and marketing rises from $50,000 to $750,000, so hiring cuts near-term owner cash even as EBITDA improves from -$160,000 in Year 1 to positive by Year 5 as pricing mix, CAC, conversion, and scale improve. This is a tradeoff, not a lifestyle call.

Stay lean

- Protect founder cash first

- Keep payroll growth slower

- Delay hires until demand proves it

- Use a small support stack

Hire to scale

- Hire when sales gets efficient

- Add support as tickets rise

- Spend more on marketing only with conversion

- Grow staff when EBITDA can absorb it

What costs reduce inventory management software owner income?

The main drag on Inventory Management Software owner income is cost structure: service delivery eats revenue first, then operating expenses squeeze what’s left. For launch budgeting, see How Much Does It Cost To Open And Launch Your Inventory Management Software Business?. Here’s the quick math: cloud hosting runs at 50% to 30% of revenue, third-party APIs at 30% to 20%, payment processing at 20% to 16%, and support payroll can range from $27,500 to $110,000.

Then operating costs cut deeper: sales commissions at 60% to 40%, marketing from $50,000 to $750,000, wages from $342,500 to $815,000, and fixed overhead of $72,000 reduce EBITDA and delay distributions.

Service delivery costs

- Cloud hosting: 50% to 30% of revenue

- Third-party APIs: 30% to 20%

- Payment processing: 20% to 16%

- Support payroll: $27,500 to $110,000

Operating expenses

- Sales commissions: 60% to 40%

- Marketing: $50,000 to $750,000

- Wages: $342,500 to $815,000

- Fixed overhead: $72,000

Want the six owner-income drivers?

1

$62K-$3.7MPaid MRR

More paid accounts turn acquisition spend into monthly recurring revenue (MRR), and that base can climb from about $62K to $3.7M a month as CAC and conversion improve.

2

$187-$399ARPA

Higher account revenue per user lifts income from each customer, so the same base earns more without adding the same amount of support work.

3

20%-35%Retention

Trial-to-paid conversion rising from 20% to 35% keeps more signups from leaking out, which boosts paid volume and shortens payback.

4

$150-$80CAC Efficiency

Customer acquisition cost falls from $150 to $80, so each marketing dollar buys more users and supports faster scale.

5

8%-5.6%Gross Margin

Hosting, APIs, commissions, and payment fees run at about 8% of revenue in Year 1 and about 5.6% by Year 5, so more sales drop to profit.

6

$342K-$815KPayroll Load

Payroll rises from $342.5K to $815K as product, sales, support, and marketing staff grow, and EBITDA still moves from -$160K to $14.8M if revenue outpaces labor.

Inventory Management Software Core Six Income Drivers

Paying Customers And MRR

Paying Customers and MRR

Monthly recurring revenue (MRR) comes from paying accounts, not free trials or website traffic. If marketing budget divided by CAC (customer acquisition cost) implies about 333 customers in Year 1, 1,154 in Year 2, and 9,375 in Year 5 before churn, the real question is how many convert into paid plans fast enough to fund owner pay.

Here’s the quick math: more paid accounts lift MRR, which improves cash flow and makes a $150,000 owner salary easier to support. The main inputs are paid accounts, trial-to-paid conversion, CAC, and churn. If conversion rises from 200% to 350%, the same lead flow turns into more recurring revenue and less pressure on new sales every month.

Track Paid Conversions, Not Traffic

Measure trial-to-paid conversion, logo churn (customer cancellations), and MRR per paid account each month. A bigger funnel only helps if paid accounts grow and stay active. If trials are busy but paid seats stall, MRR stays thin and owner draws get harder to fund.

Use CAC payback and cohort retention to test whether growth is healthy. More qualified paid accounts raise recurring revenue quality, but weak onboarding or slow activation can erase the gain. If onboarding takes too long, churn risk rises and every new customer has to replace lost MRR before profit reaches the owner.

1

Average Revenue Per Account

Average Revenue Per Account

Higher ARPA means each paying account brings in more monthly revenue, so the owner needs fewer customers to support pay. For this inventory software model, weighted monthly ARPA from subscription plus usage is about $187 in Year 1, $215 in Year 2, and $399 in Year 5. That gap matters because it lifts MRR without the same jump in account count.

