Owner income$165k

Owner income$165kHow Much Can a Manuscript Assessment Service Owner Make? $95k–$165k

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$165k  Net margin15.7%

Net margin15.7% Revenue for target pay$1.05M

Revenue for target pay$1.05M Business difficultyHard

Business difficultyHard

You’re pricing expert feedback, managing reviewers, and trying to turn manuscript work into owner income These planning assumptions show $447k Year 1 revenue, $70k EBITDA, and a $95k Managing Director salary, with breakeven in Month 6 Figures cover revenue, gross margin, costs, reserves, and workload before taxes they are not guaranteed earnings, salary data, or tax advice

Owner income$165kNet margin15.7%Revenue for target pay$1.05MBusiness difficultyHardWant to test your manuscript assessment income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will change with pricing, volume, staffing, taxes, debt, and reserve policy.

How do you check owner income in the Manuscript Assessment Service model?

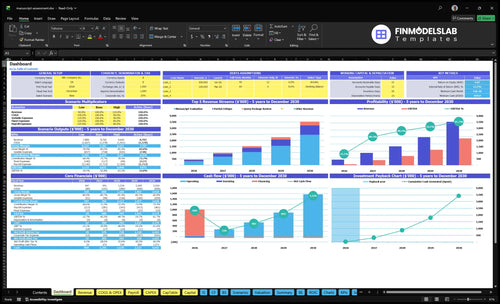

This dashboard shows revenue, EBITDA, owner salary, breakeven month, payback, and cash need in the Manuscript Assessment Service Financial Model Template. Open it.

Owner-income model highlights

- Year 1 vs Year 5

- Assumptions drive scenarios

- Margin expansion is charted

Can a manuscript assessment service make good money?

Yes, a Manuscript Assessment Service can make good money if pricing, volume, and reviewer quality stay tight; see How Much To Launch Manuscript Assessment Service Business? for startup cost context. The Year 1 model shows $447k revenue, a $95k owner-manager salary, and $70k EBITDA, while Year 5 reaches $3.524M revenue and $2.174M EBITDA only with scaled operations.

Money Works If

- Hold reviewer quality steady

- Control turnaround time

- Protect pricing discipline

- Keep utilization high

Main Constraint

- Full evaluations need 12 billable hours

- Solo capacity caps revenue

- Contractors add scale risk

- EBITDA means operating profit before financing and taxes

What costs reduce manuscript evaluation gross margin?

If you’re mapping How To Launch Manuscript Assessment Service Business?, the gross margin drag comes from direct delivery costs, not overhead. In Year 1, that means 18% freelance editor pay plus 2% manuscript management software fees, then 3% payment processing and 5% referral commissions on each job.

Hits gross margin

- 18% freelance editor payments

- 2% manuscript software fees

- 3% payment processing

- 5% referral commissions

Does not hit gross margin

- $1,950 monthly overhead

- Hosting, CRM, insurance, storage

- Accounting and virtual office

- $1,845k payroll, plus $15k marketing

That overhead still matters, but it cuts EBITDA and cash, not gross margin. So the clean read is: separate service delivery costs from fixed cost load, then watch reserves because they can reduce distributable cash even when EBITDA stays positive.

Can a manuscript assessment service scale?

Yes, the Manuscript Assessment Service can scale, but owner income won’t rise automatically. At 63 projects a month in Year 1 and an implied 359 projects a month by Year 5, the real limit is reviewer capacity and quality control, not demand. Here’s the quick math: at a $819 weighted fee and 12 billable hours per full evaluation, volume growth can strain onboarding, coordination, and turnaround fast.

Year 1 load

- 63 projects per month

- 756 billable hours monthly

- $819 weighted fee per project

- Margins depend on utilization

Year 5 pressure

- 359 projects per month

- 4,308 billable hours monthly

- QC becomes the bottleneck

- Slow onboarding hurts margin

What drives manuscript assessment owner income most?

1

$596Pricing Mix

The Year 1 blended fee is $596, so small shifts toward higher-priced packages lift revenue fast without adding much extra work.

2

63/moAssessment Volume

About 63 monthly assessments drives the top line, and every added project drops more revenue into owner income if quality holds.

3

18%Editor Labor

Freelance editor payments start at 18% of revenue, so tighter delivery labor keeps more gross profit in the business.

4

67 hrsScope Load

A 67-hour weighted workload stretches capacity, so bigger manuscripts can raise revenue but also slow throughput and cash flow.

5

$120Client CAC

With a $120 acquisition cost, better conversion lowers payback time and leaves more of each sale for owner take-home.

6

$1.95KOverhead

Fixed overhead is $1,950 a month before the $95,000 owner salary, so cost control decides how much revenue turns into cash.

