Owner income$250k

Owner income$250kHow Much Micro-Satellite Launch Owners Make After $11M Capex

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$250k  Net margin79%

Net margin79% Revenue for target pay≈$318k

Revenue for target pay≈$318k Business difficultyHard

Business difficultyHard

You’re planning owner income in a capital-heavy US launch service, not a simple salary business This view covers five years of revenue, mission costs, fixed aerospace overhead, reserves, capex, EBITDA, and founder pay versus distributions It excludes tax advice, guaranteed pay, investor waterfalls, and exact returns because outcomes depend on launch success, contracted backlog, and capital structure

Owner income$250kNet margin79%Revenue for target pay≈$318kBusiness difficultyHardWant to test your launch owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income is not guaranteed salary, tax advice, or owner distribution advice.

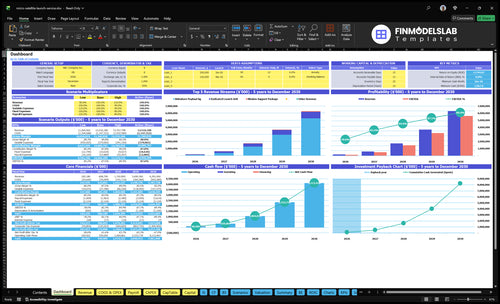

How do you check owner income in the Micro-Satellite Launch model?

This dashboard shows revenue, EBITDA, cash, reserves, and owner pay; open the Micro-Satellite Launch Financial Model Template. It also tracks launch cadence, payload pricing, mission costs, engineering payroll, insurance, capex, and five-year scenarios, from Year 1 EBITDA of $143,927 million to Year 5 EBITDA of $5,625 billion.

Owner-income model highlights

- CEO pay and distributions

- Revenue, EBITDA, cash

- Five-year scenario charts

How many launches per year does a micro-satellite launch service need?

There is no single launch count for Micro-Satellite Launch; the real answer depends on contracted backlog, not a fixed annual target. Year 1 has to cover $177,000 in monthly fixed overhead plus $122 million in payroll, and Year 5 payroll rises to $278 million. Year 1 implied revenue is about $182.945 million, but with direct costs at 195%, the schedule only works if rideshare kilograms, dedicated launch units, support packages, and ground station services are sold before launches are planned.

Cadence depends on backlog

- Backlog drives launch count.

- $177,000 monthly fixed overhead must clear.

- $122 million Year 1 payroll must fund.

- Year 5 payroll reaches $278 million.

Revenue must fill the vehicle

- Sell rideshare kilograms.

- Sell dedicated launch units.

- Sell support packages.

- Sell ground station services.

Should a micro-satellite launch owner reinvest or take income?

For Micro-Satellite Launch, reinvest first; early cash should stay in the business until launch cadence, reserves, and customer confidence are proven. The first big use is the $11 million capex stack: manufacturing facility, propulsion test stand, ground support equipment, tooling, lab equipment, launch control systems, and IT infrastructure. Salary can be planned, but owner distributions should come later, after reliability, regulatory readiness, insurance, and capacity are funded.

Reinvest first

- $11 million capex comes first

- Build the manufacturing facility

- Fund the propulsion test stand

- Buy launch control systems and IT

Take income later

- Plan salary, not early distributions

- Pay out after proven mission cadence

- Keep reserves for insurance and readiness

- Expand capacity before owner draws

When can a micro-satellite launch owner pay themselves?

A Micro-Satellite Launch owner can take planned payroll when the budget can fund it, but true owner distributions should wait until commercial launches are proven and cash is protected. The model includes a $250,000 CEO salary from Year 1, but as What Is The Current Growth Trend For Micro-Satellite Launch Business? shows, growth does not equal free cash until launch success, customer backlog, $1,968 million minimum cash, $11 million capex, and reinvestment needs are covered.

Pay Salary First

- Use payroll, not profit distributions

- Budget $250,000 CEO pay

- Protect launch reliability spend

- Delay pay if cadence slips

Wait On Distributions

- Prove successful launch execution

- Build contracted customer backlog

- Hold $1,968 million minimum cash

- Cover $11 million capex first

Want to see what moves owner income most?

1

10-28/moLaunch Cadence

More billable launch days spread fixed costs across more missions and raise owner cash.

2

$20K/kgPayload Pricing

A higher contract rate lifts revenue fast on each kilogram and dedicated launch unit.

3

50%-90%Manifest Fill

A fuller payload manifest keeps each launch from flying with empty, low-margin capacity.

4

10.5%-19.5%Direct Mission Cost

Lower variable launch cost keeps more of each contract as take-home profit.

5

$177K/moFixed Overhead

The $177K monthly base has to be covered before the business turns cash positive.

6

$1.97MCash Reserves

The $1.97M cash floor protects the $11M buildout and limits how much profit can be pulled out early.

Micro-Satellite Launch Core Six Income Drivers

Successful Launch Cadence

Successful Launch Cadence

Successful paid launches are what spread engineering, facilities, compliance, insurance, and management cost across revenue. Use actual completed paid launches, not planned dates, because a slipped mission can push revenue out while $177,000 per month in fixed overhead still runs before wages. One clean launch per contract helps cash flow; one slip hurts owner pay fast.