ARPA comes from tiered plans, more users, more warehouse locations, integrations, usage-based transactions, and premium support. The catch is simple: if ARPA rises only because prices rise, retention has to hold or the extra revenue leaks out through churn and support load. One clean line: more revenue per account makes owner draw easier to fund.

Raise ARPA Without Breaking Retention

Track ARPA by cohort and by plan mix, not just in one monthly average. Use the formula monthly subscription revenue + usage revenue divided by paying accounts. Then watch the inputs that move it: users per account, warehouse locations, integrations, transaction volume, and premium support attach rate. If those rise and churn stays flat, owner cash flow improves.

Test upgrades on real accounts before pushing price. A 10% ARPA lift across the base is worth more than chasing new logos, but only if support tickets, renewals, and revenue churn stay controlled. If larger plans add service work faster than revenue, gross margin drops and the owner’s take-home gets tighter, even when top-line MRR looks better.

2

Churn And Retention

Churn And Retention

Churn means customers cancel and monthly recurring revenue (MRR) drops. For this software model, make churn an editable assumption, not a fixed rate. Track logo churn and revenue churn, because lost accounts force replacement sales before growth shows up in owner pay.

Here’s the quick math: retained MRR supports margin, cash flow, and distributions; churned MRR does the opposite. If cancellations rise, CAC payback stretches, support work repeats, and EBITDA available for owner draws falls. Growth only counts when new and expansion MRR beat churn.

Track Retention Before You Scale Sales

Measure logo churn, revenue churn, and expansion revenue by cohort, plan, and channel count. Use renewal dates, support tickets, and onboarding time to spot where cancellations start. If one segment churns after setup, fix training and implementation before spending more on acquisition.

Use upsells from more users, more locations, and more integrations to offset losses. A simple rule: if retained accounts add more MRR than canceled accounts remove, owner income gets steadier. If not, the business is paying to refill a leaky bucket.

3

Customer Acquisition Cost And Sales Efficiency

Customer Acquisition Cost

CAC, or customer acquisition cost, is the cash needed to win one paying account. In this model, CAC improves from $150 in Year 1 to $80 in Year 5, even as marketing spend rises from $50,000 to $750,000. That means growth can scale, but only if each new customer costs less to win than the gross profit it brings in.

High CAC slows owner pay because cash gets burned before revenue matures. Sales commissions also matter: falling from 60% to 40% of revenue improves sales efficiency, but only if trial conversion, paid conversion, demos, onboarding, and payback period stay tight. If payback stretches, ARR can rise while distributions to the owner stay delayed.

Measure CAC by channel and stage

Track CAC as marketing spend + sales commissions + onboarding cost, divided by new paying customers. Then split it by channel, because paid search, outbound, partner sales, and demos rarely perform the same. A lower CAC with faster payback gives the owner more free cash for salary or draws; a higher CAC does the opposite.

- Track spend by channel

- Measure demo-to-paid close rate

- Watch onboarding time to activation

- Compare CAC to first-year gross profit

- Set a payback target by cohort

Use the funnel to find leaks: better trial conversion, cleaner demos, and faster onboarding often cut CAC faster than ad cuts do. If commissions stay at 60% of revenue, CAC stays heavy; moving toward 40% frees more cash for profit and owner pay, even before revenue growth slows.

4

Gross Margin And Service Delivery Costs

Gross Margin on Service Delivery

Gross margin is what’s left after you pay to deliver the software. Here that means hosting, APIs, payment processing, and support labor. In the model, hosting drops from 50% to 30% of revenue, APIs from 30% to 20%, and payment processing from 20% to 16%. Th at mix lifts EBITDA and makes owner distributions easier.

The catch is support payroll rises from $27,500 to $110,000, so margin still depends on workload. Barcode scans, integrations, API calls, database usage, and support tickets all drive service cost. More volume can help revenue, but if each account creates too many tickets or scans, take-home pay gets squeezed fast.

Track Cost Per Account

Measure gross margin by customer tier, not just company-wide. The key inputs are revenue, hosting cost, API usage, payment fees, and support payroll. Also track barcode scans, integrations, API calls, and support tickets per account so you can see which clients consume profit and which ones fund owner pay.

