Owner income$301k–$2.4M

Owner income$301k–$2.4MHow Much Does a Marble and Granite Fabrication Owner Make at $122M?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$301k–$2.4M  Net margin25%–58%

Net margin25%–58% Revenue for target pay$486k

Revenue for target pay$486k Business difficultyHard

Business difficultyHard

You’re looking at owner take-home, not just sales This estimate uses a first-year to mature-year model with $122M to $4103M in annual revenue, 440 to 1,190 completed jobs, listed product costs, and caveats for overhead, debt, reserves, reinvestment, and personal taxes

Owner income$301k–$2.4MNet margin25%–58%Revenue for target pay$486kBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, labor, overhead, reserves, debt service, and target pay.

Planning note: Research-based planning estimate only; it is not guaranteed salary, tax advice, or owner distribution advice.

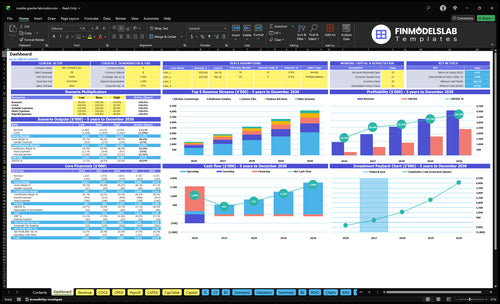

Want to see the Marble and Granite Fabrication financial model?

Open the Marble and Granite Fabrication Financial Model Template to review the dashboard, revenue assumptions, unit volume, pricing, COGS, labor, equipment, overhead, debt service, reserves, scenarios, and owner income. The charts connect kitchen countertops, bathroom vanities, custom tiles, fireplace surrounds, and outdoor kitchens to annual revenue, with first-year revenue at $122M and mature-year revenue at $4103M; use it as a planning tool, not tax advice or an income guarantee.

Owner-income model highlights

- Owner income outputs shown

- Revenue and margin drivers

- Volume, pricing, and COGS

- Scenarios and reserves built in

How does the owner’s role change income and risk?

Marble and Granite Fabrication usually preserves cash when the owner stays hands-on, because the owner can sell, template, fabricate, install, and manage jobs directly. That also shifts risk onto the owner’s time, so income depends on labor, quality, and scheduling, not just sales. At 367 jobs per month, one bad install week can hit cash fast; at 992 jobs per month, systems and managers matter more than owner labor.

Income stays owner-led

- Owner sells and closes jobs

- Owner templates and measures

- Owner fabricates and installs

- Cash stays tighter

Risk shifts with scale

- Payroll adds fixed cost

- Equipment needs steady use

- Scheduling errors hit margins

- Managers replace owner labor

How much can a granite countertop shop owner make?

A Marble and Granite Fabrication shop owner can’t be valued by a salary claim alone; the better answer is by shop size, job count, and what’s left after fixed costs, debt, payroll, and reinvestment. In the provided model, scale runs from 440 jobs and $1.22M revenue in an owner-operated year to 1,190 jobs and $4.103M revenue at higher volume, so What Is The Primary Metric That Reflects The Success Of Marble And Granite Fabrication? is tied more to throughput and margin control than top-line sales alone.

By shop size

- Owner-operated: 440 jobs

- First-year revenue: $1.22M

- Crew-supported: 658–865 jobs

- Mid-scale revenue: $1.918M–$2.615M

What owner keeps

- High volume: 1,032–1,190 jobs

- Revenue range: $3.322M–$4.103M

- Depends on overhead and payroll

- Subtract debt, reserves, reinvestment

What affects marble and granite fabrication profit margin most?

Profit margin in Marble and Granite Fabrication comes down most to slab buying, slab utilization, remnant control, breakage, rework, labor hours, install quality, and pricing discipline. For the startup math, see How Much Does It Cost To Open And Launch Your Marble And Granite Fabrication Business? because a kitchen countertop carries $675 in first-year cost plus 0.8% of revenue, or $711 on a $4,500 sale. Bathroom vanities run $180 plus 0.8% ($189.60 on $1,200), and custom tile runs $450 plus 0.8% ($474 on $3,000), so overhead still decides owner take-home.

