Owner incomeUp to $1.82M

Owner incomeUp to $1.82MMini Pile Underpinning Owner Income On $284M Year 1 Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeUp to $1.82M  Net margin64.1%

Net margin64.1% Revenue for target pay$2.84M

Revenue for target pay$2.84M Business difficultyHard

Business difficultyHard

This page estimates mini pile underpinning business revenue, foundation underpinning business profit, and what can flow to the owner over the five-year model period The supplied model shows $2838M in first-year revenue, 707% contribution after listed direct and variable costs, and $15,650 in monthly fixed overhead It separates revenue, profit pool, reserves, and owner compensation it does not cover employee wage benchmarking, taxes, or guaranteed distributions

Owner incomeUp to $1.82MNet margin64.1%Revenue for target pay$2.84MBusiness difficultyHardWant to test your owner pay case?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Mini Pile Foundation Underpinning model?

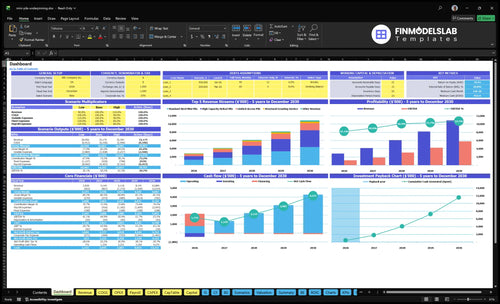

The screenshot shows revenue, unit pricing, job costing, crew capacity, overhead, reserves, and owner take-home assumptions in the Mini Pile Foundation Underpinning Financial Model Template. It also ties the $2838M first-year revenue, 707% contribution margin, $15,650 monthly overhead, and $1818M pre-payroll profit pool, so open the model for the full income view.

Owner-income model highlights

- Owner take-home shown clearly

- Revenue and margin linked

- Scenarios test assumptions fast

How much revenue does a mini pile underpinning business need to pay the owner?

For a Mini Pile Foundation Underpinning business, the owner-pay target should be backed into from revenue, not copied from a generic sales rule. Using the supplied 70.7% contribution margin, every $100,000 of owner pay needs about $141,000 of contribution-backed revenue before fixed overhead, field payroll, debt service, and reserves. The first-year model shows $2.838M of revenue, but true owner pay still depends on the missing labor and financing schedule, and taxes are excluded.

Revenue math

- Start with the owner pay target.

- Add fixed overhead and field payroll.

- Add debt service and reserves.

- Divide by 70.7% margin.

Pay reality

- $100k pay needs about $141k revenue.

- $2.838M is the first-year model.

- Labor schedule changes owner take-home.

- Financing schedule changes owner take-home.

What affects profit margin in mini pile underpinning?

Profit margin in Mini Pile Foundation Underpinning moves with pile depth, pile type, site access, soil testing, engineering review, crew hours, spoil handling, mobilization, rework, and change-order control; for a cost view, see What Are Operating Costs For Mini Pile Foundation Underpinning?. Limited-access work can still look good on price, but it adds 9% site costs plus $350 in unit materials. A 1-point margin shift can change the owner profit pool by about $284k.

Big margin drivers

- Pile depth drives labor and material use.

- Pile type changes install time.

- Soil testing can add upfront cost.

- Engineering review adds professional fees.

Margin leak points

- Site access can add 9% site cost.

- Mobilization hurts small jobs.

- Rework cuts gross margin fast.

- Change orders protect profit if controlled.

Can a mini pile underpinning business support a full-time owner?

Yes, a Mini Pile Foundation Underpinning business can support a full-time owner, but only after field payroll, debt service, taxes, warranty reserves, and reinvestment fit inside the profit pool; see How Much To Start Mini Pile Foundation Underpinning Business? for the startup cost side. Here’s the quick math: $2.838M revenue, $2.006M contribution, and $1.878M listed fixed overhead leave about $128k before unprovided payroll and reserves.

Owner Pay Test

- 70.7% contribution margin

- $2.657M listed overhead break-even

- $128k profit pool before gaps

- Salary means planned payroll

Cash Risk

- Distributions are profit withdrawals

- Retained cash stays inside the business

- Downtime cuts reliable owner pay

- Permit delays stretch job cash flow

Want to see what really drives owner income?

1

$2.84MLead Flow

Year 1 revenue starts at $2.838M, so more qualified leads fill the schedule and lift owner take-home first.

2

$3.4KProject Value

The pile mix averages about $3,397 per pile, so more high-value work pushes revenue up without adding as many jobs.

3

5.0xCrew Use

Field technician capacity rises from 2 FTE to 10 FTE, so every idle crew hour hurts cash.

4

$284K/ptJob Costs

A one-point margin swing moves about $284K of owner take-home, so labor waste and rework go straight to income.

5

8%Mobilization

Transport, fuel, cleanup, and site setup costs stack fast, so tight routing and staging protect the job margin.

6

$15.65KOwner Scale

Fixed overhead is $15,650 a month, so owner time has to shift from field work to estimating and control.

