Owner income$127K/mo

Owner income$127K/moMini Trampoline Fitness Studio Owner Income: $127K/Month EBITDA Case

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$127K/mo  Net margin71% to 87%

Net margin71% to 87% Revenue for target pay$2.15M

Revenue for target pay$2.15M Business difficultyMedium

Business difficultyMedium

You’re trying to see whether class volume can pay you, not just cover rent This five-year US mini trampoline fitness studio model shows $2149M Year 1 revenue, $1527M Year 1 EBITDA, and the path from revenue to owner take-home before personal taxes, reserves, debt service, and distributions

Owner income$127K/moNet margin71% to 87%Revenue for target pay$2.15MBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. It also excludes personal taxes and your household budget.

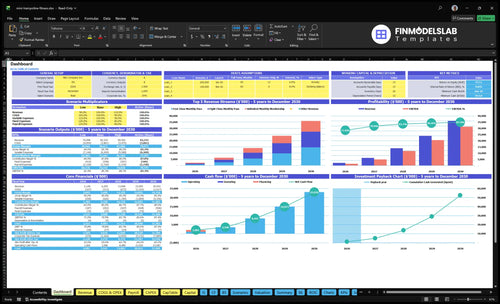

How do I check owner income in the Mini Trampoline Fitness Studio model?

This screenshot shows revenue, margin, costs, reserves, and take-home assumptions. Open the Mini Trampoline Fitness Studio Financial Model Template.

Owner-income model highlights

- Dashboard and income outputs

- Capacity, memberships, cash flow

- Scenario tests on pricing

Are memberships or drop-ins better for a mini trampoline fitness studio?

For a Mini Trampoline Fitness Studio, memberships are the safer base because they bring cash in before each class fills. In the model, Year 1 recurring revenue is about $38,000 a month from 80 unlimited members at $180, 100 eight-class passes at $140, and 120 four-class passes at $80. By Year 5, that rises to about $123,000 a month, so drop-ins and class packs should be the add-on, not the core.

Memberships first

- Year 1 recurring revenue: $38,000/month

- Year 5 recurring revenue: $123,000/month

- Cash lands before classes fill

- Helps cover fixed overhead early each month

Drop-ins as add-on

- Can lift revenue per visit

- Class packs widen buyer choice

- Retention risk matters more with one-off visits

- Use them after recurring revenue is stable

How much revenue does a mini trampoline fitness studio need to pay the owner?

A Mini Trampoline Fitness Studio doesn’t need owner-pay revenue just to break even; it needs enough cash left after payroll, rent, marketing, fees, cleaning, reserves, and debt service. In this model, plan around $179K/month in Year 1 revenue, with $127K/month EBITDA, before setting a meaningful owner draw; see What Are Operating Costs For Mini Trampoline Fitness Studio? for the operating-cost base.

Revenue Target

- Year 1 revenue: $2.149M

- Monthly revenue: about $179K

- Break-even: Month 1

- Owner pay starts after cash coverage

Pay Check

- Year 1 EBITDA: $1.527M

- Monthly EBITDA: about $127K

- Payroll: $162K/year

- Facility costs: $5,820/month

What are the biggest costs for a mini trampoline fitness studio?

The biggest costs in a Mini Trampoline Fitness Studio are payroll, rent, and marketing, plus occupancy shortfalls that cut cash when classes don’t fill. If you’re mapping startup spend, see How Much To Launch Mini Trampoline Fitness Studio? Year 1 wages total $162K, rent is $4,500 a month, and another $1,320 a month goes to utilities, software, music licensing, insurance, internet, and phone.

Fixed Cost Drivers

- $162K Year 1 wages total

- $4,500 monthly rent

- $1,320 monthly utilities and overhead

- Occupancy shortfalls hit take-home pay

Variable and Startup Costs

- Digital marketing can be 100% of Year 1 revenue

- Processing fees take 30%

- Cleaning supplies take 20%

- Rebounder fleet capex is $15K

Want to see what moves owner income most?

1

45%-85%Class Fill

Filling more spots lifts sales fast, because empty rebounder seats leave money on the table.

2

26-30dBillable Days

More billable days per month raise class volume without adding much new fixed cost.

3

$180-$200Plan Mix

A better split across unlimited and class passes pushes average revenue per member higher.

4

$162KPayroll Load

Keeping instructor payroll tight protects EBITDA as class load and staffing grow.

5

$5.82K/moFixed Overhead

Monthly rent, utilities, software, and insurance must stay controlled or sales gains get diluted.

6

80-350Repeat Rate

Growing member counts across the three plans steadies cash flow and cuts lead pressure.

