Owner income$110k

Owner income$110kMade-to-Order Manufacturing Owner Income at $835K Year 1 Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$110k  Net margin-15% to 48%

Net margin-15% to 48% Revenue for target pay$89.4k

Revenue for target pay$89.4k Business difficultyHard

Business difficultyHard

A made-to-order manufacturing owner may earn a planned salary if they fill an operating role, but profit distributions depend on cash left after materials, labor, overhead, payroll, reserves, and debt In the researched Year 1 case, revenue is $835,000 with 715% gross margin, but listed payroll and fixed costs produce about a $144,000 operating loss before taxes and reserves If the owner fills the General Manager role, the model includes $110,000 of annual compensation, but it does not support extra owner take-home in Year 1 By the mature year, revenue reaches $776 million and operating profit reaches about $364 million before taxes, debt, and reserves

Owner income$110kNet margin-15% to 48%Revenue for target pay$89.4kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the forecast?

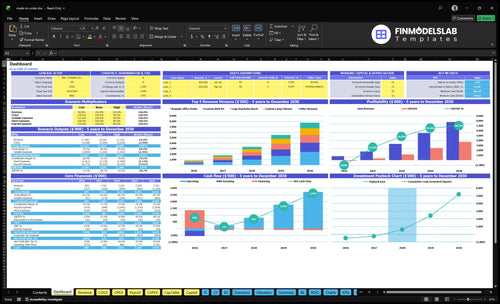

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Made-to-Order Manufacturing Financial Model Template; open it to test owner income.

It connects dashboard, revenue assumptions, COGS, payroll, operating expenses, scenarios, and income outputs. Charts show revenue from $835,000 to $776 million, gross margin from 715% to 732%, and operating profit from -$144,115 to $364 million.

Owner-income model highlights

- Owner pay stays visible

- Revenue and margin swing

- Test scenarios fast

Can a made-to-order manufacturing business scale owner income?

Yes—Made-to-Order Manufacturing can scale owner income, but only if utilization rises faster than overhead and the model keeps improving. In the projection, operating profit moves from -$144,115 in Year 1 to $110 million in Year 3 and $364 million in Year 5, so the upside comes from more completed orders, better quoting, repeatable workflows, and skilled technicians. The catch is payroll also grows from $415,000 to $122 million, so idle labor can wipe out the gain.

Where income expands

- Year 1: -$144,115 operating profit

- Year 3: $110 million operating profit

- Year 5: $364 million operating profit

- Scale comes from more completed orders

What can break it

- Payroll rises from $415,000 to $122 million

- Idle labor can erase margin gains

- Keep reserves for equipment and inventory

- Plan for maintenance and slower collections

How much does a made-to-order manufacturing business owner make?

A Made-to-Order Manufacturing owner can model $110,000 in annual General Manager pay if they run the shop, but owner cash take-home is not the same as profit; Year 1 shows -$144,115 operating profit before taxes and reserves. For profit mechanics, see How Increase Made-To-Order Manufacturing Profitability?; distributions depend on cash, debt, inventory, and reinvestment.

Owner-operator case

- $110,000 modeled General Manager compensation

- -$144,115 Year 1 operating profit

- Before taxes and reserves

- Paycheck possible; distributions unlikely

Scaled operation

- $332 million Year 3 revenue

- $110 million Year 3 operating profit

- $776 million Year 5 revenue

- $364 million Year 5 operating profit

How much revenue does a made-to-order manufacturer need to pay the owner?

If you're trying to pay the owner from Made-to-Order Manufacturing, the key limit is cash after production COGS, marketing, and payment fees. Here’s the quick math: Year 1 contribution margin is about 60.6%, and with $19,600 in fixed overhead plus $34,583 in listed payroll, break-even revenue is about $89,400/month before owner distributions. Year 1 averages about $69,600/month, so extra owner pay is not covered yet; owner pay has to come through payroll, draws, or distributions depending on structure.

Owner pay math

- 60.6% contribution margin

- $19,600 fixed overhead

- $34,583 listed payroll

- $89,400 break-even monthly revenue

What this means

- $69,600 Year 1 average revenue

- Extra owner pay is not covered

- Debt service cuts owner cash further

- Reserves should come before distributions

What drives owner income most?

1

$8.35K/ptQuoting Accuracy

Every 1 margin point on Year 1 revenue adds about $8,350, so tighter quotes go straight to take-home.

2

$835K-$7.76MOrder Volume

Revenue grows from $835K in Year 1 to $7.76M by Year 5, so order count is the main scale lever.

3

$150-$950Mix Quality

Higher-value desks and lamp fixtures lift revenue per order, while low-ticket batches dilute margin.

4

$415KLabor Utilization

Year 1 payroll is $415K, so higher machine and labor use turns fixed staff cost into more gross profit.

5

$12-$80Material Yield

Direct inputs run from $12 to $80 per unit, so scrap and rework can erase margin fast.