Mini Pile Foundation Underpinning Core Six Income Drivers

Qualified lead flow

Qualified Lead Flow

Lead count only helps when the calls are real structural repair jobs. Here, the useful inputs are engineer referrals, urgent settlement issues, and qualified inspections, because those leads close faster and tend to turn into larger pile work. The first-year model assumes 80 foundation inspections at $1,200 each, or $96,000 in inspection revenue.

Here’s the risk: unqualified homeowner calls can burn estimating time without producing work. That hurts owner income twice, because sales hours replace production hours and cash does not come in unless the job closes. A useful one-liner: more inspections only matter if they lead to proposals and contracts.

Track Lead Quality, Not Just Volume

Measure inspection-to-proposal rate, proposal-to-contract rate, average days to approval, and revenue booked per inspection. Those four numbers show whether lead flow is feeding profitable work or just creating busywork. If the team spends too long on bad leads, gross margin and owner pay both slip because labor gets spent before revenue lands.

Use a simple filter before scheduling: engineer referral, visible settlement damage, or pre-sale structural need. Track which source converts best, then spend more time there. If inspections convert into larger pile jobs, lead flow supports cash flow and steadier production; if not, it becomes a drain on estimating and collections.

- Track source before booking.

- Reject vague homeowner calls.

- Log approval lag in days.

- Compare booked revenue per inspection.

1

Average project value

Average Project Value

Average project value is the average revenue per underpinning job, and it rises when the mix shifts toward more piles, deeper installs, harder access, and better mobilization fees. In this model, pile revenue totals $2.616M across 770 piles, or about $3,397 per pile. First-year prices are $2,800 for standard steel mini piles, $4,500 for high capacity helical piles, and $3,800 for limited access piles.

Higher ticket jobs can improve gross profit and owner pay, but only if added work is priced in. Small tight-access jobs can look strong on paper and still lose margin after transport, setup, and protection materials. The real inputs are pile count, pile type, depth, access, and mobilization value. If change orders are weak, revenue rises slower than crew effort and cash gets squeezed.

Price The Job, Not Just The Piles

Track average revenue per pile, mobilization per job, and gross margin by access type. Here’s the quick math: if a limited-access job needs more setup, protection, or travel, the quoted price must cover that before labor starts. Price mobilization and change orders clearly, or you end up with busy crews and thin owner draw.

Test quotes against the mix that pays best: standard steel at $2,800, helical at $4,500, and limited access at $3,800. The goal is simple: lift average contract value without letting field costs outrun the ticket. What this estimate hides is rework risk, so lock scope in writing before the crew rolls.

2

Crew utilization

Crew utilization

Crew utilization is the share of scheduled production days that turn into installed piles, inspections, and grouting. In mini pile work, days can be lost to weather, inspections, engineering approvals, permit coordination, equipment moves, and site readiness. If those days slip, the business books less revenue per crew day, and the $15,650 monthly fixed overhead stays uncovered.

First-year volume averages about 64 piles per month plus inspections and grouting, so every idle day matters. The owner should watch installed piles per crew day, downtime days, backlog, and revenue per production day; if utilization is high but supervision is weak, rework and warranty claims can eat the take-home draw.

Protect production days

Track the schedule in one view: sold work, approved work, and ready-to-install work. The goal is to keep field time tied to paid work, not waiting on permits or site prep. One clean metric beats a busy calendar.

Use a simple daily log and price around real field loss. Measure installed piles per crew day, downtime days, backlog, and revenue per production day. If a job is not ready, push it before the crew rolls, so labor, equipment, and overhead stay on productive work.

- Count paid crew days each week

- Record lost days by cause

- Review backlog before mobilizing

- Check rework and warranty risk

3

Job cost control

Job Cost Control

On mini pile underpinning jobs, profit lives or dies on how tightly you hold labor hours, steel, grout, couplers, drive head wear parts, drill bits, engineering review, soil testing, cleanup, subcontractors, and rework. First-year listed product and site costs are about $5,626k before selling and payment fees, so even small waste hits owner pay fast.

Here’s the quick math: every 1-point miss in margin changes the owner pool by about $284k on first-year revenue. That means cost creep, especially from rework and scope drift, can wipe out cash that should pay debt, overhead, and the owner’s draw.

Control Scope Drift

Use written scopes, field photos, daily cost logs, and signed change orders before work expands. Track planned vs actual labor hours, material use, and rework on every job, then review them at closeout. If the job changes but the paper doesn’t, margin leaks straight into the owner’s income.

- Track cost per pile installed.

- Log change orders the same day.

- Price extra access and cleanup.

What this estimate hides: unbilled engineering time, small site losses, and late fixes can stack up fast. Tight job costing protects cash flow, keeps contribution closer to plan, and makes owner pay less dependent on one good month.

4

Equipment and mobilization economics

Equipment Cash First

Mini pile underpinning can show good accounting profit and still squeeze cash. On the listed equipment lines, fuel and lubricants are 20%, heavy equipment transport is 25%, specialized rig maintenance is 15%, and equipment calibration is 10% where needed. That is 70% of these buckets before owner pay. Owner income comes after maintenance reserves, move costs, and loan payments.