Manuscript Assessment Service Core Six Income Drivers

Average Assessment Fee And Package Mix

Average Fee and Package Mix

Income starts with average realized fee per project, not inquiry count. In Year 1, the weighted fee is $596, built from $1,020 manuscript evaluations, $380 partial critiques, and $220 query package reviews. If volume stays flat, moving to the Year 5 weighted fee of about $819 lifts revenue by about 37% ($819 ÷ $596), but only if clients accept the price.

Package mix drives take-home income because each service has a different price and delivery load. By Year 5, manuscript evaluations reach 48% of the mix, so the fee rises as the offer shifts upmarket. Price has to fit scope, depth, manuscript length, and author segment, or higher fees can cut conversion and leave the owner with fewer paid projects.

Track mix before you raise prices

Measure weighted fee = total assessment revenue ÷ completed assessments each month, then split it by package. Watch which offer sells best at $1,020, $380, and $220. If the mix tilts toward low-price reviews, revenue per project falls even when inquiry volume looks healthy.

- Track fee by package monthly

- Track conversion by package

- Set page and scope limits

- Test price changes in steps

- Document clear deliverables

What this estimate hides is simple: a higher posted price only helps if the offer feels worth it. Clear deliverables, turnaround time, and length tiers protect conversion and keep the owner’s cash flow steadier than a vague premium offer.

1

Completed Assessments Per Month

Completed Assessments Per Month

Owner income tracks paid completed assessments, not inquiries. Here’s the quick math: $447k in Year 1 at a $596 weighted fee implies about 750 projects a year, or 63 a month. That volume is what has to clear before the owner can pay themselves well.

By Year 3, the plan needs about 183 assessments a month at a $699 weighted fee. By Year 5, it jumps to 359 a month at $819. Because a full evaluation takes 12 billable hours, late work can quickly turn into missed referrals and weaker repeat demand.

Track Throughput, Not Leads

Measure inquiry-to-paid conversion, completed assessments per month, and average turnaround time. If completions rise but deadlines slip, the extra revenue can vanish in rework, reviewer load, and lost referrals. One clean rule: every paid assessment should fit a clear delivery slot before it is sold.

- Track paid completions weekly.

- Flag any 12-hour jobs early.

- Protect deadlines on full evaluations.

2

Owner Versus Reviewer Delivery Cost

Delivery Labor Mix

Delivery labor is a direct margin driver here. Year 1 freelance editor pay is 18% of revenue, easing to 16% by Year 5, so the spread between owner-performed work and outside review changes how much cash stays in the business. Owner work can save cash early, but it also caps how many manuscript reviews you can complete.

With full evaluations taking 12 billable hours, contractor-heavy delivery can raise volume, but it adds quality-control time and reviewer management. Treat reviewer pay as direct project cost, not overhead. If turnaround slips, referral demand can soften, and that hits owner pay fast.

Track Reviewer Cost per Project

Here’s the quick math: start with completed assessments, then split delivery labor between owner hours and reviewer hours. Measure reviewer pay as a percent of revenue, plus the time you spend checking samples and fixing revisions. If that hidden management time rises, your real gross margin drops even when contractor rates look flat.

Use a simple control set:

- Track reviewer pay by project.

- Cap turnaround time by package.

- Review samples before scaling.

- Price scope before work starts.

Hybrid delivery works best when the owner sets standards, checks a sample of work, and keeps feedback consistent. If quality varies by reviewer, rework eats margin and delays cash collection.

3

Manuscript Scope And Length Control

Scope and Length Control

Scope drives labor cost and owner pay. Full manuscript evaluations use 12 billable hours, partial critiques use 4, and query package reviews use 2. With a 67-hour weighted workload per project in Year 1, longer books, deeper reports, rush timelines, and follow-up calls can push real labor above plan and squeeze margin.

Here’s the quick math: if a project shifts from a 2-hour review to a 12-hour evaluation, labor load rises 6x. If price does not rise with scope, gross margin falls and the owner earns less per hour. This driver matters most when revisions keep growing after the first read.

Set Scope Limits Up Front

Track page count, word count, package type, and promised deliverables before you quote. Use length tiers, defined report sections, and paid add-ons for rush work or extra calls so scope does not leak into unpaid labor. One clean rule: price the work you will actually do, not the work you hope it stays at.

Measure hours per project against package mix and flag anything above plan. If full evaluations are consuming more than 12 billable hours, or if follow-up calls are adding time without new revenue, tighten the revision limit, shorten the feedback format, or reprice the add-on. That protects cash flow and keeps owner income tied to paid output.

- Track hours by package

- Cap follow-up call time

- Charge for rush timelines

- Set page-count tiers

- Invoice extra feedback separately

4

Client Acquisition And Author Conversion

Qualified Author Demand

Client acquisition only helps owner pay when it turns into paid assessments. In Year 1, a $15k marketing budget at $120 CAC buys about 125 customers. If lead quality is weak, sales time rises and cash returns fall, even if inquiry count looks busy. Referrals are cheaper, but the business still needs qualified authors who can buy the right package.

