Owner income$125k base

Owner income$125k baseLactate Threshold Testing Owner Income: $125K Salary Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$125k base  Net margin9% → 85%

Net margin9% → 85% Revenue for target pay$1.4M

Revenue for target pay$1.4M Business difficultyHard

Business difficultyHard

You’re pricing a sports testing service, so revenue alone won’t tell you what the owner can take home This model covers a US lactate threshold testing service over a five-year period, with $380k in first-year revenue, $527M by Year 5, operating costs, payroll, reserves, and owner pay before personal taxes

Owner income$125k baseNet margin9% → 85%Revenue for target pay$1.4MBusiness difficultyHardWant to test your owner-income target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Can the Lactate Threshold Testing Service support a $125K owner salary?

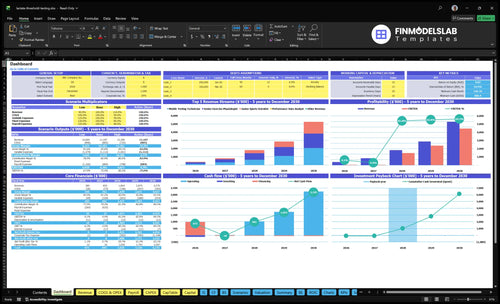

This Lactate Threshold Testing Service Financial Model Template screenshot is a scenario check, not a pitch: it shows revenue forecast, EBITDA, cash need, payback, and owner salary. It also includes $150 to $400 Year 1 pricing, 45% to 55% capacity, $79k monthly overhead, and $120k startup assets. Open the model.

Owner-pay model highlights

- Owner pay versus cash reserve

- Revenue by delivery role

- Margin bridge by scenario

- Low, base, high cases

What profit margin can a lactate threshold testing service reach?

If you price a Lactate Threshold Testing Service well, the core model can show a very high EBITDA margin, but that still doesn’t mean the owner can take all the cash. What Are Operating Costs For Lactate Threshold Testing Service? matters because direct consumables are $950 per test, while marketing, referral commissions, fuel, travel, payroll, reserves, and owner distributions all hit what’s left.

Cost drivers

- $650 for strips and lancets

- $300 for calibration and consumables

- 80% of revenue for marketing and referrals

- 50% for fuel and travel

Cash flow layers

- $79k monthly fixed overhead before payroll

- 92% EBITDA margin in Year 1

- 845% EBITDA margin in Year 5

- Cash to owner still depends on reserves

Can a lactate threshold testing business scale beyond the owner?

Yes—the Lactate Threshold Testing Service can scale beyond the owner, but it turns into a utilization business fast. In the stated plan, headcount grows from 2 senior exercise physiologists, 1 junior sports scientist, and 2 mobile testing technicians in Year 1 to 8, 10, and 12 by Year 5, while revenue rises from $380k to $527M. That works only if mobile team sessions, endurance team contracts, coaching partnerships, and technician-led testing keep the calendar full; if travel, quality control, reporting, or acquisition cost outrun booked tests, owner take-home drops.

Why it can scale

- Mobile testing reaches more athletes.

- Team contracts add repeat volume.

- Coaching partnerships feed referrals.

- Technicians lift session capacity.

What hurts margin

- Travel cuts paid hours.

- QC adds time per test.

- Reporting slows throughput.

- Low utilization hurts take-home.

How many lactate threshold tests per week are needed?

For the Lactate Threshold Testing Service, Year 1 needs about 38 tests per week — or 163 per month — with 2 senior exercise physiologists, 1 junior sports scientist, and 2 mobile testing technicians running at 45% to 55% utilization. At about $194 per completed test, that points to roughly $380k in annual revenue. By Year 5, the plan rises to about 459 tests per week, but that scale gets tight because of setup, athlete briefing, blood sampling, cooldown, reporting, travel, and retest scheduling.

Year 1 load

- 163 completed tests monthly

- 38 tests needed weekly

- 2 senior exercise physiologists

- $194 revenue per test

Year 5 pressure

- 1,989 tests per month

- 459 tests per week

- Capacity gets tight fast

- Travel and retests slow throughput

Want the six levers that drive owner income?

1

38-459/wkWeekly Tests

More weekly tests drive most of the owner take-home, and the model scales fast from launch to Year 5.

2

$176-$215Athlete Price

A higher price per athlete drops straight into income because direct test costs stay low versus the fee.

3

87%-93%Gross Margin

Strips, lancets, calibration, travel, and commissions leave most of each test to cover profit and owner pay.

4

$7.9K/moFixed Overhead

Rent, insurance, software, hosting, and telecoms run about $7.9K a month before wages, so cash stays tight until volume builds.

5

HighRepeat Rate

More retests keep athletes on the calendar and raise revenue without resetting the whole sales effort.

6

$125KOwner Model

The modeled owner salary is $125K, so take-home depends on whether the founder stays in delivery or delegates that work.

