Owner income$73.7M-$815.5M

Owner income$73.7M-$815.5MHow Much a Brand Mention Tracking Service Owner Can Make: $737M EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$73.7M-$815.5M  Net margin79%-84%

Net margin79%-84% Revenue for target pay$93.2M

Revenue for target pay$93.2M Business difficultyMedium

Business difficultyMedium

A brand mention tracking service owner can only take home what remains after data costs, hosting, payroll, marketing, reserves, taxes, and reinvestment In the provided assumptions, EBITDA is $73719M in Year 1 and $815473M in Year 5, which is the available profit pool before owner pay decisions and excluded items Here’s the quick math: Year 1 revenue of $93191M with 130% cloud and API COGS leaves an 870% gross margin before sales commissions and payment fees The model reaches break-even in Month 1, but owner take-home is still a policy choice, not a guaranteed salary

Owner income$73.7M-$815.5MNet margin79%-84%Revenue for target pay$93.2MBusiness difficultyMediumWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

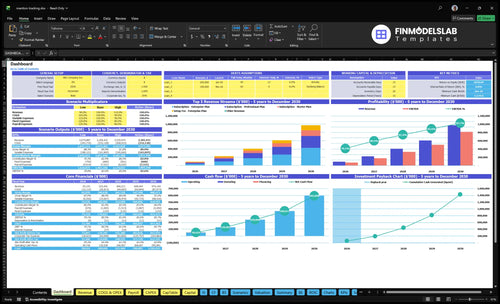

How do I check owner income in the financial model?

This screenshot shows revenue, EBITDA, minimum cash, break-even month, payback month, and owner pay assumptions; open the Brand Mention Tracking Service Financial Model Template. Year 1 revenue is $93,191, Year 1 EBITDA is $73,719, and Year 5 revenue reaches $974,144.

Owner-income model highlights

- Owner pay capacity

- Revenue and EBITDA

- Scenario tabs change inputs

How much profit can a brand mention tracking service make?

A Brand Mention Tracking Service can be profitable fast on paper: this How To Write A Business Plan For Brand Mention Tracking Service? model shows EBITDA of $73,719M in Year 1, $179,823M in Year 2, $331,404M in Year 3, $502,848M in Year 4, and $815,473M in Year 5. Still, that profit is not owner take-home until reserves, taxes, debt service, and reinvestment are covered.

Profit Drivers

- Keep subscription churn low

- Grow monthly recurring revenue

- Control data costs tightly

- Push annual prepaid plans

Owner Reality

- Reinvest early profit into engineers

- Improve data quality and alerts

- Fund sales and support headcount

- Lower data COGS from 130% to 90%

Can a brand mention tracking service scale profitably?

Yes, the Brand Mention Tracking Service can scale profitably, but only if automation keeps support load from rising faster than revenue. The founder-led model helps retention through onboarding, reporting, and issue handling, while the SaaS model needs self-serve setup, accurate alerts, billing automation, and report templates to cut manual cost. Payroll rises from $585k in Year 1 to $1,885M in Year 5, so revenue has to grow faster than staff or owner income gets squeezed.

Founder-led service

- Onboarding protects retention

- Reporting builds trust

- Issue handling keeps churn down

- Owner time stays capped

Automated SaaS model

- Self-serve setup cuts labor

- Billing automation speeds cash

- Report templates reduce manual work

- Alert quality must stay high

Revenue rises from $93,191M to $974,144M, and EBITDA rises from $73,719M to $815,473M, so the model works only if automation scales cleanly. If alerts get weaker, churn risk rises and owner income falls.

How much MRR is needed to pay the owner?

For the Brand Mention Tracking Service, the owner gets paid only after the business clears the operating floor: at a $249 Year 1 weighted ARPU and 80.1% contribution margin, you need about 350 paid accounts, or roughly $87,150 MRR, just to cover the fixed burden. Here’s the quick math: $249 × 80.1% = $199.45 contribution per account, and $69.75k in fixed monthly costs divided by that equals about 350. Owner pay needs extra MRR above that, plus reserves; taxes and debt service are not included.

Break-even MRR

- $249 weighted ARPU

- 80.1% contribution margin

- $199.45 per account

- 350 paid accounts needed

Owner pay add-on

- Start above $87.15k MRR

- Add reserves for cash safety

- Mix shifts change the target fast

- No taxes or debt service included

Want the six main income drivers?

1

31KPaid Accounts

More paid accounts push MRR up and spread the $585K Year 1 payroll and $11K monthly overhead across more seats, so owner pay rises fastest here.

2

$249ARPU

A higher weighted ARPU lifts monthly revenue, and with about 87% gross margin, most of the extra sales drop through to profit.

3

EditableRetention

Churn is not provided, so retention stays an editable lever; keeping accounts active protects MRR and avoids re-spending CAC.

