Owner income$438k–$19.2M

Owner income$438k–$19.2MHow Much Laser Safety Goggles Business Owners Make: $438k EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$438k–$19.2M  Net margin31.8%–79.1%

Net margin31.8%–79.1% Revenue for target pay$115k/mo–$2.0M/mo

Revenue for target pay$115k/mo–$2.0M/mo Business difficultyHard

Business difficultyHard

Laser safety goggles business owner earnings can be meaningful, but they’re not the same as revenue or EBITDA In the researched base case, the business generates $1376M revenue and $438k EBITDA in the first year, rising to $24234M revenue and $19160M EBITDA by Year 5 That EBITDA is the pre-tax operating profit pool before debt service, reinvestment, and owner distributions Actual laser safety goggles owner take-home depends on inventory needs, payroll, marketing spend, reserves, and whether the owner is paid through salary, draws, or both

Owner income$438k–$19.2MNet margin31.8%–79.1%Revenue for target pay$115k/mo–$2.0M/moBusiness difficultyHardWant to test your laser eyewear profit?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Want the full Laser Safety Goggles Sales forecast?

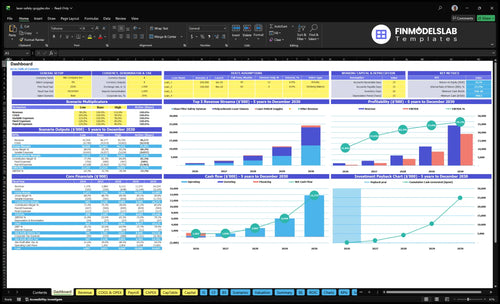

The Laser Safety Goggles Sales Financial Model Template shows dashboard, revenue build, and owner pay; charts span revenue from $1,376M to $24,234M and EBITDA from $438k to $19,160M. Open it.

Owner-income model highlights

- Sales assumptions and channels

- Gross margin, CAC, repeat buyers

- Inventory, fixed costs, payroll

- EBITDA, cash need, payback

- Working capital and distributions

Are laser safety goggles profitable to sell?

Yes—Laser Safety Goggles Sales can be profitable if it keeps procurement tight, sells to qualified buyers, and avoids slow stock; see How Much To Start Laser Safety Goggles Sales Business?. Here’s the quick math: first-year gross margin is 880%, and after 50% shipping and 29% payment processing, contribution margin is about 801%. Year 5 improves to about 853% as procurement falls to 80%, quality control to 12%, shipping to 30%, and payment fees to 25%; CAC starts at $45 and drops to $35.

Margin drivers

- 880% first-year gross margin

- 801% contribution margin

- 853% by Year 5

- $45 CAC, then $35

Cash risk

- Slow SKUs trap cash

- Wavelength mix must stay tight

- Optical-density stock can sit

- Paid acquisition still matters

Can a laser safety goggles business be scaled?

Yes, Laser Safety Goggles Sales can scale if larger commercial accounts, repeat buys, and better supplier terms grow contribution faster than payroll, inventory, and marketing. Here’s the quick math: revenue rises from $1.376M to $24.234M, EBITDA from $438k to $19.16M, while payroll moves from $370k to $765k, marketing from $120k to $400k, and fixed overhead stays at $9,750/month.

What drives scale

- Sell to larger commercial accounts

- Grow repeat purchasing

- Improve supplier terms

- Automate sales and stock tasks

What can break it

- Too many SKUs too soon

- Inventory growth before demand

- Payroll rising faster than sales

- Owner pulled away from supplier control

How many laser safety goggles do I need to sell to make a living?

For Laser Safety Goggles Sales, you need about $895k revenue, or roughly 1,869 orders and 4,673 units per year, to support a separate $110k owner-pay target; for the planning setup, see How Do I Write A Business Plan For Laser Safety Goggles Sales?. Here’s the quick math: $479 AOV with about 80.1% contribution must cover $117k fixed overhead, $120k marketing, $370k payroll, and $110k owner pay.

Sales target

- $895k annual revenue target

- 1,869 orders per year

- 4,673 units per year

- $479 average order value

Owner-pay caveat

- $110k General Manager proxy

- Revenue falls if owner fills that role

- Inventory reserves still reduce cash

- Taxes still reduce take-home pay

What drives laser goggles owner income?

1

$1.4M-$24.2MOrder Volume

More orders are the biggest income swing, and revenue rises from $1.376M in Year 1 to $24.234M in Year 5.

2

88%Gross Margin

About 88% gross margin keeps room for profit, but small cost leaks hit take-home fast.

3

$479Order Value

Average order value (AOV) is about $479, so upsells and mix shifts lift revenue without more traffic.

4

$45Acquisition Cost

CAC near $45 keeps paid growth efficient and shortens the payback window.

5

$9.8K/moInventory Control

Fixed overhead is $9,750 a month, so stock, packing, and freight waste can eat cash quickly.

