Owner income$675k–$1.39M

Owner income$675k–$1.39MHow Much Does A Meadery Owner Make? $675k Year 1 Cash View

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$675k–$1.39M  Net margin38%–51%

Net margin38%–51% Revenue for target pay$1.15M–$3.09M

Revenue for target pay$1.15M–$3.09M Business difficultyHard

Business difficultyHard

You’re looking at owner pay from a US craft meadery with an on-site tasting room, bottle sales, events, clubs, and limited wholesale In the provided model, first-year revenue is $1147M, blended gross margin is 831%, and cash before owner pay, taxes, debt service, and reserves is about $675k This is not tax, legal, or alcohol distribution advice

Owner income$675k–$1.39MNet margin38%–51%Revenue for target pay$1.15M–$3.09MBusiness difficultyHardWant to test your meadery owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will shift with sales mix, staffing, aging inventory, compliance costs, debt, and reinvestment needs.

Want to see owner income in one Meadery and Tasting Room model?

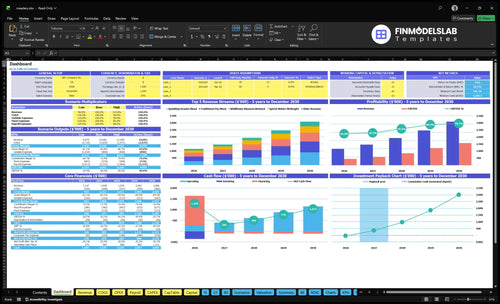

This Meadery and Tasting Room Financial Model Template ties revenue, production costs, staffing, fixed overhead, cash flow, reserves, and owner take-home into one view. Open the model to check the assumptions behind the charts and tables.

Owner-income model highlights

- Owner take-home output

- Revenue and margin trend

- Scenarios and cash flow

The model also maps product lines like Traditional Dry Mead, Wildflower Blossom Melomel, Spiced Winter Metheglin, Sparkling Session Mead, and Reserve Barrel Aged Mead. Year 1 to Year 5 revenue runs from $1147M to $3086M, with gross margin moving from about 831% to 844%.

Does a meadery make more from tasting room or wholesale?

A Meadery and Tasting Room usually makes more owner income from tasting room sales than wholesale because flights, pours, bottle sales, clubs, and events keep more retail value in-house; see How Much To Open A Meadery And Tasting Room? for startup cost context. With modeled product prices of $18 to $55 per unit, wholesale can add volume, but it lowers realized revenue per unit and can tie up cash in inventory.

Tasting room wins

- Capture retail price per bottle

- Add flights and by-the-glass sales

- Build clubs, events, and repeat visits

- Best fit for ages 21-40

Wholesale tradeoff

- Compare revenue per unit

- Track gross margin by channel

- Count labor hours per sale

- Watch cash collection speed

How much revenue does a meadery need to pay the owner?

For a Meadery and Tasting Room, start with contribution margin, not total sales. With Year 1 revenue of $11.47M, $1.941M in COGS, and $1.204M in variable expenses, contribution is about $8.324M, or 72.6%. That puts break-even before owner pay, taxes, debt, and reserves at roughly $492k in annual revenue, and every $1k of owner pay needs about $1.38k of revenue at that margin.

Core margin math

- $11.47M Year 1 revenue

- $1.941M COGS

- $1.204M variable expenses

- 72.6% contribution margin

Owner pay floor

- $357.2k fixed payroll plus overhead

- Break-even at about $492k

- $1k owner pay needs $1.38k revenue

- This is before taxes and reserves

Can a small meadery be profitable?

Yes—a small Meadery and Tasting Room can be profitable, but only if local demand is steady, seasonality is managed, and fixed costs stay tight. In the model, Year 1 revenue reaches $1.147M with an 83% gross margin, which leaves about $675k before owner pay, taxes, debt, and reserves. Payroll is $242k in Year 1 and rises to $354k in Year 4, so scale only helps if traffic and sell-through keep up with production.

Profit drivers

- $1.147M Year 1 revenue

- 83% gross margin

- $675k before owner pay

- Local demand must stay strong

Cost pressure

- $242k payroll in Year 1

- $354k payroll in Year 4

- Owner labor cuts cash costs

- Staffing helps hours and events

Want the six meadery income drivers?

1

$1.15MTasting Traffic

More visitors lift bottle sales and tasting revenue, and Year 1 revenue is $1.147M.

2

$18-$65Visitor Spend

Each extra bottle or reserve pour lifts take-home fast because the product price span runs from $18 to $65.

3

10.5%Direct Sales Mix

More on-site and direct sales help keep the variable expense load near 10.5% instead of letting fees eat margin.

4

$3.20-$9.20Unit Cost

Batch cost swings from $3.20 to $9.20 per unit, so yield loss cuts owner income quickly.

5

$242KPayroll

Year 1 wages total $242K, so staffing choices shape the cash left after sales.