Year 1 referrals cost 5% of revenue, or about $22.4k on $447k revenue, then drop to 3% by Year 5. That helps margin, but only if workshops, content, and partnerships feed the paid assessment funnel. Inquiries are not income. The real driver is inquiry-to-paid conversion and completed project volume.

Track Conversion By Source

Measure inquiry-to-paid conversion, CAC by channel, package mix by source, and completed project volume. Here’s the quick math: if one channel brings cheap leads but low closes, it can still hurt profit because staff time gets wasted before a sale. Use source-level tracking so you can shift spend toward the channels that produce full manuscript evaluations, not just clicks.

Test referrals, workshops, content, and partnerships as feeders into paid assessments, then watch whether those sources increase average order value and reduce CAC from $120 toward $95 by Year 5. Better leads protect owner income. Unqualified leads do the opposite because they slow response time, lower close rates, and crowd out higher-value project work.

5

Overhead, Reserves, And Owner Pay Discipline

Overhead, Reserves, And Owner Pay

Owner income is what’s left after $1,950 per month in fixed overhead, delivery payroll, and reserve set-asides. In this model, distributable owner income is not the same as profit, because taxes, legal structure, and planned distributions can pull cash apart fast.

What this estimate hides is timing. Year 1 payroll is $1,845k, including a $95k Managing Director salary, and $375k of capex sits in the portal, website, hardware, framework, identity, onboarding, and resource library. If reserves are skipped, owner pay gets funded from cash you still need for operations.

Track Cash Before You Pay Yourself

Measure monthly cash after overhead, payroll, and reserve targets. The overhead base includes hosting, CRM, insurance, storage, accounting, and virtual office, so even a small rise in fixed cost can cut distributable income. One clean rule: no owner draw until the reserve bucket is full.

- Track overhead by line item monthly.

- Separate tax reserves from profit.

- Set owner pay after cash coverage.

- Review capex cash needs before draws.

Use three inputs to set owner pay: monthly revenue, total operating costs, and reserve policy. If operating cash is thin, keep distributions modest and leave room for legal and tax needs. That discipline protects the business when project volume dips or payment timing slips.

6

Compare lean, base, and high owner-income scenarios

Owner income scenarios

Income swings with service mix, billable hours, referral costs, and staffing as the business moves from lean launch to high volume.

| Scenario | Lean CaseLean Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | Year 1 is the lower-income path, with a small but active book of clients and the owner still close to every review. | Year 3 is the modeled middle path, with steadier demand and a larger team supporting more throughput. | Year 5 is the stronger earnings path, but it needs high volume, tighter process control, and more working cash. |

| Typical setup | Year 1 mix, about 63 assessments a month, $447k revenue, a $596 weighted fee, 72% contribution, $70k EBITDA, and a $95k owner salary keep the model hands-on and lean. | Year 3 mix, about 183 assessments a month, $1.534M revenue, a $699 fee, 74.5% contribution, $747k EBITDA, and $842k before reserves point to a busier but still efficient operation. | Year 5 mix, about 359 assessments a month, $3.524M revenue, an $819 fee, 77% contribution, $2.174M EBITDA, and $2.269M before reserves show the upside and the strain. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $165kLean owner income | $842kBase owner income | $2.269MHigh owner income |

| Best fit | Best for founders stress-testing early demand, thin staffing, and quality control when volume is still modest. | Best for planning the most likely operating case and checking how much staff and referral spend the model can carry. | Best for testing upside, staffing load, cash need, and quality risk when the business runs at full pace. |

Planning note: Scenario ranges are researched planning assumptions only, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Manuscript Assessment Service Porter's Five Forces Analysis

- Manuscript Assessment Service BCG Matrix

- Manuscript Assessment Service Business Model Canvas

- What Are The 5 Core KPI Metrics For Manuscript Assessment Service?

- Manuscript Assessment Service Business Plan Template in Pre-Written Word

- How Increase Profitability Of Manuscript Assessment Service?

- What Are Operating Costs For Manuscript Assessment Service?

- Manuscript Assessment Startup Costs: $375K CAPEX, $859K Cash

- Manuscript Assessment Financial Model Template in Excel

- Start A Manuscript Assessment Service With A 12-Hour Core Offer

- How Increase Manuscript Assessment Service Profitability?

- Manuscript Assessment Service Marketing Mix

- Manuscript Assessment Service Marketing Plan

- Manuscript Assessment Service Business Proposal

- Manuscript Assessment Service PESTEL Analysis

- Manuscript Assessment Service Pitch Deck Example Editable PPTX

- Manuscript Assessment Service Business SWOT Analysis

- Manuscript Assessment Service Value Proposition Canvas

Frequently Asked Questions

The model shows a minimum cash need of $859k, with the lowest cash point in Month 2 That includes early staffing, marketing, fixed costs, and $375k of capex for portal, website, hardware, framework, identity, onboarding, and resource setup It is a planning cash cushion, not a required legal minimum