Owner income$180k+

Owner income$180k+How Much Does A Legal Services Business Owner Make? $180k Plan

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180k+  Net margin16.5%

Net margin16.5% Revenue for target pay$659k

Revenue for target pay$659k Business difficultyHard

Business difficultyHard

You’re not comparing lawyer salaries here you’re modeling law firm owner take-home pay from a US legal services firm This page uses a $180,000 founding attorney salary, Year 1 EBITDA of $109,000, a Month 6 breakeven point, and a required minimum cash cushion of $800,000 Owner pay means salary plus any draw only after payroll, overhead, reserves, and reinvestment

Owner income$180k+Net margin16.5%Revenue for target pay$659kBusiness difficultyHardWant to test your own owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

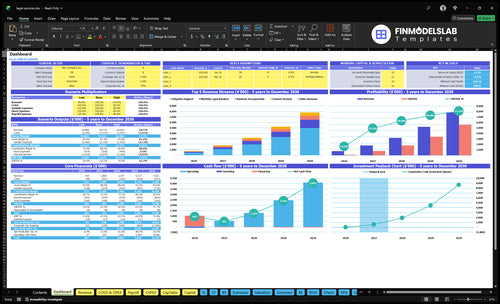

Want to check owner income in the Legal Services model?

This dashboard shows owner take-home, revenue, margin, costs, reserves, and assumptions. See the full Legal Services Financial Model Template and open the model.

Owner-income model highlights

- Owner income forecast

- EBITDA and breakeven

- Scenario charts and assumptions

What affects law firm owner income the most?

If you’re looking at Legal Services, the biggest swing in owner income comes from collections rate, realization rate, and billable utilization; the launch-cost side is here: What Is The Estimated Cost To Open And Launch Your Legal Services Business? Matter mix matters too, because Year 1 leans 40% incorporations at $250 and 20% litigation support at $350, while Year 5 shifts to 40% litigation and 35% retainers at $280.

Top income drivers

- Collections decide cash in hand.

- Realization cuts billed write-downs.

- Utilization lifts billable hours.

- Reserves protect take-home pay.

Mix and overhead

- Year 1 mix: 40% incorporations.

- Year 1 litigation support: 20%.

- Year 5: 40% litigation, 35% retainers.

- Payroll, marketing, insurance, software, rent matter.

How much revenue does a law firm need to pay the owner?

Legal Services needs about $659,000 in collected revenue in Year 1 to pay a $180,000 owner salary and still produce $109,000 in EBITDA, assuming 28% variable costs, $105,600 fixed overhead, and $260,000 payroll. Here’s the quick math: revenue equals EBITDA + fixed costs + payroll, then divide by the 72% contribution margin. No single multiple works, because litigation, retainers, incorporations, and contract review use different hours and rates.

Revenue math

- $659,000 revenue target

- 28% variable cost load

- 72% contribution margin

- $474,600 covers profit, overhead, payroll

What drives it

- $180,000 owner pay inside payroll

- $105,600 fixed overhead

- Different matters have different billing math

- Use collected revenue, not booked revenue

Is a solo law firm more profitable than hiring associates?

A solo Legal Services firm can look more profitable at first because payroll stays low, but owner income hits a ceiling once capacity fills up. In this model, associate FTE grows from 0.5 in Year 2 to 2.0 in Year 5, and associate payroll rises from $55,000 to $220,000. The leverage only works if new staff turn into collected revenue faster than they add salary, supervision, software, and marketing cost.

Solo margin

- Lower payroll lifts margin

- Owner keeps more revenue

- Capacity still caps income

- One lawyer can only sell so many hours

Hiring test

- Year 2: 0.5 associate FTE

- Year 5: 2.0 associate FTE

- Payroll grows to $220,000

- Revenue must outpace added cost

Want the six drivers that move owner income?

1

$659KFee Volume

More matters and retainers lift the $659K Year 1 revenue base, so this is the cleanest way to raise owner take-home.

2

$109K-$5.6MStaffing Leverage

As the team scales from the founder to added support and attorneys, take-home rises fast only if billable work stays full.

3

$220-$390Pricing Power

Hourly rates run from $220 to $390, so even small price gains flow straight into profit.

4

2-19 hrsUtilization

Billable hours vary from 2.0 to 19.0, so better utilization spreads fixed overhead across more fee work.

5

$25K/$350Acquisition Cost

Year 1 marketing is $25,000 and CAC is $350, so cheaper lead flow protects margin and cash.

6

$105.6K/$800KCash Buffer

Fixed overhead is $105.6K a year and minimum cash is $800K, so reserve control decides how much can be paid out early.