6

$115KFixed Overhead

Fixed costs run about $115K a year, and that base has to be covered before owner profit shows up.

Meadery and Tasting Room Core Six Income Drivers

Tasting Room Traffic

Tasting Room Traffic

More visitors only helps owner pay when they buy, book, or join. Track visitors per day, average ticket, bottle-to-go conversion, club conversion, and event attendance. A crowded room with weak conversion just raises labor and supply costs, but qualified traffic lifts profit by spreading fixed overhead across more sales.

Track conversion, not foot traffic

Watch weekend spikes closely. If traffic jumps but staffing hours and pour costs rise at the same pace, owner income can stall. Here’s the quick math: each extra guest should add flights, pours, bottles, or a booking fast enough to protect gross margin. If the room needs more staff, pre-schedule them by daypart and tie labor to expected conversion.

Measure each visit by tickets sold, club signups, and repeat orders. A simple rule: more heads are good only when the room converts them into cash, not just noise.

1

Average Visitor Spend

Average Visitor Spend

Average visitor spend is the money each guest leaves per visit. It includes flights, full pours, bottles to go, premium releases, gift packs, and event add-ons. The key metric is average visitor spend = tasting room revenue ÷ visitors. If the ticket moves from $18 in Year 1 toward $65 for Reserve Barrel Aged Mead in Year 5, revenue can rise without equal traffic growth.

This driver matters because higher spend per guest can lift owner take-home faster than chasing more foot traffic. The risk is simple: if price rises faster than the tasting experience, perceived quality, and repeat purchase behavior, return visits can fall. Price power only sticks when the room feels worth it.

Raise spend, not just volume

Track spend by visit type and by item mix. Separate flights, by-the-glass sales, bottles, gift packs, and event add-ons so you can see what actually lifts the ticket. Watch visitors, average ticket, and bottle-to-go rate each week. If spend rises but repeat visits slip, the price move is too sharp.

Use premium releases and pairing offers to raise spend without forcing every guest into the top price. Test small steps first, then check whether full pours, reserve bottles, and event add-ons increase enough to justify the higher ticket. If the product story feels weak, the higher price will not hold.

- Measure spend by visit type.

- Test premium add-ons first.

- Watch repeat visits after price changes.

2

Direct-To-Consumer Mix

Direct-to-Consumer Mix

DTC mix means the share of sales from tasting room bottles, clubs, private tastings, events, and repeat orders. It usually pays better than wholesale, but only if discounts, fulfillment, club churn, and event labor stay under control. With card processing at 30% of revenue, the margin gain can vanish fast if the mix shifts toward low-ticket sales.

The key inputs are DTC share, wholesale share, average order value, discounts, fulfillment cost, and club churn. Higher DTC share usually means more cash for owner pay, because you keep more of each sale, but only after staffing and compliance costs. More direct sales help only when cash margin rises faster than sales costs.

Track the mix, not just revenue

Track DTC share by channel each month, then split it by tasting room, club, events, and repeat orders. Compare each channel’s margin after card fees, labor, and fulfillment. If wholesale is lower-priced but steadier, use it as the floor and push DTC where the margin is clearly better.

Test club churn, event labor hours, and discount depth before you scale. If compliance, customer acquisition, or staffing costs rise faster than DTC revenue, owner pay can fall even while sales grow. The quick check: if a higher DTC mix does not lift cash after fees and labor, it is not helping income yet.

3

Production Cost And Yield

Production Cost And Yield

Production cost drives gross margin and how much cash stays in inventory. Here’s the quick math: unit COGS is $375 for Traditional Dry Mead, $530 for Wildflower Blossom Melomel, $455 for Spiced Winter Metheglin, $320 for Sparkling Session Mead, and $920 for Reserve Barrel Aged Mead, plus revenue-based COGS of 10% to 32%.

Better yield means more sellable bottles from the same batch, so owner cash rises faster. But if honey costs swing, fruit runs short, barrels leak, or packaging gets pricier, margin falls fast. Quality matters too: batch inconsistency can cut repeat purchases, so a cheap batch that tastes off can hurt take-home income later.

Track Batch Yield Hard

Measure cost per finished bottle by style, not just total batch spend. Track input loss, spoilage, packaging cost, and sellable yield each run. If a reserve batch sits near $920 COGS, small waste can wipe out profit fast, so standardize recipes, weigh losses, and compare actual yield to plan every batch.

- Log honey and fruit costs each batch

- Track barrel loss and packaging breakage

- Compare planned vs. finished bottles

- Watch repeat sales after recipe changes

Keep one rule: protect margin without dulling the flavor. If cost cuts lower quality, repeat orders drop and the owner loses cash twice, first in margin and then in future sales.

