Owner income$142k

Owner income$142kHow Much Does a Japanese Restaurant Owner Make? $142K Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$142k  Net margin18% to 46%

Net margin18% to 46% Revenue for target pay$792k

Revenue for target pay$792k Business difficultyHard

Business difficultyHard

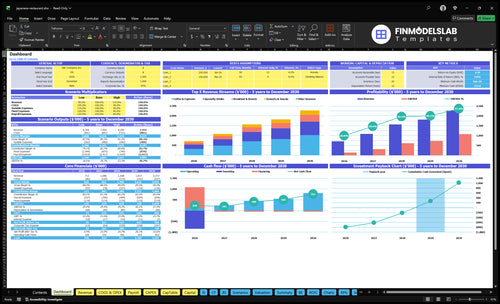

In the researched base case, a Japanese restaurant owner could have a profit pool of about $142k in Year 1 EBITDA, before taxes, debt service, reserves, and discretionary owner draws Monthly revenue starts near $66k and reaches about $194k by Year 5, based on modeled covers and average order value The model reaches break-even in Month 3, but still needs $214k minimum cash in Month 9 and shows a 43-month payback Treat this as a planning case, not a salary promise

Owner income$142kNet margin18% to 46%Revenue for target pay$792kBusiness difficultyHardWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on sales, margins, payroll, debt, taxes, reserves, and timing.

Want the full Japanese Restaurant financial model?

This screenshot shows revenue build-up, AOV assumptions, costs, EBITDA, cash flow, break-even, and owner income; open the Japanese Restaurant Financial Model Template.

Owner-income model highlights

- Owner take-home outputs

- Lean, base, strong tabs

- Monthly sales and cash charts

Does a Japanese restaurant owner need to work in the business?

For a Japanese Restaurant, the owner does not always have to work in the business, but stepping back usually lowers take-home unless sales and margins can cover a $70k/year store manager from Month 1. In this base case, absentee ownership is partly funded, so the model can work, but only if the business keeps enough margin to pay that payroll. A chef-owner can protect quality and ease food-cost pressure, but it also adds workload; multi-location growth needs managers, systems, cash reserves, and repeatable food cost control.

Owner stays involved

- Protects food quality

- Reduces payroll pressure

- Adds daily workload

- Fits early-stage control

Owner steps back

- Needs paid management

- Raises cash needs

- Needs repeatable systems

- Works best with margin

What costs reduce Japanese restaurant owner income?

For a Japanese Restaurant, the biggest income drains are raw materials and packaging, payment fees, and marketing and loyalty; see How Much Does It Cost To Open Your Japanese Restaurant? for the startup side. Raw materials and packaging run 12% of sales in Year 1 and improve to 10% by Year 5, while payment fees add 25% in Year 1. Sushi seafood, ramen prep labor, tempura oil, spoilage, and delivery packaging all hit cash before the owner gets paid.

Direct cost drains

- 12% of sales goes to materials.

- 25% goes to payment fees.

- 5% goes to marketing and loyalty.

- Fixed costs run $145k/month.

Payroll pressure

- Payroll starts at 2225k/year.

- Payroll rises to 505k by Year 5.

- Spoilage cuts cash fast.

- Delivery packaging adds more drain.

How much revenue does a Japanese restaurant need to pay the owner?

For a Japanese Restaurant, there isn’t a single owner-pay revenue number; use target-pay planning instead. In the model, Year 1 revenue is about $66k/month with $142k EBITDA, and Year 5 is about $194k/month with 1078M EBITDA; owner pay must come after raw materials, fees, marketing, payroll, rent, debt service, taxes, and cash reserves.

Pay comes last

- $145k/month fixed costs before payroll

- Raw materials come first

- Fees and marketing come next

- Then payroll, rent, taxes, reserves

Model the revenue path

- Year 1 revenue: $66k/month

- Year 1 EBITDA: $142k

- Year 5 revenue: $194k/month

- Year 5 EBITDA: 1078M

Want the six income drivers that matter most?

1

$66K-$194K/moSales Volume

More covers and faster table turns push monthly sales from about $66K to $194K, so this is the biggest cash lever.

2

$8-$12Average Check

Raising the check with better menu mix and add-ons lifts revenue without the same jump in labor.

3

$223K-$505KLabor Scheduling

Payroll grows from about $223K to $505K a year, so shift timing and staffing mix decide how much sales become profit.

4

12%-10%Food Cost

Raw materials and packaging fall from 12% to 10% of sales, which widens gross margin on every order.

5

$14.5K/moFixed Costs

Rent, tech, insurance, and other overhead total about $14.5K a month, so weak traffic hits owner cash fast.

