Owner income-$653K

Owner income-$653KHow Much Luxury Watch Rental Owners Make: $223K Pre-Overhead

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income-$653K  Net margin-77%

Net margin-77% Revenue for target pay$1.6M

Revenue for target pay$1.6M Business difficultyHard

Business difficultyHard

Key Takeaways

- Higher utilization lifts revenue, but claim risk rises.

- Pricing mix drives revenue and insurance exposure.

- Insurance and reserves can wipe out rental profit.

- Repeat renters lower CAC and support scale.

Owner income-$653KNet margin-77%Revenue for target pay$1.6MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

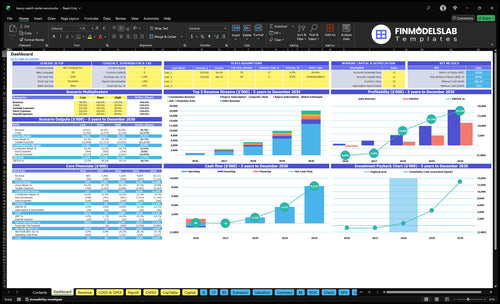

How do you check owner income in the financial model?

The dashboard in the Luxury Watch Rental Financial Model Template shows revenue, gross margin, marketing spend, pre-overhead cash flow, and owner-pay scenarios—open it now.

Owner-income model highlights

- Owner pay scenarios

- Revenue and gross margin

- Year 1-3 assumptions

Can a luxury watch rental owner run the business absentee?

Luxury Watch Rental can run absentee, but not cheaply: once the founder steps back, payroll has to replace the work in vetting, customer support, logistics, claims handling, seller onboarding, and secure fulfillment. An owner-run setup may protect more of the Year 1 $223K pre-overhead pool, but it adds time risk. A lean staffed model should pay payroll before distributions, and a scaled model only makes sense if trust and safety, insured shipping, and support quality keep claims and churn under control.

Owner-run upside

- Keeps more Year 1 cash.

- Reduces early payroll burn.

- Speeds decisions.

- Works best before scale.

Absentee tradeoff

- Payroll replaces founder labor.

- Claims and support need staff.

- Shipping must stay insured.

- Scale only works with control.

What gross margin can a luxury watch rental business earn after insurance and damage costs?

Luxury Watch Rental’s model shows a 140% direct cost load in Year 1, 135% in Year 2, and 127% in Year 3, with the source data labeling that as gross margins of 860%, 865%, and 873% after insurance premiums, authentication and servicing, payment processing, and secure shipping subsidies. If you want the deeper cost picture, see What Is The Estimated Cost To Open And Launch Your Luxury Watch Rental Business? before calling anything distributable. The catch is simple: the file does not include separate theft, fraud, chargeback, replacement, or major repair reserves, and one loss can wipe out many small-margin rentals.

Included direct costs

- Insurance premiums are included

- Authentication and servicing are included

- Payment processing is included

- Secure shipping subsidies are included

Missing reserve layers

- Theft reserves are not shown

- Fraud reserves are not shown

- Chargeback reserves are not shown

- Replacement and major repair reserves are not shown

How much can a luxury watch rental owner make?

Under the model’s researched Year 1 assumptions, a Luxury Watch Rental owner has an owner-pay pool of about $223K, but that’s before payroll, overhead, debt service, taxes, and added replacement reserves; for the operating metric behind this, see What Is The Most Important Indicator Of Success For Luxury Watch Rental?. Year 1 revenue is about $1.014M, but listed direct costs consume 140% and buyer plus seller marketing totals $650K, so take-home depends on cost control.

Year 1 math

- $1.014M modeled revenue

- $223K owner-pay pool before major costs

- 140% direct-cost load

- $650K buyer plus seller marketing

Year 3 upside

- $4.440M modeled revenue

- $2.176M pre-overhead cash flow

- CAC improves as repeat orders rise

- Claims, storage, staffing, financing still matter

Want to see the six income drivers?

1

0.15-1.00xWatch Use

More rental days per watch push the same inventory through more orders, so owner take-home rises fastest when watches stay booked.

2

$1.2K-$4.5KPrice Mix

Higher rental tiers and a richer corporate mix lift revenue per order, with corporate rentals at $3,500 to $4,500 doing the most work.

3

$2.5K CACSeller Supply

Inventory supply stays expensive at a $2,500 Year 1 seller CAC, so better sourcing and financing protect cash and keep watches on the platform.

4

14%-11%Risk Reserves

Year 1 direct costs run about 14% from insurance, servicing, payment fees, and shipping subsidies, and that spread drops to about 11.3% by Year 5.

5

$280-$160Buyer CAC

Buyer CAC starts at $280 and falls to $160 by Year 5, and repeat orders plus memberships decide whether growth turns into profit.

6

$731K/yrOverhead

Year 1 operating overhead is about $731K, so faster fulfillment and tighter staffing matter until EBITDA turns positive in Year 2.

