Owner incomeY1 $0; Y3 ~$492k

Owner incomeY1 $0; Y3 ~$492kHow Much Can a Machinist Training Program Owner Make at 85% Fill?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeY1 $0; Y3 ~$492k  Net margin36% / 69% / 78%

Net margin36% / 69% / 78% Revenue for target pay$6.7M

Revenue for target pay$6.7M Business difficultyHard

Business difficultyHard

You’re estimating owner pay for a private precision machining and computer numerical control (CNC) training school, not machinist employee wages This view covers tuition revenue, $21,800 in monthly fixed overhead, instructor payroll, lab costs, equipment spend, reserves, and pre-tax owner take-home over the first five model years

Owner incomeY1 $0; Y3 ~$492kNet margin36% / 69% / 78%Revenue for target pay$6.7MBusiness difficultyHardCould this CNC training school profit calculator support your target pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Can you check owner income in the Machinist Training Program model?

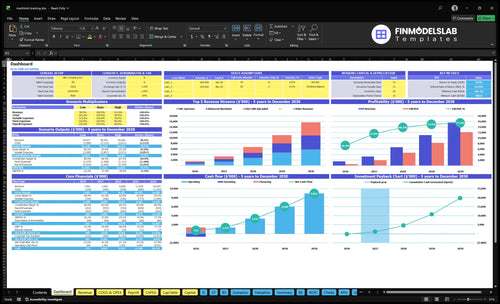

The dashboard tab shows annual revenue, operating profit, cash needs, and owner-income outputs. Open the Machinist Training Program Financial Model Template to test scenarios.

Owner-income model highlights

- Owner take-home output

- Year 1, 3, 5

- Scenario testing comes first

How does owner-operated income compare with hiring instructors?

If the owner teaches or serves as Director of Education in the Machinist Training Program, the $110,000 salary stays as earned owner compensation instead of adding a new payroll line. Hiring more instructors helps the program scale, but it also lifts the break-even point, and Lead CNC Instructor headcount rises from 10 FTE in Year 1 to 30 FTE by Year 4. So the tradeoff is simple: keep more cash in the business with owner labor, or spend more on staff and make sure admissions, scheduling, safety, and enrollment are strong enough to cover it.

Owner-led cash control

- $110,000 stays in-house

- Owner teaches or leads education

- Lower payroll pressure early

- Better cash protection at launch

Hiring for scale

- 10 FTE in Year 1

- 30 FTE by Year 4

- Needs stronger admissions

- Needs tight safety controls

Can a machinist training program support an owner?

Yes, a Machinist Training Program can support an owner, but not reliably at launch under these assumptions; see How Do I Launch A Machinist Training Program Business? for the setup path. Year 1 shows $575,400 revenue against $365,000 payroll and $261,600 fixed overhead, creating about a $166,000 operating loss before debt, taxes, and reserves.

Launch Reality

- Revenue: $575,400

- Payroll: $365,000

- Fixed overhead: $261,600

- Operating loss: about $166,000

Owner Pay Path

- Fill the $110,000 education director role

- Delay draws until occupancy improves

- Target 85% occupancy by Year 3

- Year 3 pre-tax profit: about $492,000

What CNC training school expenses cut owner take-home most?

Payroll and facility-heavy overhead cut owner take-home most in a Machinist Training Program. If you’re mapping the numbers, see How To Write A Business Plan For Machinist Training Program?. Year 1 payroll is $365,000, fixed overhead is $261,600, and startup equipment plus buildout add $655,000, so income falls fast when enrollment misses because rent, utilities, software, maintenance, insurance, and core staff still run.

Main cost pressure points

- Payroll: $365,000 in Year 1

- Fixed overhead: $261,600 yearly

- Equipment and buildout: $655,000 upfront

- Enrollment gaps hit take-home fast

Other direct cost drains

- Raw materials and stock: 6% of revenue

- Tooling and inserts: 4% of revenue

- Marketing: 8% of revenue

- Testing fees: 2% of revenue

Which six drivers change machinist training program owner income most?

1

$575K-$1.6MEnrollment Fill

Filled seats move revenue fastest; at 55% to 85% occupancy, annual revenue climbs from about $575K to $1.6M.

2

$1.8K-$3.4KTuition Mix

A stronger mix of CNC Operator, Advanced Machinist, and CAD CAM Specialist seats lifts monthly tuition per student from $1.8K to $3.4K.

3

21 daysBillable Days

Using all 21 billable days keeps the shop and instructors busy, so fixed costs spread across more revenue.

4

$365K-$705KInstructor Load

Payroll rises from about $365K to $705K as FTEs step up, and that can erase gains if class fill slows.

5

8%-10%Shop Costs

Shop margin depends on keeping direct cost bands near 8% to 10% and stopping waste in materials, tooling, and upkeep.

6

8%-5%Marketing Efficiency

Marketing falls from 8% to 5% of revenue as the program matures, so lower acquisition cost flows straight to EBITDA.