Mini Trampoline Fitness Studio Core Six Income Drivers

Paid Class Occupancy

Paid Class Occupancy

Paid class occupancy is the share of available rebounding spots that turn into paid visits. Once instructor and room costs are covered, every extra paid spot spreads the studio’s $5,820 monthly facility cost across more visits, so EBITDA and owner draw improve. The model’s occupancy rises from 450% in Year 1 to 850% in Year 5, which means the business is built on better fill, not just more classes.

The trap is counting inquiries or booked slots as revenue. Use paid attendance, not interest, to forecast cash. Track booked spots, attended spots, no-shows, and waitlist conversion; if attendance slips, fixed costs stay put and owner take-home gets squeezed even when demand looks strong.

Measure Paid Fill

Measure occupancy as paid spots ÷ class capacity, then compare it by class time. Here’s the quick math: more filled spots mean the same rent, software, insurance, and front-desk costs are spread over more visits, so margin rises without raising payroll at the same pace.

- Track booked spots versus attended spots.

- Separate no-shows from true empty seats.

- Measure waitlist-to-paid conversion.

- Compare fill by morning, evening, weekend.

1

Class Schedule Capacity

Class Schedule Capacity

For a mini trampoline fitness studio, class schedule capacity is the hard cap on revenue in the same leased space model. When billable days move from 26 per month in Years 1 and 2 to 30 per month in Years 4 and 5, the studio can sell more class slots, but only if demand and instructor coverage keep up.

The key inputs are classes scheduled, classes filled, peak-time utilization, and instructor coverage. Morning, evening, weekend, and off-peak slots can raise income, but weak off-peak turnout can dilute margin because fixed rent and staffing stay in place while paid spots do not.

Track Slot Fill, Not Just Slot Count

Watch scheduled classes versus filled classes every week. A fuller schedule only helps owner pay if the added sessions are paid, not just open. One clean rule: more time slots should raise cash, not just workload.

Use a simple scorecard: classes filled, instructor coverage, peak-time utilization, and off-peak attendance. If off-peak classes stay thin, cut them back and move capacity into higher-demand hours. That protects gross margin and keeps more revenue left after payroll and rent.

- Track fill rate by class time

- Compare peak and off-peak demand

- Match staffing to booked demand

- Drop weak classes fast

2

Pricing And Membership Mix

Membership Mix Sets Cash Stability

Pricing and membership mix decide both average revenue per visit and how steady monthly cash feels. In Year 1, the $140 eight-class plan equals $17.50 per visit and the $80 four-class plan equals $20 per visit. By Year 5, those move to $160 and $100, which lifts revenue if demand holds. Unlimited at $180 to $200 only works if members actually use it.

If the mix tilts too far toward heavy unlimited users, revenue per visit can fall even when classes look full. Recurring memberships help owner pay because cash is more predictable than one-off sales, but the studio still needs enough retention and visit frequency to keep the math clean. Drop-ins, class packs, and private events can add revenue, but only if local demand supports the price.

Track Visits Before You Raise Prices

Watch intro-offer conversion, visits per member, and renewal rate by tier. Here’s the quick math: if eight-class members are visiting fewer than eight times, the effective price per visit goes up; if unlimited members visit often, you may need higher prices or better retention to protect margin. That’s the lever on owner take-home.

- Split revenue by membership tier.

- Check visits per member weekly.

- Test price changes on new signups.

- Keep private events margin-positive.

3

Instructor Payroll Efficiency

Instructor Payroll Efficiency

For a mini trampoline studio, payroll can protect owner pay or eat it fast. Year 1 payroll is $162K and includes four roles; by Year 5, staffing rises to one manager, two lead instructors, five junior instructors, and 25 front desk FTEs (full-time equivalents), so labor has to grow only with real class demand.

The key check is payroll as a percentage of revenue, plus classes per instructor, attendance per labor hour, and missed-class coverage. Owner-taught classes can cut cash wages, but they do not remove true labor cost, because the owner’s time is still labor. If coverage rises faster than paid attendance, gross margin falls and take-home income gets squeezed.

Keep Labor Tied to Filled Spots

Track booked spots, attended spots, no-shows, and the labor hours behind each class. Here’s the quick math: labor cost per attended class equals instructor pay plus front-desk coverage, divided by attended spots. If a class runs light, the same wage bill buys less revenue, so the studio needs fuller classes, better prices, or fewer weak time slots.

Set staffing rules from demand, not habit. Test how many classes one instructor can cover before quality slips, then use owner-taught sessions only where they protect margin. Keep a coverage log for sick days and swaps; missed-class coverage can force overtime or extra front-desk hours. Tight control here makes monthly profit steadier and leaves more cash for owner pay.

4

Fixed Overhead Control

Fixed Overhead Hurdle

Fixed overhead is the monthly bill you pay before one class fills and before owner pay starts. Here that base is $5,820 per month: $4,500 rent, $600 utilities, $250 booking software, $150 music licensing, $200 insurance, and $120 internet and phone.