Lactate Threshold Testing Service Core Six Income Drivers

Testing volume and appointment utilization

Testing volume and appointment utilization

More completed lactate threshold tests per week raise owner take-home because fixed costs get spread over more billed appointments. The model starts at 55% utilization for senior exercise physiologists, 50% for junior sports scientists, and 45% for mobile testing technicians in Year 1, then climbs to 85%, 85%, and 80% by Year 5.

Capacity is not just booked slots. Realistic testing time must include setup, athlete briefing, blood sampling, cooldown, travel, data cleanup, and reporting. Missed appointments hit hard because rent, software, insurance, and salaries still run, even when a test no-shows.

Track show rate and usable test hours

Measure booked tests, completed tests, and show rate by staff type every week. Then compare real utilization to the Year 1 base and Year 5 ceiling so you can see where idle time sits and where owner pay is leaking.

- Booked tests

- Completed tests

- Show rate by role

- Travel and reporting time

To improve income, tighten reminders, block enough time for reporting, and keep travel windows realistic so one late athlete does not wipe out the next slot. If the schedule looks full but completions stay low, cash flow stays thin and fixed overhead keeps eating margin.

1

Average revenue per athlete test

Average Revenue per Athlete Test

Income rises when each completed test carries a higher ticket price. Here, Year 1 listed prices are $250 for senior-led testing, $175 for junior-led testing, and $150 for mobile technician testing, with a blended revenue per completed delivery test of about $194. That blend matters because it sets how much cash each booked athlete adds before overhead and owner pay.

At 163 tests a month, that blend implies about $31.6k in monthly revenue. By Year 5, prices rise to $310, $215, and $180, so the owner’s income depends on keeping the right mix of premium and lower-touch visits, not just adding volume. If the mix shifts toward cheaper tests, take-home drops fast.

Price the Test Mix, Not Just the Headcount

Track completed tests, service mix, and average price per test every month. The key inputs are test type, package scope, and local willingness to pay. A senior-led test should not be priced like a mobile technician visit, because report depth and expertise are different.

Test pricing locally before hiring ahead of demand. If athletes accept the $250 and $175 offers today, the blended average can hold near $194; if discounting is needed to fill slots, owner cash shrinks even when bookings look busy. One clean rule: price has to cover the test, the time, and the profit draw.

2

Repeat testing and athlete retention

Repeat testing lifts retention

Repeat lactate testing turns one athlete into a recurring client instead of a one-time lead. That matters because completed volume rises from about 163 tests per month in Year 1 to 1,989 in Year 5, so more revenue comes from booked retests and less from fresh marketing. The key inputs are athletes retained, retest timing after training blocks, and completed test count.

Here’s the cash-flow angle: retests are easier to plan, so utilization stays steadier and owner pay gets less choppy. If retests slip, the gap shows up fast in sales, because the model still needs enough new leads to fill the calendar. One delayed retest can be small; a weak repeat rate across the base can cut monthly tests and pressure profit.

Track retest rate by training block

Measure how many athletes return within the planned retest window after a block, then compare that against monthly capacity. A simple rule helps: if repeat bookings fall, marketing has to replace them, and that usually costs more than keeping the athlete warm with a package. Retest packages also improve forecasting, but keep performance claims cautious if timing drifts.

Watch repeat tests per month, utilization, and days between tests. If the calendar is thin, push pre-booked retests before the first test ends, and tie follow-up dates to the athlete’s training cycle. That keeps revenue more stable and protects take-home income without adding as much lead-gen spend.

3

Gross margin per lactate test

Gross Margin per Test

Gross margin per lactate test means what’s left after strips and lancets, calibration, reporting time, payment fees if you add them, and travel tied to that visit. In Year 1, direct consumables are $950 per test: $650 for strips and lancets plus $300 for calibration. At a $194 blended revenue per completed test, the test-level margin is negative before fixed overhead or owner pay.

By Year 5, direct consumables fall to $650 per test, but marketing and travel still run at 90% of revenue, down from 130% in Year 1. So the owner’s take-home depends on getting each test below price; if the per-test stack stays too high, more volume can still drain cash instead of funding profit.

Cut Test-Level Cost

Measure margin by test type, route, and staff mix. Keep fixed overhead and equipment reserves out of the per-test math so you can see the real contribution from each completed test.

- Track strips and lancets separately.

- Log calibration cost per test.

- Time reporting minutes per athlete.

- Measure travel cost per visit.

- Compare all costs to test price.

If marketing and travel stay near 130% of revenue in Year 1, cash burn will crowd out owner draw. Batch nearby visits, charge for travel-heavy jobs, and cut report time before adding more tests or staff.

4

Fixed overhead and equipment reserves

Fixed Overhead and Equipment Reserves

This business carries $79k per month in fixed overhead: $45k rent, $12k vehicle fleet insurance, $850 scientific software, $600 professional liability insurance, $450 data hosting, and $300 telecom. It also ties up $120k in startup assets, including the vehicle, testing equipment, software build, power systems, furniture, and IT. If test volume dips, this cost stays fixed, so owner take-home can get squeezed fast.

