Owner income$145K

Owner income$145KHow Much Can a Legionella Prevention Service Owner Make by Year 5?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$145K  Net margin47%–89%

Net margin47%–89% Revenue for target pay$309K

Revenue for target pay$309K Business difficultyHard

Business difficultyHard

You’re looking at a compliance-heavy water safety company where revenue can scale fast, but owner cash is not the same as sales This estimate uses a five-year operating model with $203M Year 1 revenue, $1410M Year 5 revenue, $145K annual CEO pay, and a $610K minimum cash need It covers revenue, margin, payroll, lab costs, insurance, equipment, reserves, and owner take-home before tax, but not tax planning or guaranteed distributions

Owner income$145KNet margin47%–89%Revenue for target pay$309KBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay. Use it to test how active clients, tier mix, audit fees, and direct service costs change cash left for the owner.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, reserves, and timing. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the model?

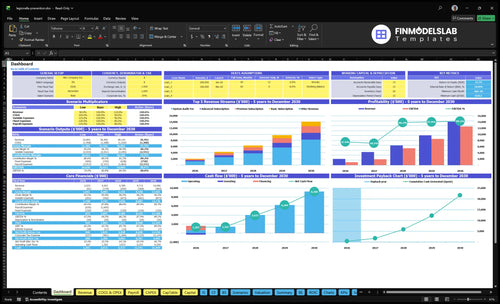

This Legionella Prevention Service dashboard shows revenue, EBITDA, owner pay, cash need, payback, and IRR; tabs include subscriptions, audits, lab costs, payroll, capex, reserves, and scenarios. Open the Legionella Prevention Service Financial Model Template.

Owner-income model highlights

- Owner pay is clear

- Revenue charts scale up

- 4-month break-even shown

- 10-month payback shown

- $610K cash floor

How much revenue does a Legionella prevention business need for owner pay?

The Legionella Prevention Service needs revenue high enough to cover $145K owner pay after 85% variable plus lab costs, $150K fixed overhead, $550K payroll, and $120K marketing. Here’s the quick math: a $145K owner salary is 71% of $203K revenue, not $203M, so that ratio only works if the revenue figure is a typo. Break-even lands in Month 4 only if the sales ramp is strong and cash reserves hold.

Cost stack

- $150K fixed overhead

- $550K payroll

- $120K marketing

- 85% variable and lab costs

Pay math

- $145K owner pay target

- Month 4 break-even timing

- Strong sales ramp needed

- Cash reserves must hold

How much does a Legionella prevention service owner make?

A Legionella Prevention Service owner can model $145K as CEO salary, but extra owner distributions depend on cash left after reserves, taxes, capex, and debt payments; see How To Launch Legionella Prevention Service Business? for the setup path. Year 1 shows $203M revenue and $955K EBITDA, but EBITDA is not guaranteed take-home pay.

Owner Pay

- Modeled CEO salary: $145K

- Year 1 EBITDA: $955K

- EBITDA is not cash pay

- Distributions need cash surplus

Scale Case

- Year 5 revenue: $1410M

- Year 5 EBITDA: $1258M

- Contract base drives scale

- Debt and capex reduce payouts

What Legionella prevention service costs most affect profit margin?

For Legionella Prevention Service, the biggest margin drag is lab analysis and testing kits at 45% of Year 1 revenue, easing to 35% by Year 5, and the profit tradeoff is clear in How Increase Profits For Legionella Prevention Service?. Sales commissions and processing also stay heavy, falling from 40% to 30%, while payroll rises from $550K to $143M as the team scales.

Big cost drains

- Lab analysis and kits: 45% Year 1

- Lab analysis and kits: 35% Year 5

- Sales commissions and processing: 40% to 30%

- Watch variable cost mix closely

Scale costs to watch

- Payroll grows from $550K to $143M

- Fixed overhead starts at $125K monthly

- Early capex totals $345K

- Capex covers vehicles, lab setup, IT, furniture

Want the six income drivers at a glance?

1

$2.0M-$14.1MContract Base

Subscriptions and audits build the cash base, lifting revenue from $2.0M in Year 1 to $14.1M in Year 5 as renewals stack.

2

4.5%-3.5%Lab Costs

Lab kits run at 4.5% of revenue in Year 1 and 3.5% in Year 5, so tighter test control drops more gross profit to EBITDA.

3

$2.8K-$3.6KPremium Margin

Higher-ticket remediation and premium work at $2.8K to $3.6K gives more room after labor, so take-home rises.

4

4xRoute Density

Field techs scale from 2 to 8 FTE, so dense routes and high utilization decide whether wage growth turns into profit.

5

$950-$3.6KMix Shift

Moving accounts from basic to advanced and premium raises average monthly revenue because plan prices span $950 to $3,600.

6

$150KOverhead Control

Fixed overhead is about $150K a year, and the $610K cash trough in Month 4 means reserve discipline matters as much as spend control.