6

15%-40%Repeat Share

Repeat customers grow from 15% to 40%, so reorders lower acquisition pressure and raise lifetime value.

Laser Safety Goggles Sales Core Six Income Drivers

Qualified Order Volume

Qualified Order Volume

Qualified order volume is the number of real buyers who need the right wavelength and optical density protection, not just site visitors. Using the provided first-year revenue of about $1.376M and $479 AOV, the math points to about 2,874 orders a year, or 240 orders a month. That order base is what funds owner pay, so weak intent traffic can hurt income even when clicks look strong.

The best demand comes from labs, clinics, manufacturers, universities, service companies, and laser operators. Here’s the risk: traffic alone is not income unless conversion, CAC, and margin work. If orders do not match the stocked product range, support cost and returns rise, and gross profit gets less predictable.

Measure Intent, Not Just Clicks

Track orders by buyer type, wavelength need, and optical density request, then compare that to conversion rate and CAC. If a channel brings broad safety traffic instead of buyers who know their spec, it is not helping owner pay. One clean test: count how many leads can name the laser use case before sales follow-up.

Use the stock list to qualify demand faster. Tight product match lowers wasted quotes, cuts returns, and keeps gross profit steadier. For this model, the goal is simple: more of the 240 monthly orders should come from buyers who fit what is already stocked, so cash from sales turns into usable profit instead of support work.

1

Average Order Value

Average Order Value

Average Order Value rises when buyers add multiple pairs or move into higher-priced product types for real safety needs. The disclosed benchmark climbs from $479 in year 1 to $966 in year 5, so each order throws off more gross profit and gives more room for owner pay. If AOV stays flat, CAC and fixed costs take a bigger bite of each sale.

The inputs are units per order, weighted unit price, and product mix. Here, AOV moves with 25 units at about $192 weighted price, then 40 units at $242. That only helps when the add-on is tied to wavelength, optical density, fit, or a true replacement need; otherwise returns and support drag margin.

Track order mix by use case

Track order size, mix, and repeat baskets each month. Push bulk lab orders, specialty frames, storage cases, and replacements only after the spec is confirmed. One rule keeps income clean: no upsell without a documented safety reason.

Bigger baskets should lower the pressure on paid traffic and help cash cover fixed costs, but only if support time and returns stay controlled. If add-ons raise service load or create spec mistakes, owner income drops even when revenue looks better.

- Measure units per order monthly.

- Split AOV by buyer type.

- Track replacements versus first buys.

- Approve add-ons by safety need.

2

Gross Margin

Gross Margin

Gross margin is the cash left after product cost and quality control, and it’s what pays for marketing, payroll, reserves, and owner pay first. In this model, gross margin is 880% in year 1 and 908% in year 5, driven by 100% wholesale procurement dropping to 80% and quality control falling from 20% to 12%.

The real risk is margin leak from discounting, returns, and bad spec matches. If the eyewear does not fit the buyer’s laser wavelength or optical density needs, the sale can turn into a return or a discount fast, and that hits owner income before overhead is even paid.

What to control

Track landed cost, supplier terms, QC cost, return rate, and discount rate by SKU. Gross margin only helps if the right product ships the first time, with the right wavelength and protection rating.

- Match spec sheets to each buyer.

- Cut returns on wrong OD or wavelength.

- Review margin by product type monthly.

- Protect pricing on urgent orders.

Use the margin pool to fund growth, but don’t let broad traffic or weak fulfillment eat it. Cleaner orders with fewer credits, swaps, and fixes leave more cash for owner pay.

3

Customer Acquisition Efficiency

Customer Acquisition Efficiency

When acquisition works, ad spend turns into qualified laser safety goggle orders, not random clicks. Judge marketing against contribution margin and payback—the time it takes gross profit to cover CAC (customer acquisition cost). With annual marketing spend rising from $120k to $400k and CAC falling from $45 to $35, the owner keeps more cash for payroll and profit.

At about $479 AOV, there is enough gross room for a $45 CAC if returns and support stay controlled. The risk is paying for broad safety-equipment traffic that never matches wavelength or optical density needs, so the business buys education clicks instead of real buyers.

Lower Wasted Spend

Track CAC by channel, quote-to-order rate, return rate, and support time. Here’s the quick math: CAC = marketing spend ÷ new customers. If paid search, search content, marketplace listings, fast RFQ replies, spec sheets, and trust signals cut waste, first-year contribution near 801% gives more room for owner draw and overhead.

- Split search by laser intent.

- Measure RFQ speed daily.

- Block low-intent traffic.

- Watch returns and support cost.

If CAC falls from $45 to $35, each new buyer leaves $10 more before fixed costs. That only helps income if the order is qualified, the product matches the laser need, and post-sale service does not eat the margin.

4

Inventory And Fulfillment Control

Inventory and Fulfillment Control

When stock is too deep, owner pay gets trapped in boxes instead of cash. Here, $120k of initial inventory and a $760k cash peak in Month 2 show why EBITDA can look fine while bank cash is tight.