Here’s the quick ma th: income only flows to the owner after contribution covers fixed burn. In equipment-heavy testing, reserves are not optional profit; they are replacement cash for worn gear and downtime risk. If the vehicle, meter, or software stack fails and there is no reserve, cash flow drops and the owner may have to cut pay to keep the service running.

Track Burn Before You Draw Pay

Track fixed overhead, reserve funding, and cash on hand as separate lines. Set a replacement calendar for the vehicle, testing equipment, software, power systems, furniture, and IT, then fund it monthly. One clean rule: if the reserve balance is thin, owner pay is too high. That keeps equipment replacement from eating the next month’s income.

Watch booked tests against the $79k monthly overhead load. If appointments slip, cut nonessential spend fast and avoid adding staff or gear before utilization supports it. Missed bookings hurt twice here: revenue falls, but rent, insurance, software, and telecom still run, so the gap comes straight out of profit and owner draw.

5

Owner role and labor leverage

Owner Labor Leverage

An owner-led lactate testing model keeps more contribution per test because the owner is doing the science work instead of paying another lead. But it also caps volume, so income rises only until the owner’s calendar fills. The Year 1 payroll base includes a $125k CEO and Head of Science salary, plus a $75k operations manager and admin support, so owner pay depends on whether those roles add enough booked tests.

By Year 5, staffing expands into senior exercise physiologists, junior sports scientists, mobile technicians, analysts, and program directors. That can lift revenue if technician utilization stays high, but payroll turns into cash drag when hiring runs ahead of demand. More staff only helps when test volume keeps pace.

Track tests per paid hour

Measure completed tests per tester-hour, booked utilization, and payroll per completed test. The key inputs are owner hours, technician hours, test capacity, and actual bookings. If utilization slips, the business pays for idle labor and owner take-home falls even when reported revenue looks better. Here’s the quick check: add payroll only when booked tests are already filling current capacity.

Use role-by-role staffing targets before you hire. Tie each new senior exercise physiologist, junior sports scientist, or mobile technician to a test count forecast, not hope. If the schedule cannot absorb the added hours, keep the work owner-operated longer. That protects contribution and avoids turning growth into lower owner cash.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income swings fast here because test volume, staffing, and utilization rise together, while fixed lab, vehicle, and software costs stay in place.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | This is a low-earnings launch path with tight volume and early cash pressure. | This is the modeled growth path with stronger earnings and better operating spread. | This is the stronger upside path with much higher throughput and larger earnings potential. |

| Typical setup | Year 1 revenue is $380,000, EBITDA is $35,000, volume is about 38 weekly tests, and the owner salary line is $125,000, which works out to about a 9.2% EBITDA margin. | Year 3 revenue is $1,824,000, EBITDA is $1,477,000, volume is about 172 weekly tests, and higher utilization supports wider distribution and more staff coverage. | Year 5 revenue is $5,270,000, EBITDA is $4,453,000, volume reaches about 459 weekly tests, and the model needs a much larger team with tighter delivery control. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $125,000Low case | $1.48MBase case | $4.45MHigh case |

| Best fit | Use this if you want a conservative launch view and need to stress-test cash in the first operating year. | Use this as the core planning case for a growing regional service with strong utilization. | Use this to test scale, hiring complexity, and whether demand can absorb a much bigger field team. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Lactate Threshold Testing Service Porter's Five Forces Analysis

- Lactate Threshold Testing Service BCG Matrix

- Lactate Threshold Testing Service Business Model Canvas

- What Are The 5 KPI Metrics For Lactate Threshold Testing Service?

- Lactate Threshold Testing Service Business Plan Template in Pre-Written Word

- How Increase Profits For Lactate Threshold Testing Service?

- What Are Operating Costs For Lactate Threshold Testing Service?

- How Much It Costs To Start A Lactate Threshold Testing Service: $806k

- Lactate Threshold Testing Service Financial Model Template in Excel

- How To Open A Lactate Threshold Testing Service In 6 To 10 Weeks

- How To Write A Business Plan For Lactate Threshold Testing Service?

- Lactate Threshold Testing Service Marketing Mix

- Lactate Threshold Testing Service Marketing Plan

- Lactate Threshold Testing Service Business Proposal

- Lactate Threshold Testing Service PESTEL Analysis

- Lactate Threshold Testing Service Pitch Deck Example Editable PPTX

- Lactate Threshold Testing Service Business SWOT Analysis

- Lactate Threshold Testing Service Value Proposition Canvas

Frequently Asked Questions

This model shows a minimum cash need of $806k, with the low point in Month 2 Startup assets total $120k before working capital, including a vehicle, testing equipment, software build, lab furniture, IT, and power systems That cash need is separate from the owner’s $125k modeled salary and any future distributions