Legionella Prevention Service Core Six Income Drivers

Recurring Contract Base

Recurring Contract Floor

Recurring Legionella compliance contracts set the monthly income floor. Year 1 pricing runs from $950 for Basic to $1,850 for Advanced and $3,200 for Premium, so the contract mix drives how much cash lands before any project work. By Year 5, the mix shifts to 45% Advanced and 25% Premium, which lifts average monthly revenue per account to about $1,918.

Here’s the quick math: the Year 5 mix leaves 30% Basic, 45% Advanced, and 25% Premium. That raises revenue quality, but only if churn stays low and renewals are not missed. Scope creep and underpriced reporting work hit gross margin fast, so the owner’s take-home depends on keeping each contract tied to a clear service scope and a clean renewal calendar.

Protect Renewal Value

Track active contracts, tier mix, renewal month, and realized monthly fee. If the mix moves toward Advanced and Premium, forecast cash flow and owner pay from the weighted fee, not just the logo count. One clean metric to watch is monthly recurring revenue per account; if it slips, churn or discounting is usually the cause.

Price reporting, retesting, and extra site work separately. Use a renewal checklist so each account has a defined scope, service frequency, and document load. If a client wants more sampling, more reports, or faster turnaround, price it into the next tier or a change order. That keeps recurring cash predictable and stops hidden labor from eating profit.

1

Testing Volume And Lab Cost Control

Testing Volume and Lab Cost Control

Legionella testing volume drives revenue, but each extra sample also adds third-party lab and kit cost. In the model, lab analysis and testing kits are 45% of revenue in Year 1 and ease to 35% by Year 5. That spread is the margin story: higher test counts help cash flow only if pricing covers sample volume, retests, and travel.

Track samples per site, retest rate, and revenue per route. If testing and remediation are blended, margin gets blurred and owner pay gets less predictable. Here’s the quick math: every point of lab cost saved flows straight into gross profit, while uncontrolled retests or small one-off visits can eat the gain.

Protect Testing Margin

Price retests separately and set sample-count limits in the contract. Use route batching so one trip covers more sites, and keep markup discipline on kits and analysis. The owner should forecast revenue using site count, scheduled samples, and expected retests, then compare actual lab spend to the 45% to 35% target band.

Track lab cost per sample.

Review retests weekly.

Batch nearby service calls.

Separate testing from remediation.

What this estimate hides: rush orders, failed samples, and extra documentation can raise cost fast. If testing volume rises but markup stays flat, owner take-home falls even when top-line revenue looks better.

2

Remediation And Treatment Project Margin

Remediation Project Margin

Legionella remediation can lift revenue when testing finds a problem, but profit depends on what the project really costs. Each job should include shock chlorination, flushing, retesting, technician hours, supervisor review, and client reporting. If you miss change orders or undercount documentation time, the sale looks good but owner take-home falls because rework, liability, and callback risk eat the margin.

Here’s the quick math: revenue only matters after direct costs. A corrective job can turn weak fast when labor, chemicals, and retests stack up, while the business still carries $125K a month in fixed overhead. The key input is scope discipline; chain-of-custody records, meaning sample handoff logs, protect cash by reducing disputes and unpaid follow-up work.

Price Scope, Track Rework

Build every quote from the same inputs: technician hours, supervisor hours, chemicals, retests, reporting, and expected callbacks. Put change orders in writing before extra work starts. That is how you protect gross margin and cash flow when a remediation job gets bigger than the first estimate.

- Track labor by job.

- Track retests by project.

- Track change orders daily.

- Log chain-of-custody every sample.

- Price documentation as billable work.

If the team cannot prove sample handling and corrective steps, the job can become a margin leak. The owner earns more when the crew closes out jobs fast, invoices cleanly, and avoids unpaid revisits.

3

Technician Utilization And Route Density

Technician Utilization and Route Density

Utilization means the share of paid time spent on billable field work. In this model, the labor base is 2 senior field technicians in Year 1 and 8 by Year 5 at $75K each, so payroll rises from $150K to $600K before any burden. Owner take-home improves when each tech completes more compliant sampling visits per day, because payroll then supports more revenue instead of more drive time.

Route density is the number of jobs packed into a smaller travel area. Better density cuts unpaid windshield time, missed appointments, and callbacks, which protects gross margin and cash flow. The risk is simple: if speed starts hurting documentation quality or sample handling, rework and liability eat the gain fast.

Measure Visits, Drive Time, and Callbacks

Track billable visits per technician per day, drive minutes per stop, callback rate, and documentation pass rate. Here’s the quick math: more completed compliant visits spread the same salary across more revenue, while lower route waste keeps labor from leaking into non-billable time. If a tech needs extra revisits or weak chain-of-custody work, the margin gain disappears.

- Set a daily visit target per tech

- Map stops by zip code clusters

- Reject low-density one-off routes

- Review callbacks by technician

- Audit sample handling and paperwork

Use route planning to batch nearby accounts and cut dead miles. Tie dispatch to compliance quality, not just speed, so the team keeps samples clean and records auditable. That keeps more of each subscription and testing dollar available for overhead, reserves, and owner draw.