This driver matters because cadence only supports profit when missions are sold and completed. If a launch slips, rent, R&D lease, payroll, software, legal, accounting, and IT still burn cash, so EBITDA weakens even if backlog looks strong. The key input is completed paid missions per month, not launch intent or press-ready schedule.

Track completed launches, not booked dates

Measure signed contracts, completed launches, and schedule slip days. Here’s the quick math: more completed missions means the same fixed base gets spread thinner, so each flight carries more of the overhead load. If a mission is delayed, revenue recognition moves right, but fixed costs keep hitting the P&L.

- Booked missions vs completed missions

- Slip days per launch

- Overhead per completed launch

- Cash burn during delays

Keep a forecast built from completed paid launches only. That protects owner income by showing when cadence is real and when it is just a schedule on paper.

1

Contracted Payload Pricing

Contracted Payload Pricing

Owner income rises when contracts carry more revenue per kilogram, a higher dedicated mission value, or paid mission support. With Year 1 assumptions of $20,000 per kilogram for rideshare payloads, a 500 kg booking equals $10 million before support fees. A dedicated launch at $15 million and a $250,000 support package can help absorb the fixed $177,000 monthly overhead before wages.

This driver includes the contract price, payload mass, mission type, and service scope. Here’s the key point: higher pricing lifts cash flow and makes owner pay more reachable, but only if the market will sign at that level. Exact pricing should stay scenario-based and tied to the customer, orbit needs, and what the mission actually includes.

Track Price per Kilogram, Not Just Launch Count

Measure contracted $/kg, dedicated mission price, and support package revenue on every signed deal. Then compare booked revenue against payload mass, orbit needs, and service scope so you can see whether pricing is really covering overhead and funding profit, not just filling the manifest.

Use a simple watchlist: signed kilograms, average price per kilogram, support attach rate, and mission-level gross margin. If discounts creep in or service scope expands without a price reset, owner income drops fast even when launches stay busy. Price each mission from the customer’s use case, not from a fixed menu.

- Track signed $/kg by contract

- Separate rideshare, dedicated, support

- Test price by orbit and scope

- Reprice scope changes fast

2

Manifest Fill Rate

Manifest Fill Rate

Manifest fill rate is the share of launch capacity that is sold and contracted. In Year 1, the model assumes 500 payload kilograms at 50% occupancy, then scales to 4,000 kilograms and 90% occupancy by Year 5. Revenue only rises when booked kilograms rise, because empty slots still carry launch operations and compliance costs.

Here’s the quick math: thin manifests cut gross profit even if headline pricing stays high. Use booked kilograms and signed payloads, not theoretical capacity, because missed fill rates can delay owner distributions when the mission flies under capacity.

Track booked kilograms, not empty slots

Measure fill rate by mission and by month using sold payload kg ÷ available payload kg. Track signed payloads, launch-date slips, and revenue per kilogram together, since an underfilled flight still burns launch ops cash and can weaken take-home profit.

- Compare booked vs. available kilograms.

- Separate sold from theoretical capacity.

- Watch occupancy by mission month.

- Flag underfilled rideshare manifests early.

If fill rate stalls near 50%, owner pay stays under pressure because fixed mission costs still run. Moving toward 90% occupancy is the cleanest way to turn capacity into distributable profit.

3

Direct Launch Cost

Direct Launch Cost

Direct launch cost is the cost tied to each mission before overhead and owner pay: launch vehicle production, payload integration, launch operations fees, insurance, and mission-specific regulatory compliance. In this model, the direct cost load is 195% in Year 1 and 105% by Year 5, so gross profit is still under pressure until cost drops below revenue. If a mission brings in $10 million, Year 1 direct cost would be $19.5 million.

That matters because owner income comes from what is left after direct cost, then overhead. Here’s the quick math: if direct cost stays above 100% of revenue, the business can sell launches and still lose gross profit. Lower cost helps only if reliability, compliance, and customer trust hold up. Watch cost creep in vehicle manufacturing, propulsion, range, insurance, and integration, because those lines hit margin fast.

Control the mission cost stack

Track direct cost per mission against booked revenue, and split it by vehicle production, payload integration, launch operations, insurance, and regulatory work. Compare actual completed launches to plan, not just scheduled flights. If integration or insurance spikes, gross margin drops fast, and owner draws get pushed back even when sales look healthy.

Use a simple rule: every mission should show the path from revenue to gross profit before it is sold. Measure cost per kilogram, launch-specific fees, and rework from delays or payload changes. Keep cost cuts tied to flight reliability and compliance, because a cheaper launch that hurts trust can cost more in lost contracts and slower cash collection.

4

Fixed Aerospace Overhead

Fixed Overhead Burn

Fixed overhead can block owner income even when missions sell. This stack includes headquarters rent, the R&D lease, utilities, insurance, software, legal, accounting, and IT payroll, and it keeps running through delays and onboarding. The disclosed $177,000 monthly fixed expense is $2.124 million a year before wages, so cash has to cover that before the owner can take meaningful draw.

