Owner income$0 to $90k

Owner income$0 to $90kHow Much Does a Lumber Yard Owner Make? $397k Year 2 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0 to $90k  Net margin-75% to 77%

Net margin-75% to 77% Revenue for target pay$1.44M

Revenue for target pay$1.44M Business difficultyHard

Business difficultyHard

You’re estimating owner income from a lumber yard’s operating cash flow, not a fixed paycheck In this five-year model, the yard shows -$336k EBITDA in Year 1, reaches breakeven in Month 14, and produces $397k EBITDA in Year 2 before taxes, debt service, reserves, and owner draws

Owner income$0 to $90kNet margin-75% to 77%Revenue for target pay$1.44MBusiness difficultyHardWant to test your lumber yard owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margin, payroll, taxes, debt, reserves, and the owner's draw policy; it is not guaranteed salary, tax advice, or owner distribution advice.

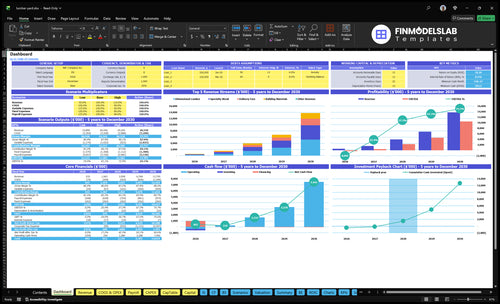

Can you check owner income in the Lumber Yard model?

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions; open the Lumber Yard Financial Model Template.

Owner-income model highlights

- EBITDA by year

- Breakeven month tracked

- Stress 150% to 250%

- Payroll, COGS, and overhead

- Owner pay timing

Is a lumber yard profitable for an owner operator?

Yes, but only if volume is high enough to cover payroll, yard costs, trucks, inventory, and reserves. In this model, breakeven lands in Month 14 and payback takes 28 months, with a minimum cash need of $393k. Owner-operated economics can improve cash flow if the owner fills the $90k general manager role; otherwise, that cost stays in the payroll base and owner take-home comes from what’s left.

Why it works

- Owner fills the $90k GM role

- Manager-run keeps $90k in payroll

- Breakeven hits in Month 14

- Payback takes 28 months

Cash risk

- Minimum cash need is $393k

- Early draws raise cash strain

- Volume must cover fixed costs

- Reserves matter from day one

How much revenue does a lumber yard need to pay the owner?

For a Lumber Yard, revenue alone does not pay the owner; contribution margin does. Using the provided Year 1 math, 86.0% gross margin minus 45% variable costs leaves 81.5% before payroll and overhead, and the quick estimate puts needed sales at about $971k to cover $440k payroll, $2,616k fixed overhead, and $90k owner pay, before debt and reserves. If the owner replaces the $90k general manager role, that target changes.

Owner pay math

- 86.0% gross margin

- 45% variable costs

- 81.5% left before overhead

- $90k owner pay target

What drives sales need

- $440k payroll to cover

- $2,616k fixed overhead

- Debt and reserves come after this

- Owner-manager role changes the math

How much can a lumber yard owner make per year?

A Lumber Yard owner can make $0 in Year 1 if cash is tight, or target about $90k/year if they work as the operator; the model shows EBITDA moving from -$336k in Year 1 to $397k in Year 2, then $2.249M, $4.556M, and $10.417M in Years 3–5. For the driver behind that income, see What Is The Most Important Indicator Of Success For Lumber Yard?; EBITDA is not take-home after taxes, debt, inventory reserves, and reinvestment.

Owner Pay Paths

- Work in yard: target $90k salary

- Hire GM: reduce owner cash available

- Distributions only: depends on profit

- Year 1 EBITDA: -$336k

Modeled Upside

- Year 2 EBITDA: $397k

- Year 3 EBITDA: $2.249M

- Year 4 EBITDA: $4.556M

- Year 5 EBITDA: $10.417M

Want the six lumber yard income drivers?

1

86%-88%Gross Margin

A better mix of dimensional lumber, specialty wood, and materials lifts profit on every sale.

2

15%-25%Sales Volume

Conversion moves from 15% to 25% and repeat share from 30% to 50%, so fixed costs get spread over more orders.

3

10%-12%Supplier Terms

Lower wholesale buys and inbound freight keep more cash in the business as volume grows.

4

$440K-$750KPayroll

Payroll climbs from about $440K to $750K, so staffing and delivery have to stay productive.

5

$393KCash Need

The model bottoms out at a $393K cash need around Month 14, so funding terms affect survival.

6

Month 14Stock Turns

Slow turns and shrink trap cash, and that pressure shows up before breakeven in Month 14.