4

13%-9%Data Costs

Cloud hosting and API fees run near 13% of revenue in Year 1 and fall to 9% by Year 5, so every point saved widens EBITDA.

5

$2-$3Acquisition Cost

With a $120K marketing budget and CAC around $2 to $3, cheaper acquisition buys more trials, shortens payback, and protects cash flow.

6

$585KAutomation

Year 1 payroll is $585K, so better automation cuts manual support work and gives the clearest lift to owner take-home.

Brand Mention Tracking Service Core Six Income Drivers

Paid Customers

Paid customers

Paid customers are the only accounts that turn into monthly recurring revenue (MRR). Free trials and freemium users do not cover the bills until they convert. In the Year 1 model, 100% of customers start on trial and only 50% convert to paid; by Year 5, trials rise to 150% and conversion reaches 100%.

More monitoring accounts help only if data use and support tickets do not grow faster. That is why 350 Year 1 paid accounts is the key threshold here: it roughly covers the modeled monthly burden before owner pay. Low-quality signups can still add alert noise and support work without adding matching revenue, which cuts cash flow fast.

Track paid conversion, not just trial volume

Measure active monitoring accounts separately from paid accounts, then watch trial-to-paid conversion, churn, and support tickets per account. Here’s the quick math: if signups rise but conversion stays at 50%, you still need more trials just to hold MRR. If support rises faster than revenue, owner pay gets squeezed.

- Review trial-to-paid weekly.

- Flag noisy accounts early.

- Cap support per low-value trial.

- Prioritize high-intent signup sources.

1

ARPU and Plan Packaging

Plan Packaging

ARPU (average revenue per user) is the monthly mix that decides how many paying accounts you need to cover staff, data, and owner pay. In Year 1, weighted ARPU is $249/month from $99 Starter, $299 Professional, and $999 Enterprise. Here’s the quick math: break-even account count = fixed costs ÷ ARPU, so higher ARPU directly lowers the account load.

Year 5 ARPU rises with $119 Starter, $349 Professional, $1,199 Enterprise, and a 200% Enterprise mix. That only helps if the extra price is tied to more tracked keywords, seats, alert volume, reporting, API access, or white-label use. Price hikes without better alerts or reports can raise churn and pull cash flow back down.

Price the value, not just the logo

Track ARPU by plan and by feature use. Separate starter users, professional teams, and enterprise accounts so you can see which upgrades actually lift monthly revenue and owner take-home income.

- Track keywords per account

- Track seats and alerts

- Watch report usage

- Test API and white-label demand

- Measure churn after price changes

If enterprise buyers do not use better reporting or more alerts, the higher price will not stick. Tie each tier jump to a clear feature gain, then forecast how many paid accounts are needed to cover payroll, data costs, and owner pay.

2

Retention and Churn

Retention and Churn

Retention protects monthly recurring revenue (MRR) and makes owner pay more predictable. Here, churn rate is the monthly loss rate, so it should stay as an editable model field. At Year 1 weighted ARPU of $249/month, every 10 retained accounts protect $2,490 MRR before any upsell. Lower churn means less paid acquisition just to stay flat, which improves cash flow.

Cut noisy alerts

Retention depends on clean onboarding, accurate alerts, useful integrations, low noise, and reports customers can send to their teams. If missed mentions or noisy alerts make the service feel optional, churn rises and expansion slows. Track active accounts vs. paying accounts, then watch expansion from more keywords, users, archives, reports, and Enterprise upgrades. One clean rule: trusted alerts keep subscriptions sticky.

- Model churn as a field.

- Separate active from paying users.

- Measure expansion by plan.

3

Data and API Costs

Data and API Costs

For this service, data and API cost is the first margin gate before owner pay. The model shows cloud hosting and data processing at 80% of revenue in Year 1 and 60% in Year 5, while API costs run 50% and 30%. That puts combined cost of goods sold (COGS) at 130% in Year 1 and 90% in Year 5, so gross margin starts negative and stays thin unless pricing and usage stay disciplined.

Here’s the quick math: at 130% COGS, each $1 of revenue uses $1.30 in direct cost, so there is no room for owner distributions. Even at 90% COGS, only $0.10 remains before overhead. More sources, tighter crawling limits, bigger archives, heavier AI analysis, and faster alerts all push cost up, so every extra point of COGS cuts owner-pay capacity.

Control Usage Before It Controls Margin

Track cost per monitored account, cost per source, and API spend as a share of revenue. If the service adds more keywords, history, or alert frequency without matching price, gross margin slips fast. A simple rule: price by usage tier, and cap costly features unless the plan covers them.

- Watch API spend weekly.

- Limit archive depth by plan.

- Test alert volume by segment.

- Reprice heavy data users.

Also separate base monitoring from high-cost add-ons like deep historical search and AI-heavy analysis. If direct cost rises from 90% toward 130%, the business can still grow revenue and lose cash. That is the point where owner draws get squeezed first.

