Owner income$223k to $378M

Owner income$223k to $378MHow Much Does an Investment Platform Owner Make? 5-Year Income View

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$223k to $378M  Net margin34% to 648%

Net margin34% to 648% Revenue for target pay$55.0M

Revenue for target pay$55.0M Business difficultyHard

Business difficultyHard

An investment platform owner can make little or nothing early if cash is held for compliance, growth, and reserves In the researched assumptions, the business produces about $66 million of Year 1 revenue, 920% gross margin, and about $223,000 of EBITDA-like profit before taxes, reserves, reinvestment, and owner pay By Year 5, revenue reaches about $583 million, gross margin reaches 946%, and the pre-reserve profit pool is about $378 million These are planning assumptions, not guaranteed salary or distribution figures

Owner income$223k to $378MNet margin34% to 648%Revenue for target pay$55.0MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Not guaranteed salary, tax advice, or owner distribution advice.

Need the full model view for owner income?

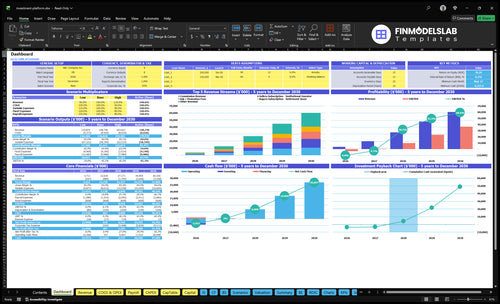

This dashboard shows revenue, gross margin, EBITDA-like profit, runway, and owner take-home assumptions; open the Investment Platform Financial Model Template for the full view.

Owner-income model highlights

- Retained cash and reserves

- Reinvestment and distributions

- Scenario checks: $66M to $583M

How many customers does an investment platform need to pay the owner?

For an Investment Platform, there is no single customer count that pays the owner; it depends on funded accounts, average order value, repeat activity, subscription mix, CAC (customer acquisition cost), and fixed operating costs. In the Year 1 model, 20,000 acquired buyers and 1,250 acquired sellers produce about $66 million of revenue and $223,000 of pre-reserve operating profit. So owner pay should be modeled after acquisition spend and reserves, not revenue alone.

What drives pay

- Funded accounts set scale

- Repeat activity lifts revenue

- Subscriptions smooth cash flow

- Fixed costs cap owner pay

Year 1 math

- 20,000 buyers acquired

- 1,250 sellers acquired

- $150 buyer CAC

- $1,200 seller CAC

How much can an investment platform founder make?

An Investment Platform founder usually has limited early cash income: Year 1 shows $66 million revenue but only about $223,000 of EBITDA-like profit after $45 million acquisition spend, fixed costs, COGS, and variable expenses. For the operating KPI behind that spread, see What Is The Main Indicator Of Success For Your Investment Platform?; by Year 5, the pre-reserve profit pool reaches about $378 million, but take-home depends on salary, distributions, reserves, and reinvestment.

Early cash limits

- Protect licensing support first

- Fund compliance and cybersecurity

- Keep engineering spend active

- Expect thin Year 1 profit

Founder upside

- Separate salary from distributions

- Track retained cash monthly

- Value equity apart from cash

- Set reserves before payouts

What affects investment platform profit margins?

Investment Platform margins are driven by market data feeds, trade execution, payment processing, compliance/legal, CAC (customer acquisition cost), cybersecurity, infrastructure, software licenses, and support. If you want the launch budget behind that math, see How Much Does It Cost To Launch Your Investment Platform Business? because fixed costs can start at $58,000/month. COGS (cost of goods sold) can fall from 80% of revenue in Year 1 to 54% in Year 5, while variable expenses can drop from 100% to 60%; this is business economics, not legal advice.

Biggest Levers

- Market data feeds raise base cost.

- Execution and payment fees squeeze spread.

- CAC can overwhelm early margins.

- Support load grows with active users.

Cost Shape

- Year 1 COGS can hit 80%.

- Year 5 COGS can fall to 54%.

- Variable expenses can drop to 60%.

- Cloud, licenses, legal, cybersecurity total $58,000 monthly.

Want the six main income drivers?

1

20K/1.25KFunded Accounts

Year 1 starts with 20,000 buyers and 1,250 sellers, so account scale is the main engine behind fee revenue.

2

$1.5K-$7KAccount Value

Higher order values lift commission dollars and subscription value, with retirement savers at the top of the range.

3

$2+0.25%Monetization Mix

The platform earns from a $2 trade fee, a 0.25% variable fee, and monthly subscriptions, so income rises with each active account.

4

1.0-5.5xTrading Activity

Repeat orders matter because growth investors go from 4.0 to 5.5 orders per account, and more activity lifts revenue without much extra fixed cost.

5

$150->$85Acquisition Cost

Buyer CAC falls from $150 to $85 and seller CAC from $1,200 to $650, so the marketing budget buys more funded accounts.

