Owner income$75k

Owner income$75kHow Much Can a Janitorial Supply Store Owner Make on $75K Pay?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$75k  Net margin80.1%

Net margin80.1% Revenue for target pay$33.4k

Revenue for target pay$33.4k Business difficultyHard

Business difficultyHard

A janitorial supply store owner’s income is not the same as store revenue In this 60-month planning case, the model includes $75,000 annual owner pay, breakeven in Month 25, a 33-month payback, and a $438,000 minimum cash need before taxes, debt service, and owner distributions

Owner income$75kNet margin80.1%Revenue for target pay$33.4kBusiness difficultyHardCan this store pay you $75K?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay for a janitorial supply store.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Results depend on revenue, margin, payroll, taxes, debt, and reinvestment.

Can you stress-test the $438K cash need?

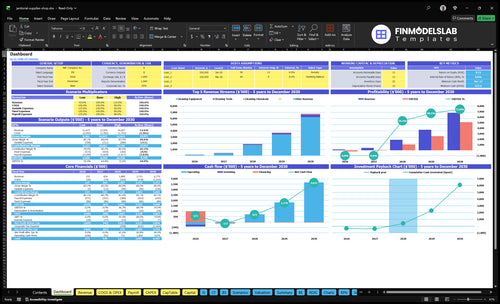

The screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Janitorial Supply Store Financial Model Template; open it to test the $438K cash need, $75,000 owner payroll, Month 25 breakeven, 33-month payback, 872% ROE, and 007% IRR. It also lets you change conversion from 80%, repeat rate from 250%, product units per order, equipment mix, rent, payroll, and inventory reserve.

Owner-income model highlights

- Owner pay: $75K

- Breakeven: Month 25

- Payback: 33 months

How much revenue does a janitorial supply store need?

The Janitorial Supply Store needs about $25,600 in monthly sales to cover operating break-even, but if you work back from $75,000 a year in owner pay, plus $85,800 of fixed overhead and $160,000 of non-owner payroll, you’re closer to $33,400 a month before debt and reserves. Salary, draw, and profit are separate, so don’t mix owner pay with the sales target.

Owner pay math

- $75,000 yearly owner pay

- $6,250 monthly before tax

- $85,800 fixed overhead yearly

- $160,000 non-owner payroll yearly

Sales target

- $25,600 monthly operating break-even

- $33,400 monthly with owner pay

- Debt is not included here

- Reserve cash is not included here

What is a janitorial supply store profit margin?

A Janitorial Supply Store’s profit margin is driven by product mix, not one markup. In the Year 1 model, see How Much Does It Cost To Open, Start, Launch Your Janitorial Supply Store?, the mix leans on 500% chemicals, 350% tools, and 150% equipment, with gross margin dollars of $15, $45, and $1,800. After 149% wholesale inventory cost, 20% inbound freight drag, 18% payment fees, and 12% packaging plus overhead risk, deep commercial discounts can grow revenue while cutting take-home.

Margin drivers

- Product mix sets take-home.

- Chemicals, tools, equipment differ.

- Year 1 gross margin: $15, $45, $1,800.

- Mix shown at 500%, 350%, 150%.

Margin pressure

- 149% wholesale inventory cost hurts.

- 20% inbound freight adds drag.

- 18% payment fees stack up.

- 12% packaging and overhead bite.

Is a janitorial supply store profitable?

Yes—a Janitorial Supply Store can be profitable when repeat demand, margin, and overhead line up. In the source case, break-even hits Month 25, payback takes 33 months, and the minimum cash need is $438,000 at Month 24; the modeled return on equity is 872%. Profit is possible, but freedom costs money.

Profit drivers

- Repeat orders support steady sales

- Commercial accounts lift revenue

- Delivery coverage can expand reach

- Margin and overhead must stay aligned

Owner tradeoffs

- $75,000 owner role keeps control close

- $60,000 Store Manager adds payroll load

- Staff scale can raise service costs

- Inventory cash gets tied up fast

What drives owner take-home most?

1

8%-18%Account flow

More commercial buyers and repeat orders lift sales fast because conversion rises from 8% in Year 1 to 18% in Year 5.

2

83%-85%Product mix

Shifting more sales into higher-ticket equipment helps gross margin stay near 83% and edge higher as inventory cost falls.

3

2 ptsPrice discipline

Tight buying terms and steady price lifts protect take-home because wholesale inventory cost drops from 14.9% to 13.0%.

4

$438KInventory turns

Slow stock turns trap cash, and the model's minimum cash sink hits $438K before breakeven, which presses owner returns.

5

$7.2K/moFixed overhead

About $7,150 of fixed monthly overhead sets the profit floor, so rent, utilities, software, and marketing must stay tight.

6

$75KOwner role

Owner pay is $75,000 a year, and the $235,000 Year 1 payroll bill means staffing choices hit profit right away.