4

Customer Acquisition Efficiency

Customer Acquisition Efficiency

CAC is the spend needed to win one paying account. In this model, annual marketing budget rises from $120k in Year 1 to $12M in Year 5, and the CAC assumption moves from $20 to $30; both are model inputs, not market guarantees. Active monitoring accounts do not fund owner pay until they convert.

Improve CAC Payback

Track where paid customers come from, how fast trials convert, and how many months it takes to recover CAC from subscription gross profit. Referrals, content, integrations, and niche positioning usually bring in higher-intent buyers, so payback improves and more cash stays in reserves and owner pay. Cheap acquisition is a trap if conversions lag.

- Marketing spend by channel

- Trial-to-paid conversion

- Paid accounts added

- CAC and payback months

5

Automation and Support Load

Automation and Support Load

Support load is a profit line, not just a service issue. In this model, payroll rises from $585k in Year 1 to $1,885M in Year 5 as engineering, data science, sales, and customer success headcount grow. If automation cuts manual work in onboarding, alerts, billing, reporting, and account health checks, EBITDA margin improves and the ow ner has more cash available to pay themselves.

The catch is churn. Self-serve keyword setup, saved report templates, alert tuning, and automated billing retries only help if they reduce tickets without making the product feel noisy or hard to trust. Less manual support should mean more recurring profit, not more churn.

Track Support Work per Account

Measure tickets, onboarding time, and alert noise by account tier. The key test is whether automation lowers support hours per paid customer while keeping retention stable. Track manual touches in the first 30 days, failed billing retries, report requests, and health-check escalations so you can see which workflows still need people.

Use automation where the volume repeats: self-serve setup, saved reports, billing retries, and alert tuning. If support drops but churn rises, the math fails fast. Every saved hour should either lift owner draw or protect it by keeping gross profit and renewals intact.

- Count tickets per active account.

- Track onboarding days to first value.

- Watch churn after alert changes.

- Audit failed payment retries monthly.

6

Scenario objective: compare low, base, and high owner income assumptions without promising results

Owner income scenarios

Paid customer mix, conversion, and data costs drive owner income here. The base case follows the model path, while low and high cases test slower growth or better Enterprise mix and automation.

| Scenario | Low CaseConservative | Base CaseModel Base | High CaseUpside |

|---|---|---|---|

| Launch model | Lower owner income comes from a softer launch with fewer paid customers and weaker margins. | The base case follows the modeled revenue and EBITDA path with steady scale. | Stronger owner income comes from a better mix, better retention, and leaner data costs. |

| Typical setup | Paid customer count lands below plan, conversion runs softer, the Starter plan stays heavy, and support plus acquisition pressure trim owner take-home. | Year 1 revenue is about $93.2M and EBITDA about $73.7M, rising to about $974.1M and $815.5M by Year 5 as paid customer count, average revenue per customer, and Enterprise mix scale. | Enterprise share rises faster, retention improves, and automation trims support and data costs, so owner take-home moves above the base path. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Below base take-homeDownside case | Modeled take-home pathBase case | Above base take-homeUpside case |

| Best fit | Use this to stress-test a slow launch, weak conversion, or heavier support load. | Use this as the planning anchor for budgets, hiring, and owner draws. | Use this to test a faster scale plan with better Enterprise sales and automation. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Brand Mention Tracking Service Porter's Five Forces Analysis

- Brand Mention Tracking Service BCG Matrix

- Brand Mention Tracking Service Business Model Canvas

- What Are The 5 Core KPIs For Brand Mention Tracking Service Business?

- Brand Mention Tracking Service Business Plan Template in Pre-Written Word

- How Increase Profits Brand Mention Tracking Service?

- What Are Operating Costs For Brand Mention Tracking Service?

- Brand Mention Tracking Service Startup Costs: $1135M Month 1 Cash

- Brand Mention Tracking Service Financial Model Template in Excel

- How To Start A Brand Mention Tracking Service In 4 To 8 Weeks

- How To Write A Business Plan For Brand Mention Tracking Service?

- Brand Mention Tracking Service Marketing Mix

- Brand Mention Tracking Service Marketing Plan

- Brand Mention Tracking Service Business Proposal

- Brand Mention Tracking Service PESTEL Analysis

- Brand Mention Tracking Service Pitch Deck Example Editable PPTX

- Brand Mention Tracking Service Business SWOT Analysis

- Brand Mention Tracking Service Value Proposition Canvas

Frequently Asked Questions

The model shows EBITDA capacity of $73719M in Year 1 and $815473M in Year 5, but that is not the owner’s guaranteed take-home Actual pay comes after reserves, taxes, debt service, and reinvestment No owner salary or distribution policy is provided, so EBITDA is the cleanest ceiling from the data