6

$19.6K/moOverhead Control

Fixed overhead is $19.6K a month, and reserve control matters because break-even needs about $89.4K in monthly revenue.

Made-to-Order Manufacturing Core Six Income Drivers

Quoting Accuracy

Quoting Accuracy

Thin quotes cut owner pay fast. Custom work lives or dies on quote accuracy. If you miss material cost, setup hours, direct labor, revisions, or change orders, revenue can look fine while gross margin slips. On $835,000 of Year 1 revenue, every 1-point margin miss costs $8,350 before taxes and reserves. That hits jobs like desk specs, prototype tolerances, lamp wiring, and wall art finishes.

The owner’s take-home depends on charging enough for spec changes and rework. If a desk needs one extra revision or a prototype tolerance shifts, the quote has to cover it. Better quotes protect cash, keep hidden labor from eating profit, and leave more income available for owner pay.

Quote from real inputs

Price the work, not the hope. Build each quote from quoted material cost, setup hours, direct labor, revision allowance, and target margin. Don’t start with a market price and hope it works. If the job needs more hands-on time than planned, the quote must charge for it or the owner is subsidizing the order.

Track quote-to-actual on every order and compare the margin gap by product type. If wall art finishes or custom wiring keep overrunning, raise the standard quote, add change-order rules, or require pre-approval for spec changes. That keeps margin from leaking into overtime, rush fixes, and lower owner draws.

1

Order Volume and Backlog Quality

Qualified Order Backlog

Order volume only helps if the jobs are real, priced well, and likely to ship. The key inputs are completed orders, booked backlog, conversion rate, cancellation risk, and revenue per production slot. In the plan, Year 1 has 2,900 orders and $835,000 revenue, while Year 5 reaches 24,000 orders and $776 million. That gap shows why backlog quality matters as much as volume.

Here’s the quick math: more qualified orders keep labor and machines busy, so fixed payroll gets spread across more output. But if the backlog fills with low-margin or cancel-prone jobs, work rises without the same lift in owner cash. One clean line: busy is not the same as profitable.

Track Fill Rate, Not Noise

Measure orders at the point they become production-ready, not when they are just inquiries. The owner should watch:

- Booked backlog by margin band

- Cancellation rate before release

- Revenue per production slot

- Completed orders versus planned output

If slots are full but margin is weak, cash flow can still lag. The fix is simple: prioritize jobs that cover labor, materials, and setup time before you add more volume.

2

Average Order Value and Product Mix

Average Order Value

When your mix shifts from wall art at $150 to desks at $850 and prototypes at $500, blended AOV rises from about $288 in Year 1 to about $323 in Year 5. That lifts revenue per production slot, but only if engineering time, setup time, and rework stay priced in. If the mix gets more complex without better pricing, owner take-home gets squeezed by hidden labor and delay costs.

The key inputs are blended AOV, product mix, order count, setup hours, engineering hours, and rework rate. Higher-ticket jobs help only when the extra work is billed. If a custom desk takes twice the setup time but sells at a thin premium, revenue looks better while cash and margin get worse.

Price for Complexity

Track AOV by product line, not just in total. Set price floors for desks, prototypes, and other high-touch jobs so added design and setup time is covered. Then review rework on every batch; if revisions rise, your real margin falls even when AOV rises.

- Track AOV by product line.

- Price setup and engineering separately.

- Watch rework after every run.

3

Material Yield and Supplier Control

Material Yield and Supplier Control

If material waste drifts up, the owner feels it twice: gross profit falls and cash gets stuck in extra inventory. In Year 1, unit COGS totals $137,700 across wood, steel, acrylic, wiring, resin, packaging, and labor-linked inputs, so small scrap or supplier-price misses can quickly cut the cash left for owner pay.

This driver depends on BOM accuracy (bill of materials, the exact parts list), scrap rate, supplier pricing, minimum order quantities, and inventory turns. Spec changes and rush orders raise waste, and the model shows 120% revenue-based production cost risk, so tighter control matters before any distribution is made.

Track Yield Before You Buy

Track planned versus actual material use on every order. Compare quoted BOM cost, purchased quantity, scrap, and rework by product line; if one part or finish is driving repeat waste, reprice it or stop offering it. Faster inventory turns matter too, because slow-moving wood, steel, or resin ties up cash that could go to labor or owner draw.

Set purchase rules around supplier pricing and minimum order quantities, and lock change-order fees before production starts. Here’s the quick math: if materials are already a big share of unit COGS, every avoided scrap run protects margin and cash. The goal is simple: buy closer to need, waste less, and keep profit available for the owner.

- BOM accuracy versus actual use

- Scrap rate by product line

- Supplier pricing changes

- Minimum order quantities impact

- Inventory turns each month

4

Labor Efficiency and Machine Utilization

Labor Efficiency and Machine Utilization

Labor efficiency is how many good units you finish per paid hour, and machine utilization is how much of available machine time is actually used. In made-to-order manufacturing, better scheduling lifts throughput without the same rise in labor cost, so more backlog turns into cash and owner pay. The listed technician base rises from 20 FTE in Year 1 to 120 FTE in Year 5, so idle hours get expensive fast.