Legal Services Core Six Income Drivers

Collected Fee Volume

Collected Fee Volume

Owner income starts with cash collected, not invoices sent. With Year 1 collected revenue at $659,000, that is about $54,900 per month; a 5% miss is about $33,000 less cash before owner distributions. Track collection rate, retainer balances, payment timing, write-offs, and bad debt, because unpaid work does not fund draws.

This driver includes hourly fees, flat fees, and retainers only after cash lands. The key inputs are billed work, cash received, and the gap between service and payment. If collections slow, reported revenue can look fine while owner pay gets squeezed. One late payer can ripple through payroll, rent, and planned distributions.

Protect Cash Conversion

Use clear intake terms, retainer deposits, and firm due dates to keep cash moving. Watch collection rate by client type and matter type, then act fast on weak accounts. If retainers stay funded, the owner has steadier draw capacity; if payment terms are loose, cash turns into a delay, then a haircut.

- Cash collected each month

- Retainer balance by client

- Write-offs and bad debt

- Invoice-to-cash timing

Set a weekly cash report and compare it to the EBITDA model. If collection miss starts near 5%, owner pay can fall by about $33,000 on this base. That is the number that tells you when to tighten terms, ask for deposits, or pause work until accounts are current.

1

Practice Area And Pricing Mix

Practice Mix Sets the Cash Rate

Practice area mix changes both revenue speed and margin. In Year 1, the firm prices business incorporation at $250 an hour, litigation support at $350, monthly retainers at $280, and contract review at $220. With a 40% / 20% / 15% / 25% mix, the weighted average is about $267 per hour. If litigation reaches 40% and retainers 35% by Year 5, billed revenue can rise, but only collected cash funds owner pay.

Track Collected Revenue by Matter Type

Measure this driver as matter count, billable hours, billed rate, and collected dollars by practice. Track how long each matter takes to collect, because retainer work can smooth cash while litigation can slow it. The clean test is collected revenue per hour by practice each month. If lower-rate work crowds out higher-rate work, or invoices sit unpaid, take-home income drops fast.

- Hours by practice area

- Collected cash by matter type

- Retainer balances on hand

- Write-offs and bad debt

- Days to collect by client

Push more time into higher-rate work only when payment terms are tight and collection stays clean. Retainers should be billed and collected on time, and litigation should be reviewed against realized hours so busy work does not fake profit. If a matter adds rate but not cash in the month, it does not help owner draws yet.

2

Utilization And Realization

Billable Hours That Stick

Utilization is the share of attorney time that can be billed, and realization is the share of billed work that becomes earned fees. In this model, the work mix shifts from 2 hours for incorporation, 15 for litigation support, 8 for monthly retainers, and 3 for contract review in Year 1 to 19 hours of litigation and 10 hours of retainers by Year 5. More billed hours only help owner pay if quality holds and write-downs stay low.

If litigation is billed at $350 an hour and retainers at $280, the math is simple: more realized hours lift earned fees before overhead. The risk is nonbillable time, discounting, and disputed work, because they cut gross margin and cash available for owner draw even when the schedule looks full.

Track Billable Time and Write-Downs

Measure utilization by attorney and matter type, then compare worked hours to billed hours and billed hours to earned fees. A low realization rate usually means weak scoping, slow time entry, or poor documentation, not just slow collections. If more work is done but fees do not rise, margin is leaking.

Set tighter matter budgets, review time weekly, and train staff to bill promptly and describe work clearly. Watch litigation and retainer work closely, because those hours rise from 15 to 19 and from 8 to 10. Better billing discipline protects owner take-home without adding headcount.

3

Staffing Leverage

Staffing Leverage

Staffing leverage means adding associates, paralegals, and support staff so the firm can bill more work, but each hire also adds fixed payroll. In this model, payroll rises from $260,000 in Year 1 to $635,000 in Year 5, so owner income improves only if the extra team produces more collected fee contribution than their salary plus supervision cost.

The quick test is simple: if a hire does not lift collected revenue, billable hours, or realization enough to cover their cost, the owner’s draw gets squeezed. A useful check is contribution per FTE after direct payroll and management time; more headcount is not more profit unless the work is priced and collected well.

Measure contribution before hiring

Track collected revenue per lawyer and staff member, plus billable hours, realization, and supervision time. Build the forecast from salary, expected billed hours, and collection rate, then compare the added contribution to the added payroll. If a new associate or paralegal only fills backlog but does not raise collected cash, owner pay usually falls before it rises.

- Year 1 payroll: $180,000 owner, $30,000 paralegal, $50,000 office manager

- Year 5 payroll: $635,000 total with 20 associates

- Watch: billable hours, realization, collections

- Stop: hiring when supervision eats margin

One clean rule: add people only when the next hire has a clear lift in collected fees, not just capacity. In legal work, the cash effect shows up fast if retainers, flat fees, or hourly matters cannot absorb the payroll step-up.