Top margin drivers

- Slab purchase price sets the base.

- Utilization cuts waste and lifts yield.

- Remnant control protects usable leftovers.

- Pricing discipline keeps jobs profitable.

Hidden cost leaks

- Breakage destroys margin fast.

- Rework adds labor and delay.

- Install quality can trigger callbacks.

- Overhead still decides take-home.

Want to see the six main income drivers?

1

$1.22M-$4.10MJob Volume

From 440 jobs in Year 1 to 1,190 in Year 5, more installs push revenue up fast and do most of the cash work.

2

82%-84%Gross Margin

Keeping direct cost near 15% and cutting slab waste and rework keeps more cash in each job before fixed costs.

3

$1.2K-$10KSales Mix

More kitchens and outdoor kitchens raise blended revenue per order, while fewer fixes stop margin from leaking.

4

$2.8K-$3.4KAvg Ticket

A higher blended ticket lets the same crew hours and shop space create more revenue per install.

5

$222K-$410K/FTELabor Productivity

Higher revenue per shop FTE slows payroll growth and lets more sales drop to owner take-home.

6

$16.3K/moOverhead Load

Lean rent, insurance, software, utilities, vehicles, and admin costs matter because they hit every month.

Marble and Granite Fabrication Core Six Income Drivers

Installed Job Volume

Installed Job Volume

More completed, paid countertop jobs lift revenue only when the shop can keep up. The forecast moves from 440 annual jobs to 1,190 annual jobs, or about 37 to 99 jobs per month. If capacity breaks, extra volume turns into overtime, missed templates, install delays, and callbacks, which cuts the cash that can flow to the owner.

The inputs that matter are paid jobs, template-to-install timing, crew hours, and callback rate. The owner wins when added volume uses existing shop capacity first, before adding new fixed costs like more labor, vehicles, or shop overhead. One clean rule: more jobs only help if each one still closes on time and on spec.

Measure Capacity Before Pushing More Jobs

Track booked jobs, templated jobs, installed jobs, and paid jobs each week. Here’s the quick math: 1,190 ÷ 12 = 99 jobs per month, so the real test is whether the current team can hold that pace without overtime or rework. If paid volume rises but callbacks rise too, margin falls fast.

Set a hard ceiling for install slots and labor hours, then compare it to actual throughput. Add volume only when the shop still hits schedule, fit, and finish targets. That keeps gross profit cleaner and leaves more cash for owner pay instead of fixing avoidable mistakes.

1

Average Project Ticket

Average Project Ticket

Average project ticket is the revenue per installed job, and it depends on product mix first. First-year prices run from $1,200 for bathroom vanities to $8,000 for outdoor kitchens; mature-year prices widen to $1,500 to $10,000. Bigger tickets lift revenue and can support owner pay, but only if the added complexity does not eat the margin.

Here’s the quick math: average ticket = total installed revenue ÷ installed jobs. Higher-ticket work can raise cash per project, but premium stone, edge profiles, backsplashes, sinks, and outdoor work can add labor, breakage, and rework. That means a higher sales number does not always mean higher take-home income if install costs rise faster.

Price for Mix, Not Just Size

Track average ticket by job type, not just by month. Split out vanities, kitchens, and outdoor work, then compare each ticket to direct labor, breakage, and callback cost. A $10,000 job with heavy rework can be worse than a clean $6,000 job. One bad template can wipe out the gain from several small installs.

- Track ticket by product line

- Price add-ons separately

- Measure labor hours per job

- Log breakage and rework

Push the mix toward higher-ticket work only when the shop can hold quality. Use measured templates, clear scope notes, and upfront pricing for sinks, backsplashes, and outdoor installs. If mature-year tickets reach $1,500 to $10,000, protect gross margin first, because that margin is what turns sales into owner draw.