Here’s the quick math: if a feature-heavy customer drives low ticket volume and low usage cost, margin stays strong; if usage rises faster than subscription price, EBITDA drops. Set alerts when support time or API load spikes, and price high-use plans so gross margin stays wide enough to cover fixed costs and still leave cash for the owner.

5

Staffing, Development, And Owner Role

Staffing And Founder Pay

Staffing is a cash decision, not just a people decision. In this model, payroll rises from $342,500 in Year 1 to $815,000 in Year 5, a jump of $472,500 or about 138%. Developers protect the product, support protects retention, and sales expands pipeline, but each hire lowers near-term owner cash unless paid accounts, ARPA, and retention grow with it.

The owner’s pay is the squeeze point. The CEO Product Lead role still needs funding, so hiring only works when recurring revenue can carry the extra fixed cost. If staffing grows faster than MRR, cash flow tightens and owner take-home drops. If the team improves uptime, closes more deals, and cuts churn, payroll can scale without starving distributions.

Hire To Support Revenue, Not Vanity Headcount

Track payroll by function, MRR per employee, support tickets per rep, and pipeline per seller. Those four inputs show whether each hire is earning its keep. One clean test: if a role does not improve product stability, retention, or booked revenue within the forecast window, it is raising owner risk instead of owner income.

- Protect developers when bugs hurt retention.

- Add support when tickets delay renewals.

- Expand sales when pipeline is thin.

- Delay hires if cash payback lags.

Use a simple rule: hire only when added recurring revenue can cover the new salary and still leave room for owner pay. If revenue holds but retention slips, payroll becomes a drag fast, because you keep paying for growth while replacing lost accounts.

6

Compare lean, base, and growth owner-income scenarios

Owner income scenarios

Owner income moves from salary-only to distribution-capable as revenue scales and mix shifts toward higher-priced plans.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path, with Year 1 still negative at the EBITDA line. | This is the modeled path, where scale turns EBITDA positive and owner cash room opens. | This is the stronger earnings path, where mature scale creates the most owner distribution capacity. |

| Typical setup | Year 1 lands at about $363,000 implied revenue, $187 ARPA, 333 acquired customers before churn, 84% contribution, and -$160,000 EBITDA, so owner income is salary-only. | Year 2 reaches about $1.672 million revenue, $215 ARPA, 1,154 acquired customers before churn, 85.3% contribution, and $735,000 EBITDA, so owner income is reserves-first. | Year 5 reaches about $18.365 million revenue, $399 ARPA, 9,375 acquired customers before churn, 89.4% contribution, and $14.781 million EBITDA, so owner income has the most upside after reinvestment and obligations. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $150,000 salary onlyLow Case | Salary plus limited drawBase Case | Post-tax distribution roomHigh Case |

| Best fit | Use this to stress-test the first year when distribution capacity is zero. | Use this for the likely operating plan once the business clears break-even and starts building reserves. | Use this to test upside after taxes, reserves, reinvestment, debt, and investor terms. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Inventory Management Software Porter's Five Forces Analysis

- Inventory Management Software BCG Matrix

- Inventory Management Software Business Model Canvas

- 7 Essential SaaS Metrics for Inventory Management Software Growth

- Inventory Management Software Business Plan Template in Pre-Written Word

- How to Increase Inventory Management Software Profitability

- What Are the Monthly Running Costs for Inventory Management Software?

- Inventory Management Software Startup Costs: $465K+ First-Year Budget

- Inventory Management Software Financial Model Template in Excel

- How To Start An Inventory Management Software Business In 3 To 9 Months

- How to Write an Inventory Management Software Business Plan

- Inventory Management Software Marketing Mix

- Inventory Management Software Marketing Plan

- Inventory Management Software Business Proposal

- Inventory Management Software PESTEL Analysis

- Inventory Management Software Pitch Deck Example Editable PPTX

- Inventory Management Software Business SWOT Analysis

- Inventory Management Software Value Proposition Canvas

Frequently Asked Questions

The model includes $150,000 annual CEO pay, but distributions depend on cash flow EBITDA is -$160,000 in Year 1, then $735,000 in Year 2 after Month 13 breakeven By Year 5, EBITDA reaches $14781 million before taxes, reserves, debt service, reinvestment, and investor payouts