Invoice Factoring Service Startup Costs: $97M Funding Capacity

You’re funding receivables before you’re buying assets In the researched base plan, the invoice factoring business startup cost is driven by $97 million of first-year invoice advances, $125 million of operating and reserve assets, $545,000 of Year 1 payroll, and $18,700 in monthly fixed overhead Narrow CAPEX is not provided as a fixed amount in the research, so computers, secure IT hardware, office equipment, and capitalized software setup should be modeled separately These are planning assumptions, not vendor quotes, guarantees, or legal-financial advice

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

This estimates capitalized startup assets only, so you can see launch CAPEX before funding invoices, payroll, or working cash.

Excluded from CAPEX This calculator excludes invoice purchase capital, payroll runway, monthly fixed overhead, debt service, deposits, inventory, marketing, reserves, legal retainers, UCC filing fees, and other working capital or operating costs. The model's excluded funding items, including about $97M of invoice purchase capital, about $545k of payroll runway, and about $187k of monthly fixed overhead, stay outside startup CAPEX.

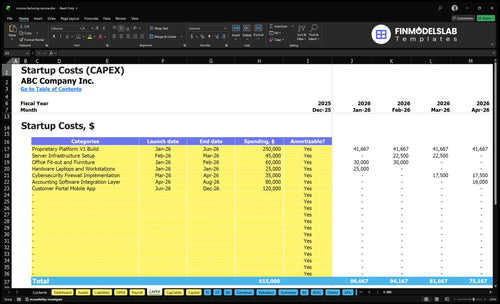

Does this CAPEX tab validate launch costs?

This Invoice Factoring Service Financial Model Template CAPEX tab shows startup cost categories, timing, costs, and depreciation/amortization—review assumptions now.

Key screenshot checks

- Computers, office, phones

- Software and security

- Depreciation and amortization

- Separate startup expenses

- Launch through year one

- Test $97M advances

- Confirm $125M reserves

- Verify $545k payroll

- Match $2,244k overhead

- Cover $95M liabilities

What hidden costs come with starting an invoice factoring service?

If you start an Invoice Factoring Service, the hidden costs are the legal and control steps that let you buy receivables safely. That includes legal agreements, personal guarantees, debtor notices, lien searches, UCC-1 financing statements, state-specific legal review, credit checks, fraud prevention, collections setup, payment controls, insurance, and bad-debt reserve planning; see How To Start Invoice Factoring Service? for the launch sequence. The biggest cost traps are the stated assumptions: 120% bad debt provision, 45% credit data and verification fees, $22k monthly professional insurance, and $18k monthly security and compliance audits.

Core cost drivers

- Legal agreements and state review

- UCC-1 filings and lien searches

- Credit checks and verification fees

- Insurance and reserve planning

Operational readiness

- Debtor notices and payment controls

- Fraud prevention and collections setup

- Security audits at $18k monthly

- Professional insurance at $22k monthly

How much capital do factoring companies need to buy invoices?

For an Invoice Factoring Service, the money you need is working capital, not CAPEX: you need enough cash to buy invoices and wait for payment. In the first-year model, advances total $97M across $25M staffing, $32M manufacturing, $18M IT services, $12M government contractor funding, and $10M wholesale trade credit. Modeled rates run from 120% to 180% by segment, so bigger funding pools raise revenue capacity but also raise credit checks, reserves, bad debt exposure, and lender covenants.

Capital need

- Buy invoices, not equipment.

- Fund the gap until payback.

- Scale with advance volume.

- Track cash by segment.

Risk load

- More capital means more checks.

- Set reserves before growth.

- Watch bad debt closely.

- Expect tighter covenants.

How should an invoice factoring business financial model handle startup funding?

Handle startup funding as a liquidity plan, not just a raise. Model CAPEX, startup spend, invoice purchase capacity, advance rates, fee or interest income, funding costs, reserves, bad-debt provision, and collections timing by month and year. In the base plan, $97M of advances, $125M of operating and reserve assets, and $95M of interest-bearing liabilities support about $1,511M of Year 1 factoring income before other asset income and before liability interest expense, with $545k payroll and $2,244k annual fixed overhead setting the break-even test.

Startup funding inputs

- Model CAPEX first.

- Include startup expenses upfront.

- Size invoice purchase capacity.

- Link funding to advance rates.

Cash and spread checks

- Price fee or interest rates.

- Test funding cost spread.

- Hold reserves for bad debt.

- Map collections timing monthly.