That is $69,840 a year before payroll. Add reserves for worn gear: $15K rebounders, $8K audio, $12K flooring and mirrors, and $5K lobby furniture for $40K total. If fixed cost creeps up, break-even attendance rises and the owner’s draw gets pushed back.

Keep the Monthly Hurdle Low

Track the fixed bill monthly, not just at lease signing. If rent, software, and insurance rise by even $500, the studio needs $6,000 more cash a year before owner pay. The quick test is simple: compare booked paid spots against the fixed cost wall, not against inquiries or likes.

Build a reserve for replacement, then stick to it. Rebounders, audio, flooring, and lobby gear wear out, and that cash gap can hit when attendance softens. Keep a rolling reserve and review fixed spend each month so higher overhead does not force discounting, unsafe load levels, or skipped owner draws.

5

Retention And Repeat Attendance

Retention And Repeat Attendance

When members keep coming back, the studio spends less to replace them, so more revenue turns into cash the owner can take home. Here, marketing starts at 100% of revenue in Year 1 and falls to 50% by Year 5, so retention is a direct profit lever.

Repeat attendance also supports the move from 80 to 200 unlimited members, 100 to 300 eight-class members, and 120 to 350 four-class members. Track churn, renewal rate, visits per member, intro-offer conversion, and inactive accounts so growth comes from loyalty, not constant replacement sales.

Measure Renewals, Not Just Sign-Ups

Watch the full path: intro-offer conversion, first 30-day visits, renewal rate, and inactive accounts. If intro offers convert but visits fade fast, retention is leaking and marketing will stay heavy. Better retention raises lifetime value and lowers acquisition cost, which improves owner pay.

A simple rule: if visit frequency falls, react before churn shows up in revenue. Build weekly reports for booked visits, attended visits, no-shows, and renewals, then follow up with members who miss two straight weeks.

- Track churn by membership tier.

- Flag inactive accounts every week.

- Measure visits per member monthly.

- Test reminders after missed classes.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income changes with class fill, membership mix, and staffing. The low case assumes slower retention and higher marketing, while the high case reflects mature-year demand and fuller classes.

| Scenario | Low CaseDownside case | Base CaseBase case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is a weaker launch where classes fill slowly and owner draw stays tight. | This is the modeled path with steady class fill and normal owner draw. | This is a stronger mature-year path with fuller classes and a much higher owner draw. |

| Typical setup | Use slower occupancy than 45.0%, lower retention, higher marketing, and tighter reserves; rent stays at $4,500 a month and payroll stays heavy early. | Use 45.0% occupancy, 26 billable days, 80 unlimited members, 100 eight-class passes, and 120 four-class passes; revenue is $2.149M and EBITDA is $1.527M. | Use 85.0% occupancy, 30 billable days, 200 unlimited members, 300 eight-class passes, and 350 four-class passes; revenue reaches $35.935M and EBITDA reaches $31.406M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Thin owner drawLow income | $1.53MModeled income | $31.41MUpside income |

| Best fit | Use this to stress-test a slow start, soft repeat visits, and early cash pressure. | Use this as the main planning case for staffing, rent, and cash flow. | Use this to test upside, but don't treat it as the normal run rate. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Mini Trampoline Fitness Studio Porter's Five Forces Analysis

- Mini Trampoline Fitness Studio BCG Matrix

- Mini Trampoline Fitness Studio Business Model Canvas

- What 5 KPIs Should Mini Trampoline Fitness Studio Business Track?

- Mini Trampoline Fitness Studio Business Plan Template in Pre-Written Word

- How Increase Mini Trampoline Fitness Studio Profits?

- What Are Operating Costs For Mini Trampoline Fitness Studio?

- Mini Trampoline Fitness Studio Startup Costs: $913K Funding Plan

- Mini Trampoline Fitness Studio Financial Model Template in Excel

- How To Open A Mini Trampoline Fitness Studio In 8–16 Weeks

- How To Write A Business Plan For Mini Trampoline Fitness Studio?

- Mini Trampoline Fitness Studio Marketing Mix

- Mini Trampoline Fitness Studio Marketing Plan

- Mini Trampoline Fitness Studio Business Proposal

- Mini Trampoline Fitness Studio PESTEL Analysis

- Mini Trampoline Fitness Studio Pitch Deck Example Editable PPTX

- Mini Trampoline Fitness Studio Business SWOT Analysis

- Mini Trampoline Fitness Studio Value Proposition Canvas

Frequently Asked Questions

The researched base case shows about $127K per month in Year 1 EBITDA, based on $2149M revenue and $1527M EBITDA That is not the same as guaranteed owner salary Owner take-home still depends on cash reserves, debt service, reinvestment, personal taxes, and whether the owner leaves cash inside the business