Here’s the quick math: payroll adds $122 million in Year 1 and $278 million by Year 5, lifting total fixed burden to about $124.124 million and $280.124 million . That is roughly 2.3x growth in payroll load, so higher launch cadence matters only if completed paid missions outpace this burn.

Track Fixed Burn per Completed Launch

Separate fixed overhead from per-mission cost and track fixed overhead per completed paid launch = annual fixed overhead ÷ completed paid launches. Use completed launches, not planned dates, because schedule slips and investigations still consume cash. Cadence helps only when contracts are signed and missions close.

- $177,000 monthly fixed expense

- $122 million Year 1 payroll

- $278 million Year 5 payroll

- Completed paid launches, not planned launches

- Delay days and onboarding days

If onboarding takes longer or a mission slips, the same overhead stays on the books, so owner pay gets pushed out. The clean control is a monthly break-even check against fixed burn, then a cadence plan that matches actual signed work, not the schedule on paper.

5

Reserves And Reinvestment

Reserves First, Draws Second

If you run a micro-satellite launch business, reserves decide when the owner can actually pay themselves. The model needs $19.68 million minimum cash plus $11 million in early capex, so cash is a planning tool, not leftover profit. Until those reserves are funded, distributions can drain the balance sheet and slow recovery after a failed mission, delay, or insurance claim.

That capex includes $5 million for the launch vehicle manufacturing facility, $2 million for the propulsion test stand, $1.5 million for ground support equipment, $1 million for tooling, $750,000 for lab equipment, $500,000 for launch control systems, and $250,000 for IT infrastructure. Here’s the quick math: reserve funding and reinvestment come before owner pay, because they protect future capacity, debt service, and upgrade spend.

Track Cash Before Distributions

Measure minimum cash, capex funded, and cash after each launch cycle. Tie any owner draw to completed paid launches and a reserve floor, not to booked demand or planned launch dates. If you are below the $19.68 million cash target, the safest move is to hold distributions and fund recovery, insurance, and future capacity first.

- Track reserve balance weekly.

- Separate capex from operating cash.

- Stress-test missed-launch scenarios.

- Block draws below reserve floor.

- Reinvest before scaling mission count.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Launch cadence, payload fill, pricing, and direct costs drive owner take-home here. Revenue can rise fast, but cash still gets tied up by staffing, overhead, and capex.

| Scenario | Low CaseDownside | Base CasePlan case | High CaseUpside |

|---|---|---|---|

| Launch model | Launches slip, occupancy lags, and owner take-home stays at funded salary only, if any. | The base case supports the modeled $250,000 CEO salary and some pre-tax owner take-home. | Higher cadence, better utilization, stronger pricing, and lower direct cost rates lift owner take-home. |

| Typical setup | Lower billable days and weak payload fill keep revenue thin, and fixed overhead plus capex pull cash away from the owner. | Year 1 uses 10 billable days, 50.0% occupancy, 500 kg rideshare payload, one dedicated launch unit, and two support packages, with about 80.5% gross margin before fixed costs, $143.9 million EBITDA, $11 million capex, and a $1.968 million minimum cash floor. | Year 5 scale reaches 28 billable days, 90.0% occupancy, 4,000 kg rideshare payload, five dedicated launch units, and 20 support packages, with about 89.5% gross margin before fixed costs. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary onlyNo upside | $250,000 salaryModeled salary | Salary plus distributionsCash upside |

| Best fit | Use this to stress-test delayed missions, weak demand, and cash strain. | Use this as the working plan for lender, board, or investor talks. | Use this to test a full schedule, better margins, and whether revenue turns into cash distributions. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Micro-Satellite Launch Porter's Five Forces Analysis

- Micro-Satellite Launch BCG Matrix

- Micro-Satellite Launch Business Model Canvas

- 7 Critical Financial KPIs for Micro-Satellite Launch

- Micro-Satellite Launch Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Micro-Satellite Launch Profitability

- How Much Does It Cost To Run A Micro-Satellite Launch Business Monthly?

- Micro-Satellite Launch Startup Costs: $13M+ Launch-Readiness Budget

- Micro-Satellite Launch Financial Model Template in Excel

- How To Open A Micro-Satellite Launch Service In 18–36 Months

- How to Write a Micro-Satellite Launch Business Plan

- Micro-Satellite Launch Marketing Mix

- Micro-Satellite Launch Marketing Plan

- Micro-Satellite Launch Business Proposal

- Micro-Satellite Launch PESTEL Analysis

- Micro-Satellite Launch Pitch Deck Example Editable PPTX

- Micro-Satellite Launch Business SWOT Analysis

- Micro-Satellite Launch Value Proposition Canvas

Frequently Asked Questions

A founder may earn little discretionary income during development, while the model includes a $250,000 CEO salary The base case shows Year 1 EBITDA of $143927 million, but EBITDA is company earnings before taxes, debt service, reserves, and reinvestment Owner distributions depend on launch success, backlog, and cash needs