Machinist Training Program Core Six Income Drivers

Enrollment fill rate

Enrollment Fill Rate

Enrollment fill rate is the share of training seats that are actually sold and attended. In this model, occupancy rises from 55% in Year 1 to 85% in Year 3 and 92% in Year 5, which is why revenue moves from $575,400 to $160 million to $259 million. Empty seats hurt first because lease, utilities, software, maintenance, insurance, and payroll keep running.

The main inputs are available seats, enrolled students, and tuition per student. Here’s the quick math: if seats stay open, revenue drops but fixed cost does not, so gross margin and cash flow tighten fast. Do not assume every seat stays full year-round, especially during early ramp-up.

Track Seat Fill Weekly

Measure fill rate by cohort and program, not just at the company level. Track capacity, booked seats, show-up rate, and tuition collected so you can catch weak cohorts before they drag down owner take-home. One clean rule: open seats are wasted fixed cost.

Build forecasts with a fill-rate haircut, because 92% occupancy is not the same as every seat being full every month. If a cohort cannot cover fixed costs like the $12,000 lease, $3,500 utilities, $2,200 software, and $1,800 maintenance, delay owner draws and fix enrollment before adding more sessions.

- Track fill by cohort and month.

- Separate booked seats from attended seats.

- Stress-test early ramp-up occupancy.

1

Tuition pricing and payer mix

Tuition Price and Payer Mix

Tuition mix changes owner income fast because each seat does not earn the same cash. Year 1 monthly tuition is $2,200 for CNC Operator, $2,800 for Advanced Machinist, and $1,800 for CAD CAM Specialist, so the program mix sets revenue per class and how much cash is left after instructors and lab costs.

Corporate training adds $54,000 in Year 1 and $180,000 by Year 5, and that can make cash flow steadier. Employer-paid seats help predict revenue, but contracts, grants, and financed students should stay as sensitivities, not base-case income. One clean contract can matter more than a few extra walk-in enrollments.

Track Price by Payer, Not Just Headline Tuition

Measure revenue by program and payer source each month. The key inputs are seat count, monthly tuition, corporate contract value, and the share of employer-paid, cash-paying, grant-backed, and financed students. If a lower-priced program fills faster, total cash per cohort can still fall, even when occupancy looks strong.

Build three cases: signed corporate revenue, confirmed student tuition, and upside from grants or financing. Keep the forecast tied to collected cash, not promises. If the payer mix shifts toward financing-dependent students, collections slow and owner draw gets tighter, even when reported enrollment looks healthy.

2

Cohort frequency and schedule utilization

Cohort Frequency

Cohort frequency is how often the lab runs billable classes. With 21 billable days per month, more evening, weekend, or employer cohorts can lift tuition revenue only if instructors, machines, and safety coverage keep pace. The upside is better use of fixed assets; the risk is that too many sessions can weaken training quality and placement results, which then hurts future enrollments and owner take-home.

The key inputs are seat capacity across the three programs, instructor hours, machine uptime, and graduate outcomes. Owner income improves when extra cycles fill idle lab time and spread fixed overhead over more students. If schedule pressure forces smaller cohorts, rushed labs, or overtime, gross margin can drop even when top-line revenue looks stronger.

Protect Quality

Track billable days used, seat fill by program, machine downtime, instructor-to-student coverage, and placement rates. If a new cohort adds revenue but also raises overtime, repair risk, or absences, the extra cash can disappear fast. The best schedule uses spare lab hours without adding a new full fixed cost base.

Test evening, weekend, or employer cohorts one at a time. Keep the same safety rules and pass/fail standards, and watch whether completion and job placement hold steady. If outcomes slip, the schedule is too tight. Owner pay should come from higher throughput on the same assets, not from squeezing more classes into an already full week.

3

Instructor utilization

Instructor Utilization

Teaching labor drives margin in a hands-on CNC lab. Lead CNC Instructor payroll is $85,000 per FTE, and headcount grows from 10 FTE in Year 1 to 30 FTE by Year 4, or $850,000 to $2.55 million a year before the $110,000 Director of Education and $50,000 Shop Technician are added. If class load does not fill those hours, owner pay gets squeezed fast.

Owner teaching can ease cash strain because every instructor FTE the owner covers instead of hiring saves $85,000, but safe student-to-instructor coverage has to come first. The main inputs are student count, class size, teaching hours, and how many sections each instructor can cover without hurting safety or outcomes. If the lab is understaffed, the hidden cost is weaker completion and slower tuition growth.

Track Teaching Load

Measure billable class hours, students per instructor, and filled seat hours by cohort. That shows whether paid teaching time is producing revenue or just carrying idle payroll. Compare scheduled sections against instructor FTE each month, and flag any class that needs extra coverage before you add more seats.

To improve owner income, use owner teaching only where it cuts hired labor without breaking safety. Build the schedule around the minimum safe instructor coverage, then add cohorts only when the current team is near full use. One extra class should pay for itself before it adds another $85,000 of annual payroll.