6

$1.77MFixed Overhead

About $1.77M of Year 1 fixed spend sits ahead of profit, so control of compliance, cloud, software, and staff costs speeds take-home cash.

Investment Platform Core Six Income Drivers

Funded account growth and activation

Funded Account Activation

Registered users are not the same as funded accounts. Only users who deposit and start trading become revenue-generating customers, so downloads without funding do not pay the owner. In Year 1, $30 million of buyer marketing at $150 CAC creates 20,000 buyers; $15 million of seller marketing at $1,200 CAC creates 1,250 sellers.

This driver lifts subscriptions, commissions, trading activity, cash economics, and future asset growth. By Year 5, the annual assumption reaches 105,882 buyers and 6,462 sellers acquired. If funding and activation lag, CAC is paid up front but owner income comes later, or not at all.

Measure Funding, Not Just Signups

Track registered users, funded accounts, active accounts, and the time from signup to first deposit. The key ratio is funded accounts divided by registrations. That tells you whether marketing is buying real customers or just app installs.

Also watch first trade rate and repeat activity by buyer and seller segment. If activation is weak, subscriptions and commission revenue stay thin, while compliance and support costs still run. That squeezes cash flow and delays owner pay.

- Separate signups from funded accounts

- Track first deposit speed

- Track first trade conversion

- Track active users by segment

1

Assets under management and average account balance

Assets Under Management and Average Account Balance

AUM, or assets under management, is the dollar value of client assets on the platform. It only improves owner income when the revenue model turns balances into fees, cash balance income, or premium services. If the platform cannot monetize balances, bigger accounts just mean more support and compliance work.

By segment, the benchmark order values are $1,500-$2,500 for retail investors, $3,000-$5,000 for growth investors, and $5,000-$7,000 for retirement savers. Higher balances can lift recurring revenue, but they are not a guaranteed fee base, so low monetization can leave profit and owner pay under pressure.

Measure Balance Quality, Not Just Balance Size

Track funded accounts, segment mix, average balance, and which fee path each account uses. Separate users who trade, subscribe, or buy premium tools from users who only register. Use AUM as a model input, not a promise, because the same balance can produce very different revenue depending on pricing and product fit.

- Track balance by customer segment

- Measure fee yield per account

- Watch support cost per funded account

- Check if balances cover compliance

2

Monetization mix across revenue streams

Monetization Mix

This revenue driver is the split between subscriptions, fixed commissions, variable commissions, premium tools, and promoted placement fees. The owner’s income rises when the mix shifts toward recurring fees and high-margin add-ons, because revenue is less tied to trading volume alone. Here’s the quick math: buyer subscription is $1,450 monthly, seller subscription is $10,650 monthly, fixed commission is $2 per order, and variable commission starts at 0.25% of order value in Year 1.

That mix matters because the commission rate falls to 0.15% by Year 5, so subscription and tool attach rate need to carry more of the profit load. Not every platform can use every revenue method, so the real input is which features are allowed, which customer segment pays, and how often they trade. If premium tools and subscriptions are weak, owner pay gets squeezed even when account counts look good.

Measure Fee Yield

Track revenue per funded buyer, revenue per seller, and commission per order. Those three numbers show whether the mix is improving or just shifting work onto support and compliance. One clean check: subscriptions should cover a big share of fixed cost before you rely on trading activity. If order count drops, the 0.15% to 0.25% take-rate change can hit cash fast.

Test attach rates for premium tools and promoted placement fees by segment, then forecast monthly cash by customer type. Watch how many buyers stay at $1,450 and how many sellers stay at $10,650 after onboarding. If a stream needs extra service or regulatory work, treat that cost as part of margin, not an afterthought.

- Track funded accounts, not downloads.

- Price by segment and activity.

- Separate recurring from usage revenue.

- Test premium tool attach rates monthly.

- Watch commission yield as rates fall.

3

Trading, cash, and activity sensitivity

Trading activity revenue

When trading rises, revenue rises faster than account count. In Year 1, 53,000 orders and $1.2 billion of order value create $406,000 of commission revenue; by Year 5, 444,706 orders and $187 billion support about $37 million. That spread shows why owner income depends on activity, not just funded users.

The main inputs are order count, average order value, commission rate, idle cash assumptions, margin lending, and partner agreements. Product design, regulation, market rates, and customer behavior can push this driver up or down fast, so cash flow and owner pay can swing even when account growth looks fine.

Track orders and take-rate

Measure orders per active account, average order value, and take-rate every month. Here’s the quick math: commission revenue = orders × average order value × take-rate. If activity slows, revenue drops before headcount does, so the forecast should track trade frequency by cohort, not just total signups.

Track funded and active accounts separately.

Watch idle cash yield by rate cycle.

Test margin and partner fee income.

Push the features that lift repeat trading without adding too much support or risk cost. If regulation or market rates change, reset the cash and margin assumptions fast. That keeps profit, free cash flow, and the owner’s draw tied to real activity, not stale plan numbers.

