Owner income$80k+

Owner income$80k+How Much Does a Makeup Salon Owner Make? $80K Salary Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$80k+  Net margin-19% to 26%

Net margin-19% to 26% Revenue for target pay$380k

Revenue for target pay$380k Business difficultyHard

Business difficultyHard

You’re trying to see if a makeup salon can pay you, not just stay busy These first five-year planning assumptions show $286k to $804k in annual revenue, an $80k owner-manager salary, and EBITDA moving from -$53k to $207k before taxes, debt service, and owner distributions

Owner income$80k+Net margin-19% to 26%Revenue for target pay$380kBusiness difficultyHardWhat would your makeup salon pay you?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

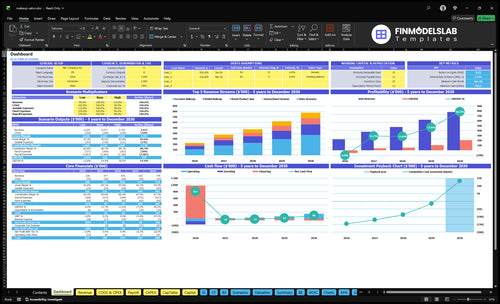

Can you check owner income in the Makeup Salon financial model?

The screenshot shows dashboard, assumptions, booking forecast, pricing mix, costs, payroll, owner pay, EBITDA, breakeven, cash, and scenarios. It runs revenue from $286k to $804k, EBITDA from -$53k to $207k, with Month 14 breakeven, 55-month payback, and $100k startup capex. Open the Makeup Salon Financial Model Template to test owner salary, hiring, rent, bridal mix, marketing, reserves, and downside cases.

Owner-income model highlights

- Owner pay is built in

- Revenue reaches $804k

- Scenarios test downside cases

How much revenue does a makeup salon need for owner pay?

A Makeup Salon should not promise a fixed $80k owner salary unless revenue is well above Year 1 levels. In the model, $286k revenue still leaves -$53k EBITDA, while about $380k revenue supports $44k EBITDA at the Year 1 price mix, so owner pay has to track volume, overhead, and booking quality.

Revenue and pay

- $286k revenue still loses money

- -$53k EBITDA after payroll and costs

- $380k revenue reaches $44k EBITDA

- Owner pay needs stronger volume

What drives the target

- Average ticket changes booking needs

- No-shows cut real revenue fast

- Bridal packages lift ticket size

- Artist staffing tightens overhead

Is a makeup salon profitable?

Yes, a Makeup Salon can be profitable, but this model loses money first: -$53k EBITDA in Year 1, then turns positive at $44k in Year 2 and reaches $207k by Year 5. Breakeven occurs in Month 14, so the key question is not demand alone; it’s whether booked revenue grows faster than payroll and fixed overhead, as explained in What Is The Most Important Indicator Of Success For Your Makeup Salon?. The one-liner is simple: busy chairs don’t help if payroll outruns booked revenue.

Profit Timing

- Year 1 EBITDA: -$53k

- Year 2 EBITDA: $44k

- Year 5 EBITDA: $207k

- Breakeven: Month 14

Main Levers

- Raise booking density per artist

- Grow average ticket: $143 to $17860

- Increase bridal mix: 100% to 120%

- Control payroll timing and overhead

What makeup salon costs reduce profit margin?

In a Makeup Salon, the biggest margin killers are product COGS, payment fees, marketing, and payroll, so gross margin looks better than operating margin on paper. For startup context, see How Much Does It Cost To Open, Start, And Launch Your Makeup Salon Business? Year 1 product COGS are 82% of revenue, split between 30% professional cosmetics and 52% retail product COGS, while payment fees add 25% and performance marketing adds 40%. Fixed overhead is $5,150/month before wages, and payroll is the biggest pressure point with an $80k owner salary, $65k lead artist salary, and $15k admin cost.

Gross margin drag

- 82% product COGS in Year 1

- 30% professional cosmetics

- 52% retail product COGS

- Gross margin gets hit first

Operating margin drag

- 25% payment fees

- 40% performance marketing

- $5,150/month fixed overhead

- Payroll can outrun bookings fast

Want the six main makeup salon income drivers?

1

8-18/dayBooking Volume

More booked visits spread rent and staff cost over more sales, so owner profit rises fastest here.

2

$143-$178Average Ticket

A higher ticket lifts revenue from every appointment, especially when bridal and instructional work sell more.

3

$160K-$318KLabor Model

Payroll is the biggest cost block, so staffing too early can erase the gain from more bookings.

4

10%-12%Bridal Mix

More bridal work pushes up the average sale, but it also needs tighter timing and prep.

