Owner income$185k

Owner income$185kHow Much Can a Microplastic Testing Lab Owner Make by Year 5?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$185k  Net margin9% to 63%

Net margin9% to 63% Revenue for target pay~$2.0M

Revenue for target pay~$2.0M Business difficultyHard

Business difficultyHard

This US planning model shows $1986M revenue and $186K EBITDA in Year 1, rising to $12376M revenue and $7746M EBITDA in Year 5 Owner take-home is not the same as profit: the model includes a $185K Laboratory Director salary, $172M launch capex, a -$971K minimum cash point in Month 6, and a 28-month payback These are planning assumptions, not certified earnings, tax advice, or compensation advice

Owner income$185kNet margin9% to 63%Revenue for target pay~$2.0MBusiness difficultyHardWant to test your owner pay case?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay for a microplastic testing laboratory.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income will vary with revenue, margin, payroll, reserves, and financing.

Want to check owner income in the Microplastic Testing Laboratory model?

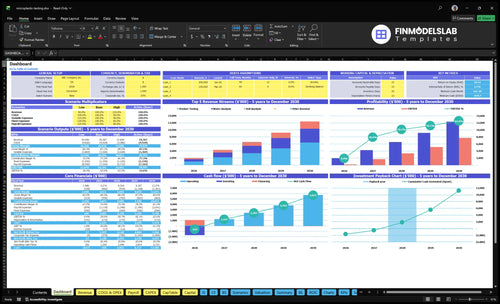

The Microplastic Testing Laboratory Financial Model Template screenshot shows the dashboard, assumptions, cash flow, and owner income scenarios—open it.

Owner-income model highlights

- $1.986M Year 1 revenue

- $12.376M Year 5 revenue

- $186K to $7,746M EBITDA

- $172M startup capex

- -$971K minimum cash

- Month 6 break-even

- 28-month payback

- Charts compare salary, reserves

Is a microplastic testing lab profitable?

Yes, a Microplastic Testing Laboratory can be profitable, but the profit comes from volume, repeat work, and tight lab utilization—not from opening the doors. The base case shows $186K EBITDA on $1.986M revenue in Year 1, and by Year 5 reaches $7.746M EBITDA on $12.376M revenue; track the drivers in What Are The 5 KPI Metrics For Microplastic Testing Laboratory Business?.

Profit Drivers

- Grow paid sample volume

- Keep repeat clients active

- Raise instrument utilization

- Protect pricing power

Cash Risks

- Control labor hours

- Cut variable costs from 27.0% to 17.0%

- Fund $1.72M capex

- Plan for -$971K minimum cash

Can a microplastic testing lab scale?

Yes — a Microplastic Testing Laboratory can scale if capacity, QA/QC, and cash are planned before demand shows up. The owner-operated model saves cash but hides replacement labor, while a technician-supported model adds payroll and lifts throughput; with $22,150 in monthly fixed overhead, recurring clients matter because they spread that load over more billable work. Staff growth can move from 7 FTE in Year 1 to 16 FTE in Year 5.

What makes it scale

- Plan capacity before demand arrives.

- Use technicians to raise throughput.

- Sell recurring clients to spread overhead.

- Track cash for major instruments.

Main bottlenecks

- Sample prep slows the queue.

- Raman spectroscopy limits instrument time.

- FTIR imaging microscopy can bottleneck.

- Py-GC-MS, review, and downtime bite.

How much revenue does a microplastic testing lab need to pay the owner?

To pay the owner, the Microplastic Testing Laboratory needs about $138K in monthly revenue before marketing, debt service, taxes, and reserves. The model should keep the owner as a $185K Laboratory Director salary, not a distribution, and it also carries $22,150 a month in fixed overhead plus about $760K in Year 1 payroll. Here’s the quick math: the direct fixed burden is about $100.9K per month, and at a 73% contribution margin after variable costs, revenue has to reach about $138K a month.

Owner pay setup

- Model the owner as salary first

- Use $185K annual pay

- That is about $15.4K per month

- Keep distributions after fixed costs

Revenue to cover it

- $22,150 monthly fixed overhead before payroll

- $760K Year 1 payroll is about $63.3K per month

- Direct fixed burden totals about $100.9K monthly

- At 73% contribution, need about $138K monthly revenue

Want to see what moves owner income?

1

$1.99M-$12.38MSample Volume

More tests are the main growth engine: revenue climbs from $1.986M in Year 1 to $12.376M in Year 5, and EBITDA rises from $186K to $7.746M.

2

$250-$410/hrAverage Rate

Higher rates matter fast because water analysis starts at $250 per hour and product testing reaches $410, so better pricing lifts owner income.

3

30%-40%Test Mix

Product testing grows from 30% to 40% of the mix, and that shift raises the blended rate because it is the highest-priced service.

4

15-28hUtilization

Billable hours per active customer rise from 15.0 to 28.0 a month, so each account spreads fixed lab cost across more work.

5

$760K-$1.57MLab Labor

Payroll moves from $760K to $1.57M as the team scales, and tighter QA work helps keep the 27% to 17% variable-cost slide on track.