Luxury Watch Rental Core Six Income Drivers

Utilization And Rental Days Per Watch

Rental Days Per Watch

Utilization is the share of time a watch is rented instead of sitting idle. Higher utilization spreads insurance, servicing, and storage across more paid days, so each order can support more margin and a larger owner draw. But the source data only gives order volume, not watch count, so the model needs inventory count and average rental length to turn 1,796 Year 1 orders and 7,413 Year 3 orders into rental days per watch.

Push utilization too hard and the business pays for it in shipping delays, cleaning, authentication checks, servicing downtime, and fraud review. That can raise claims, increase wear, and hurt repeat demand, which means profit looks good on paper but cash flow gets choppy. The key is not max rentals; it is the highest safe rental days per watch.

Keep Watches Moving Without Raising Claims

Use a simple formula: rental days per watch = paid rental days ÷ active watches. Build the forecast after you enter inventory count, average rental length, and the days lost to shipping, cleaning, authentication, servicing, and fraud review. That shows how much of each watch’s calendar really earns money.

- Set a max turnaround time.

- Track claims by watch tier.

- Watch repeat orders by utilization band.

- Pause high-risk watches for service.

More booked days only help if the watch comes back clean and on time. If claims rise as utilization rises, cut back before margin and owner pay start to slip.

1

Average Rental Price And Watch Mix

Average Rental Price and Watch Mix

Your income here is driven by blended average order value and the mix of event renters, watch enthusiasts, and corporate clients. Year 1 AOVs are $1,800, $1,200, and $3,500; by Year 3 they rise to $2,100, $1,400, and $4,000. Higher AOV lifts commission revenue and owner-pay capacity, but only after service and insurance costs.

Price each rental by demand, replacement value, rental duration, and insurance risk. A higher corporate mix can raise revenue fast, but it can also add account support and service standards, which pushes overhead up. The key inputs are segment mix, order volume, AOV, commission rate, and the cost to serve each rental.

Track Segment Mix, Not Just Blended Revenue

Here’s the quick math: more corporate orders usually mean higher AOV, but the extra gross revenue only helps if added support cost stays below the margin lift. Track AOV by segment every month, not just one blended number. If corporate orders rise but support hours and claims rise too, owner pay can fall even when sales look strong.

- Track AOV by customer segment.

- Track support hours per order.

- Review claims and insurance by tier.

- Test pricing by rental length.

Raise rates on longer rentals and higher-risk pieces first. Keep lower-risk enthusiast rentals priced to stay busy, since that helps cash flow without adding much service load. The goal is a mix that protects margin, keeps inventory moving, and leaves a clean payout for owners after operating costs.

2

Inventory Acquisition And Financing

Inventory Sourcing Cost

Owner income here depends on how cheaply you source watch inventory and how much cash you lock up. The source model uses seller-supplied inventory, with seller CAC at $2,500 in Year 1 and $1,900 in Year 3. That cost sits before rental revenue, so every extra seller that converts has to earn back onboarding spend through commissions and repeat rentals.

Consignment keeps capital lighter than owned stock, but it adds onboarding, verification, commission sharing, and relationship risk. Owned inventory would also add purchase cost, depreciation risk, debt service, and cash tied up in watches. Here’s the quick math: lower seller CAC and better supply mix improve cash flow first, then profit, then the owner’s draw.

Track Seller CAC By Source

Measure seller CAC by channel, then compare it with gross commission per active watch. The source mix is listed as 600% private collectors, 300% boutique stores, and 100% certified dealers, so keep each source separate in the model and verify which one brings faster approvals and lower servicing needs. If CAC drifts above the payback window, owner income gets squeezed fast.

Track three inputs every month: sellers added, approval rate, and revenue per listed watch. Push the cheapest reliable supply first, but don’t cut verification to save time. One bad supplier can raise claims, stall rentals, and eat the margin from many orders. What this estimate hides: commission splits and onboarding labor can matter almost as much as the first CAC hit.

3

Insurance, Damage, Fraud, And Reserves

Insurance, Damage, and Reserves

This line item includes insurance premiums, authentication, servicing, and reserves for theft, fraud, chargebacks, replacements, and major repairs. In this model, insurance runs at 60% of revenue in Year 1, 58% in Year 2, and 55% in Year 3, while authentication and servicing add 15%, 15%, and 14%. That means the business can burn 75% of Year 1 revenue before other overhead. Owner income gets squeezed fast.

The key inputs are revenue, claim frequency, average loss per claim, and reserve rate per rental. Here’s the quick math: if revenue is $100,000, Year 1 insurance is $60,000 and auth plus servicing is $15,000, before any reserve for fraud or damage. One claim can wipe out profit from many rentals, so owner pay should be set after these reserves, not before them.

Track Claims Before Owner Pay

Build reserves into every rental quote. Track claim rate, loss per claim, chargebacks, repair turnaround, and the gap between gross revenue and cash left after protection costs. If the reserve pool is thin, owner draws are too high. That is the whole risk here.

- Set reserve % by rental value

- Log every claim by cause

- Separate repairs from fraud loss

- Review cash after each payout

- Raise pricing when claims rise

Use a monthly reserve target tied to revenue, then test it against real losses. If claims stay low, excess reserve can help profit; if not, it protects cash flow and keeps the owner from paying themselves out of money that should cover replacement risk.