Lumber Yard Core Six Income Drivers

Sales Volume and Customer Mix

Sales Volume That Pays

More contractor sales and repeat builder orders raise gross profit dollars, not just top-line sales. This yard expects 150 to 250 daily visitors on Year 1 operating days, with 250 on Saturday and 50 on Sunday, so the owner’s income depends on turning traffic into buying customers.

Here’s the quick math: the model’s conversion metric rises from 150% in Year 1 to 250% in Year 5, and repeat customers rise from 300% to 500%. If traffic stays high but buying stays weak, there is not enough gross profit to cover payroll, delivery, or owner draws.

Measure Buyers, Not Foot Traffic

Track daily visitors, buyer count, contractor share, and repeat order rate every week. Those four inputs tell you whether sales volume is creating usable cash or just busy aisles.

- Watch Saturday conversion first.

- Separate contractor and DIY orders.

- Count repeat builder purchases monthly.

Push follow-up on quotes and special orders, because repeat builders lift margin quality and make owner pay more stable. If the yard gets 250 visitors but few buy, the operation still misses the cash needed for labor, delivery, and draws.

1

Gross Margin and Product Mix

Gross Margin Mix

Mix is the fastest way the yard changes gross profit without changing total units. If dimensional lumber moves from 500% to 420%, specialty wood from 150% to 190%, building materials stays at 300%, and delivery fees rise from 50% to 90%, the average ticket can look steady while gross profit per order shifts. That directly changes cash available for payroll, overhead, and owner draw.

Listed prices also move from $25 to $29, $75 to $87, $15 to $17, and $100 to $120. Higher prices help only if the mix and discounting hold. What this hides: freight, damage, and slow-moving stock can erase the gain fast.

Price by Category

Track gross profit by category, not just total sales. Use category mix, average selling price, unit cost, delivery attach rate, and discount rate. If specialty wood and delivery carry better realized margin, pushing those lines can lift owner pay faster than chasing more low-margin lumber volume.

- Units sold by category

- Average selling price

- Realized gross profit per order

- Delivery attach rate

- Discounts and write-downs

Set a margin floor by SKU class, then test price changes in small steps. One size won’t fit every item, so price around cost and sell-through, not one target. If a line gets slow or damaged, protect cash by cutting reorder size first.

2

Purchasing Power and Supplier Terms

Supplier Costs and Terms

Supplier costs and terms decide how much of each sale turns into owner cash. In this yard, listed wholesale material purchases fall from 120% of sales in Year 1 to 100% in Year 5, and inbound freight falls from 20% to 16%. The provided gross margin metric moves from 860% to 884%, so better buying lifts profit if the yard keeps selling through stock fast.

The key inputs are sales, landed cost, freight, payment terms, rebates, and inventory days. Here’s the quick math: lower buy cost raises gross profit dollars, and better terms delay cash out the door. What this hides is the cash drain from slow stock, damaged boards, and rebate timing if inventory sits too long before it sells.

Track Landed Cost

Ask each supplier for payment terms, rebates, and buying-group access. Measure landed cost, not sticker price, because freight and terms change the real margin. One clean rule: cheaper buying only helps owner income when inventory turns fast and does not trap cash on the yard.

- Track inventory days on hand.

- Reconcile rebates every month.

- Compare vendor terms side by side.

If a rebate arrives late, it helps profit but not payroll. So forecast cash with supplier due dates and stock turnover together, then protect owner draw from gaps between buying, selling, and collecting.

3

Inventory Turnover and Shrink

Inventory Turnover and Shrink

Inventory is both a margin lever and a cash-flow constraint. Lumber, boards, specialty wood, and building materials only help the owner if they sell before they age, get damaged, or get stolen. With a $393k minimum cash need and Month 14 breakeven sensitivity, strong accounting profit can still leave weak owner cash if stock must be replenished before contractor receivables are collected.

- Track turns by product class.

- Track shrink by cause code.

- Watch aging stock weekly.

A faster turn rate puts cash back to work sooner, so more cash is available for payroll, reorders, and owner draws. Slow-moving boards, damaged materials, theft, weather exposure, and lumber price swings all press margins and cash at the same time. One clean rule: if stock sits, cash stalls.

Cut shrink before you chase volume

Use an item-level count cycle and compare it to on-hand records every week. Break out losses from damage, theft, weather, and price changes, then fix the biggest bucket first. That tells you whether the answer is better storage, tighter receiving, or smaller buys.

Also track supplier payment dates against customer collection dates. If you pay to refill inventory before contractor cash comes in, owner pay gets squeezed even when profit looks fine. Faster turns shorten that gap and improve the cash available for draws.

4

Labor and Delivery Efficiency

Labor and Delivery Efficiency

Payroll and delivery execution decide how much gross profit reaches the owner. Here’s the quick math: payroll climbs from $440k in Year 1 to $750k in Year 5, a $310k jump. That only works if labor supports sales. The staffing mix includes a $90k general manager, $50k sales associates, $40k yard workers, $45k drivers, and a $40k admin assistant.