4

Customer Segment And Pricing Mix

Customer Segment Mix

Customer mix sets both revenue and admin load. Healthcare, senior living, hospitality, multifamily, commercial buildings, and cooling towers each bring different urgency, documentation, and renewal timing, so the same contract can take ver y different effort. If the mix skews toward high-touch accounts, non-billable work rises and owner pay gets squeezed unless pricing keeps up.

Here’s the quick math: Basic at $950 drops from 45% in Year 1 to 30% in Year 5, while Advanced at $1,850 rises from 35% to 45%. That mix shift improves pricing power because the tier spread is $900 per month per account. The gain shows up in margin and cash flow only if extra reporting time is controlled.

Price for Complexity

Track segment count, tier mix, admin hours per account, and renewal rate by segment. If one segment keeps asking for more reports, faster turnarounds, or tighter proof of work, raise the price or narrow the scope before it turns into unpaid labor. The goal is simple: more revenue per account without letting admin time outrun billing.

- Watch renewals by client type.

- Charge more for heavy documentation.

- Limit free scope creep.

- Protect margin on higher-touch accounts.

What this estimate hides is labor drag. A segment with stronger urgency can also create more follow-up, more file checks, and more compliance proof, so the owner should measure billed revenue against service minutes, not just signed contract value. When the mix shifts toward Advanced, take-home income improves only if those extra minutes stay billed or tightly capped.

5

Overhead, Insurance, Equipment, And Reserves

Overhead, Insurance, and Reserves

$125K a month in fixed costs sets the cash floor here, including $55K rent, $25K fleet insurance and maintenance, and $18K professional liability insurance. That overhead protects delivery capacity, but it also cuts distributable cash, so owner pay depends on staying ahead of the burn rate.

Early capex is $345K, and the model’s minimum cash need hits $610K in Month 4. Cash is the real constraint here. If monthly revenue slips or collections slow, the owner may have to hold back draws even when jobs are busy.

Track Cash Burn Before Owner Draw

Watch fixed cost coverage each month: revenue minus $125K overhead, before variable testing and labor costs. That tells you how much cash is left for the owner, reserves, and growth. If overhead rises faster than contract backlog, take-home income gets squeezed fast.

- Track cash runway monthly

- Hold the $610K reserve

- Review insurance and fleet spend

Keep the reserve target tied to the Month 4 cash need, not to hope. A simple rule works: don’t expand equipment or add fixed staff unless recurring contracts can cover the added burn. That keeps cash available for payroll, claims gaps, and delayed payments.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Owner income changes with revenue scale, staffing, and lab-plus-processing costs. Year 1 is mainly salary driven, while Year 5 leaves more room for distributions after reserves.

| Scenario | Low CaseConservative | Base CaseCore | High CaseUpside |

|---|---|---|---|

| Launch model | This is the cautious path, where the owner mostly relies on salary. | This is the modeled middle path, where the owner pays themselves and keeps some cash after reserves. | This is the stronger path, where scale supports salary and larger distributions. |

| Typical setup | Year 1 revenue is $2.033 million with $955,000 EBITDA, a 45% basic mix, and about $550,000 payroll before any distributions. | Year 3 revenue reaches $6.385 million with $5.506 million EBITDA as the mix shifts toward more advanced and premium plans. | Year 5 revenue reaches $14.096 million with $12.580 million EBITDA, lower unit costs, and enough cash for distributions after reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | CEO salary onlySalary only | Salary plus modest distributionsModest upside | Salary plus larger distributionsDistribution upside |

| Best fit | Use this if you want a downside check and plan to stay close to Year 1 scale. | Use this as the working plan most founders would budget against. | Use this to test upside if sales, staffing, and cash discipline all hold. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Legionella Prevention Service Porter's Five Forces Analysis

- Legionella Prevention Service BCG Matrix

- Legionella Prevention Service Business Model Canvas

- What Are The 5 KPI Metrics For Legionella Prevention Service Business?

- Legionella Prevention Business Plan Template in Pre-Written Word

- How Increase Profits For Legionella Prevention Service?

- What Are Operating Costs For Legionella Prevention Service?

- Legionella Prevention Service Startup Costs: $345K CAPEX Plan

- Legionella Prevention Service Financial Model Template in Excel

- How To Start A Legionella Prevention Service In 8–16 Weeks

- How Do I Write A Business Plan For Legionella Prevention Service?

- Legionella Prevention Service Marketing Mix

- Legionella Prevention Service Marketing Plan

- Legionella Prevention Service Business Proposal

- Legionella Prevention Service PESTEL Analysis

- Legionella Prevention Service Pitch Deck Example Editable PPTX

- Legionella Prevention Service Business SWOT Analysis

- Legionella Prevention Service Value Proposition Canvas

Frequently Asked Questions

It can be profitable under the researched assumptions, but only with strong contract volume and cost control The model shows $203M Year 1 revenue, $955K Year 1 EBITDA, and 4-month break-even Still, EBITDA is before taxes, debt service, capex, and owner distributions, so cash discipline matters