Janitorial Supply Store Core Six Income Drivers

Commercial account volume

Commercial Account Volume

Repeat commercial accounts make income steadier than walk-in-only sales. In Year 1, repeat customers are 250% of new customers, and by Year 5 they rise to 650%. That matters because office buildings and cleaning contractors reorder chemicals, paper products, and tools about once per month, so the owner gets more predictable order flow and a longer revenue life.

Here’s the catch: volume helps only after gross margin, delivery cost, payment timing, and inventory reserve. A slow-paying account can show profit on paper but still create cash stress in the bank. Repeat life moves from 6 months to 15 months, so the real income gain is not just more sales; it’s keeping the cash cycle tight enough to pay the owner without starving stock.

Measure Account Quality

Track new accounts, repeat accounts, orders per month, average repeat life, and days to pay. If a customer buys once a month but pays late, the account may hurt take-home income even when revenue looks strong. The goal is simple: add repeat volume that improves cash, not just top-line sales.

- Count repeat orders by account

- Watch payment timing by customer

- Split chemical, paper, tool demand

- Hold inventory for fast movers

One clean account beats three sloppy ones. If an account adds frequent reorders but also long payment delays, build stricter terms or smaller delivery runs. That protects gross margin, keeps inventory from swelling, and gives the owner a clearer path to regular profit draw.

1

Product mix and blended margin

Product mix drives blended margin

When the store sells more chemicals, tools, or equipment, the blended gross margin changes fast. In this model, Year 1 mix is 500% chemicals, 350% tools, and 150% equipment, then shifts by Year 5 to 300%, 350%, and 350%. That mix, plus unit prices rising from $15 to $17, $45 to $51, and $1,800 to $2,000, sets the revenue and profit pool.

Equipment can lift ticket size, but it also brings demo time, service, storage, and slower replenishment. The model also assumes wholesale inventory cost improves from 149% to 130%, while inbound freight stays a 20% risk. If mix drifts toward heavy equipment without enough margin, owner pay gets squeezed even when sales look strong.

Watch mix, not just sales

Track gross margin by category, not just total revenue. Here’s the quick math: units sold, category price, inbound freight, and service time all feed the blended margin. Use monthly mix reports to see whether chemicals still cover cash needs while equipment raises the average ticket. The one-liner: margin follows mix.

Set floor margins by category and test equipment sales with clear rules. Measure demo time, storage days, reorder speed, and freight per order so the higher-ticket items do not eat the profit they create. If equipment sales rise but inventory sits longer, cash flow weakens and owner draws should wait until replenishment cash is safe.

2

Pricing and vendor terms

Pricing and Vendor Terms

For a janitorial supply store, pricing and vendor terms decide how much of each bulk order turns into owner pay. The source model shows 831% gross margin in Year 1 and 850% in Year 5 after inventory and inbound freight, so the real job is protecting that spread when large commercial accounts ask for discounts.

Track wholesale cost, inbound freight, and any rebate or discount given on chemicals, tools, and equipment. If a large account’s discount is bigger than the freight and fulfillment savings, monthly sales can rise while take-home income falls. Price discipline pays the owner.

Protect the Floor Margin

Set an account-level floor margin before you quote volume deals. Use category rules for chemicals, tools, and equipment, then compare each offer against the cash cost of picking, packing, delivery, and credit terms. That keeps discounts tied to real savings, not just top-line growth.

What to track: net shelf price, vendor freight, rebate value, and take-home profit per account. There is no source default for rebate tiers, so test terms carefully and document them by customer. More sales only help if margin stays intact.

3

Inventory turnover and cash flow

Inventory turnover and cash flow

Inventory is a cash-flow driver, not just an expense line. This model starts with $30,000 of stock, and wholesale inventory cost runs at 149% of sales in Year 1, so cash leaves the bank before it comes back in from repeat orders. The minimum cash need climbs to $438,000 in Month 24, before breakeven in Month 25.

Dead stock ties up cash, stockouts lose repeat orders, and slow equipment sales can crowd out fast-moving chemicals and tools. The inputs that matter are days on hand, repeat demand by category, reorder lead time, and owner pay. One clean rule: if the shelf is full but cash is thin, income is being trapped in inventory, not earned.

Track category stock turns

Measure days on hand by category for chemicals, tools, and equipment, then reorder from actual repeat demand, not old buying patterns. That tells you where cash is stuck and where a stockout would hit revenue. Fast movers should earn shelf space first, because they turn into cash and support owner pay faster.

Set a cash reserve before taking draws. If owner pay drains replenishment cash, you miss reorders, lose repeat orders, and end up with more dead stock. Watch the gap between stock buys and sales receipts each month, and trim slow equipment first when cash tightens.