Calculate Fuding Needs

Startup Cost Summary

This table summarizes startup CAPEX and excluded cash needs for an invoice factoring service under low, base, and high cases.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Proprietary Platform V1 Build | $250,000 | Core software build and workflow automation | Yes |

| Accounting Software Integration Layer | $80,000 | Data sync and accounting system setup | Yes |

| Customer Portal Mobile App | $120,000 | Client onboarding and invoice status access | Yes |

| Cybersecurity Firewall Implementation | $35,000 | Security controls and compliance hardening | Yes |

| Hardware Laptops and Workstations | $25,000 | Staff setup and underwriting readiness | Yes |

| Invoice Purchase Capacity and Operating Runway | $47,595,000 | Invoice advances, bad debt, payroll, and fixed overhead | No |

Invoice Factoring Service Core Five Startup Costs

Invoice Purchase Capital Startup Expense

Working Capital Pool

Invoice purchase capital is working capital, not CAPEX. Year 1 source advances total $97M across $25M staffing, $32M manufacturing, $18M IT services, $12M government contractor invoices, and $10M wholesale trade credit. The model only works if paid invoices recycle fast enough to fund the next advance.

Sizing Inputs

Size this pool from average invoice size × advance rate × outstanding days, then adjust for debtor payment terms, concentration limits, and default risk. Year 1 cost pressure ranges from 120% to 180%, so the real question is how much cash stays deployed before collections bring it back.

- Watch debtor payment terms

- Cap single-customer exposure

- Measure recycle speed weekly

Control The Float

Keep exposure tight: cap one debtor, shorten payment terms where you can, and track how fast paid invoices recycle back to cash. Don't let a few large buyers dominate the book. Faster collections and lower default risk cut the amount of funding capacity you need to keep the platform moving.

What Drives Cash Need

Average invoice size, advance rate, and payment speed drive cash need more than office spend. If invoices are slow, concentrated, or disputed, the funding line gets used up fast, so this expense behaves like a revolving pool, not a one-time launch asset.

Legal And Compliance Setup Startup Expense

Legal build

Formation and paper covers entity setup, receivables purchase agreements, factoring agreements, personal guarantees, debtor notices, lien searches, UCC-1 filing workflows, state-by-state legal review, privacy controls, and collections language. Use quote-based inputs, because the research gives operating risk figures but not vendor prices. Do not claim a universal licensing requirement; rules vary by state and model.

Trim spend

Keep it lean by reusing one base contract, then localize only the state terms, debtor notice, and collections language. Budget with counsel quotes, filing fees, and review hours, not guesswork. The main mistake is skipping lien searches or filing UCC-1 late, which can weaken priority and invite fraud or enforceability problems.

Controls

Priority first: this spend protects who gets paid first if an invoice turns ugly. UCC-1 timing, debtor notice, and clean privacy controls support lien priority and collections. If you buy invoices with 30, 60, or 90-day terms, the legal file has to be tight before the first advance goes out.

Enforceability

Debtor notice and signed paper are not admin chores; they are how you make the purchase enforceable and reduce disputes over who owns the receivable. Clean notices, exact assignment language, and a tracked filing workflow help support fraud control and collections when a customer pays late or contests the invoice.

Software And Underwriting Tools Startup Expense

Setup Split

Separate one-time implementation and capitalized setup from monthly SaaS. For FlowCapital, the stack includes the factoring platform, client portal, CRM, accounting integration, credit reports, bank verification, document storage, cybersecurity, payment tracking, and collections workflow. The monthly tech base is $55k before launch work, made up of $25k cloud, $18k audits, and $12k licensing.

What It Covers

Model setup with quotes, user counts, and months of coverage. One-time spend should cover configuration, data migration, and controls; monthly spend should cover active seats and usage. The key variable is verification volume: Year 1 variable verification costs are modeled at 45%, so each file review, bank check, and credit pull needs a unit cost.

Keep It Lean

Buy only what underwriting and collections need on day one. Ask vendors for per-invoice, per-check, or per-user pricing, and avoid paying for idle seats. The common mistake is treating verification as fixed overhead; with 45% variable cost in Year 1, small volume changes can move cash need fast.

- Price by active volume.

- Delay extra seats.

- Review usage monthly.

Budget Burn

Budget the tech burn at $55k per month before implementation costs, then layer setup on top. If invoice volume rises, the 45% verification load can outgrow SaaS spend, so track funded invoices, not just software seats. That keeps underwriting, compliance, and collections funded without surprises.

Staffing Readiness Startup Expense

Payroll Runway

Payroll runway is working capital here, unless it is tied to recruiting, training, or pre-opening setup. The Year 1 staffing line is $545k, or about $454k per month before taxes and benefits, so cash needs depend on months covered, hiring timing, and whether the team is fully ramped before invoices start cycling.