6

$22.2K/moOverhead Load

The fixed stack is $22,150 a month, and the $1.72M build-out keeps cash tight early, so reserves have to protect owner draws.

Microplastic Testing Laboratory Core Six Income Drivers

Paid Sample Volume And Repeat Clients

Paid Sample Volume

This driver is the number of paid billable sample hours from active clients, not inquiries, grants, unpaid research, or validation trials. When billable hours per active customer rise from 150 in Year 1 to 280 in Year 5, revenue per client climbs by 86.7%, so rent, insurance, software, cleanroom utilities, and accreditation costs get spread over more sales.

The income gain shows up in cash and owner pay only if repeat clients keep sending work without breaking turnaround times or QA review. More volume helps margin; rushed volume hurts it. If the lab accepts too much low-value work, rework and client disputes can erase the extra gross profit.

Track Repeat Billable Hours

Track active customers, paid billable hours, repeat rate, CAC, and turnaround time together. Marketing rises from $120K to $220K while CAC falls from $1,500 to $1,000, so the goal is not just more leads; it is more paid hours per customer and fewer one-off accounts.

Set a hard cap on intake when sample prep, instrument use, or QA signoff starts slipping. More volume only helps owner income if every job is billed, reviewed, and delivered on time. Add clients when repeat work is filling idle capacity, not when the lab is already stretched.

1

Average Revenue Per Test

Average Revenue Per Test

Average revenue per test is the price you actually collect for each billed test. In this lab, that lifts owner income when pricing reflects method complexity, reporting depth, urgency, and client value instead of just sample count. The modeled hourly price moves from $250 to $290 for water analysis, $275 to $315 for soil analysis, and $350 to $410 for product testing.

Here’s the tradeoff: higher-priced product work can improve cash, but it often needs more prep and reporting time. If the lab fills capacity with low-cost screening, revenue can look busy while owner pay, equipment reserves, and reinvestment cash stay thin. One-line check: price has to rise faster than labor time.

Price the work, not the sample

Track realized price by test type, then compare it with prep hours, analyst hours, and report time. The input set that matters is simple: test mix, billable hours, rush fees, QA review time, and rerun rate. If product jobs pay $410 but take too much non-billable labor, they may still underperform water tests priced at $290.

- Separate urgent from routine work.

- Price complex methods higher.

- Log prep and reporting time.

- Reject low-margin screening fill.

Use that data to set floor prices that protect gross margin. If the lab keeps selling cheap screening just to stay full, cash gets trapped in payroll and overhead instead of flowing to owner compensation and reserve accounts.

2

Service Mix Complexity

Service Mix Complexity

Mix matters more than headline price. Water, soil, and product testing use different prep, instrument time, QA/QC, and reporting labor, so the same sales dollars can turn into very different gross margin. In the model, water allocation moves from 450% to 550%, soil stays at 250%, and product testing rises from 300% to 400%.

Billable hours also change by job type: water goes from 12 to 16, soil from 10 to 14, and product testing from 20 to 28. That means higher-revenue work can still squeeze profit if validation and reporting take more staff time, which leaves less cash for owner pay.

Track Mix, Not Just Sales

Measure mix by job type, billable hours per job, and QA/QC time. The key inputs are water, soil, and product volume, plus prep labor, instrument time, reporting hours, and validation work. If product testing brings in more revenue but needs heavy review, gross margin can fall even when sales rise.

- Track hours by test type.

- Price heavy validation separately.

- Watch report rework weekly.

- Forecast owner draw after QA.

Use the mix that protects margin, not just the highest ticket. A lab that fills capacity with low-rework jobs usually converts more revenue into cash, and that gives the owner a steadier draw.

3

Utilization And Turnaround Time

Utilization and Turnaround Time

Utilization is the share of available lab hours that turn into billed hours, and turnaround time is the days from sample receipt to signed report. In this lab, the bottlenecks are sample prep, digestion equipment, Raman spectroscopy, FTIR imaging microscopy, Py-GC-MS analysis, data processing, and QA signoff. Better scheduling lifts revenue before you buy another instrument or hire another analyst.

That matters because faster, defensible reports improve cash flow and support owner pay. But speed only helps if QA/QC stays tight; reruns, failed reports, and client disputes can erase margin. With $22,150 in monthly fixed overhead, unbilled time is expensive.

Track Hours, Reruns, and Cycle Time

Use a weekly dashboard for hours available, hours billed, rerun rate, and report cycle time. If cycle time slips, cash comes in later and owner draw gets pushed back. If billed hours rise without more rework, fixed costs spread over more revenue, so take-home income improves.

- Book prep before instrument slots.

- Hold daily QA signoff blocks.

- Split delays by bottleneck step.

- Track reruns by method type.

4

Staffing And QA/QC Costs

Staffing and QA/QC Load

Owner income swings with who is actually doing the work. If the owner runs the lab, sells accounts, or reviews quality assurance/quality control (QA/QC), payroll can stay low for a while, but that is not steady-state profit. The model includes a $185K Laboratory Director, $1 15K senior analytical chemists, $65K lab technicians, $130K data scientists, $95K sales managers, and a $105K QA manager.