The key inputs are SKU depth by wavelength, optical density rating, frame type, and use case. Get that mix wrong and you get stockouts, slow-moving items, returns, and obsolete stock. With first-year shipping at 50% of revenue and payment fees at 29%, fulfillment choices can decide how much cash the owner can actually take home.

Track Reorder Timing, Not Just Sales

Watch sell-through by SKU, not just total orders. Match replenishment to the real order mix so cash is not locked in slow movers. Separate EBITDA from cash tied up in stock, then forecast Month 2 liquidity against the $760k peak. That keeps owner draws tied to cash, not paper profit.

Use a simple control list: fast movers, slow movers, and obsolete items. Cut depth on SKUs that do not match current wavelength or optical density demand, and protect stock for repeat-use cases. When inventory depth fits demand, the business can absorb 50% shipping and 29% payment fees with less cash strain.

5

Repeat And Commercial Account Mix

Repeat And Commercial Mix

Repeat and commercial account mix means the share of sales from clinics, universities, labs, manufacturers, and service firms that buy again. That matters because repeat customers are 150% of new customers in Year 1, 300% in Year 3, and 400% in Year 5. With lifetime rising from 24 to 48 months, acquisition cost gets spread over more orders.

Here’s the quick math: repeat orders rise from 0.08 to 0.18 per month, so a buyer goes from about 1.0 annual order to 2.2. That lifts cash flow and owner pay only if the orders are real. Do not call it subscription revenue unless contracts actually exist.

Track Reorders By Account

Track repeat share by cohort, orders per repeat customer, and commercial account mix. Split accounts by industry and watch who reorders inside 24 months versus 48 months. That shows where to spend on follow-up, support, and sales time.

- Tag replacement timing by use case.

- Bundle extra pairs for teams.

- Forecast cash from reorders.

Commercial accounts can place larger first orders and create replacement demand, so one account can beat several small one-off buyers. If repeat rates stay low, CAC stays heavy and payback stretches. The fix is disciplined follow-up, not discounting.

6

Compare low, base, and high owner-income planning scenarios

Owner income scenarios

Income changes fast here because revenue scales from a Year 1 ramp to a Year 5 commercial mix, while payroll, marketing, and inventory depth also rise.

| Scenario | Low CaseRamp case | Base CaseCore case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is a lower owner-income path built on the first-year ramp and tight cash control. | This is the modeled operating case at Year 3 scale and the first steady owner-income profile. | This is the stronger owner-income path tied to Year 5 scale and a much larger commercial mix. |

| Typical setup | Year 1 revenue is about $1.376M, or $115k a month, with 88.0% gross margin, $45 CAC, $120k marketing, $370k payroll, and $117k fixed overhead. | Year 3 revenue reaches about $6.112M with 89.4% gross margin, $40 CAC, $250k marketing, $567.5k payroll, and $3.992M EBITDA. | Year 5 revenue reaches about $24.234M with 90.8% gross margin, $35 CAC, $400k marketing, $765k payroll, and $19.160M EBITDA as sales shift toward glass-filter eyewear. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $438kRamp income | $3.992MCore income | $19.160MUpside income |

| Best fit | Use this to stress-test a slower launch, a lean owner role, and tighter cash needs. | Use this as the main plan if demand holds, repeat orders build, and the owner stays close to cash and inventory. | Use this to test a scaled operator plan, bigger inventory needs, and the cash load that comes with faster growth. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Laser Safety Goggles Sales Porter's Five Forces Analysis

- Laser Safety Goggles Sales BCG Matrix

- Laser Safety Goggles Sales Business Model Canvas

- What Are The Top 5 KPIs For Laser Safety Goggles Sales Business?

- Laser Safety Goggles Sales Business Plan Template in Pre-Written Word

- How Increase Laser Safety Goggles Sales Profitability?

- What Are Operating Costs For Laser Safety Goggles Sales?

- Laser Safety Goggles Startup Costs: $760K Funding Need

- Laser Safety Goggles Sales Financial Model Template in Excel

- How To Open A Laser Safety Goggles Sales Business In 6-12 Weeks

- How Do I Write A Business Plan For Laser Safety Goggles Sales?

- Laser Safety Goggles Sales Marketing Mix

- Laser Safety Goggles Sales Marketing Plan

- Laser Safety Goggles Sales Business Proposal

- Laser Safety Goggles Sales PESTEL Analysis

- Laser Safety Goggles Sales Pitch Deck Example Editable PPTX

- Laser Safety Goggles Sales Business SWOT Analysis

- Laser Safety Goggles Sales Value Proposition Canvas

Frequently Asked Questions

The researched model shows $438k of first-year EBITDA on $1376M revenue, rising to $19160M EBITDA on $24234M revenue by Year 5 That is not guaranteed take-home The owner still has to fund taxes, inventory, debt service, reserves, and any reinvestment before taking distributions