What It Covers

Build this cost from FTE count times annual pay, then add recruiting and training months. The core jobs here are underwriting procedures, account management, collections playbooks, bookkeeping, and outsourced finance operations. One clean rule: hire for the cash cycle you can support, not the org chart you want later.

- Headcount by role

- Salary per FTE

- Ramp months before cash

Cost Control

Keep this line tight by staging hires, outsourcing bookkeeping, and using outside finance ops until volume proves out. Don’t hire a full bench before collections, debtor notices, and reconciliations work cleanly. The biggest risk is paying for capacity before invoices start paying back into cash.

- Delay non-core hires

- Outsource finance work

- Hire to payment volume

Operating Bench

Underwriting, account management, and collections need clear playbooks from day one, because speed only helps if cash is tracked and recovered on time. Bookkeeping and outsourced finance operations should close the loop on invoice aging, debtor notices, and cash posting, so the team can scale advances without losing control of the ledger.

Insurance, Risk, And Marketing Startup Expense

Coverage Base

This spend covers professional liability or E&O, cyber coverage, crime/fidelity coverage, broker help, and the website plus credibility materials used to win B2B clients. For an invoice factoring platform, the point is not just protection; it is proof you can handle money, data, and collections.

Cost Inputs

Price it with monthly insurance quotes, months of coverage, and one-time website and brand assets. The source fixed cost is $22k a month for professional insurance and $45k a month for the marketing agency retainer, or $67k monthly before any variable lead spend.

- Policy quotes by coverage type

- Website and credibility build

- Agency retainer each month

Risk Controls

Keep this cost tied to controls that reduce loss: invoice vali dity checks, debtor payment risk review, client concentration limits, collections follow-up, and fraud controls. Use the Year 1 model inputs of 120% bad debt provision and 45% credit data and verification fees to test if fee income can still cover losses.

- Invoice validity before funding

- Debtor risk by customer

- Fraud checks on every file

Budget Fit

This is a fixed-cost block, so it scales slowly while revenue depends on deal flow. A $67k monthly base means broker relationships and B2B lead generation have to produce enough qualified invoices to justify the spend, or the platform burns cash even before claims and write-offs show up.

Compare 3 Startup Cost Scenarios

Scenario table

Smaller vertical launches can start with one or two invoice pools, but the base plan needs far more capital because advances, reserves, payroll, and compliance scale fast.

| Scenario | Lean LaunchSmall verticals | Base LaunchYear 1 model | Full LaunchYear 2 scale |

|---|---|---|---|

| Launch model | Start with a founder-led launch in one or two smaller verticals like wholesale trade credit or government contractor invoices. | Run a broader launch across core verticals with the Year 1 balance sheet and staffing plan. | Build for Year 2 capacity with a much larger advance book and broader market coverage. |

| Typical setup | Keep underwriting manual, limit advance size, and use a small team with basic reporting. | Plan for $97M in advances, $125M in reserve and operating assets, $545k payroll, and $187k monthly fixed costs. | Prepare for $230M advance capacity, higher staff, more software, legal work, reserves, and lender reporting. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | $10M - $25MLow capital | $97M - $125MModel base | $230M+High capacity |

| Best fit | Founders testing one niche before adding more sectors. | Teams ready to operate at full Year 1 scale from the start. | Operators planning fast growth and tighter institutional controls. |

Planning note: These ranges are researched planning assumptions, not exact quotes; actual capital needs depend on underwriting speed, reserve policy, and funding mix.

Related Products

- Invoice Factoring Service Porter's Five Forces Analysis

- Invoice Factoring Service BCG Matrix

- Invoice Factoring Service Business Model Canvas

- What Are The 5 KPI Metrics For My Invoice Factoring Service Business?

- Invoice Factoring Business Plan Template in Pre-Written Word

- How Increase Invoice Factoring Service Profits?

- How Increase Invoice Factoring Service Profitability?

- Invoice Factoring Service Financial Model Template in Excel

- How Much an Invoice Factoring Service Owner Can Make at $97M Volume

- How To Start An Invoice Factoring Company In 60–120 Days

- How To Write A Business Plan For Invoice Factoring Service?

- Invoice Factoring Service Marketing Mix

- Invoice Factoring Service Marketing Plan

- Invoice Factoring Service Business Proposal

- Invoice Factoring Service PESTEL Analysis

- Invoice Factoring Service Pitch Deck Example Editable PPTX

- Invoice Factoring Service Business SWOT Analysis

- Invoice Factoring Service Value Proposition Canvas

Frequently Asked Questions

The researched base plan needs funding capacity for $97M of first-year invoice advances, plus $125M in operating and reserve assets It also carries $545k of Year 1 payroll and $187k in monthly fixed overhead Narrow CAPEX is separate because the research does not provide a fixed equipment or implementation total