6

7.5%-6.0%Delivery Profit

Payment fees and marketing run about 7.5% to 6.0% of sales, so takeout and delivery only help when the ticket covers the fee stack.

Japanese Restaurant Core Six Income Drivers

Sales Volume and Table Turns

Sales Volume and Table Turns

More covers lift revenue faster than rent, so this driver has a direct pull on owner income. In the model, weekly covers rise from 1,660 in Year 1 to 4,020 in Year 5, while monthly sales climb from about $66k to $194k. One clean line: more seats filled, more cash left after fixed costs.

The risk is slow turns. If lunch, dinner, weekend demand, reservations, seat use, or kitchen throughput slip, fixed costs stay the same and the owner keeps less cash. That means lower profit, tighter cash flow, and less room for owner pay, even if food quality stays strong.

Track Covers and Turn Time

Measure covers by daypart, table turns per service, reservation fill rate, and average seat time. Track kitchen ticket time too, because the dining room can only turn as fast as the slowest station. If lunch or weekend turns lag, the lost revenue shows up fast in owner draw.

Use this simple lens: covers × average check × service speed. Push more seats through the same rent base, but don’t let pace hurt quality. Watch for long waits, empty tables, or prep bottlenecks, since each one cuts revenue without cutting the monthly fixed-cost load.

- Count covers by lunch, dinner, weekend

- Track average turn time daily

- Compare reserved seats to seated guests

- Watch kitchen ticket delays closely

- Flag slow turns before cash tightens

1

Average Check and Menu Mix

Average Check and Menu Mix

Average check (AOV) is the dollars each guest spends per visit. For this concept, it starts at $8 midweek and $10 on weekends, then rises to $10 and $12 by Year 5. At the same cover count, that lift goes straight into revenue, but only if sushi combinations, ramen add-ons, tempura sides, beverages, and set meals do not add equal food or labor cost.

Here’s the quick math: a $2 check lift per guest is meaningful because volume already drives the model. The owner benefits most when the higher check comes from items with strong margin and low prep time. If premium mix needs more fish, labor, or waste, profit can stall even while sales rise.

Raise Check, Protect Margin

Track AOV by day, menu mix, and attach rate for drinks, add-ons, and set meals. Compare each item’s sales lift to its ingredient cost and prep time. A higher check only helps owner pay if gross margin holds and the kitchen can still move fast enough to keep covers high.

Test pricing and bundling in small steps, then watch the mix shift. If a combo adds revenue but also adds fish, labor, or spoilage, it may not improve cash. The best items are the ones that raise check size and keep the food cost and labor cost per guest close to flat.

- Track AOV by midweek and weekend.

- Measure add-on and beverage attach rates.

- Price combos against prep time.

- Watch food cost per guest.

2

Food Cost and Ingredient Control

Food Cost Control

Food cost is a direct cash lever. With raw materials and packaging at 12% of sales in Year 1, improving to 10% by Year 5, each point saved lifts gross margin and increases cash for debt, reserves, or owner draw. At $66k monthly sales, 1 point is about $660; at $194k, it is about $1,940.

This driver covers fish, proteins, rice, noodles, produce, sauces, frying oil, packaging, waste, and portioning. The risk is simple: if yields slip or portions grow, margin drops even when covers stay strong. One clean rule matters most: tighter plate control protects take-home pay.

Track Plate Cost

Build recipe costing for every core dish, then compare it to invoice prices and actual plate weights. Watch the highest-cost SKUs first, especially sushi, proteins, and frying items, because small waste there moves profit fast. If food cost runs above plan, fix the process before you raise prices.

- Track recipe grams and yields.

- Log waste by station daily.

- Review supplier prices weekly.

- Control portions with scoops.

3

Labor Model and Staffing Efficiency

Payroll and Shift Coverage

Payroll is a major profit gate in a Japanese restaurant. The model runs from $225k/year to $505k/year, covering the store manager, support staff, operations, and marketing. Sushi skill, ramen prep, dishwashing, and front-of-house scheduling all shape service speed. If labor is thin, covers slow down; if labor is heavy, owner pay gets squeezed.

Cut Idle Labor Hours

Track labor per cover, manager hours, and peak shift coverage by daypart. If the owner is filling prep or floor gaps, payroll may look lean but growth is capped and burnout risk rises. Build staffing around dinner and weekend demand, since every slow table turn keeps fixed labor tied up and cuts cash available for owner draw.

- Match staff to peak covers.

- Measure labor by cover.

- Protect owner time from gaps.

4

Occupancy and Fixed Costs

Occupancy and Fixed-Cost Hurdle

Here’s the quick math: the model shows $145k/month in fixed costs before owner pay. The named items include $8k rent and utilities, $35k technology maintenance and licensing, and $12k cleaning and waste, plus smaller fees. These costs do not flex down when covers slow, so a weak month hits cash fast.