Delivery efficiency also matters because variable fuel and maintenance falls from 25% to 21%. That 4-point improvement keeps more cash in the business for owner pay. If routing, loading time, overtime control, forklift use, and dispatch discipline slip, the gain gets eaten by extra miles, idle labor, and late trucks.

Tighten Labor and Delivery Control

Track labor by delivery, not just by month-end payroll. Watch overtime hours, fuel per route, maintenance per mile, load-to-depart time, and missed dispatch windows. If those numbers rise while orders stay flat, payroll is outrunning gross profit and owner draw will feel the squeeze.

- Review routes every week.

- Set load cutoffs and dispatch times.

- Use forklifts to cut touches.

- Block avoidable overtime fast.

Keep each truck full enough to earn its trip. Fewer partial loads and fewer repeat touches usually mean less labor per order, tighter cash use, and more gross profit left for the owner.

5

Fixed Overhead and Working Capital

Fixed Overhead Load

This yard carries $218k a month in fixed overhead before the first load sells. That includes lease, utilities, insurance, software, marketing, supplies, and security, so the owner’s pay only starts after gross profit covers that base and still leaves room for debt service and reserves.

EBITDA, or operating profit before interest, taxes, depreciation, and amortization, is still not take-home pay. The $222k capex outlay for forklift, truck, hardware, racking, furniture, paving, signage, online setup, and cameras drains cash up front, so paper profit can look fine while owner draws stay tight.

Protect Cash Runway

Track the fixed-cost base each month and compare it with cash collected, not just booked sales. Here’s the quick math: if overhead stays at $218k, the yard needs enough gross profit dollars to clear that hurdle before the owner can pay themselves.

- $218k monthly overhead

- $222k capex timing

- Debt service comes after EBITDA

- Reserve cash before owner draws

Watch how fast receivables turn into cash and delay nonessential capex if billing slows. If the monthly run rate cannot cover overhead, reserves, and debt service together, growth only adds stress, not owner income.

6

Objective: Compare lean, base, and mature lumber yard owner income cases

Owner income scenarios

Owner pay changes fast here because year 1 is cash negative, breakeven lands in month 14, and year 5 cash flow is much stronger. Use the three cases to test draw timing and cash reserves.

| Scenario | Low CaseCash tight | Base CaseBreakeven | High CaseMature cash flow |

|---|---|---|---|

| Launch model | Year 1 stays negative, so owner pay is not supported unless outside funding covers the gap. | Year 2 reaches positive EBITDA, so owner pay can start only after debt, taxes, and inventory reserves are covered. | Year 5 supports much stronger owner income as volume, repeat mix, and EBITDA scale up. |

| Typical setup | Traffic and conversion ramp slowly, EBITDA is -$336k in Year 1, and the business needs about $393k of minimum cash. | The yard crosses breakeven in Month 14, EBITDA is $397k in Year 2, and pay depends on keeping working capital tight. | The model shows $10,417k EBITDA in Year 5 with a higher repeat mix and about $750k payroll, which points to a larger contractor-focused operation. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No owner drawNo draw | Post-debt drawCautious draw | Strong draw potentialUpside case |

| Best fit | Use this to stress-test a slow launch and the cash needed to survive the ramp. | Use this for a practical owner pay plan once the business is past the early cash squeeze. | Use this to test upside owner pay once the yard is fully scaled and cash generation is strong. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Lumber Yard Porter's Five Forces Analysis

- Lumber Yard BCG Matrix

- Lumber Yard Business Model Canvas

- 7 Core Financial KPIs to Track for Your Lumber Yard Business

- Lumber Yard Business Plan Template in Pre-Written Word

- 7 Data-Driven Strategies to Increase Lumber Yard Profitability

- How Much Does It Cost To Run A Lumber Yard Each Month?

- How Much Does It Cost To Start A Lumber Yard? Plan On $615k+

- Lumber Yard Financial Model Template in Excel

- How to Open a Lumber Yard: 4-9 Month Launch Plan

- How to Write a Lumber Yard Business Plan: 7 Essential Steps

- Lumber Yard Marketing Mix

- Lumber Yard Marketing Plan

- Lumber Yard Business Proposal

- Lumber Yard PESTEL Analysis

- Lumber Yard Pitch Deck Example Editable PPTX

- Lumber Yard Business SWOT Analysis

- Lumber Yard Value Proposition Canvas

Frequently Asked Questions

In this model, owner income is tight in Year 1 because EBITDA is -$336k Year 2 EBITDA reaches $397k, but that is before taxes, debt service, inventory reserves, and draws If the owner works as general manager, the $90k salary line is the clearest operator-pay reference