2

Gross Margin And Slab Utilization

Slab Yield And Gross Margin

Gross margin here is the money left after raw slab cost, before labor, overhead, and owner pay. On the figures given, a kitchen countertop sells for $4,500 with $500 in slab cost, a bathroom vanity sells for $1,200 with $100 in slab cost, and custom tiles sell for $3,000 with $300 in slab cost. That means raw material takes only 11.1%, 8.3%, and 10% of sales.

The real swing factor is slab utilization, or how much of each slab turns into billable product. Layout, waste disposal, breakage, remnants, and markup decide whether that $4,000, $1,100, or $2,700 left after slab cost can cover shop overhead and still leave a draw for the owner. One bad cut plan can wipe out the margin on a job that looked profitable on paper.

Track Yield, Not Just Sales

Measure slab cost per job, sale price, usable yield, breakage, and disposal cost on every install. Here’s the quick math: if the slab share stays near the numbers above, pricing has room; if waste climbs, margin shrinks fast. Build a job sheet that shows remnant use and rework so you can see which template or cut pattern is hurting owner income.

Set a floor for each product line. If a kitchen, vanity, or tile job needs heavy layout waste, charge for it upfront or push the cut plan to a higher markup. Higher sales with poor yield still pay the bills badly. The goal is to protect the dollars left after materials so fixed overhead and owner pay do not get squeezed by avoidable scrap.

- Track slab yield by job.

- Price waste into tough layouts.

- Charge for breakage and remakes.

- Use remnants where cuts fit.

3

Labor Productivity

Labor Productivity

Labor productivity is how much paid countertop work the shop ships per labor hour after overtime, subcontractors, and rework. Direct fabrication labor is disclosed at $120 for kitchen countertops, $50 for bathroom vanities, and $100 for custom tiles, so every extra hour or callback cuts the cash left for overhead and owner draw.

Accurate templating, clean cut files, efficient polishing, and tight install scheduling protect margin. If a job needs return visits, the original gross margin turns into unpaid labor fast, and that hits net income before the owner sees any profit.

Track Hours by Job

Track planned labor hours versus actual hours for each job type, plus overtime, subcontractor spend, and callback time. That tells you whether a kitchen job stays near its $120 labor target or quietly runs over and eats the draw.

Use the data to fix the bottleneck: better templates, cleaner CNC files, faster polishing, and tighter install calendars. If rework is rising, price the extra labor into the job or stop the leak before it hits cash flow.

4

Equipment And Facility Overhead

Shop Overhead Load

This driver is the shop overhead that sits between gross profit and owner pay: rent, utilities, insurance, tooling, repairs, vehicles, and stone fabrication equipment. The disclosed COGS pieces alone total 8% of COGS: factory utilities 2%, indirect shop supplies 1%, equipment maintenance 3%, quality control 1%, an d waste disposal 1%. If installed revenue is thin, these fixed bills can block owner draw.

Here’s the quick math: the more jobs the shop installs without adding new fixed costs, the more overhead is spread across each sale. But if rent, insurance, truck costs, or machine payments rise faster than installed revenue, cash flow tightens fast. What this estimate hides is idle shop time, rework, and downtime on fabrication equipment.

Track Overhead per Job

Track overhead as a percent of installed revenue and as dollars per job. The key inputs are monthly rent, utilities, insurance, tooling, repair spend, vehicle costs, equipment payments, and installed job count. If overhead per job falls while capacity stays full, owner income improves because more gross profit reaches the bottom line.

Set a minimum monthly installed revenue target that covers these fixed costs first, then pay owner draw from the leftover. That keeps a busy month from masking a weak cash month.

- Separate fixed and variable shop costs.

- Budget maintenance before breakdowns.

- Review overhead every month.

- Delay owner draw until coverage is stable.