Here’s the quick math: payroll rises from $760K in Year 1 to $157M in Year 5. So take-home only improves if billed work grows fast enough to cover replacement labor, QA signoff, and sales coverage. If the owner stops doing these roles without pricing them in, reported profit looks better than cash pay can safely support.

Price in the Replacement Labor

Track owner hours by role: lab leader, QA reviewer, seller, and backfill manager. Then load each role into the forecast at market pay, not zero. If the owner removes one full-time job from the model, replace it with a $185K, $115K, $105K, or $95K cost before raising draws.

Watch rework rate, QA hold time, and billable hours per employee. If QA slows reports, cash gets trapped in work-in-process and owner pay gets delayed. If sales is owner-led, count that as an operating role until a hired manager can keep accounts active on their own.

- Price owner labor at market rates.

- Track QA rework and report delays.

- Replace owner sales before taking draws.

5

Fixed Overhead And Equipment Reserves

Fixed Overhead And Reserves

A microplastic testing lab carries fixed overhead whether it books one sample or one hundred. At $22,150 per month, that is $265,800 a year for rent, utilities, accreditation, liability insurance, software, and office costs, before sample labor or owner pay. More billable work helps spread this load, but weak utilization leaves less cash for distributions.

Here’s the quick math: the plan’s listed equipment items total $1.3M from $350K Raman spectroscopy, $280K FTIR imaging microscopy, $420K Py-GC-MS, and $250K cleanroom construction. With minimum cash at -$971K in Month 6, owner take-home should come only after maintenance, calibration, debt service, and reinvestment reserves are funded.

Pay Yourself After The Reserve

Track monthly burn, instrument service dates, and debt payments in one cash plan. One clean rule: no owner draw until the reserve covers the next 90 days of overhead plus scheduled calibration and repairs.

- Review overhead every month.

- Ring-fence repair cash.

- Track calibration before draws.

- Cut distributions first in slow months.

Use separate buckets for routine maintenance and replacement parts so one failed instrument does not wipe out payroll or owner income. If cash falls near the -$971K low point, preserve operating cash first and delay distributions until the lab rebuilds its reserve.

6

Compare lean, base, and high owner-income cases

Owner income scenarios

These cases show how sample mix, staffing, and cash pressure change owner pay in a lab with heavy fixed costs.

| Scenario | Low CaseOwner-operator | Base CaseStaffed growth | High CaseRecurring-contract lab |

|---|---|---|---|

| Launch model | The owner stays in a lean operator role, but slower sample flow keeps income under pressure. | The model runs at Year 1 scale, with $1.986M revenue, $186k EBITDA, and a $185k lab director salary. | The owner benefits from a larger staffed lab that reaches Year 5 scale and stronger contract flow. |

| Typical setup | Volume is light, variable costs stay high, and fixed lab overhead leaves little room for owner pay. | This is the staffed core case with Month 6 breakeven and a 28-month payback, so owner pay is mostly salary-led. | Revenue reaches $12.376M and EBITDA reaches $7.746M, with about 17% variable cost load supporting higher owner income. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $75,000Tight cash | $185,000 - $250,000Core case | $500,000 - $1,000,000Upside scale |

| Best fit | Use this to stress-test owner pay when volume is slow and cash is tight. | Use this as the core operating plan for budgeting and lender or investor discussions. | Use this to test upside if recurring contracts lift volume and the lab stays fully staffed. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Microplastic Testing Laboratory Porter's Five Forces Analysis

- Microplastic Testing Laboratory BCG Matrix

- Microplastic Testing Laboratory Business Model Canvas

- What Are The 5 KPI Metrics For Microplastic Testing Laboratory Business?

- Microplastic Testing Laboratory Business Plan Template in Pre-Written Word

- How Increase Profits Microplastic Testing Laboratory?

- What Are The Operating Costs For My Microplastic Testing Laboratory?

- Microplastic Testing Laboratory Startup Costs: $172M CAPEX Plan

- Microplastic Testing Laboratory Financial Model Template in Excel

- How To Open A Microplastic Testing Laboratory In 6–12 Months

- How To Write A Business Plan For Microplastic Testing Laboratory?

- Microplastic Testing Laboratory Marketing Mix

- Microplastic Testing Laboratory Marketing Plan

- Microplastic Testing Laboratory Business Proposal

- Microplastic Testing Laboratory PESTEL Analysis

- Microplastic Testing Laboratory Pitch Deck Example Editable PPTX

- Microplastic Testing Laboratory Business SWOT Analysis

- Microplastic Testing Laboratory Value Proposition Canvas

Frequently Asked Questions

The model supports a $185K Laboratory Director salary if the owner fills that role, but distributions depend on cash flow Year 1 EBITDA is $186K on $1986M revenue, so extra owner cash is limited after reserves By Year 5, EBITDA reaches $7746M on $12376M revenue before taxes, debt service, depreciation, and owner distribution decisions