4

Customer Acquisition And Repeat Rentals

Customer Acquisition And Repeat Rentals

This driver is the cost to win a buyer and keep them renting again. The key number is buyer CAC, which falls from $280 in Year 1 to $220 in Year 3, even as buyer marketing rises from $400K to $11M. That only improves owner income if repeat rentals and order value grow faster than paid spend.

Repeat orders d o the heavy lifting. For watch enthusiasts, repeat orders rise from 40 in Year 1 to 70 in Year 3, so the same customer can throw off more margin over time. The risk is simple: if churn stays high, marketing just buys one-off rentals and cash flow gets tight.

Track CAC Against Repeat Value

Measure buyer CAC by segment, then compare it with gross profit from the first rental plus expected repeats. If enthusiasts rent again faster than event buyers, shift spend there and build subscriptions or corporate accounts around them. The mix moving toward enthusiasts is the margin lever, because it lifts revenue without a one-for-one rise in CAC.

Watch three things every week: buyer CAC, repeat order rate, and time to rebook. Lower CAC helps only when paid traffic turns into returning renters. If support issues, delivery delays, or poor fit push churn up, cut spend fast; one weak cohort can wipe out the gain from a lower CAC.

5

Operating Overhead And Fulfillment Efficiency

Fulfillment Cost per Rental

When secure shipping subsidies run 40% in Year 1, 38% in Year 2, and 35% in Year 3, plus payment processing at 25%, 24%, and 23%, direct fulfillment alone takes 65%, 62%, and 58% of revenue. That leaves little room for owner pay until order volume grows. A $1,000 rental keeps only $350 before other overhead in Year 1.

Actual overhead can also include payroll, secure storage, software, customer support, packaging, claims handling, and compliance work. Owner-operated fulfillment protects early cash, but it caps scale. Hiring can widen coverage and speed service, yet distributions usually shrink until order density is high enough to cover the team.

Track Cost per Order

Measure fulfillment on a per-order basis, not just as a monthly total. Track shipping subsidy, payment fees, labor hours, and overhead per rental, then compare that against average order value and order count. If the shipping subsidy stays near 40% and processing near 25%, the model needs higher volume or better routing fast.

Test ways to cut touches: denser shipping lanes, fewer re-ships, tighter damage checks, and clearer return rules. Add staff only when forecasted orders can absorb payroll without cutting owner draw. If order density is weak, keep fulfillment lean and protect cash until the fixed cost per rental falls.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Income shifts as the business moves from a Year 1 launch ramp to a Year 3 scale-up, with higher revenue and repeat use improving cash before overhead.

| Scenario | Low CaseBefore overhead | Base CaseBefore overhead | High CaseBefore overhead |

|---|---|---|---|

| Launch model | A lower earnings path built on the Year 1 ramp and slower cash build. | A modeled middle path built on Year 2 traction and steadier cash generation. | A stronger upside path built on Year 3 scale and repeat demand. |

| Typical setup | Year 1 assumptions with about $1.014M revenue, 86.0% gross margin, $650K marketing, and $223K pre-overhead cash flow. | Year 2 assumptions with about $2.156M revenue, 86.5% gross margin, $1.1M marketing, and $766K pre-overhead cash flow. | Year 3 assumptions with about $4.440M revenue, 87.3% gross margin, $1.7M marketing, and $2.176M pre-overhead cash flow. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $223KYear 1 ramp | $766KYear 2 core | $2.176MYear 3 surge |

| Best fit | Use this to stress-test a slow launch and tighter early cash. | This is the main planning case if you expect the modeled breakeven path. | Use this to test a fast-growth case after the business clears its early launch drag. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Luxury Watch Rental Porter's Five Forces Analysis

- Luxury Watch Rental BCG Matrix

- Luxury Watch Rental Business Model Canvas

- 7 Core KPIs to Scale Luxury Watch Rental Profitability

- Luxury Watch Rental Business Plan Template in Pre-Written Word

- How to Boost Luxury Watch Rental Profitability with 7 Key Strategies

- How to Run a Luxury Watch Rental: Monthly Operating Costs

- Luxury Watch Rental Startup Costs: $650K Year 1 Marketing Plus Assets

- Luxury Watch Rental Financial Model Template in Excel

- How To Open A Luxury Watch Rental Service In 10-16 Weeks

- How to Write a Business Plan for Luxury Watch Rental

- Luxury Watch Rental Marketing Mix

- Luxury Watch Rental Marketing Plan

- Luxury Watch Rental Business Proposal

- Luxury Watch Rental PESTEL Analysis

- Luxury Watch Rental Pitch Deck Example Editable PPTX

- Luxury Watch Rental Business SWOT Analysis

- Luxury Watch Rental Value Proposition Canvas

Frequently Asked Questions

The researched Year 1 case shows about $223K after listed direct costs and acquisition marketing, but before payroll, fixed overhead, debt service, taxes, and added loss reserves Revenue is about $1014M, gross margin is 860%, and total buyer plus seller marketing is $650K Actual take-home depends on staffing, claims, financing, and reinvestment