4

Labor Model

Labor Model

The labor model decides how much of production, tasting room shifts, events, admin, bookkeeping, and compliance is paid staff work versus owner work. Here, payroll is $242k in Year 1 with a Head Mazer at $75k, Tasting Room Manager at $55k, Production Assistant at $42k, and two tasting room staff at $35k each. By Year 4, payroll reaches $354k, so owner take-home depends on keeping labor matched to sales.

If the owner is covering unpaid shifts and calling that profit, the books can overstate real income. Unpaid owner labor is not free labor. Watch weekends, events, and compliance work closely, because weak staffing can hurt service and cash flow at the same time.

Right-Size Roles and Hours

Track labor by function, not just headcount. Measure production hours, tasting room coverage, event labor, admin time, and compliance work against sales days and visitor traffic, then price and staff from that plan.

Compare payroll of $242k in Year 1 and $354k in Year 4 against the revenue plan. If payroll rises faster than bottle sales, tasting room sales, or event income, owner pay gets squeezed. Right-sized labor protects service, cash flow, and the ability to pay the owner.

- Track hours by function

- Separate owner and paid labor

- Price for weekend coverage

- Forecast event labor first

5

Fixed Overhead And Debt Service

Fixed Overhead And Debt Service

$96k/month in fixed overhead, or $1.152M/year , is a hard cash drag before debt service. That includes $55k lease, $850 insurance, $12k utilities and internet, $450 compliance software, $600 maintenance, and $1k professional services. If gross margin looks healthy but sales slow, owner pay still gets squeezed because these costs do not flex much.

The key inputs are monthly lease, insurance, utilities, admin software, maintenance, professional fees, plus loan payments and reserve targets. Debt service and reserves are not provided, so model them separately. If operating cash does not clear fixed overhead after variable costs, any owner draw is coming from a thin cushion.

Track Monthly Cash Break-Even

Track the monthly cash break-even: fixed overhead plus debt service, divided by gross margin dollars. Then test slow months, because tasting room traffic can fall while rent and support costs stay fixed. If you can lift average ticket or bottle mix, each extra dollar of gross profit helps owner pay more than cutting costs that are already locked in.

Watch loan terms, maintenance, and reserve gaps first. Equipment loans and surprise repairs can turn accounting profit into thin cash fast. Update the 12-month forecast every month, and set a cash reserve before owner draws. If the plan cannot cover $96k plus debt service in a weak season, delay distributions.

6

Compare lean, base, and high meadery owner income cases

Owner income cases

Owner income moves with traffic, mix, labor, and reserves. These low, base, and high cases show how much cash can flow to the owner under different operating patterns.

| Scenario | Low CaseOwner-operated | Base CaseStaffed growth | High CaseInventory-heavy |

|---|---|---|---|

| Launch model | Traffic runs light, tickets stay low, and the owner covers more of the work. | The model follows the source Year 1 plan with steady volume and enough cash to fund normal operations. | Stronger traffic, a richer premium mix, and better yield push owner income higher. |

| Typical setup | This is a lean tasting room with weaker direct-to-consumer mix, higher labor burden, and tighter cash after reserves. | Year 1 revenue is about $1.147M, with modeled EBITDA of $438k and cash before owner pay, taxes, debt, and reserves of about $675k. | This case assumes more direct-to-consumer sales, tighter payroll control, and more inventory tied up in aging stock. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Below base caseLean income | About $675kModeled base | Upper six figuresUpside case |

| Best fit | Use this to stress-test early demand and slow repeat visits. | Use this as the planning case for staffing, pricing, and cash control. | Use this to test what happens if demand and premium sales beat plan. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Meadery and Tasting Room Porter's Five Forces Analysis

- Meadery and Tasting Room BCG Matrix

- Meadery and Tasting Room Business Model Canvas

- What Are The 5 Core KPIs For Meadery And Tasting Room Business?

- Meadery and Tasting Room Business Plan Template in Pre-Written Word

- How Increase Profits Meadery And Tasting Room?

- What Are Operating Costs For Meadery And Tasting Room?

- How Much It Costs To Start A Meadery: $358K CAPEX Plan

- Meadery And Tasting Room Financial Model Template in Excel

- How to Open a Meadery and Tasting Room in 9-18 Months

- How To Write A Business Plan For Meadery And Tasting Room?

- Meadery and Tasting Room Marketing Mix

- Meadery and Tasting Room Marketing Plan

- Meadery and Tasting Room Business Proposal

- Meadery and Tasting Room PESTEL Analysis

- Meadery And Tasting Room Pitch Deck Example Editable PPTX

- Meadery and Tasting Room Business SWOT Analysis

- Meadery and Tasting Room Value Proposition Canvas

Frequently Asked Questions

A meadery owner can take home only the cash left after business needs are covered In the provided Year 1 model, revenue is $1147M, gross profit is about $953k, and cash before owner pay, taxes, debt, and reserves is about $675k Actual owner income may be much lower if inventory, equipment, debt, or taxes absorb cash