5

Sales Channel And Rework Control

Sales Channel and Rework Control

Channel mix changes owner income because retail jobs usually carry higher prices but take more design time, while builder and contractor jobs bring volume with tighter pricing and slower payment. Commercial jobs can be larger, but cash comes later. When jobs range from $1,200 vanities to $10,000 outdoor kitchens, the real win is the cash left after selling time, not just the sale.

Rework means fix-up work after the first template, cut, or install. Change orders, wrong measurements, and callbacks eat labor and delay collections, so a strong sales month can still cut take-home pay. Owner draw, or take-home pay, only grows when the job is sold, installed, invoiced, and collected with little waste.

Track channel profit, not just sales

Measure each job by channel, design hours, rework hours, and days to collect. That shows which mix creates the best margin and cash, not just the biggest top line.

- Tag retail, builder, contractor, commercial.

- Log change orders before fabrication.

- Count callbacks by job and installer.

- Age receivables by channel.

- Price design time separately when needed.

If one channel books fast but pays late, it can still starve owner cash. Tight measurement control and clear approvals protect margin better than chasing volume.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income moves with job volume, pricing, and payroll load in this shop. The low, base, and high cases show how full the plant runs and how fast equipment payback hits cash.

| Scenario | Low CaseTough start | Base CaseSteady run | High CaseCapacity upside |

|---|---|---|---|

| Launch model | This is the lower owner-income path, tied to a slower ramp and tighter cash. | This is the modeled owner-income path, built on the middle-year run rate. | This is the stronger owner-income path, tied to higher volume and better plant use. |

| Typical setup | About 440 jobs and $1.22M revenue, or 36.7 jobs a month, with gross margin near 85% before commissions, a hands-on owner, and early payroll, lease, and equipment payments. | About 865 jobs and $2.615M revenue, or 72.1 jobs a month, with a fuller product mix, a staffed shop, and margin pressure from labor burden, overhead, and reserve spending. | About 1,190 jobs and $4.103M revenue, or 99.2 jobs a month, with closer-to-capacity output, firmer pricing, and more room after fixed overhead and equipment payments. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Low five-figure drawThin take-home | Mid five-figure drawSteady take-home | Upper six-figure drawStrong take-home |

| Best fit | Use this to stress-test a slower ramp, thinner cash, and a founder who must cover sales and operations. | Use this as the main planning case for a steady shop mix and normal hiring. | Use this if the shop fills capacity, keeps pricing firm, and avoids cash leaks. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. Financing costs, owner tax, and any perks or dividends not shown in the model are not included.

Related Products

- Marble and Granite Fabrication Porter's Five Forces Analysis

- Marble and Granite Fabrication BCG Matrix

- Marble and Granite Fabrication Business Model Canvas

- 7 Critical KPIs to Scale Marble and Granite Fabrication

- Marble And Granite Business Plan Template in Pre-Written Word

- How to Boost Marble and Granite Fabrication Profit Margins

- How To Calculate Monthly Running Costs for Marble and Granite Fabrication

- Marble And Granite Fabrication Startup Costs For 440 First-Year Jobs

- Marble and Granite Fabrication Financial Model Template in Excel

- How To Open A Marble And Granite Fabrication Business In 4–9 Months

- How to Write a Marble and Granite Fabrication Business Plan

- Marble and Granite Fabrication Marketing Mix

- Marble and Granite Fabrication Marketing Plan

- Marble and Granite Fabrication Business Proposal

- Marble and Granite Fabrication PESTEL Analysis

- Marble and Granite Fabrication Pitch Deck Example Editable PPTX

- Marble and Granite Fabrication Business SWOT Analysis

- Marble and Granite Fabrication Value Proposition Canvas

Frequently Asked Questions

The provided data supports revenue planning, not a fixed owner salary The model shows $122M first-year revenue from 440 jobs and $4103M mature-year revenue from 1,190 jobs Owner take-home depends on rent, equipment payments, admin payroll, debt service, reserves, reinvestment, and personal tax treatment