Track direct labor hours, setup time, technician utilization, throughput, and rework hours. Keep direct production labor separate from owner labor, support, software, and admin overhead, because only production efficiency tells you if the shop is converting demand into margin. If hiring outruns orders, payroll grows before revenue does, and cash available for distributions falls.

Measure and tighten utilization

Build the schedule from confirmed backlog, not hope. Here’s the quick math: more completed jobs per shift only helps if setup time and rework hours stay flat or fall. If utilization is high but rework climbs, profit leaks back out. The owner’s take-home improves when each paid hour produces more sellable output, not just more motion.

Review weekly: planned hours, actual hours, machine uptime, and rework by product type. Then set hiring to demand, not to the largest forecast. A shop with 120 FTE can burn cash fast if the backlog is weak, but the same team can turn backlog into owner-pay capacity when slots are filled and changeovers are sequenced cleanly.

5

Overhead, Debt Service, and Reserves

Overhead, Debt Service, and Reserves

This driver is the fixed cash burden that comes out before owner pay: facility lease, software, insurance, accounting, communication, maintenance, debt payments, and a working capital reserve. Here, fixed overhead is $19,600 per month, or $235,200 per year. That cash must be covered before the owner can pull meaningful income.

The main inputs are monthly fixed costs, debt service, and the reserve target. Payroll is listed at $415,000 in Year 1 and $122 million in Year 5, so the business has a big cost stack to carry. Even profitable months can block distributions if repairs, inventory buys, or slow collections absorb cash.

Track cash before owner draw

Measure overhead as a hard monthly cash plan, not a leftover number. Track lease, software, insurance, accounting, communication, maintenance, debt payments, and reserve funding separately so you can see what is fixed and what moves with volume. One clean rule: no owner distribution unless cash stays positive after those items.

Watch collections and inventory timing closely. If receivables slow down or a machine repair lands, the reserve protects payroll and vendor payments first, and owner pay second. That keeps profitable months from turning into cash crunches.

6

Owner income scenario objective

Owner income scenarios

Owner income moves hard with order volume, pricing, and fixed plant payroll. The low case stays cash-tight, while the base and high cases show what scale can support.

| Scenario | Low CaseCash-tight | Base CaseScalable | High CaseManagement-heavy |

|---|---|---|---|

| Launch model | This is the lower earnings path, where the model is still building volume and owner draw is constrained. | This is the modeled middle path, where volume and margin are strong enough to support steady owner income. | This is the stronger earnings path, where the business runs at higher volume and owner income rises fast. |

| Typical setup | Year 1 shows about 2,900 orders, $288 AOV, $835,000 revenue, 71.5% gross margin, and a loss before taxes and reserves, with no extra distribution supported. | Year 3 reaches about 10,900 orders, $305 AOV, $3.319 million revenue, 72.4% gross margin, and $1.10 million operating profit before reserves. | Year 5 reaches about 24,000 orders, $323 AOV, $7.761 million revenue, 73.2% gross margin, and $3.64 million operating profit before taxes, debt, and reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0No draw | $1.10MCore case | $3.64MUpside case |

| Best fit | Use this to stress test the launch period when plant costs and payroll outrun cash flow. | Use this as the main planning case for a growing operation with repeat demand and tighter control of plant costs. | Use this to test upside when the shop has enough capacity, sales support, and working capital to keep up. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Made-to-Order Manufacturing Porter's Five Forces Analysis

- Made-to-Order Manufacturing BCG Matrix

- Made-to-Order Manufacturing Business Model Canvas

- How Increase Profitability In Made-To-Order Manufacturing?

- Made-to-Order Manufacturing Business Plan Template in Pre-Written Word

- How Increase Profitability In Made-To-Order Manufacturing?

- How Increase Made-To-Order Manufacturing Profitability?

- Made-to-Order Manufacturing Startup Costs: Plan For $792K Cash

- Made-to-Order Manufacturing Financial Model Template in Excel

- How to Open a Made-to-Order Manufacturing Business in 8 to 20 Weeks

- How Increase Profitability In Made-To-Order Manufacturing?

- Made-to-Order Manufacturing Marketing Mix

- Made-to-Order Manufacturing Marketing Plan

- Made-to-Order Manufacturing Business Proposal

- Made-to-Order Manufacturing PESTEL Analysis

- Made-to-Order Manufacturing Pitch Deck Example Editable PPTX

- Made-to-Order Manufacturing Business SWOT Analysis

- Made-to-Order Manufacturing Value Proposition Canvas

Frequently Asked Questions

The model supports $110,000 of annual General Manager compensation if the owner fills that role In Year 1, the business still shows about a $144,000 operating loss before taxes and reserves, so extra distributions are not supported By Year 5, operating profit reaches about $364 million before reserves, debt, and taxes