4

Equipment, tooling, and facility costs

Equipment, tooling, and facility costs

This driver covers machining centers, CNC lathes, the metrology lab, workstations, tooling, workholding, buildout, and safety systems. Startup spend totals $655,000, so this is cash tied up before tuition hits the bank. Monthly fixed overhead is already $19,500 from the $12,000 lease, $3,500 utilities, $2,200 software, and $1,800 maintenance.

That means owner pay comes last. Here’s the quick math: before any draw, the business has to cover that $19,500 monthly base, plus repair, replacement, and any financing payments. If equipment sits idle or breaks down, you lose both revenue capacity and cash, so distributions should wait until the asset base is funded and stable.

Protect the cash behind the machines

Track each cost separately: lease, utilities, software, maintenance, and a replacement reserve. Also track machine uptime, tool wear, and class hours per asset so you know whether each machine is carrying its share of overhead. If debt is used, model debt service alongside repair spend so owner draw does not drain working cash.

- Keep a monthly equipment reserve.

- Watch uptime before adding seats.

- Fund maintenance before owner draw.

- Check replacement timing every month.

Use a simple rule: no owner distribution until the business covers $19,500 in monthly fixed costs, plus scheduled maintenance and near-term replacement needs. That keeps income tied to real free cash, not just busy classrooms or full schedules.

5

Student acquisition and placement reputation

Qualified Enrollments and Placement Reputation

This driver covers how many leads turn into qualified enrollments, how many students finish, and how many get placed. Marketing only helps owner income if it fills seats. In Year 1, recruitment marketing is 8% of revenue, then 6% in Year 3 and 5% by Year 5, so weak conversion quickly eats margin and reduces take-home pay.

Placement reputation changes the whole funnel. The Career Services Coordinator starts at $65,000 and grows to 20 FTE by Year 5, so this is a real operating cost, not a side task. Strong employer ties can lower acquisition pressure, but weak completion results raise churn risk and make every new student more expensive to win.

Track Conversions, Placements, and Cost per Seat

Measure the full funnel: leads, qualified leads, enrollments, completions, interviews, and job placements. The key test is simple: if marketing spend rises but qualified enrollments do not, owner income falls because tuition revenue does not cover the acquisition bill. A one-line check: marketing spend ÷ qualified enrollments should move down as reputation improves.

Build the employer side early. Keep a count of active hiring partners, interview offers, and placement outcomes by cohort. If completion slips, expect higher rework in admissions and more pressure on career services payroll. Track it monthly, because slower placements usually show up later as softer referrals and weaker fill rates.

- Track lead-to-enrollment conversion.

- Track completion and placement rates.

- Track cost per qualified enrollment.

- Track employer interviews per cohort.

- Review churn after weak outcomes.

6

Scenario objective: compare lean, base, and high machinist training program income cases

Owner income scenarios

Occupancy, pricing, and staffing scale income fast here, so the three cases show how the school moves from launch-year profit to mature-year upside.

| Scenario | LeanLean case | BaseBase case | HighHigh case |

|---|---|---|---|

| Launch model | This is the lower-earnings launch path, using Year 1 volume and 55% occupancy. | This is the modeled middle path, using Year 3 volume and 85% occupancy. | This is the stronger upside path, using Year 5 volume and 92% occupancy. |

| Typical setup | Year 1 runs at 55% occupancy with $1.561M revenue, $365k payroll, and $261.6k annual fixed overhead. | Year 3 reaches 85% occupancy, $6.696M revenue, $587.5k payroll, and about 16% combined direct and variable costs. | Year 5 reaches 92% occupancy, $15.655M revenue, $705k payroll, and about 15% combined direct and variable costs. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $566kLean income | $4.6MBase income | $12.1MUpside income |

| Best fit | Use this if you want a launch-year stress test for cash and staffing. | Use this as the core planning case for a scaled, repeatable school. | Use this to test upside if classes stay full and add-on training keeps growing. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Machinist Training Program Porter's Five Forces Analysis

- Machinist Training Program BCG Matrix

- Machinist Training Program Business Model Canvas

- What Are Five KPIs For Machinist Training Program Business?

- Machinist Training Program Business Plan Template in Pre-Written Word

- How Increase Machinist Training Program Profitability?

- What Are Operating Costs For Machinist Training Program?

- Machinist Training Program Startup Costs: $655K CAPEX Plan

- Machinist Training Financial Model Template in Excel

- How To Open A Machinist Training Program In 6 To 12 Months

- How To Write A Business Plan For Machinist Training Program?

- Machinist Training Program Marketing Mix

- Machinist Training Program Marketing Plan

- Machinist Training Program Business Proposal

- Machinist Training Program PESTEL Analysis

- Machinist Training Program Pitch Deck Example Editable PPTX

- Machinist Training Program Business SWOT Analysis

- Machinist Training Program Value Proposition Canvas

Frequently Asked Questions

In this model, Year 1 does not support profit distributions because operating profit is about negative $166,000 before debt, taxes, and reserves By Year 3, revenue reaches about $160 million and pre-tax operating profit is about $492,000 Owner take-home still depends on salary role, equipment financing, cash reserves, and reinvestment