4

Operating costs and fulfillment overhead

Operating Costs and Fulfillment Overhead

Overhead hits owner income before any draw. Here’s the quick math: fixed costs are $7,150/month or $85,800/year, and Year 1 payroll is $235,000, including $75,000 owner pay, $60,000 manager, $45,000 senior sales, $35,000 sales associate, and $20,000 ops support.

A $40,000 delivery van is cash, not profit, and it can make routes messy if stops are spread out. Add routes only when account density supports them, or you get more labor and driving without enough extra gross profit to protect owner distributions.

Keep Overhead Out of Owner Pay

Track the inputs that set this driver: lease, utilities, insurance, software, marketing, website, accounting, payroll, and route count. The one-line test is simple: if monthly sales and margin can’t support $7,150 of fixed overhead plus staffing, the owner’s take-home gets squeezed fast.

- Track overhead by month.

- Measure revenue per route.

- Delay van adds without density.

Build the forecast with separate lines for fixed overhead and fulfillment labor, then stress test slower account growth. If a new route adds payroll and driving but not enough repeat order volume, it lowers cash available for owner pay even when sales look better on paper.

5

Owner role and management structure

Owner vs. Manager Pay

This driver is about who does the work and who gets paid for it. The model budgets Owner/General Manager at $75,000 a year and Store Manager at $60,000 a year, so the store can run with either owner oversight or hired management. If the owner replaces a hire, payroll drops on paper, but the owner is still doing real labor with economic value.

The key inputs are owner hours, manager salary, and which tasks stay with the owner: purchasing, vendor negotiation, account relationships, and hard equipment sales. More freedom needs more revenue because management payroll has to be covered before owner draw. One clean rule: if the owner steps back, the store needs enough gross profit to pay the replacement manager and still support cash flow.

Track Labor Before You Outsource It

Measure owner time by function, not just by hours. Put a value on purchasing, sales close work, and key accounts, then compare that value with the $60,000 manager cost and the $75,000 owner-run budget. That shows whether the owner is saving cash, adding profit, or just shifting labor off the payroll line.

- Track owner hours by task.

- Price manager coverage at $60,000.

- Protect margin on big accounts.

- Keep vendor terms and reorder control.

If the owner is still the main buyer and problem-solver, don’t treat the business as hands-off. The real test is whether gross profit can carry management payroll and still leave room for owner pay after rent, staff, and inventory needs are covered.

6

Compare lean, base, and high-volume owner-income scenarios

Owner income scenarios

Owner income moves with traffic, conversion, repeat orders, and inventory mix. This store is cash-intensive, account-driven, and sensitive to payroll and stock timing.

| Scenario | Low CaseTight cash | Base CasePlan case | High CaseUpside case |

|---|---|---|---|

| Launch model | The launch stays lean, and owner income is mostly salary with little room for draws. | The model follows the planned growth path and supports the owner salary once sales and margin hold. | A stronger sales path creates room for salary plus distributions after reserves and debt service. |

| Typical setup | Year 1 and Year 2 stay cash tight, with modest traffic, weak conversion, and limited repeat buying. | Breakeven lands around Month 25, so the planned $75,000 owner salary is the main take-home item before draws. | By Years 3 to 5, repeat customers, two-unit orders, and a richer equipment mix lift earnings above the base plan. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $75,000Salary only | $75,000Modeled pay | $75,000+Draws possible |

| Best fit | Use this to stress-test a slow start and tight cash control before breakeven. | Use this as the core operating case for lender talks and annual planning. | Use this to test upside if account volume, basket size, and stock turns all beat plan. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Janitorial Supply Store Porter's Five Forces Analysis

- Janitorial Supply Store BCG Matrix

- Janitorial Supply Store Business Model Canvas

- 7 Essential KPIs to Track for a Janitorial Supply Store

- Janitorial Supply Store Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Janitorial Supply Store Profitability

- How to Manage Monthly Running Costs for a Janitorial Supply Store

- Janitorial Supply Store Startup Costs: Plan $438K Cash Need

- Janitorial Supply Store Financial Model Template in Excel

- How To Open A Janitorial Supply Store In 8 To 16 Weeks

- How to Write a Janitorial Supply Store Business Plan in 7 Steps

- Janitorial Supply Store Marketing Mix

- Janitorial Supply Store Marketing Plan

- Janitorial Supply Store Business Proposal

- Janitorial Supply Store PESTEL Analysis

- Janitorial Supply Store Pitch Deck Example Editable PPTX

- Janitorial Supply Store Business SWOT Analysis

- Janitorial Supply Store Value Proposition Canvas

Frequently Asked Questions

The researched plan carries $75,000 in annual Owner/General Manager pay before taxes That is payroll, not a guaranteed distribution The store also needs cash discipline because the model shows a $438,000 minimum cash need in Month 24, breakeven in Month 25, and payback in 33 months