5

$5.15K/moFixed Overhead

Rent and the rest of fixed overhead set the breakeven floor, so every extra dollar here matters.

6

4%-3%Acquisition Efficiency

Lower marketing spend keeps more cash from each booking, and the savings add up as volume grows.

Makeup Salon Core Six Income Drivers

Booking Volume

Booking Volume

Booking volume means paid visits, not inquiries. In this model, volume grows from 8 visits/day to 18 visits/day across 250 operating days, so annual visits rise from 2,000 to 4,500. That can push revenue from $286k to $804k when price and mix also improve.

The owner only pays out if each extra booking covers artist labor, product use, rent, admin time, and no-show risk. One clean rule: more bookings help only when the added visit is profitable, not just busy.

Track Paid Visits, Not Leads

Measure booked visits per day, show rate, and the split between weekdays and weekends. Empty weekdays hurt cash flow, while overbooked weekends can strain staff and raise service errors. A simple forecast should start with paid visits, then subtract no-shows and slow days before you count owner pay.

Test calendar rules that fill gaps without discounting premium slots. Keep an eye on whether extra visits still leave room for labor, supplies, and admin. 2,000 visits at low margin can pay less than 4,500 visits with stronger pricing and mix, so volume has to work with margin, not against it.

1

Average Service Ticket

Average Service Ticket

The ticket matters because each visit has to cover makeup labor, product use, and part of overhead. In the provided model, average service ticket rises from $143 in Year 1 to $17,860 in Year 5, driven by bridal work, instructional sessions, retail, and add-ons.

The cleanest lift is add-ons: per-visit add-on revenue moves from $15 to $25, so owner take-home improves only if conversion holds and product COGS stay controlled. The risk is pricing past local demand or discounting premium services too often, which lifts volume on paper but weakens margin.

Track ticket by visit type

Measure average ticket, add-on rate, retail attach rate, and discount rate by bridal, instructional, and occasion visits. Here’s the quick math: more ticket per booked client means more gross profit to cover fixed costs and pay the owner, as long as product spend and labor stay in line.

- Track ticket by service type

- Watch add-ons per client

- Protect premium pricing

- Limit discounting on peak dates

2

Bridal and Event Mix

Bridal Mix

Bridal work lifts owner income because the $350 Year 1 bridal price is about 2.9x the $120 occasion makeup price. If the bridal mix rises from 100% to 120%, revenue per booked client can move up fast, especially when trials, deposits, group bookings, and travel fees are charged on top.

What this hides: bridal jobs take more coordination time, hit weekends hard, and can create travel gaps. That raises staffing needs and can squeeze margins if packages do not cover labor. The owner only keeps the upside when each bridal booking protects the calendar and pays for prep, artist time, and no-show risk.

Price the bridal package, not just the face

Track revenue per bridal client, deposit rate, travel fees collected, and trial conversion. The key check is simple: if a bridal slot does not earn more than a standard event slot after extra coordination and staffing, it is hurting owner pay.

- Require deposits to hold dates.

- Charge for trials and travel.

- Bundle group bookings by event.

- Schedule weekends before weekdays.

One clean rule: protect the calendar first, then price the labor.

3

Artist Labor Model

Artist Labor and Owner Pay

Labor is the main growth engine here, but it also drives the biggest margin risk. Payroll starts at $160k in Year 1 and reaches $3,175k in Year 5, so owner pay only improves if added bookings cover wages, product use, and admin time.

This model includes an $80k owner-manager, a $65k lead artist, junior artists, admin coverage, and a part-time marketing role later. Owner-done services lift gross margin, but they cap capacity; staffed services expand volume, but only if revenue per artist and booked hours per week stay high.

Track Artist Utilization

Watch the math on every pay period. The key inputs are booked visits, hours sold per artist, wage per role, and the share of work done by the owner versus staff. If payroll rises faster than booked hours, take-home income gets squeezed even when sales look strong.

- Track revenue per artist each week.

- Track booked hours, not just inquiries.

- Keep weekend coverage tight.

- Use owner time on highest-ticket jobs.

Here’s the useful test: if the calendar is full but artists are underbooked, margin leaks through idle labor. If owner services fill the highest-value slots, margin improves; if staff handles more volume, set a utilization target so labor stays tied to cash collected.

4

Fixed Overhead

Fixed overhead

Fixed overhead is the monthly nut the salon pays before owner profit. Here it is $5,150/month: $3,500 rent, $400 utilities, $150 insurance, $250 software, $300 professional fees, plus cleaning, supplies, and website costs. This spend does not fall when bookings slow, so weak weeks hit the owner’s take-home fast. One clean rule: if cash is thin, owner pay comes last.