4

Acquisition cost and retention efficiency

CAC and Retention

Owner income rises when cost to acquire a funded customer falls and that customer keeps assets on the platform. In the model, buyer CAC drops from $150 in Year 1 to $85 in Year 5, and seller CAC drops from $1,200 to $650. But total acquisition b udgets still rise from $45 million to $132 million, so payback still has to work.

What matters is lifetime value and retained balances, not downloads. If retention is weak, the owner keeps buying the same revenue twice. A funded account that stays active can support subscriptions, commissions, and balance-based monetization; a signed-up user who never funds adds cost, not cash flow.

Measure Payback by Funded Cohort

Measure CAC by cohort, not by total marketing spend. Use CAC = acquisition spend ÷ funded accounts, then compare it with retained balances, trading activity, and subscription revenue. Split buyers and sellers, because a $150 buyer and $1,200 seller have very different payback needs.

Watch three inputs each month: funded account count, balance retention, and repeat activity. If balances and activity fall after funding, lower CAC alone won’t lift owner income. Cut spend on low-funding channels, improve activation, and keep the channels that bring users who fund and stay.

- Track funded, not registered, users

- Measure retention by cohort

- Test payback by segment

- Cut spend on low-value channels

5

Fixed compliance and technology cost control

Fixed compliance and tech cost control

When this platform adds users, revenue does not automatically reach owner pay. The floor is already $58,000 a month in fixed costs: cloud hosting $25,000, software licenses $15,000, regulatory and legal retainer $10,000, and cybersecurity $8,000. One line is incomplete for office rent, and variable compliance can rise with revenue, so the true break-even point is higher.

Here’s the quick math: before the owner takes a draw, gross profit must cover those fixed costs plus partner fees, data feeds, clearing or custody costs, engineering, and support. If funded accounts grow but usage spikes cloud and compliance spend, margins can tighten fast. This is not legal or regulatory advice, but it is a cash rule: fixed overhead delays distributions until volume is large enough.

Track cost per funded account

Measure fixed cost per funded account, plus cloud cost per trade, support tickets per 1,000 accounts, and compliance spend as a percent of revenue. Tie vendor budgets to active users, order count, and data-feed volume, not just downloads. If the platform has 53,000 orders in Year 1, small per-order fee changes can matter more than top-line growth.

Cut waste in the biggest lines first: cloud, licenses, legal retainers, and cybersecurity. Ask vendors for usage caps, monthly true-ups, and lower rates at higher volume. Keep a monthly forecast that separates fixed spend from revenue-linked spend, so you know when subscription and commission income can safely cover owner pay instead of just funding the stack.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts with activation speed, CAC, and the mix of traders, portfolio managers, and institutions. Faster scale helps, but marketing, compliance, and staffing can still squeeze take-home.

| Scenario | Low CaseDownside case | Base CaseBase case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the slow-start case, where activation lags and owner income stays tight. | This is the modeled case, with steady growth and owner income tracking the core forecast. | This is the upside case, where scale comes faster but reinvestment stays heavy. |

| Typical setup | The model starts with weaker funded-buyer activation, higher CAC, lower repeat orders, and a heavier day-trader mix. | The base case follows the researched mix shift from 45% day traders to 25%, 55% portfolio managers by Year 5, CAC easing from $1,200 to $650, and revenue moving from $66 million in Year 1 to $583 million in Year 5. | The high case assumes faster buyer and seller growth, stronger repeat orders, more subscription income, and higher support and compliance spend. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Below $223kThin band | $223k - $378MCore band | Above $378MUpside band |

| Best fit | Use this to stress-test a slow launch and a cash-tight first year. | Use this as the main planning case for budgeting, hiring, and reserve policy. | Use this to test what happens if growth outruns staffing, support, and compliance capacity. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Investment Platform Porter's Five Forces Analysis

- Investment Platform BCG Matrix

- Investment Platform Business Model Canvas

- 7 Critical KPIs for Scaling Your Investment Platform

- Investment Platform Business Plan Template in Pre-Written Word

- Increase Investment Platform Profitability: 7 Key Financial Strategies

- How Much Does It Cost To Run An Investment Platform Monthly?

- Investment Platform Startup Costs: $62M First-Year Launch Budget

- Investment Platform Financial Model Template in Excel

- How To Start An Investment Platform In 9 To 18+ Months

- How to Write an Investment Platform Business Plan in 7 Steps

- Investment Platform Marketing Mix

- Investment Platform Marketing Plan

- Investment Platform Business Proposal

- Investment Platform PESTEL Analysis

- Investment Pitch Deck Example Editable PPTX

- Investment Platform Business SWOT Analysis

- Investment Platform Value Proposition Canvas

Frequently Asked Questions

An owner’s take-home depends on funded accounts, trading activity, subscriptions, CAC, compliance costs, and reserves In the researched base case, Year 1 revenue is about $66 million with roughly $223,000 of pre-reserve operating profit By Year 5, revenue reaches about $583 million and the pre-reserve profit pool reaches about $378 million