What this hides: owned rigs need repair reserves, rented rigs need strong utilization, and financed rigs need debt service coverage. Book depreciation is not cash for repairs or principal. If transport days rise or a rig sits idle, the paycheck gets hit fast even when the job still looks profitable on paper.

Track Cash by Rig and Move

Measure equipment cash by job, not just by month. Here’s the quick math: if $10,000 of job cost sits in these equipment buckets, $7,000 is already spoken for in fuel, transport, maintenance, and calibration. That makes owner draw a leftover, not a starting point.

- Track move cost per mobilization.

- Track idle days per rig.

- Set a maintenance reserve rate.

- Check debt coverage before paying out.

Use separate cash targets for owned, rented, and financed rigs. Owned rigs need a repair reserve. Rented rigs need high utilization. Financed rigs need enough project cash to cover principal and interest before any draw.

5

Owner role and overhead

Owner Role and Overhead

Owner labor can save payroll, but it is not free. In a mini pile underpinning shop, every hour in the field steals time from sales, estimating, project management, collections, and engineer coordination, which can slow booked work and cash in the door. The fixed overhead is $15,650 per month, so the owner has to cover that before paying themselves.

The real test is profit after replacement labor. Compare owner-in-field, owner-manager, and multi-crew setups by the extra payroll they need and the revenue they unlock. If a manager or estimator keeps crews full and shortens approval cycles, profit can rise; if not, the added wage just lowers owner take-home.

Track Owner Time by Role

Split the owner’s week into field labor, estimating, sales, collections, and engineer follow-up. Then watch proposal rate, days to approval, and revenue booked per owner hour. One clean rule: if field time is blocking closed work, the owner is the bottleneck, not the fix.

- Track owner hours by task.

- Measure booked work per hour.

- Test manager pay against added output.

- Compare profit after replacement labor.

Use the same job mix when you model each case. Subtract replacement labor from gross profit, then compare the result to the $15,650 monthly overhead. If the added payroll does not produce more sold work, faster collections, or better crew utilization, the owner should stay tightly focused on the highest-value tasks.

6

Compare low, base, and high owner income scenarios

Owner income scenarios

Owner income moves with job mix, pricing, and fixed overhead. Low, base, and high cases show how much cash is left before payroll, debt, taxes, and retained cash.

| Scenario | Low CaseLow | Base CaseBase | High CaseHigh |

|---|---|---|---|

| Launch model | This is the lower earnings path built from the first operating year. | This is the modeled middle path built from Year 3 operating levels. | This is the stronger earnings path built from Year 5 scale. |

| Typical setup | About 910 jobs and units at a weighted average price near $3,116, with a 70.7% contribution profile, $1.878M fixed overhead, and a $1.818M pre-payroll pool before payroll, debt, taxes, and retained cash. | About 1,800 jobs and units at a weighted average price near $3,399, with a 72.8% contribution profile, $4.268M fixed overhead, and a $4.268M pre-payroll pool before payroll, debt, taxes, and retained cash. | About 2,980 jobs and units at a weighted average price near $3,650, with a 74.4% contribution profile, $7.915M fixed overhead, and a $7.915M pre-payroll pool before payroll, debt, taxes, and retained cash. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $1.818MConservative pool | $4.268MModeled pool | $7.915MUpside pool |

| Best fit | Use this if you want a downside check for a smaller launch year and tighter crew utilization. | Use this as the core planning case for steady demand, fuller crews, and normal field execution. | Use this to test what happens if the shop reaches higher volume and keeps pricing firm while capacity expands. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Mini Pile Foundation Underpinning Porter's Five Forces Analysis

- Mini Pile Foundation Underpinning BCG Matrix

- Mini Pile Foundation Underpinning Business Model Canvas

- How Increase Mini Pile Foundation Underpinning Profitability?

- Mini Pile Foundation Underpinning Business Plan Template in Pre-Written Word

- How Increase Mini Pile Foundation Underpinning Profitability?

- What Are Operating Costs For Mini Pile Foundation Underpinning?

- Mini Pile Foundation Underpinning Startup Costs For Year 1

- Mini Pile Foundation Underpinning Financial Model Template in Excel

- Open A Mini Pile Underpinning Business In 90 To 180 Days

- How To Write A Business Plan For Mini Pile Foundation Underpinning?

- Mini Pile Foundation Underpinning Marketing Mix

- Mini Pile Foundation Underpinning Marketing Plan

- Mini Pile Foundation Underpinning Business Proposal

- Mini Pile Foundation Underpinning PESTEL Analysis

- Mini Pile Foundation Underpinning Pitch Deck Example Editable PPTX

- Mini Pile Foundation Underpinning Business SWOT Analysis

- Mini Pile Foundation Underpinning Value Proposition Canvas

Frequently Asked Questions

Hold enough cash for fixed overhead, job costs, and slow collections The supplied model has $15,650 in monthly fixed overhead, about $832k in first-year listed direct and variable costs, and $2365k in average monthly revenue Payroll, debt service, warranty claims, and tax payments are not included, so working capital should be set after those schedules are added