Occupancy matters because each extra cover spreads the same base over more sales. The disclosed line items add to $56.8k, so the $145k hurdle implies other overhead is built into the model. If lunch traffic, dinner turns, or reservations slip, owner pay is the first thing squeezed.

Track Covers Against Fixed Cost

Track monthly covers, seat turns, and average check by daypart. That tells you whether sales are covering the fixed-cost base or just filling seats. One clean test: compare monthly revenue to the $145k hurdle before owner draw, then watch how much cash is left after rent, tech, cleaning, and the other fixed bills.

- Covers by lunch and dinner

- Weekend turns versus weekdays

- Check size by menu mix

- Fixed-cost run rate monthly

- Empty seats by service

If slower months are normal, build a cash buffer and staff to the real demand curve, not peak nights. Use reservations and service pacing to protect turns, because rent and tech stay flat even when covers drop. That is where owner income gets protected or lost.

5

Takeout and Delivery Profitability

Takeout and Delivery Profitability

Takeout share can raise sales, but it only helps income when the added margin beats de livery commissions, packaging, and discounts. For this restaurant, the calculator should track order count, average order value, and the take-home margin per order, not just total tickets. If fees and waste outrun the lift, delivery volume cuts owner pay instead of adding it.

Menu durability matters here. Ramen can tolerate transit with better packaging, but sushi faces spoilage risk and tempura can lose quality fast. That means the same order can produce very different profit by item mix. The quick test is simple: if an order’s incremental gross profit after fees is below zero, it is a bad sale, even if the top line looks stronger.

Track Margin Per Delivery Order

Measure each channel separately: takeout share, commission rate, packaging cost, discount rate, and item mix. Then compare incremental revenue to incremental cost, including spoilage and remake risk. A simple rule: only scale the items that still leave cash after fees.

Use a short list of menu items for delivery and test them weekly. Track whether ramen, sushi, and tempura hold quality in transit, and remove items that create refunds or complaints. If delivery volume grows but owner draw falls, the menu mix is the problem, not demand.

6

Scenario objective for Japanese restaurant owner income planning

Owner income scenarios

Lower covers, tighter pricing, and heavier payroll can keep owner take-home thin. Stronger traffic and higher weekend spend lift income, but the plan still needs $214k minimum cash and a 43-month payback.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path, with thin traffic and a small owner draw. | This is the modeled base case, where the restaurant runs at the plan level. | This is the stronger earnings path, with Year 5 traffic and premium weekend spend. |

| Typical setup | Year 1-style covers, $8 midweek and $10 weekend spend, 12% raw materials, 2.5% processing fees, and full payroll burden keep cash tight. | Year 1 revenue is about $66k a month, raw materials sit at 12%, fixed costs run about $14.5k a month, payroll is about $222.5k, and EBITDA is $142k. | Year 5 revenue reaches about $194k a month, raw materials drop to 10%, payroll rises to $505k, and EBITDA reaches $1.078M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Limited owner drawLow Case | Mid-six-figure drawBase Case | Seven-figure upsideHigh Case |

| Best fit | Use this to stress test cash risk and see what the owner can safely take out early on. | Use this as the working plan for budgeting, lender talks, and owner pay planning. | Use this to test upside, staffing scale, and whether the cash plan can hold through growth. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Japanese Restaurant Porter's Five Forces Analysis

- Japanese Restaurant BCG Matrix

- Japanese Restaurant Business Model Canvas

- 7 Key Financial KPIs to Track for Your Japanese Restaurant

- Japanese Restaurant Business Plan Template in Pre-Written Word

- Increase Japanese Restaurant Profitability: 7 Data-Driven Strategies

- How Much Does It Cost To Run A Japanese Restaurant Monthly?

- Japanese Restaurant Startup Costs: $845K CAPEX Plus $214K Cash

- Japanese Restaurant Financial Model Template in Excel

- How To Open A Japanese Restaurant: Month 1 To Month 9 Launch Roadmap

- How to Write a Japanese Restaurant Business Plan: 7 Essential Steps

- Japanese Restaurant Marketing Mix

- Japanese Restaurant Marketing Plan

- Japanese Restaurant Business Proposal

- Japanese Restaurant PESTEL Analysis

- Japanese Restaurant Pitch Deck Example Editable PPTX

- Japanese Restaurant Business SWOT Analysis

- Japanese Restaurant Value Proposition Canvas

Frequently Asked Questions

In this model, the owner’s profit pool is $142k Year 1 EBITDA, rising to $1078M by Year 5 That is not guaranteed take-home pay Actual owner income comes after taxes, debt service, reserves, reinvestment, and any salary already included in payroll