4

Client Acquisition Efficiency

Client Acquisition Efficiency

Client acquisition efficiency is how much you spend to win a retained client, not just a lead. The key inputs are marketing spend, intake conversion, referral share, and collected revenue per client. Year 1 marketing is $25,000 with $350 CAC; by Year 5 it rises to $110,000 while CAC improves to $270. Lower CAC only helps income if the firm can handle the added work cleanly.

Here’s the quick math: moving from $350 to $270 cuts acquisition cost by $80, or about 23%. That can free cash for owner pay, but only if the added matters are collected and not written off. Vanity leads don’t pay the owner; retained clients do. If deadlines slip or onboarding is slow, the cheaper lead still becomes an expensive client.

Track Retained Clients, Not Leads

Measure cost per retained client, intake conversion, referral share, and collected revenue per client every month. A lead list can look busy and still hurt cash flow if it does not turn into paying work. The real test is simple: does each marketing dollar bring in a client who pays on time and stays profitable after delivery costs and admin time?

Keep marketing tied to capacity. If the firm cannot serve more matters without write-offs or missed deadlines, then lower CAC just fills the queue and squeezes margins. Use clear intake payment terms and push referral channels that bring higher-quality clients, because better-fit clients protect collections and owner draw.

5

Overhead, Risk Costs, And Reserves

Overhead, Risk Costs, And Reserves

Fixed overhead of $105,600 a year comes out before owner draws: $54,000 rent, $14,400 professional liability insurance, $9,600 accounting, and $7,200 core software. So even when the firm is busy, this spend cuts cash that could have gone to the owner.

The cash risk is bigger early on. Required minimum cash is $800,000, and the low point is Month 2. Add launch capex of $83,500, and owner distributions should wait until required costs and reserves are covered, not after optional reinvestment.

Protect cash before paying draws

Track overhead in two buckets: required costs and optional spend. Here, the required base is $105,600 a year plus $83,500 of launch capex, so the owner needs a cash plan that keeps the balance above $800,000 through the Month 2 trough.

Use monthly cash forecasts, not profit alone. If a cost does not protect compliance, collections, or client work, delay it. That keeps owner pay tied to real cash and lowers the risk of taking draws before the firm can absorb overhead.

- Separate required and optional spend.

- Model cash weekly through Month 2.

- Block draws below $800,000.

- Review renewals before approval.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Legal services income moves with collections, matter mix, CAC, staffing, and cash reserves. Low, base, and high cases show how those levers change what the owner can safely pay themself.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | Lower collections, slower matter growth, and higher CAC keep the owner at salary only. | The modeled case starts at $659,000 Year 1 revenue, $109,000 EBITDA, Month 6 breakeven, and a 13-month payback. | The upside case assumes faster litigation growth, more retainer work, CAC near $270, and Year 5 EBITDA of $5.598 million. |

| Typical setup | Cash comes in slower, new matters build late, and the owner avoids extra draws beyond the $180,000 salary. | The firm balances incorporation, litigation support, retainers, and contract review while holding the $800,000 minimum cash plan. | Litigation and retainer work grow faster, CAC eases toward $270, and reserves stay intact as staff scales. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $180,000 salary onlySalary only | $180,000 plus modest drawPlanned draw | $180,000 plus strong upsideUpside draw |

| Best fit | Use this to stress-test weak collections, slow intake, and lean cash control. | Use this as the working plan for staffing, pricing, and reserve targets. | Use this to test a faster-growth plan with more capacity and higher owner take-home. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Legal Services Porter's Five Forces Analysis

- Legal Services BCG Matrix

- Legal Services Business Model Canvas

- 7 Essential KPIs to Track for Legal Services Firms

- Legal Services Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Legal Services Profitability Fast

- How Much Does It Cost To Run Legal Services Monthly?

- Cost To Start A Law Firm: $835K CAPEX Plus Runway

- Legal Services Financial Model Template in Excel

- How To Start A Law Firm In 8 To 16 Weeks With A Client-Ready Launch

- How to Write a Business Plan for Legal Services: 7 Steps

- Legal Services Marketing Mix

- Legal Services Marketing Plan

- Legal Services Business Proposal

- Legal Services PESTEL Analysis

- Legal Services Pitch Deck Example Editable PPTX

- Legal Services Business SWOT Analysis

- Legal Services Value Proposition Canvas

Frequently Asked Questions

The model plans a $180,000 founding attorney salary, plus possible draws after reserves Year 1 EBITDA is $109,000, but that does not mean the owner should take it all The firm also needs $800,000 minimum cash and absorbs $83,500 of launch capex, so early distributions should be conservative