To size income, compare booked revenue and contribution against that $5,150 floor. Slow months still carry rent and software, so the salon needs reserves before any distribution. If the calendar softens, the owner’s income drops even if service demand later rebounds, because fixed costs keep draining cash while sales catch up.

Cover the monthly nut first

Track three inputs: booked clients, average ticket, and cash reserve. Then map them to monthly overhead so you know the minimum sales needed before owner draw. The key test is simple: if a weak month cannot cover $5,150, pause distributions and protect cash.

- Review rent and software monthly

- Keep one month of overhead cash

- Cut low-use tools fast

Check overhead creep every quarter. If bookings stay soft on weekdays, trim nonessential software, supplies, or outside fees before they eat profit. The owner should not pull money out until the salon has paid the fixed bill stack and still has room for the next slow month.

5

Client Acquisition Efficiency

Client Acquisition Efficiency

This driver is the gap between attention and paid bookings. In this salon model, marketing must create booked appointments, not just followers. The plan assumes paid marketing falls from 40% of revenue in Year 1 to 30% in Year 5 as reviews, referrals, bridal vendor ties, and repeat clients do more work. If leads do not turn into deposits, owner take-home drops fast.

Turn leads into deposits

Track cost per booked client as marketing spend divided by booked clients, plus inquiry-to-booking rate, deposit rate, and repeat purchase rate. A lead is only useful if it becomes a paid visit with cash in hand. That is where profit starts.

- Measure booked clients by source.

- Separate paid, referral, and repeat leads.

- Watch deposit losses from slow follow-up.

- Shift spend to high-ticket bridal demand.

Owner income improves when marketing fills profitable slots at the right ticket. If bookings skew to low-value weekdays or no-shows rise, ads become a cost, not a growth tool. Better reviews and vendor referrals lower paid acquisition pressure, which protects cash flow and leaves more margin for the owner draw.

6

Compare lean, base, and high makeup salon income scenarios

Owner income scenarios

Visit volume, ticket size, and payroll move owner income fast. Year 1 is salary-tight, Year 3 turns profitable, and Year 5 opens room for distributions.

| Scenario | Low CaseBreakeven Month 14 | Base CasePayback 55 months | High CaseCash upside |

|---|---|---|---|

| Launch model | This case keeps the salon at Year 1 volume and pricing, so the owner mostly lives on salary while the business absorbs early losses. | This case uses Year 3 traffic and pricing, which brings EBITDA into the black and starts to support owner draw on top of salary. | This case uses Year 5 volume, pricing, and staffing, so the business can fund salary and meaningful profit distributions. |

| Typical setup | About 8 visits a day, 250 open days, a $143 average ticket, -$53k EBITDA, and $80k planned owner salary with early cash pressure. | About 12 visits a day, a $161.50 average ticket, $485k revenue, $55k EBITDA, and a heavier payroll base across the core team. | About 18 visits a day, a $178.60 average ticket, $804k revenue, $207k EBITDA, and about $317.5k payroll at a larger team size. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $80k salary onlyCash-stress start | $135k total compStabilized case | $287k total compDistributions room |

| Best fit | Use this to stress-test the opening year and see what happens before the salon reaches break-even. | Use this as the working plan for steady operations after the first ramp year. | Use this to test upside if the salon fills capacity and keeps staffing efficient. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Makeup Salon Porter's Five Forces Analysis

- Makeup Salon BCG Matrix

- Makeup Salon Business Model Canvas

- 7 Essential KPIs to Track for a Makeup Salon

- Makeup Salon Business Plan Template in Pre-Written Word

- How to Increase Makeup Salon Profitability in 7 Actionable Strategies

- How Much Does It Cost To Run A Makeup Salon Monthly?

- Makeup Salon Startup Cost: $100K Setup Plus 14-Month Breakeven

- Makeup Salon Pro Forma & 5-Year Financial Model Template in Excel

- How To Open A Makeup Salon In 6 To 12 Weeks With Bookings

- How to Write a Business Plan for a Makeup Salon in 7 Simple Steps

- Makeup Salon Marketing Mix

- Makeup Salon Marketing Plan

- Makeup Salon Business Proposal

- Makeup Salon PESTEL Analysis

- Makeup Salon Pitch Deck Example Editable PPTX

- Makeup Salon Business SWOT Analysis

- Makeup Salon Value Proposition Canvas

Frequently Asked Questions

The model plans an $80k owner-manager salary each year, but profit distributions depend on cash EBITDA is -$53k in Year 1, then rises to $44k in Year 2 and $207k in Year 5 That means early take-home may rely on funding, while later take-home can include salary plus possible distributions